Identity Verification Market Report Scope & Overview:

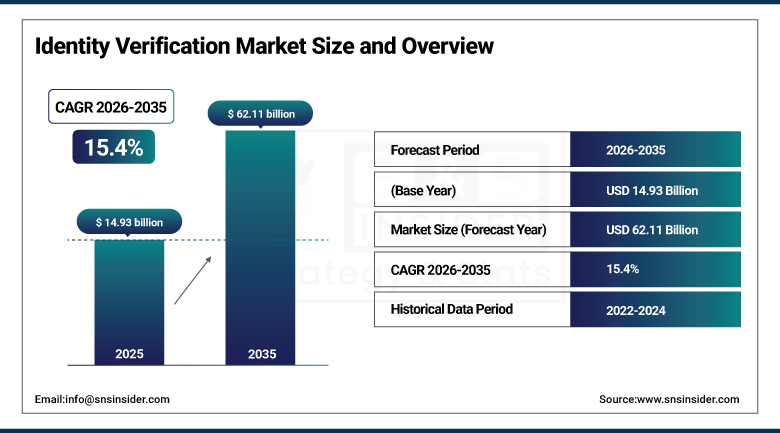

The Identity Verification Market was valued at USD 14.93 Billion in 2025 and is expected to reach USD 62.11 Billion by 2035, growing at a CAGR of 15.4% from 2026–2035.

The global identity verification market is growing at an exceptional pace. Identity verification encompasses the technologies, processes, and services used to confirm that individuals are who they claim to be in digital and physical interactions. The market is driven by rising identity fraud costs, increasing regulatory compliance requirements including KYC and AML mandates, AI-driven solution adoption enabling faster and more accurate verification, and biometric technology advancing remote identity confirmation for digital onboarding.

In 2024, Experian integrated advanced biometric verification into its fraud prevention solutions, specifically targeting the BFSI sector amid rising financial fraud losses. The integration reflects the commercial recognition that traditional knowledge-based authentication whose security relies on information already compromised in data breaches can no longer adequately protect financial institutions whose digital onboarding and transaction verification requirements demand biometric identity confirmation whose spoofing difficulty creates materially higher security assurance than password and question-based alternatives.

Market Size and Forecast

-

Market Size in 2026E: USD 17.23 Billion

-

Market Size by 2035: USD 62.11 Billion

-

CAGR: 15.4% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Identity Verification Market - Request Free Sample Report

Identity Verification Market Trends

-

AI-powered biometric verification solutions are improving identity authentication accuracy through advanced facial recognition, liveness detection, and document verification technologies

-

Rapid adoption of BNPL services and digital financial platforms is increasing demand for automated identity verification and real-time KYC compliance solutions

-

Decentralized identity and self-sovereign identity frameworks are gaining attention as privacy-focused alternatives to traditional centralized identity verification systems

-

Continuous authentication technologies are emerging as a next-generation security approach by using behavioral biometrics to verify user identity throughout digital interactions

-

Growing international travel, cross-border banking, and global e-commerce activities are driving demand for identity verification platforms capable of supporting multiple document types and languages worldwide

U.S. Identity Verification Market Outlook

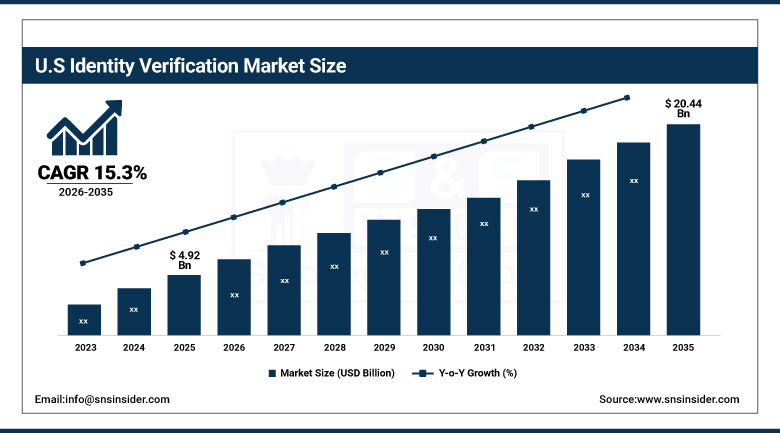

The U.S. Identity Verification Market was valued at approximately USD 4.92 Billion in 2025 and is expected to reach approximately USD 20.44 Billion by 2035, growing at a CAGR of approximately 15.3%.

