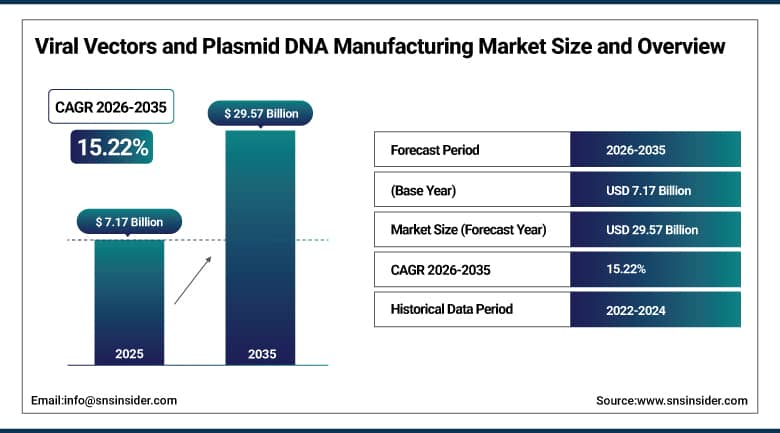

Viral Vectors and Plasmid DNA Manufacturing Market Report Scope & Overview:

The Viral Vectors and Plasmid DNA Manufacturing Market was valued at USD 7.17 Billion in 2025 and is expected to reach USD 29.57 Billion by 2035, growing at a CAGR of 15.22% from 2026–2035.

Viral vectors and plasmid DNA form the manufacturing backbone behind gene therapies, cell therapies, and a growing share of modern vaccines. A vector is essentially a gene-delivery vehicle, a DNA molecule carrying a transgene insert that gets introduced into a target cell so genetic material can be reproduced or expressed. As more gene and cell therapies clear clinical trials and reach commercial approval, biopharmaceutical companies and CDMOs are racing to build out GMP-compliant manufacturing capacity capable of producing these materials at clinical and commercial scale. That build-out is reshaping the competitive landscape, with contract manufacturers investing heavily in single-use bioreactors, automated purification systems, and expanded facility footprints.

By June 2025, there is an enhancement in the production capacity of viral vectors for Lonza Group at its Houston, Texas-based manufacturing site in view of increased demand from gene therapy pipelines. The expansion is representative of the capacity issues faced across the industry as the number of approved gene therapies increases from clinical to commercial scale.

Market Size and Forecast

- Market Size in 2026E: USD 8.26 Billion

- Market Size by 2035: USD 29.57 Billion

- CAGR: 15.22% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get More Information On Viral Vectors and Plasmid DNA Manufacturing Market - Request Free Sample Report

Viral Vectors and Plasmid DNA Manufacturing Market Trends

- Rising demand for gene therapies and personalized medicines is driving the need for large-scale viral vector and plasmid DNA production.

- Adoption of AAV, lentivirus, and adenovirus vectors continues to expand across cell and gene therapy pipelines.

- Biopharmaceutical companies and CDMOs are investing heavily in GMP-compliant manufacturing facilities.

- Contract development and manufacturing services are expanding to meet growing clinical and commercial-scale demand.

- Advances in upstream and downstream process technology, including single-use bioreactors and improved chromatography, are boosting yields and cutting costs.

- Plasmid DNA demand is climbing as a template for mRNA vaccine and gene therapy vector production.

- Strategic partnerships between pharmaceutical companies, biotech firms, and CMOs are accelerating technology transfer and manufacturing scale-up.

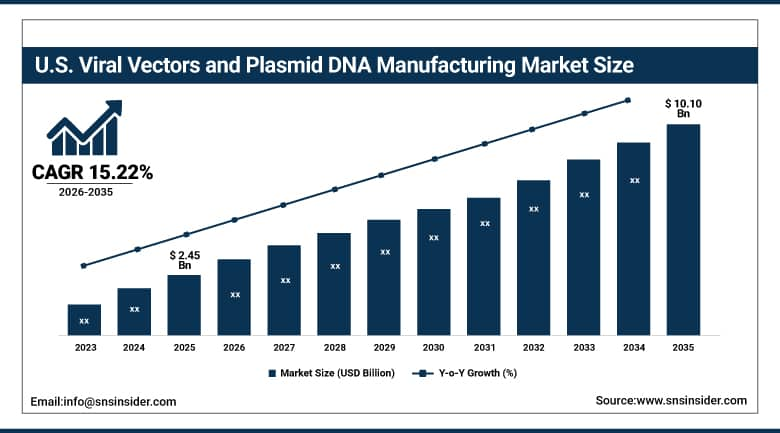

The U.S. Viral Vectors and Plasmid DNA Manufacturing Market Outlook

The U.S. Viral Vectors and Plasmid DNA Manufacturing market was valued at USD 2.45 Billion in 2025 and is projected to reach USD 10.10 Billion by 2035, growing at a CAGR of 15.22% from 2026–2035.

