In-app Advertising Market Report Scope & Overview:

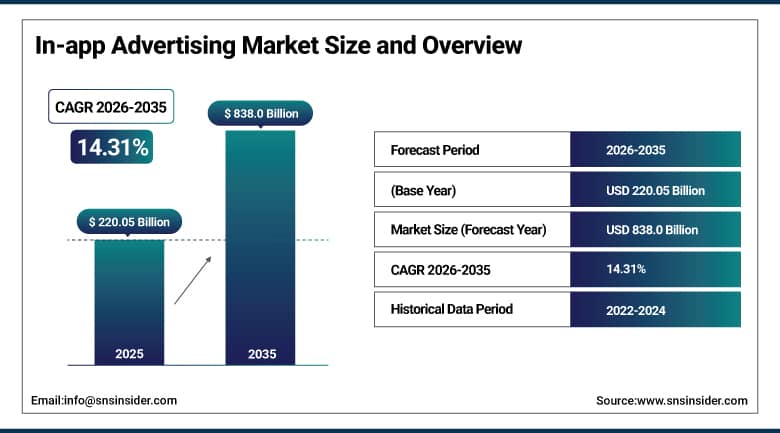

In-app Advertising Market was valued at USD 220.05 billion in 2025 and is expected to reach USD 838.0 billion by 2035, growing at a CAGR of 14.31% from 2026-2035.

In-app advertisements have become popular as a result of increasing penetration of smartphones, use of mobile applications, and consumption of online content. Targeting made more sophisticated by artificial intelligence and data analytics makes in-app ads more effective. The expansion in popularity of gaming and social media apps and also the presence of programmatic advertising make the industry grow even faster.

The U.S. Interactive Advertising Bureau (IAB) reports that mobile advertising now accounts for over 65% of total digital advertising revenue in the United States. The FTC's ongoing review of mobile advertising data practices under consumer privacy frameworks is shaping how targeting data can be collected and used across U.S. mobile advertising ecosystems.

In-app Advertising Market Size and Forecast

-

Market Size in 2025: USD 220.05 Billion

-

Market Size by 2035: USD 838.0 Billion

-

CAGR: 14.31% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On In-app Advertising Market - Request Free Sample Report

In-app Advertising Market Trends

-

Programmatic real-time bidding now accounts for the majority of in-app ad inventory transactions globally, with AI-driven demand-side platform optimization continuously improving bidding efficiency and return on ad spend.

-

Rewarded video ads where users voluntarily watch an ad in exchange for in-game currency or content access have become the highest-performing in-app ad format across gaming and entertainment categories for both engagement and conversion.

-

CTV and gaming app crossover is growing as streaming platforms develop companion apps and gaming platforms expand into streaming, blurring the entertainment category boundaries where in-app advertising operates.

-

Privacy-preserving advertising technologies including Apple's SKAdNetwork, Google's Privacy Sandbox for Android, and cohort-based targeting are replacing individual device-level tracking with privacy-compliant alternatives that maintain advertiser targeting capability.

-

Native advertising formats that match app UI aesthetics are outperforming traditional banner and interstitial formats on click-through and conversion rates, driving format mix shift toward premium native placements.

-

AR-powered interactive ad formats enabling virtual product try-on, brand experiences, and gamified brand interactions are moving from experimental to mainstream among premium brand advertisers.

-

Social commerce integration where in-app ads link directly to checkout flows without leaving the social app is creating new in-app advertising revenue streams as platforms monetize commercial intent within social engagement.

