Wooden Decking Market Report Scope & Overview:

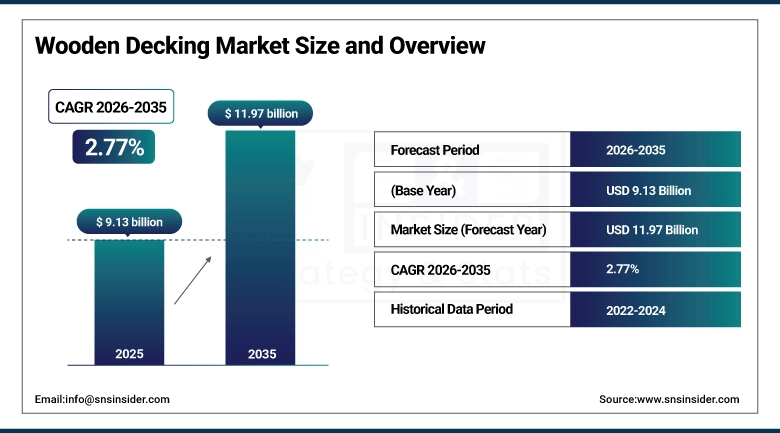

The Wooden Decking Market size was valued at USD 9.13 Billion in 2025 and is projected to reach USD 11.97 Billion by 2035, growing at a CAGR of 2.77% during 2026–2035.

Wooden decking is one of the more stable product categories in outdoor construction, and its 2.77% growth rate reflects that maturity. The market is not driven by technological disruption it is driven by housing activity, renovation spending, and homeowner investment in outdoor living.

Market Size and Forecast:

-

Market Size in 2025: USD 9.13 Billion

-

Market Size by 2035: USD 11.97 Billion

-

CAGR: 2.77% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Wooden Decking Market - Request Free Sample Report

Key Wooden Decking Market Trends:

-

Wood-plastic composites are taking measurable market share from pressure-treated lumber and natural wood species in North America and Europe as homeowners who have experienced the maintenance requirements of natural wood annual sealing, staining, and board replacement shift to low-maintenance composite alternatives that carry manufacturer warranties of 25 to 50 years.

-

Thermally modified and acetylated wood products are gaining traction in European markets as credibly sustainable alternatives that deliver composite-like dimensional stability and decay resistance without the plastic content that some buyers find objectionable from a end-of-life perspective.

-

Outdoor living investment that accelerated through the pandemic years has shifted from initial installation toward maintenance and upgrade activity, increasing the relative weight of the repair, remodeling, and replacement channel within overall market demand in North America and Europe.

-

Non-residential decking applications hotel pool decks, restaurant terraces, public park boardwalks, and marina facilities are growing faster than residential as hospitality and public infrastructure operators specify commercial-grade systems in refurbishment programs that resumed following the pandemic-era pause.

-

Tropical hardwood procurement faces increasing scrutiny from FSC certification requirements, country-of-origin documentation rules, and retailer sustainability commitments that are restricting the market access of uncertified material and supporting premium pricing for verified legal and sustainable supply chains.

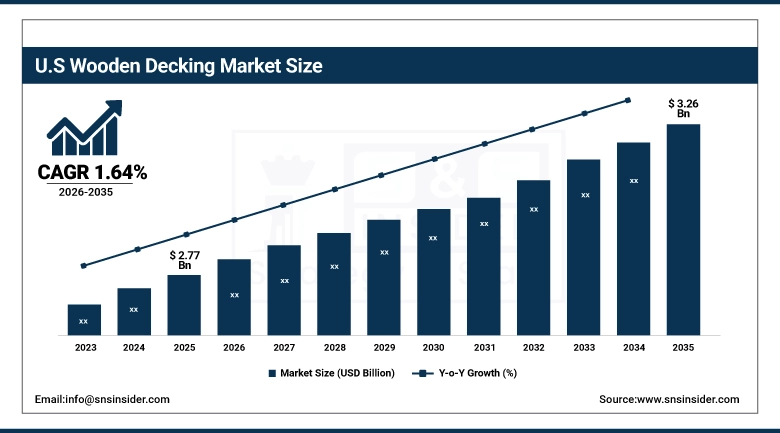

The U.S. Wooden Decking Market was valued at USD 2.77 Billion in 2025, projected to reach USD 3.26 Billion by 2035 at a CAGR of 1.64%, anchored by the highest per-capita outdoor living space construction rate among major economies and a mature home improvement retail sector. Canada holds 17.4% of North American share, growing faster at 3.30% CAGR due to above-average WPC adoption driven by extreme winter weather cycling that accelerates natural wood degradation.