The United States remains the center of gravity for viral vector and plasmid DNA manufacturing, underpinned by a deep base of biopharmaceutical companies, leading CDMOs, and a regulatory framework that has approved a growing list of gene and cell therapies. Rising clinical trial volume and the steady approval of new AAV- and lentiviral-based therapies are driving continuous investment in domestic manufacturing capacity, while academic medical centers and government research institutions add further demand for research-grade and early clinical-stage vector production.

In September 2025, Catalent Inc. launched an expanded plasmid DNA manufacturing line in Madison, Wisconsin, built specifically to support mRNA vaccine and gene therapy pipelines. The expansion increases domestic plasmid output and speeds delivery timelines for clinical programs across the country.

Viral Vectors and Plasmid DNA Manufacturing Market Segment Analysis

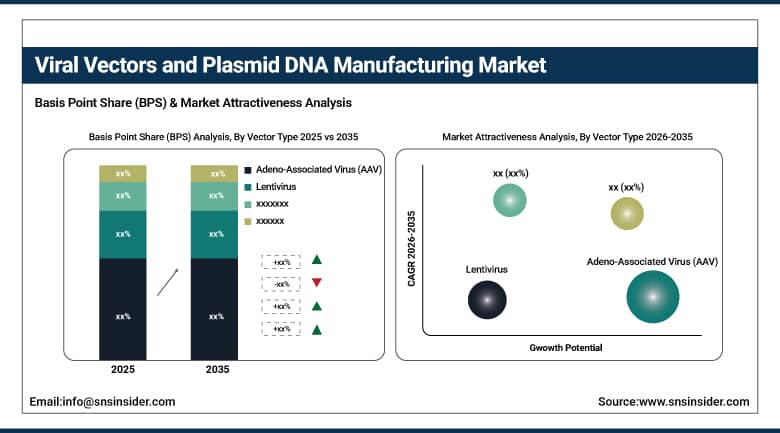

- By Vector Type: AAV dominated the viral vectors and plasmid DNA manufacturing market with 29% share in 2025, while lentivirus is growing fastest at approximately 8.13% CAGR.

- By Workflow: upstream manufacturing dominated the market with approximately 35% share in 2025, while process development is projected to be the fastest-growing segment at around 8.9% CAGR during the forecast period.

- By Application: vaccines dominated the viral vectors and plasmid DNA manufacturing market with 66% share in 2025, while gene therapy is the fastest-growing application during the forecast period.

- By Grade: GMP-grade (clinical) dominated the market with approximately 47% share in 2025, while GMP-grade (commercial) is expected to register the fastest growth at around 9.1% CAGR during the forecast period.

- By End User: biopharmaceutical & biotechnology companies dominated the market with approximately 46% share in 2025, while CDMOs/CMOs are projected to witness the fastest growth at around 9.8% CAGR during the forecast period.

By Vector Type, AAV dominate, lentivirus grows fastest

The Adeno-associated virus (AAV) dominated the vector-type component of the market in 2025, contributing 29% to the total revenue. The high safety level, minimal immunogenicity, and capability to provide long-lasting gene expression makes it an ideal vector choice for several gene and cell therapies that are driving investments in scalable AAV manufacturing technology.

Lentivirus is the fastest-growing vector type, expanding at an 8.13% CAGR through the forecast period. Lentiviral vectors can transduce both dividing and non-dividing cells, which makes them especially well suited to CAR-T and other cell therapy applications. Rising clinical trial activity and a growing list of approvals are pushing investment into higher-efficiency lentiviral production platforms.

By Application, vaccines dominate, gene therapy grows fastest

The vaccines segment dominated the market in 2025, holding 66% of the market revenue share owing to the volume of global demand for viral vector and mRNA vaccine manufacturing. Plasmid DNA manufacturing, process improvement, and fill and finish services have been increased to meet this growing demand.