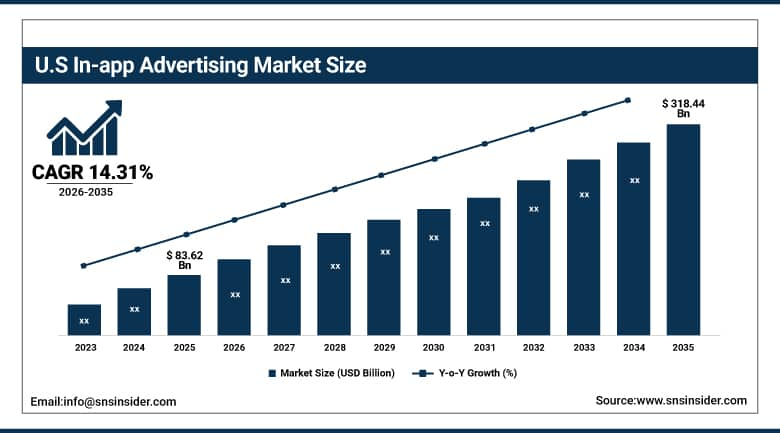

U.S. In-app Advertising Market was valued at USD 83.62 billion in 2025 and is expected to reach USD 318.44 billion by 2035, growing at a CAGR of 14.31% from 2026-2035.

There is an increase in the U.S in-app advertising market because there is extensive use of smartphones and mobile apps among users. Moreover, the existence of leading technology companies, along with digital infrastructure, programmatic ads, and audience targeting, also contributes to its growth.

The IAB's 2024 Internet Advertising Revenue Report documents that U.S. digital advertising revenue reached USD 225 billion, with mobile representing over 65% of total digital ad spend. The FTC's enforcement actions against dark patterns in mobile advertising have raised compliance expectations for in-app ad disclosure and consent mechanisms.

In-app Advertising Market Segment Analysis

-

By Platform, Android dominated the In-app Advertising Market with 70%+ share in 2025; iOS fastest growing (CAGR) with higher ad engagement rates.

-

By Application, Gaming segment dominated the In-app Advertising Market in 2025; Social and Entertainment fastest growing (CAGR).

-

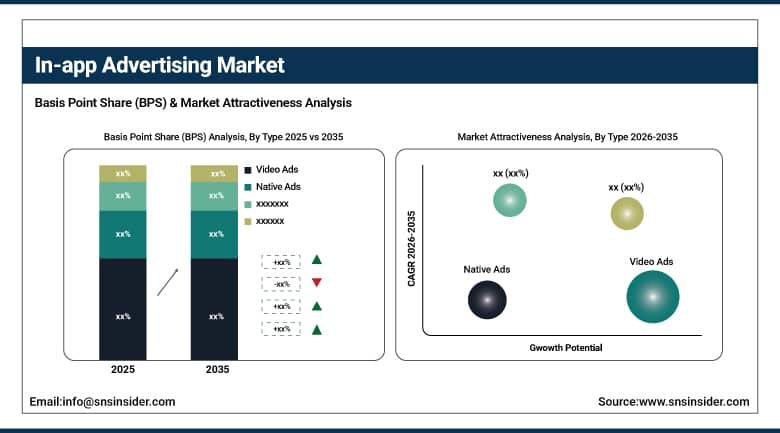

By Type, Video Ads dominated the In-app Advertising Market in 2025; Native Ads and Rewarded Ads fastest growing (CAGR).

By Type, Video ads segment dominates the In-app Advertising Market, native ads to grow fastest

Video ads continued to dominate the in-app advertising market in 2025 due to their strong engagement rates, immersive storytelling ability, and higher CPM performance compared to other formats. Their ability to capture user attention through short-form and rewarded video formats has made them the preferred choice for advertisers across gaming, social, and entertainment apps.

Meanwhile, native ads and rewarded ads are emerging as the fastest-growing segments, driven by their non-intrusive integration within app content and value-exchange model. Native ads benefit from seamless user experience and contextual relevance, while rewarded ads drive higher user opt-in and engagement, supporting strong CAGR growth.

By Platform, Android segment dominates the In-app Advertising Market, iOS expected to grow fastest

The Android platform had the highest share of platform revenues in the In-app Advertising Market in 2025 owing to its leading position in the global market share, which accounted for more than 70% of all smartphones worldwide. The presence of the Google Play Store, where billions of applications of different genres like games, social networks, entertainment applications, utility applications, and shopping applications are installed, allows for achieving maximum reach from one mobile operating system alone.

