Vyvgart (Efgartigimod) Market Report Scope & Overview:

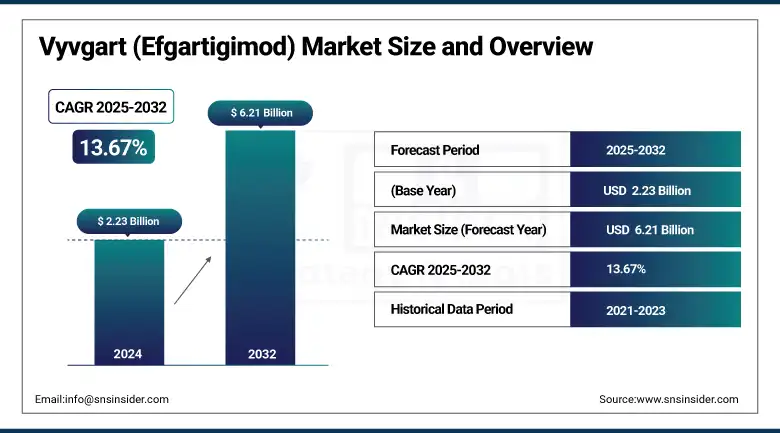

The Vyvgart (Efgartigimod) market size was valued at USD 2.23 billion in 2024 and is expected to reach USD 6.21 billion by 2032, growing at a CAGR of 13.67% over 2025-2032.

The Vyvgart (Efgartigimod) market is expected to grow very rapidly. Especially the increase in the autoimmune disease incidence, the increase in FDA and EMA approved number, and the increasing importance of biopharma company investments to reduce the autoimmune pain take the North America region’s market to the top. Efgartigimod, a neonatal Fc receptor (FcRn) inhibitor that is first-in-class, has made forays into the treatment of generalized myasthenia gravis (gMG) and chronic inflammatory demyelinating polyneuropathy (CIDP), and has received regulatory nods in the U.S., China, EU, and Japan. The Vyvgart (Efgartigimod) market can also benefit from further clinical data, such as from phase 3 trials (e.g., ADAPT and ADHERE), which demonstrate significant improvements in symptoms and functional scores. The U.S. Vyvgart (Efgartigimod) market is heavily buoyed by the approval of the self-injectable Vyvgart Hytrulo (Apr 2024), improving patient convenience and compliance.

To Get more information On Vyvgart (Efgartigimod) Market - Request Free Sample Report

In April 2025, the FDA approved Vyvgart Hytrulo in a pre-filled syringe, making it easier for patients to administer and lessening the dosing burden.

Factors that are driving the Vyvgart (Efgartigimod) market growth include the growing R&D expenditure– Argenx alone, which spent more than USD 600 million on R&D in 2023, directly dedicated towards CIDP, ITP, and additional IgG-mediated diseases. In addition, continued partnerships such as Argenx and Zai Lab (China) and EU positive CHMP opinions have increased international access. Supply chains are growing along with demand. Argenx has also extended its active development programs into the United States, Japan, China, and South Korea, providing a larger pan-regional presence in key markets around the world. Prescriptions and provider adoption every month have grown in real-world use across neurology and immunology.

Regulatory FDA's drug trials snapshot (2024) confirms drug effectiveness and safety across multiple demographics. Moreover, peer-reviewed publications of real-world data confirm GR in real life. The market share for Vyvgart (efgartigimod) is expected to increase as good reimbursement and a trend towards physician preference of targeted therapies over traditional immunosuppressants will help drive growth. The companies behind Vyvgart (Efgartigimod), Argenx with its leaches and followers, are also exploring new concepts such as making child-friendly versions and combining treatments, a fact that contributes to maintaining an optimistic market analysis and future planning for Vyvgart (Efgartigimod).

In May 2024, Argenx and Zai Lab announced regulatory approval for Vyvgart in CIDP in China, a key milestone in the internationalization of the Vyvgart (Efgartigimod) market.