The Gene Therapy segment is expected to be the most lucrative, owing to an increasing number of AAV and lentivirus-based therapies being approved for rare genetic disorders and cancer indications. With the approval of such therapies increasing, the need for process development and scalable manufacturing has also been realized by biopharmaceutical companies.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.40% |

|

Europe |

Germany |

24.90% |

|

Asia Pacific |

China |

38.60% |

|

Middle East & Africa |

Saudi Arabia |

21.50% |

|

Latin America |

Brazil |

46.80% |

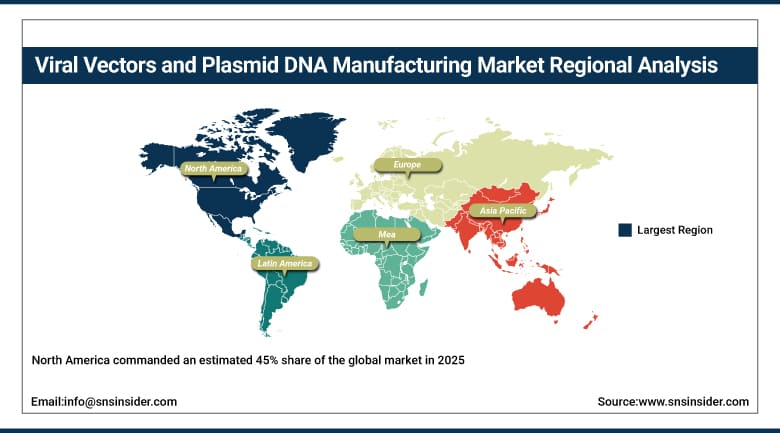

North America Viral Vectors and Plasmid DNA Manufacturing Market Insights

North America commanded an estimated 45% share of the global market in 2025, driven by advanced healthcare infrastructure, a growing number of gene and cell therapy approvals, and heavy investment in biopharmaceutical manufacturing capacity. The area is fortunate in having leading CDMO and biopharma firms such as Lonza, Thermo Fisher Scientific, and Catalent, all of whom are constantly increasing their manufacturing capabilities.

North America maintains its market dominance thanks to significant government funding, strong ties with research organizations, and an active pipeline of vaccines and gene therapies. In the North American market, the US takes the lead owing to its heavy spending on R&D and GMP manufacturing capabilities.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Viral Vectors and Plasmid DNA Manufacturing Market Insights

Europe held a significant share of the global market in 2025, driven by strong demand for gene therapies and viral-vector-based vaccines. The combination of advanced biopharmaceutical infrastructure, compliance with regulatory standards and increased number of clinical trials will continue to fuel growth of the region.

Germany dominates the European market due to a well-developed biotech ecosystem, financial backing for gene therapy studies and presence of many CDMOs. Clinical innovation and high quality manufacturing are major factors contributing to German domination of the European market.

Asia Pacific Viral Vectors and Plasmid DNA Manufacturing Market Insights

Asia Pacific is projected to grow at an estimated 12.63% CAGR, the fastest of any region, fueled by expanding biotechnology investment, emerging gene therapy research programs, and growing local CDMO capacity. Rising demand for viral vectors and plasmid DNA to support mRNA vaccines and gene therapy pipelines is accelerating regional market growth.

The dominant player in this region is China, backed by government incentives, robust biotech ecosystems, and quick adoption of gene and cell therapy pipelines. Collaboration between Chinese manufacturers and multinational companies serving as contract development and manufacturing organizations (CDMOs), together with the development of manufacturing infrastructure in the region, are boosting the supply chain capabilities of the region.

Middle East & Africa and Latin America Viral Vectors and Plasmid DNA Manufacturing Market Insights

Middle East & Africa continued to grow in 2025 on account of growing healthcare spending, biotech efforts, and growing clinical research capacity. The dominant region in this case is South Africa as a result of its investment in developing capabilities in gene therapy manufacturing using GMPs and partner programs.

Other emerging regions include Latin America, as a result of investments by Brazil and Mexico among other regions in CDMOs, increase in the number of clinical trials and government initiatives to improve vaccine and gene therapy manufacturing. Although both Latin America and Middle East & Africa are emerging regions, their contribution to the global market grows.

Market Dynamics

Growth Drivers: Growing Adoption of Gene & Cell Therapies and Expansion of GMP Manufacturing Capacity

Rising adoption of gene and cell therapies is the single biggest driver behind this market's growth. As personalized medicine gains ground, biopharmaceutical companies and research institutions need large volumes of high-quality viral vectors and plasmid DNA to support both clinical trials and commercial-stage therapies. This demand is encouraging companies to invest in sophisticated production methods such as single-use bioreactors, automated purification methods, and Good Manufacturing Practice-certified production facilities.

The increasing occurrence of rare genetic diseases and use of vectors for treating oncological conditions is also leading to increased demand for different types of vectors such as AAV, lentivirus, and adenovirus. Increasing number of gene therapy products being developed, tested, and approved is driving the growth of the global market.