The U.S. is the world's most commercially sophisticated identity verification market within North America's dominant 38% global revenue position. LexisNexis Risk Solutions, Experian, Equifax, IDEMIA, and Jumio are headquartered or have primary operations in the U.S., collectively defining the commercial technology frontier. The U.S. financial services sector's KYC and AML regulatory requirements, the FinCEN’s beneficial ownership registry mandates, and the CFPB’s fraud prevention emphasis collectively create compliance-driven identity verification procurement.

In 2024, LexisNexis Risk Solutions expanded its ThreatMetrix identity verification platform with enhanced AI-powered device intelligence and behavioural analytics, enabling financial institutions to detect sophisticated account takeover attempts through continuous session monitoring rather than point-in-time authentication. The enhancement represents the commercial evolution of identity verification from a one-time onboarding verification event toward continuous authentication whose real-time fraud signal detection substantially improves financial institution loss prevention relative to static credential-based approaches.

Identity Verification Market Segment Analysis

-

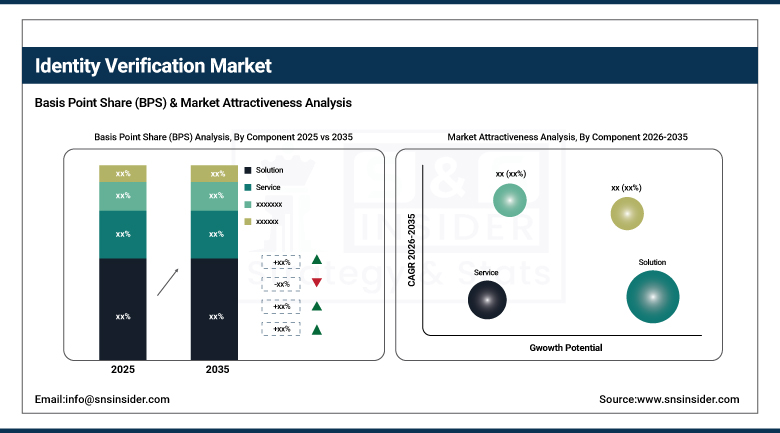

By Component, the Solution segment dominated the Identity Verification Market with approximately 63% share in 2025, while the Service segment is the fastest growing segment with a CAGR of 16.57% during the forecast period.

-

By Type, the Biometrics segment dominated the Identity Verification Market with approximately 58% share in 2025, while the Non-Biometrics segment maintains significant deployment in document and database verification applications.

-

By Deployment, the Cloud segment dominated the Identity Verification Market with approximately 64% share in 2025, while the On-Premise segment is the fastest growing.

-

By Organisation Size, the Large Enterprises segment dominated the Identity Verification Market with approximately 62% share in 2025, while the SMEs segment is the fastest growing.

-

By Verticals, the BFSI segment dominated the Identity Verification Market in 2025, while the Retail & E-Commerce segment is the fastest growing with a CAGR of 16.99%.

By Component, solution dominates, services grow fastest

Solutions retained the dominant component position with approximately 63% of the identity verification market in 2025. Identity verification software platforms encompassing document verification engines, biometric matching algorithms, liveness detection, database connectivity, and orchestration layers collectively constitute the solution portfolio whose deployed technology creates the commercial infrastructure that enterprises access for identity verification capability. The solution segment’s dominance reflects the enterprise’s foundational requirement for deployed technology infrastructure whose API integration with digital onboarding, transaction authorisation, and access management workflows creates the commercial relationships that sustain consistent procurement.

Services are the fastest-growing component at a CAGR of 16.57% because the implementation complexity of identity verification system integration, the specialised expertise required for regulatory compliance programme design, and the managed verification service model’s commercial accessibility create growing service procurement that exceeds solution licensing growth. Each enterprise that transitions from manual to automated identity verification creates implementation consulting demand, and each regulated institution that requires ongoing compliance programme management creates managed service procurement whose recurring revenue compounds with regulatory change management requirements.