It is estimated that iOS will witness the highest CAGR for any platform due to the high purchasing capability of the iOS consumer base, higher engagement with applications, and higher revenue per user. Although Apple’s ATT framework has limited the level of microtargeting on iOS platforms, the quality of the iOS user base in terms of income levels, higher conversion rates, and engagement levels supports premium prices.

By Application, Gaming segment dominates the In-app Advertising Market, Social segment growing fastest

The Gaming application category continued to hold the largest market share in the In-app Advertising Market in 2025 by earning the highest revenue from in-app advertisements due to its massive scale of usage, high frequency of sessions, prolonged durations of sessions, and the distinct in-game advertising formats of rewarded videos, playable advertisements, and interstitials. There are millions of mobile game users on a daily basis all around the world, and the advertisement-based free play business model ensures that the game earns money mainly through ads as opposed to in addition to other methods.

Social applications are growing at the fastest application CAGR as social commerce, short-form video, and in-app shopping features create new advertising inventory types and higher-value advertising moments within social environments. TikTok's advertising business built on a foundation of high-engagement short-form video with strong influencer and brand marketing presence is the most visible example of how social app advertising revenue can grow from zero to tens of billions of dollars within a short timeframe. Instagram's shopping features, Pinterest's visual commerce advertising, and Snapchat's augmented reality advertising formats each represent premium in-app advertising environments where creative formats command significantly higher CPMs than standard banner or interstitial inventory.

In-app Advertising Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

89% |

|

Asia Pacific |

China |

48% |

|

Europe |

United Kingdom |

22% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

50% |

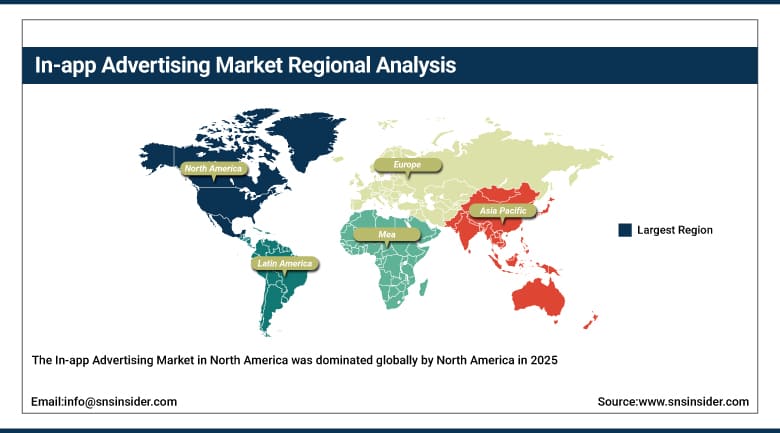

North America In-app Advertising Market Insights

The In-app Advertising Market in North America was dominated globally by North America in 2025, owing to its dominance as the most commercially mature market for programmatic advertising in the world, high advertiser expenditure density, and being the host region for the dominant players in in-app advertising technology such as Meta, Google, Apple, and Amazon. The maturity of the U.S. market implies that growth will be more about increasing spending per impression and innovation in ad formats rather than audience acquisition, making programmatic optimization, creative excellence, and first-party data utilization critical competitive fronts.

eMarketer projects total U.S. mobile advertising spend will reach USD 190 billion by 2026, representing the world's highest national mobile advertising investment. The IAB Tech Lab's Open Measurement SDK has been adopted by over 90% of major U.S. in-app advertising platforms, standardizing viewability measurement and reducing ad fraud rates.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific In-app Advertising Market Insights

Asia Pacific is the fastest-growing regional In-app Advertising Market, driven by the world's largest smartphone user populations in China and India, the highest mobile gaming revenues globally, and rapidly expanding mobile commerce ecosystems that create in-app advertising demand across multiple application categories. China's mobile advertising market dominated by Alibaba, Tencent, ByteDance, and Baidu generates advertising revenues approaching the U.S. market in absolute scale. India's rapidly expanding smartphone user base adding tens of millions of new mobile internet users annually represents the most important frontier market for global in-app advertising platform expansion. Southeast Asia's mobile-first digital economy, where many consumers are conducting their entire digital lives through mobile apps rather than desktop computers, creates in-app advertising demand density that rivals developed market levels.