Restraints: Stringent GMP Regulatory Requirements and High Manufacturing Costs

Strict regulatory requirements and high production costs remain significant restraints on market growth. The manufacture of vectors of clinical and commercial grade entails compliance with GMP regulations, safety assessments, and analytical validation, all of which necessitate large financial investment in appropriate facilities and skilled labor.

Complex upstream and downstream processes, including transfection, purification, and fill-finish operations, add further operational expense and create real barriers for small and mid-sized companies trying to enter the space. The regulatory landscape also tends to slow time-to-market, particularly for novel therapies that require entirely new vector platforms or manufacturing modifications.

Opportunities: Expansion of mRNA Vaccine Production and Strategic CDMO Partnerships

Rising usage of mRNA vaccines and gene therapy platforms is creating numerous opportunities within the market. Plasmid DNA and vectors play important roles in mRNA vaccines manufacturing and gene therapy delivery. Increasing need for efficient and scalable manufacturing techniques is leading companies to develop new technology for plasmid manufacturing and automation in purification process.

Pharmaceutical firms are entering into strategic alliances with contract development and manufacturing organizations (CDMOs). Such business relationships enable market players to diversify service offering, drive innovations in production process and meet growing demands for the next generation therapeutics.

Recent Developments:

- 2025: In June 2025, Lonza Group inaugurated a new viral vector manufacturing facility in Houston, Texas, designed to increase AAV and lentiviral vector output for clinical and commercial applications.

- 2025: In September 2025, Catalent Inc. expanded its Madison, Wisconsin facility with a dedicated plasmid DNA production line to support mRNA vaccine and gene therapy pipelines.

- 2025: In August 2025, FUJIFILM Diosynth Biotechnologies expanded its U.S. viral vector production capacity, incorporating single-use bioreactors and automated chromatography systems.

- 2025: In 2025, Thermo Fisher Scientific expanded its plasmid DNA production capacity in the U.S., introducing enhanced single-use bioreactors and automated purification platforms.

Viral Vectors and Plasmid DNA Manufacturing Market key players are:

- Thermo Fisher Scientific

- Lonza Group

- Catalent Inc.

- FUJIFILM Diosynth Biotechnologies

- Oxford Biomedica

- Aldevron

- WuXi Advanced Therapies

- Charles River Laboratories

- VGXI Inc.

- Cobra Biologics

- SIRION Biotech GmbH

- PlasmidFactory GmbH

- AGC Biologics

- Yposkesi

- Takara Bio Inc.

- UniQure N.V.

- Virovek Incorporation

- RegenxBio, Inc.

- BioMarin Pharmaceutical

- MassBiologics

Viral Vectors and Plasmid DNA Manufacturing Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.17 Billion |

| Market Size by 2035 | USD 29.57 Billion |

| CAGR | CAGR of 15.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Vector Type (Adenovirus, Adeno-Associated Virus (AAV), Lentivirus, Retrovirus, Plasmids, Others) • By Workflow (Upstream Manufacturing, Downstream Purification, Fill-Finish, Quality Control & Testing, Process Development) • By Application (Gene Therapy, Cell Therapy, Vaccines, Oncology/Oncolytic Viruses, Research Use) • By Grade (Research-Grade, GMP-Grade (Clinical), and GMP-Grade (Commercial)) • By End User (Biopharmaceutical & Biotechnology Companies, CDMOs/CMOs, Academic & Research Institutes, Vaccine Manufacturers, Government/Public Health Agencies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific, Lonza Group, Catalent Inc., FUJIFILM Diosynth Biotechnologies, Oxford Biomedica, Aldevron, WuXi Advanced Therapies, Charles River Laboratories, VGXI Inc., Cobra Biologics, SIRION Biotech GmbH, PlasmidFactory GmbH, AGC Biologics, Yposkesi, Takara Bio Inc., uniQure N.V., Virovek Inc., REGENXBIO Inc., BioMarin Pharmaceutical Inc., MassBiologics. |

Frequently Asked Questions

The market is expected to grow at a CAGR of 15.22% between 2026 and 2035.

The market was valued at USD 7.17 Billion in 2025.

Adeno-Associated Virus (AAV) held the largest share in 2025, at 29% of total market revenue.

North America led the market in 2025 with an estimated 45% share.

Growth is driven by rising adoption of gene and cell therapies, expanding CDMO manufacturing capacity, and growing demand for plasmid DNA in mRNA vaccine production.

Get in Touch