Wooden Decking Market Growth Drivers:

-

Rising Home Improvement Spending, the Aging Housing Stock in Established Markets, and Asia Pacific’s Growing Middle-Class Demand for Outdoor Living Spaces Are Sustaining Multi-Channel Demand Growth

In North America and Europe, growth is primarily maintenance-driven the housing stock that received large volumes of decking installation in the 1990s and 2000s is now reaching replacement cycle for treated lumber products, and homeowners undertaking that replacement are disproportionately choosing WPC or modified wood rather than like-for-like natural wood. The renovation and remodeling channel is capturing this activity and growing at above-market rates in both regions. Separately, the ongoing addition of outdoor living functionality to homes that did not previously have dedicated decked outdoor spaces is a sustained new demand source in suburban and exurban housing markets where lot sizes accommodate expansion. In Asia Pacific, the drivers are different urbanization is expanding the middle class that aspires to outdoor living space, and construction codes in China, Australia, and Southeast Asia are more recently incorporating timber and composite deck systems as standard residential outdoor elements. The installed base is growing from a smaller relative base, generating a faster percentage growth rate than the mature Western markets produce.

Wooden Decking Market Restraints:

-

Raw Material Cost Volatility, Timber Supply Chain Constraints, and the Competitive Pressure from Alternative Decking Materials Are Limiting Market Expansion in Established Segments

Natural wood decking is exposed to lumber price volatility in ways manufacturers cannot fully buffer. The 2020–2022 lumber price cycle which saw pressure-treated lumber prices reach multiples of pre-pandemic levels before correcting sharply created project deferral and prompted some buyers to switch permanently to composite or PVC decking with more stable pricing. Sustainable timber supply constraints are a specific pressure on tropical hardwood FSC-certified tropical species available at commercially viable prices are limited relative to demand, creating sourcing complexity for retailers and distributors who cannot absorb the risk of non-compliant material. Natural wood is also competing against PVC, aluminum composite, and fiber cement decking systems that carry no maintenance requirement and are gaining retail floor space in categories wooden decking previously held without serious competition.

Wooden Decking Market Opportunities:

-

Modified Wood Innovation, Non-Residential Refurbishment Activity, and Asia Pacific Greenfield Demand Are Creating Growth Pathways Outside the Mature North American and European Residential Replacement Cycle

Thermal modification (Thermowood, Retification) and acetylation (Accoya) are producing wood products with dimensional stability, decay resistance, and service life that justify premium pricing relative to both conventional lumber and entry-level composite. These materials sit commercially between commodity natural wood and full plastic composite, appealing to buyers who want natural aesthetics with reduced maintenance. The market for them is growing fastest in Europe, where timber sustainability credentials resonate with specifiers in both residential and non-residential applications. Non-residential refurbishment offers a volume opportunity that residential markets undervalue a single hotel pool deck or marina boardwalk replacement represents the square meterage of dozens of residential installations, and the hospitality investment pipeline deferred through the pandemic years is now actively moving through specification and procurement. Asia Pacific’s greenfield residential and mixed-use development pipeline provides straightforward volume growth from a relatively underpenetrated base that is not yet in the replacement cycle that characterizes mature Western markets.

Wooden Decking Market Segment Analysis:

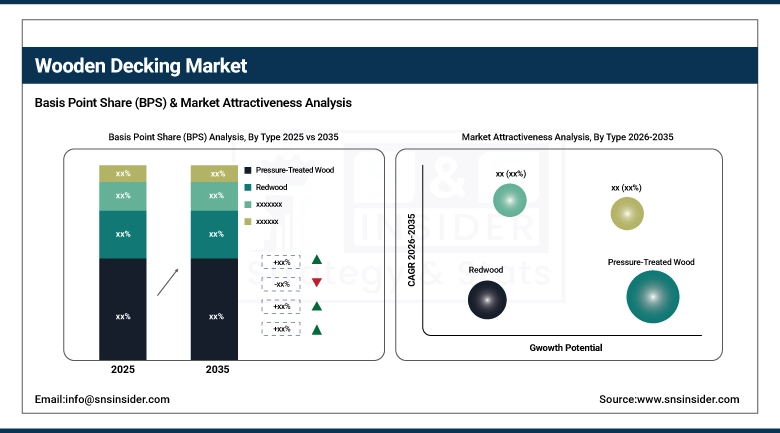

By Type: Pressure-Treated Wood Leads While WPC Drives Fastest Growth Through 2035