App Annie (data.ai) reports that consumers globally downloaded 255 billion apps in 2023, with Asia Pacific accounting for over 50% of total global app downloads. China's in-app advertising market exceeded USD 100 billion in 2023 according to CNNIC data, making it the world's second-largest national in-app advertising market after the United States.

Europe In-app Advertising Market Insights

Europe is a promising albeit compliance-focused segment for in-app advertising in which the in-app targeting and measurement of advertising campaigns are influenced by GDPR regulations, the requirements of the DMA, and the potential limitations set forth in the EU AI Act regarding algorithmic advertising. The main European segments include the UK, Germany, France, and Scandinavia. These segments have a high proportion of mobile phones among their citizens and advanced use of digital media. Consumers’ awareness about privacy issues, which resulted from years of GDPR enforcement, make European countries favorable markets for privacy-centric and transparent approaches to advertising.

The EU Digital Markets Act designated multiple in-app advertising platform operators as gatekeepers subject to interoperability, data access, and self-preferencing constraints. The European Data Protection Board's guidance on consent-based mobile advertising tracking has materially shaped consent rates that affect in-app advertising targeting effectiveness across EU member states.

Middle East & Africa and Latin America In-app Advertising Market Insights

These two regions provide some of the most promising in-app advertising markets owing to the rapid increase in mobile internet usage, a young and active population, and mobile first approach towards online business and entertainment. In MEA, UAE and Saudi Arabia provide a highly penetrated market for mobile internet usage and active participation in mobile games and social applications. The presence of a high income consumer base in the Gulf region results in CPM rates exceeding that in the rest of the region making it attractive for international companies to advertise in MEA. In Latin America, Brazil emerges as one of the key markets for in-app advertising due to the high mobile penetration and social media usage rate of the Brazilian population.

In-app Advertising Market Growth Drivers:

-

Surging mobile app usage and AI-driven programmatic advertising efficiency creating sustained growth in global in-app advertising spend

The in-app advertising market's growth is grounded in user behavior that is both deeply embedded and still expanding. Mobile apps have become the primary interface through which people consume media, communicate, shop, bank, and entertain themselves in many emerging markets they are the only digital interface the majority of users ever interact with. Advertiser investment follows that attention concentration, and the efficiency of in-app advertising relative to alternatives creates a commercial reinforcement loop: more advertiser investment funds better technology, better technology improves performance, better performance attracts more investment. Programmatic AI bidding has reached a level of sophistication where the marginal return on additional optimization is still positive for most advertisers, meaning that in-app advertising budgets continue to grow because the demonstrable performance justifies continued investment.

The Mobile Marketing Association reports that AI-optimized in-app advertising campaigns deliver 30-40% higher return on ad spend compared to non-AI-optimized campaigns. AppLovin's annual reports document that its AI-driven ad matching algorithms delivered a 100%+ year-over-year improvement in advertising revenue for its publisher network between 2022 and 2024.

In-app Advertising Market Restraints:

-

Privacy regulations and ad fraud challenges limiting in-app advertising targeting effectiveness and spend efficiency globally

In relation to the availability of data used for the targeting of in-app advertisements, Apple's ATT framework and Google's Privacy Sandbox for Android have revolutionized the situation, whereby users' consent for tracking their behavior in other apps is obtained at around 25-40%, which means that a large portion of iOS devices remains inaccessible in terms of targeting. Marketers have found themselves compelled to increase spending on first-party data collection, contextual marketing campaigns, and probabilistic attribution methods to sustain campaign effectiveness, although it is safe to say that the process of adaptation is not entirely smooth and some loss in campaign efficiency can be noted compared to the previous period. Ad fraud in the form of bot traffic, click injection, and device farms accounts for about 8-10% of all global budgets allocated to mobile advertising campaigns.