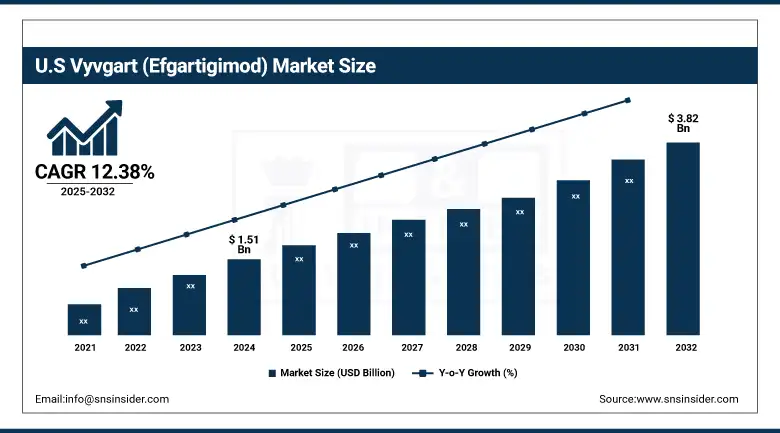

The U.S. Vyvgart (Efgartigimod) market size was valued at USD 1.51 billion in 2024 and is expected to reach USD 3.82 billion by 2032, growing at a CAGR of 12.38% over 2025-2032. Wide-reaching commercial availability, patient assistance programs, and high rates of diagnosis have further supported US dominance. In Canada, uptake has started, but market access is still small because of more restrictive health technology assessments and slower approvals than in the U.S. Mexico is a slow-growing market driven by expanding health care for rare diseases and demand for innovative immunotherapies.

Market Dynamics:

Drivers:

-

Rising Clinical Applications, R&D Investments, and Expedited Approvals Fuel Demand

A key driver of the market includes the increasing incidence of antibody-mediated autoimmune diseases and a surge in the number of indications undergoing clinical trials. Growing interest in blocking the FcRn selectively is driven by compelling clinical data in diseases such as ITP, PV, and MMN. Argenx is actively running several Phase II/III studies and has more than 12 indications in the pipeline as of 2024. This broadening has fueled a demand increase in the global Vyvgart (efgartigimod) market within neurology and immunology. R&D investments are also on the rise, and Argenx estimates investing €807 million (~USD 875 million) in R&D by 2023, demonstrating the industry’s enthusiasm for FcRn modulation.

Moreover, the FDA’s orphan drug designation for efgartigimod in several indications and the breakthrough therapy designation for CIDP have shortened the development timeline and expanded market opportunities. Clinical practice guidelines and expanding payer coverage of individualized immunotherapy also drive adoption. Biopharma companies are also undertaking numerous collaborations (e.g., argenx–Horizon Therapeutics and argenx–Stichting Sanquin), suggesting a strong expanding ecosystem. Alongside those factors, increased production capabilities and improved methods of access (subcutaneous, as well as I.V.) are helping to accelerate the rate at which doctors are using, and patients can get, Vyvgart (Efgartigimod).

Restraints:

-

High Therapy Costs, Competitive Landscape, and Access Gaps Create Barriers

Even with robust Vyvgart (efgartigimod) market trends, high treatment costs and restricted reimbursement are significant headwinds. The mean annual cost of Vyvgart treatment per patient may exceed USD 400,000 in the U.S., which represents a substantial access point, particularly for underinsured patients. Although subcutaneous formulations reduce the inconvenience, they do not bring the latter with the overall costs.

The rise of rival FcRn-targeted drugs like Johnson & Johnson’s nipocalimab and UCB’s rozanolixizumab could dilute Vyvgart (Efgartigimod) market potential. These peers are winning regulatory victories and demonstrating similar efficacy profiles, adding to pricing, formulary pressure. Also, differences in drug approval and labelling between nations (e) e.g., slower uptake in jurisdictions where inflexible pharmacoeconomic assessments are the norm, like Canada or some EU countries) made for non-uniformity of access. High cost and lack of widespread distribution in LMICs are also barriers to worldwide access. The delayed diagnosis and underdiagnosis of gMG and CIDP in emerging regions also delay patients’ medication-seeking behavior and therefore the realized potential of market expansion, despite the unmet demand and merit of gMG and CIDP. These structural and financial obstacles are also obstructing equitable growth in the global Vyvgart (Efgartigimod) market.