By Verticals, BFSI dominates, retail grows fastest

BFSI retained the dominant vertical position in the identity verification market in 2025. The financial services industry’s regulatory requirement for KYC, AML, and CIP compliance creates the most commercially structured and legally mandated identity verification procurement of any industry vertical. Each bank, insurance company, and investment firm operating in regulated markets must verify customer identity at account opening, transaction execution, and regulatory reporting, creating verification volume that scales with customer base size and transaction frequency. The extraordinary growth of digital banking, neobank onboarding, and crypto exchange customer acquisition creates above-average new verification event volume that sustains BFSI’s commercial dominance.

Retail and e-commerce is the fastest-growing vertical at 16.99% CAGR because the surge in online shopping, BNPL service adoption, and cross-border e-commerce creates above-average identity fraud exposure that commercial survival motivation sustains verification investment to prevent. The BNPL industry’s real-time credit decision requirement creates automated identity verification at application volumes that manual verification cannot process at acceptable speed, creating structured AI-powered verification procurement. Each new BNPL provider launch and each expansion of buy-now-pay-later into new merchant categories creates identity verification transaction volume that compounds with BNPL market penetration growth.

By Deployment, cloud dominates, on-premise grows for regulated sectors

Cloud deployment retained the dominant position with approximately 64% of the identity verification market in 2025. Cloud-delivered identity verification’s natural alignment with digital onboarding workflows whose consumer-facing applications operate from cloud infrastructure, combined with the scalability that cloud verification API consumption provides for variable transaction volume, creates strong commercial preference for cloud deployment across digital-native enterprises. SaaS-delivered identity verification whose pay-per-verification pricing model eliminates capital infrastructure investment creates commercial accessibility that sustains cloud dominance across both enterprise and SME customer segments.

On-premise deployment is fastest-growing for regulated industries where data sovereignty requirements, PII processing restrictions, and security classification mandates prevent cloud processing of identity verification data. Government agencies, defence contractors, and healthcare organisations whose identity verification creates sensitive data whose regulatory framework mandates localised processing create structured on-premise verification infrastructure procurement that compounds with regulatory tightening across multiple jurisdictions.

By Type, biometrics dominate, non-biometrics maintain significant share

Biometric identity verification retained the dominant type position with approximately 58% of the identity verification market in 2025. Facial recognition’s ability to compare a live selfie against identity document photographs, fingerprint matching for device authentication, and voice biometric verification for call centre identity confirmation collectively define the biometric verification category whose security advantage over knowledge-based alternatives sustains adoption momentum. Each high-profile data breach that compromises knowledge-based authentication credentials creates commercial motivation for biometric verification adoption whose spoofing difficulty creates materially superior security assurance.

Non-biometric identity verification maintains significant commercial presence through document verification, database lookup, credit history check, and knowledge-based authentication whose combined application breadth sustains commercial relevance in verification contexts where biometric capability is technically or commercially impractical. Each verification scenario requiring background check, sanctions screening, or credit history assessment creates non-biometric verification procurement that compounds with regulatory compliance programme expansion across financial services, healthcare, and employment screening contexts.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Identity Verification Market Insights

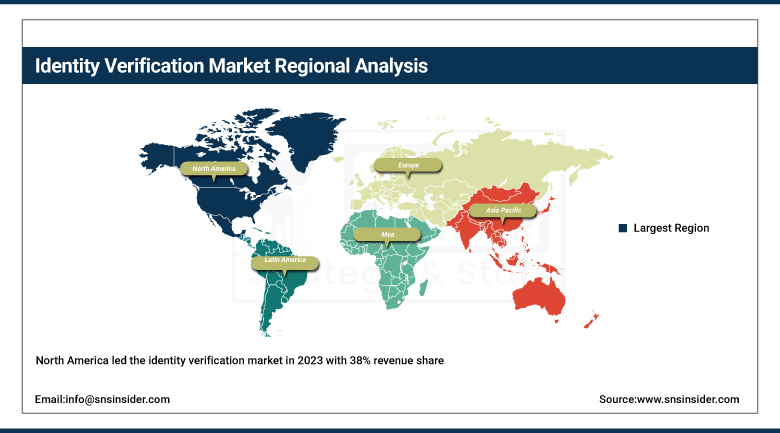

North America led the identity verification market in 2023 with 38% revenue share. The United States accounts for approximately 87.4% of North American revenues through its combination of the world’s most stringent KYC and AML regulatory framework, highest per-capita digital banking adoption, and the commercial presence of LexisNexis Risk Solutions, Experian, Equifax, IDEMIA, and Jumio whose combined portfolio defines the commercial technology standard.