In-app Advertising Market Opportunities:

-

AI personalization advances and emerging market mobile commerce growth creating vast new in-app advertising opportunities

The most compelling near-term opportunity in in-app advertising is the commercial deployment of AI systems that can achieve effective personalization under privacy constraints delivering relevant advertising experiences to users without the granular individual tracking that privacy frameworks have restricted. Large language model-enabled contextual intelligence, on-device machine learning that processes user signals locally without transmitting identifiable data, and federated learning systems that improve targeting models without centralizing user data are all active areas of development that will reshape in-app advertising targeting over the forecast period. The commerce opportunity is separately compelling: as mobile shopping behaviors mature from browsing to full transaction completion within apps, the in-app advertising environment becomes directly measurable by purchase conversion rather than click-through rate alone enabling advertisers to optimize campaigns against the outcomes that actually matter to their business.

Recent Developments:

-

2026: AppLovin announced a 35% year-over-year increase in software platform revenue, citing its AXON 2.0 AI advertising engine's improved prediction accuracy for user purchase intent and its expansion into e-commerce advertiser segments beyond mobile gaming where the platform had historically concentrated its publisher relationships.

-

2025: Meta Platforms introduced its Advantage+ Creative suite for in-app advertising, enabling automated AI-driven creative versioning that dynamically adapts ad visuals, copy, and calls-to-action based on individual user context within Facebook, Instagram, and Audience Network placements, reporting 22% improvement in conversion rates versus static creative campaigns.

-

2025: Google launched Enhanced Measurement for Android as part of its Privacy Sandbox deployment, providing advertisers with aggregated conversion signals that maintain campaign attribution capability without individual device-level tracking, establishing a privacy-preserving measurement baseline that publishers and advertisers can build audience strategies around.

In-app Advertising Market Key Players

Some of the In-app Advertising Market Companies

-

Meta Platforms Inc.

-

Alphabet Inc. (Google AdMob)

-

Apple Inc. (Apple Ads)

-

Amazon.com Inc. (Amazon DSP)

-

AppLovin Corporation

-

IronSource Ltd. (Unity)

-

Digital Turbine Inc.

-

Snap Inc.

-

Twitter / X Corp.

-

ByteDance Ltd. (TikTok for Business)

-

InMobi Group

-

MoPub (Twitter)

-

Applovin Max

-

Verizon Media (Yahoo)

-

Taboola.com Ltd.

-

Outbrain Inc.

-

Chartboost (Zynga)

-

AdColony (Digital Turbine)

-

Smaato Inc.

-

PubMatic Inc.

In-app Advertising Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 220.05 Billion |

| Market Size by 2035 | USD 838.0 Billion |

| CAGR | CAGR of 14.31% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Banner Ads, Interstitial Ads, Rich Media Ads, Video Ads, Native Ads, Others) • By Platform (Android, iOS, Others) • By Application (Entertainment, Gaming, Social, Online Shopping, Payment & Ticketing, News, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Meta Platforms Inc., Alphabet Inc. (Google AdMob), Apple Inc. (Apple Ads), Amazon.com Inc. (Amazon DSP), AppLovin Corporation, IronSource Ltd. (Unity), Digital Turbine Inc., Snap Inc., X Corp., ByteDance Ltd. (TikTok for Business), InMobi Group, MoPub (Twitter), AppLovin Max, Verizon Media (Yahoo), Taboola.com Ltd., Outbrain Inc., Chartboost (Zynga), AdColony (Digital Turbine), Smaato Inc., PubMatic Inc. |

Frequently Asked Questions

North America dominated the In-app Advertising Market in 2025.

The Gaming segment dominated the In-app Advertising Market in 2025.

The Android platform dominated the In-app Advertising Market with over 70% share in 2025.

The In-app Advertising Market was valued at USD 220.05 billion in 2025.

The In-app Advertising Market is expected to grow at a CAGR of 14.31% from 2026 to 2035.

Get in Touch