Segmentation Analysis:

By Indication

The Generalized Myasthenia Gravis (gMG) was the leading segment in 2024 on the basis of revenue and had the largest market revenue share of 97.68% in the Vyvgart (Efgartigimod) market. This position may be primarily explained by early gMG FDA approval (in 2021), robust real-world clinical data, and broad prescriber familiarity. The large and diverse patient population, combined with improved awareness and diagnosis, means that Vyvgart has been widely accepted as the first-in-class FcRn blocker in gMG. In addition, clinical guideline recommendations and increasing payer acceptance have driven up utilization rates.

In contrast, CIDP is forecasted to be the fastest-growing market segment, due to the FDA’s 2024 approval for this indication and positive outcomes from the Phase 3 ADHERE study. The clearance has made a large patient population seeking other treatments besides steroids and IVIg available for access. Argenx’s build-out of its CIDP-oriented R&D and expansion into new markets such as China (via Zai Lab) should help fuel this segment’s growth trajectory in a big way.

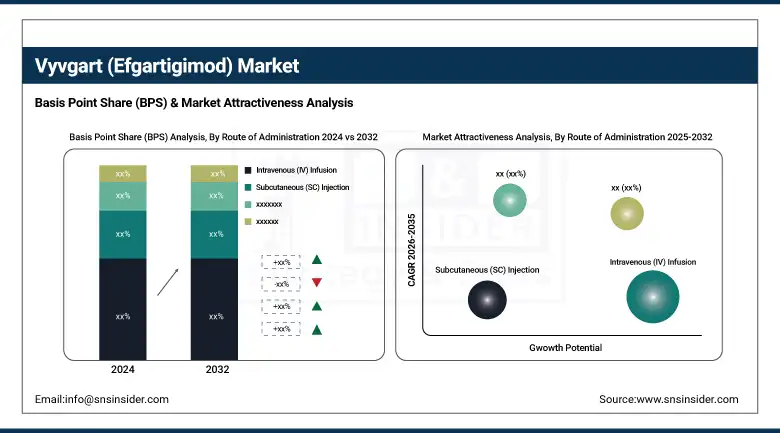

By Route of Administration

By route of administration, the market was led by the Intravenous (IV) Infusion segment of Vyvgart (efgartigimod) in 2024 with 95.78% share. That leadership comes courtesy of its earlier regulatory green light and broad usage in the clinical practice environment, including but not limited to hospitals and infusion centers. Since Vyvgart first entered the market, the IV preparation’s long-standing safety profile and low dose familiarity have established it as a reasonable default option.

The prefilled syringe segment is expected to grow at the fastest pace during the forecast period. The introduction of Vyvgart Hytrulo self-administered prefilled syringe (April 2025 FDA approval) has brought great convenience to the patients, lessening the need for repeated visits to the clinic. This dosing approach can be self-administered at home, which increases compliance and access for the patient, especially in chronic conditions that need consistent long-term treatment. Increased productivity, coupled with rapid adoption among neurologists and immunologists, is anticipated to drive the market share.

Regional Analysis:

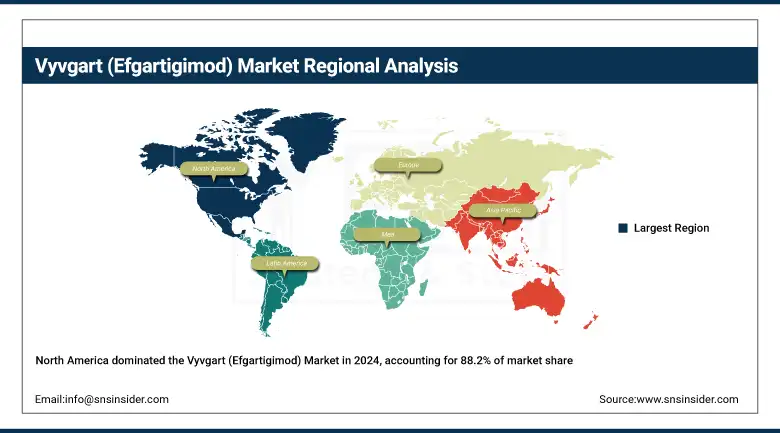

North America was the most prominent regional Vyvgart (Efgartigimod) market in 2024, which contributed to 88.2% market share, on account of early approvals from the FDA, robust healthcare infrastructure, and broad reimbursement coverage. The USW is a stronghold, with Vyvgart uptake accelerated for generalized myasthenia gravis (gMG) and chronic inflammatory demyelinating polyneuropathy (CIDP).