Canada contributes approximately 12.6% of North American revenues through its financial services sector’s verification compliance investment, the federal government’s digital identity programme, and the growing fintech sector’s KYC automation demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Identity Verification Market Insights

Europe is a technically sophisticated identity verification market where eIDAS regulation’s digital identity framework, GDPR’s data protection requirements creating privacy-preserving verification architecture, and AML Directive compliance create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its financial services sector’s compliance investment, the digital payments industry’s verification requirement, and the government digital identity programme.

The United Kingdom, France, and the Netherlands are significant secondary markets whose financial services regulatory compliance, digital banking growth, and government digital identity programme investment create consistent identity verification procurement.

Asia Pacific Identity Verification Market Insights

Asia Pacific is the fastest-growing regional identity verification market, growing at 17.5% CAGR, driven by China’s digital payment ecosystem’s verification requirements, India’s Aadhaar-based digital identity infrastructure enabling KYC, Southeast Asia’s fintech boom, and Japan and South Korea’s digital banking adoption. China accounts for approximately 44.8% of Asia Pacific revenues through its regulatory KYC requirements for digital financial services, the extraordinary WeChat Pay and Alipay transaction volume, and government digital ID programme integration.

India’s Aadhaar eKYC infrastructure whose verification API enables instant identity confirmation from a 1.3 billion person biometric database creates the most commercially scalable identity verification infrastructure of any single country, whose fintech and digital banking adoption creates above-average verification transaction volume growth.

MEA & Latin America Identity Verification Market Insights

UAE leads MEA revenues at approximately 38.4% through its digital banking sector’s KYC compliance, DIFC financial regulation, and the government’s Emirates ID digital identity infrastructure. Brazil leads Latin American revenues at approximately 44.2% through its LGPD data protection compliance, Pix instant payment system’s KYC requirements, and the large fintech sector’s identity verification investment.

Saudi Arabia’s Vision 2030 digital economy investment and South Africa’s financial services sector create significant MEA secondary markets whose verification procurement reflects growing digital financial service adoption across both jurisdictions.

Market Dynamics

Growth Drivers: Regulatory compliance mandates and rising identity fraud costs creating non-discretionary verification investment

Regulatory compliance mandates are the identity verification market’s most commercially certain structural growth driver. KYC and AML requirements across banking, insurance, and financial services, the EU’s 6th Anti-Money Laundering Directive, FinCEN’s beneficial ownership registry, and FATF guidance collectively create legally mandated identity verification investment whose compliance motivation is independent of commercial ROI calculation. Each regulatory tightening cycle and each new jurisdiction’s digital identity compliance framework creates structured procurement expansion that compounds with the global regulatory environment’s progressive strengthening.

Rising identity fraud costs create the most financially compelling commercial motivation for verification investment. The FTC’s 2023 Consumer Sentinel report documented USD 10 billion in fraud losses, creating a loss avoidance financial case whose magnitude sustains premium verification solution investment. Each percentage point reduction in identity fraud loss rate that advanced verification demonstrates creates quantifiable ROI whose calculation directly funds verification solution procurement at scales that justify premium AI-powered solution specification.

Restraints: Privacy regulation creating biometric data collection constraints and user abandonment from friction-intensive verification

Privacy regulation constraints on biometric data collection including GDPR’s special category data protections, Illinois BIPA’s biometric privacy requirements, and equivalent state-level legislation create compliance complexity for biometric identity verification deployment. Each new biometric privacy regulation creates consent management, data minimisation, and retention limitation requirements whose implementation cost and compliance risk moderate biometric verification adoption in affected jurisdictions.

User abandonment from friction-intensive verification workflows creates commercial risk for organisations whose digital onboarding conversion rate directly determines customer acquisition economics. Each verification step that requires document upload, selfie capture, waiting period, or manual review creates abandonment probability whose commercial impact on customer acquisition cost must be weighed against the fraud prevention benefit that thorough verification creates.

Opportunities: AI-powered real-time verification and digital identity ecosystem integration

AI-powered real-time identity verification represents the most commercially differentiated solution direction whose sub-second document authentication, instant liveness detection, and real-time database cross-referencing create verification accuracy and speed that regulatory compliance and user experience simultaneously require. Each AI capability improvement that reduces verification processing time from minutes to seconds while improving accuracy creates both commercial differentiation and regulatory compliance assurance whose combined value sustains premium solution pricing.

Digital identity ecosystem integration creating interoperable identity credentials whose government-issued digital ID acceptance across financial services, healthcare, and government service access creates the commercial infrastructure that reduces verification cost per transaction across the ecosystem. eIDAS 2.0’s EU digital wallet framework, India’s Aadhaar eKYC, and Singapore’s SingPass collectively demonstrate the commercial ecosystem model whose adoption reduces per-verification cost and improves accuracy across participating service providers.

Recent Developments:

-

2024: Experian integrated advanced biometric verification into its fraud prevention solutions in 2024, specifically targeting the BFSI sector with enhanced biometric identity confirmation that improves digital onboarding security amid rising financial fraud losses.

-

2024: LexisNexis Risk Solutions expanded its ThreatMetrix platform in 2024 with enhanced AI-powered device intelligence and behavioural analytics, enabling continuous session authentication that detects account takeover through real-time behavioural monitoring.

-

2024: Jumio launched its AI-powered Jumio KYX Platform with unified identity verification, eKYC, and ongoing monitoring capabilities in 2024, enabling financial institutions to manage complete customer identity lifecycle from onboarding through continuous transaction monitoring within a single integrated platform.

Identity Verification Market Key Players

-

LexisNexis Risk Solutions

-

Experian plc

-

Equifax Inc.

-

IDEMIA

-

Jumio Corporation

-

Onfido (Entrust)

-

Thales Group

-

Mitek Systems

-

Socure

-

Trulioo

-

Veriff

-

IDnow GmbH

-

AuthenticID

-

Prove Identity

-

Acuant (HID Global)

-

Daon

-

iProov

-

Intellicheck

-

TransUnion

-

GB Group plc

Identity Verification Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.79 Billion |

| Market Size by 2035 | USD 4.54 Billion |

| CAGR | CAGR of 4.98% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade (Industrial Grade, Pharmaceutical Grade, Electronic Grade) • By Process (Solvent, Catalyst, Raw Material) • By Application (Pharmaceuticals, Chemical Manufacturing, Paints & Coatings, Textile, Agriculture, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Eastman Chemical Company, Luxi Chemical Group Co. Ltd., Jiutian Chemical Group Co. Ltd., Zhejiang Realsun Chemical Co. Ltd., HELM AG, Merck KGaA, Solvay SA, Thermo Fisher Scientific Inc., Hubei Sanonda Co. Ltd. (ADAMA), Gansu Yinguang Chemical Industry Co. Ltd., Inner Mongolia Yuanxing Energy Co. Ltd., Triveni Chemicals, Archer Daniels Midland Company, Huaqiang Chemical Group, Tokyo Chemical Industry Co. Ltd., Sigma-Aldrich Corporation (Merck), LANXESS AG, Dongyue Group Ltd., and Quzhou Runtu Co. Ltd. |

Frequently Asked Questions

The Dimethylformamide Market was valued at USD 2.79 Billion in 2025.

Pharmaceutical API manufacturing expansion in India and China creating pharmaceutical-grade DMF demand, electronics-grade ultra-high-purity DMF demand from semiconductor fabrication expansion are the primary growth factors.

The Industrial Grade segment dominated the Dimethylformamide Market with approximately 58.4% share in 2025.

North America dominated the Dimethylformamide Market in 2025 with the highest revenue share of 38.9%.

Get in Touch