Get Customized Report as per Your Business Requirement - Enquiry Now

Vyvgart (Efgartigimod) market in Europe is the second fastest growing, supported by the growing burden of autoimmune diseases and regulatory developments – CHMP’s positive opinion for CIDP. Germany stands at the forefront of the region due to its sophisticated reimbursement system, high level of clinical trial enrollment, and represents the largest market in Europe for Vyvgart. Phenomenal backing of rare disease societies and progressive incorporation of treatment protocols in France and the UK are driving penetration in the market. Italy and Spain are doing the same, with higher coverage as a result of in-hospital formulation administration and recent inclusion in the payer reimbursement catalogue. Turkey and Poland have sizeable patient pools with growth potential but are plagued by regulatory sluggishness.

Among other regions, Asia Pacific is the fastest-growing Vyvgart (Efgartigimod) market, with increasing regulatory approvals and partnerships. China leads the charge, and approval of Vyvgart Hytrulo (2024) for CIDP is a significant step on the road to market, with Argenx and Zai Lab teaming up. Japan, which was already a solid gMG market for Vyvgart given its prior gMG approval, remains a high clinical adopter driven by aging and a higher incidence of autoimmune disease. India and South Korea are seeing rising demand, higher awareness, diagnosis rates, and ongoing efforts to simplify regulatory pathways. Early access. Under early access schemes and strong local clinical trial ecosystems, Singapore and Australia are using the superior SPV technology that promises greater access, enabling more people to take up vaccines.

Key Players:

Argenx SE, Zai Lab Limited, Halozyme Therapeutics Inc., Pfizer Inc., UCB Pharma, Johnson & Johnson (Janssen), Alexion Pharmaceuticals (AstraZeneca), Horizon Therapeutics, Immunovant Inc., and Takeda Pharmaceutical Company Limited.

Recent Developments:

-

In April 2025, Argenx announced that the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency (EMA) issued a positive opinion recommending the approval of VYVGART (efgartigimod alfa) for subcutaneous monotherapy in adult patients with progressive or relapsing active CIDP, particularly those previously treated with corticosteroids or immunoglobulin therapies.

-

In April 2025, argenx SE secured FDA approval for a prefilled syringe formulation of VYVGART Hytrulo (efgartigimod alfa and hyaluronidase-qvfc), allowing self-administration by adult patients with generalized myasthenia gravis (gMG) who are anti-AChR antibody positive, as well as those with chronic inflammatory demyelinating polyneuropathy (CIDP).

-

In Nov 2024, China’s NMPA approved Vyvgart Hytrulo as the first-ever CIDP therapy in the country, marking a pivotal milestone. The once‑weekly subcutaneous treatment strengthens the argenx–Zai Lab alliance and broadens treatment options for patients with limited access to alternatives such as IVIg.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.23 billion |

| Market Size by 2032 | USD 6.21 billion |

| CAGR | CAGR of 13.67% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Indication (Chronic Inflammatory Demyelinating Polyneuropathy (CIDP), Generalized Myasthenia Gravis (gMG), and Others) • By Route of Administration (Intravenous (IV) Infusion, Subcutaneous (SC) Injection, and Prefilled Syringe) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Argenx SE, Zai Lab Limited, Halozyme Therapeutics Inc., Pfizer Inc., UCB Pharma, Johnson & Johnson (Janssen), Alexion Pharmaceuticals (AstraZeneca), Horizon Therapeutics, Immunovant Inc., and Takeda Pharmaceutical Company Limited. |

Frequently Asked Questions

Ans: North America is the dominant region in the Vyvgart (Efgartigimod) market.

Ans: Even with robust Vyvgart (efgartigimod) market trends, high treatment costs and restricted reimbursement are significant headwinds.

Ans: A key driver of the market includes the increasing incidence of antibody-mediated autoimmune diseases and a surge in the number of indications undergoing clinical trials.

Ans: By 2032, the Vyvgart (Efgartigimod) Market is expected to reach USD 6.21 billion, up from USD 2.23 billion in 2024.

Ans: The Vyvgart (Efgartigimod) Market is projected to grow at a CAGR of 13.67% during the forecast period.

Get in Touch