Pressure-Treated Wood dominated with a 28.46% share in 2025 at USD 2.60 Billion, while Wood-Plastic Composites (WPC) are expected to grow at the fastest CAGR of approximately 5.23% through 2035. Pressure-treated retains its leading volume share because it is the most cost-accessible natural decking material, widely available through home improvement retail, and the default specification for price-sensitive residential projects. WPC is growing fastest because it converts homeowners who make a single maintenance-motivated decision to switch and those buyers generally do not return to natural wood. The WPC share of 27.92% in 2025 means the gap between pressure-treated and composite is narrow and closing; WPC will likely lead by value before 2035 at current trajectory rates.

By Application: Floor Decking Leads While Railing Drives Fastest Growth Through 2035

Floor Decking (Patios, Balconies, Rooftops) dominated with a 62.48% share in 2025 at USD 5.70 Billion, while Railing is expected to grow at the fastest CAGR of approximately 4.11% through 2035. Floor decking holds its dominant application position because it is the primary functional element of any decked outdoor space the decked surface is what defines the installation and drives the procurement volume. Railing is growing fastest because the commercial and non-residential channel is specifying integrated deck-and-railing systems where railing carries safety certification requirements that add per-linear-foot value, and because the composite railing category in particular is growing as homeowners completing composite deck installations choose matching composite rail rather than the natural wood rail that was the default pairing for pressure-treated lumber systems. Wall and cladding applications are also growing above the market average at 4.41% CAGR as architects and developers incorporate timber and composite cladding into building facades in both residential and commercial construction.

By End-Use: Residential Leads While Non-Residential Drives Fastest Growth Through 2035

Residential dominated with a 68.52% share in 2025 at USD 6.26 Billion, while Non-Residential (Commercial, Hospitality, Public Infrastructure) is expected to grow at the fastest CAGR of approximately 4.12% through 2035. Residential holds its commanding share because the homeowner market is deeper and broader than commercial. Non-residential is growing fastest because hospitality and public infrastructure refurbishment is proceeding at above-residential rates, commercial applications are specifying premium composite and modified wood at above-average per-square-meter values, and urban public space investment in waterfront boardwalks and pedestrian zones is generating procurement that did not exist at this scale a decade ago.

By Construction Type: New Construction Leads While Repair & Remodeling Drives Fastest Growth Through 2035

New Construction dominated with a 41.36% share in 2025 at USD 3.78 Billion, while Repair & Remodeling is expected to grow at the fastest CAGR of approximately 3.52% through 2035. New construction leads because new home builds and new commercial properties create the first installation of decking systems that will subsequently need maintenance and eventual replacement. Repair and remodeling is growing fastest because the housing stock in North America and Europe is aging into its first and second replacement cycle for decking installed in the boom periods of the 1990s and 2000s, and each replacement project tends to involve an upgrade in specification from pressure-treated lumber to WPC, or from entry-level composite to premium composite that increases per-project revenue relative to the original installation.

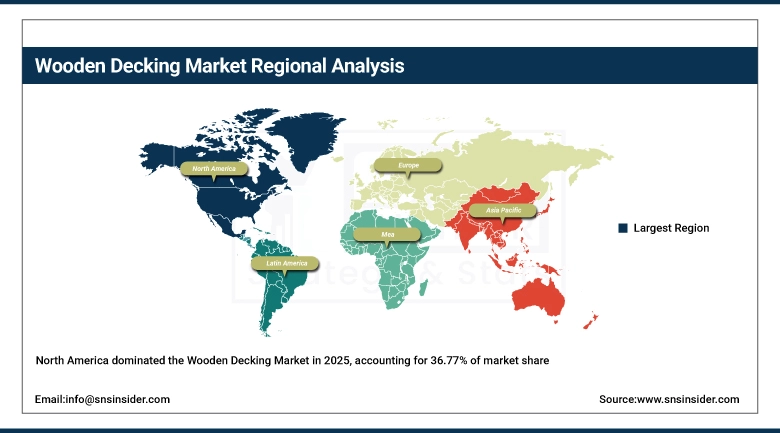

Wooden Decking Market Regional Analysis:

North America Wooden Decking Market Insights

North America dominated in 2025, accounting for 36.77% of market share at USD 3.36 Billion, projected to reach USD 4.06 Billion by 2035 at a CAGR of 1.94%. The United States leads North American demand with an 82.6% regional share at USD 2.77 Billion in 2025, the world’s largest single decking market by value, driven by high single-family home ownership rates, a mature home improvement retail infrastructure, and deep DIY and contractor installation activity across all decking material types.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Wooden Decking Market Insights

Europe held a 24.63% share in 2025 at USD 2.25 Billion, projected to reach USD 2.84 Billion by 2035 at a CAGR of 2.40%. Germany is the dominant national market within Europe, driven by a strong home improvement culture, large single-family housing stock, and active garden and terrace decking investment. The Nordic countries Sweden, Finland, Norway, and Denmark hold disproportionate per-capita decking consumption driven by a deep cultural orientation toward outdoor living and timber construction, and they are among the earliest adopters of thermally modified wood products that originated from Scandinavian forestry innovation.

Asia Pacific Wooden Decking Market Insights

Asia Pacific is expected to grow at the fastest CAGR of approximately 5.59% from 2026 to 2035, rising from USD 1.66 Billion in 2025 to USD 2.86 Billion by 2035. Australia is the dominant national market within the region, with outdoor decking embedded in the residential construction standard at rates comparable to North America, and with a large hardwood and composite decking market served by both domestic and imported product. China is growing fastest within the region as rising middle-class incomes are driving outdoor living space investment in villa-style residential developments and as composite decking systems gain specification in commercial and hospitality construction.

Latin America and Middle East & Africa Wooden Decking Market Insights

Latin America held a 10.28% share in 2025 at USD 939 Million, projected to reach USD 1.10 Billion by 2035 at a CAGR of 1.64%. Brazil leads the Latin American market and is one of the world’s largest consumers of tropical hardwood decking, sourcing domestic species including cumaru, garapa, and ipê from the country’s managed timber sector, though FSC certification requirements are progressively tightening the commercially available supply of export-grade certified material. Middle East & Africa held a 10.18% share in 2025 at USD 929 Million, growing at 1.80% CAGR to USD 1.11 Billion by 2035. The UAE leads the MEA market through high-value hospitality and resort decking specifications, particularly on artificial islands and waterfront developments where hardwood and composite decking systems are specified at premium grades. South Africa is the primary sub-Saharan market.

Competitive Landscape for Wooden Decking Market:

Trex Company, Inc.

Trex is the United States’ largest manufacturer of wood-plastic composite decking and railing, having pioneered the residential composite category in the early 1990s and built a brand position strong enough that “Trex” functions as a category shorthand in North American home improvement retail. Products are manufactured from approximately 95% recycled materials reclaimed wood fiber and polyethylene film.

In January 2025, Trex announced a fourth production line expansion at its Winchester, Virginia facility adding approximately 100 million linear feet of annual composite decking capacity, sized to meet sustained remodeling channel demand and pre-committed retail partner contracts for the 2025 and 2026 selling seasons.

West Fraser Timber Co. Ltd.

West Fraser is one of North America’s largest diversified wood products companies, producing lumber, engineered wood products, pulp, and pressure-treated wood from mills across Canada and the United States. Its decking market participation runs through pressure-treated lumber production supplying residential and commercial decking contractors via big-box retail and independent building supply distribution.

In March 2025, West Fraser announced capacity expansion at its El Dorado, Arkansas facility, adding automated pressure-treatment lines configured for the residential deck lumber dimensions most commonly specified in U.S. South and Midwest markets, sized to meet projected demand increases from residential construction recovery as mortgage rates moderated from their 2023–2024 peak levels.

Wooden Decking Market Key Players:

-

Trex Company, Inc.

-

The AZEK Company Inc.

-

Fiberon

-

UFP Industries, Inc.

-

West Fraser Timber Co. Ltd.

-

Weyerhaeuser Company

-

Stora Enso Oyj

-

UPM-Kymmene Corporation

-

Metsä Group

-

James Hardie Industries plc

-

Accsys Technologies PLC

-

Thermory AS

-

Kebony ASA

-

Setra Group AB

-

Moelven Industrier ASA

-

Vetedy Group

-

Novowood

-

Silvadec

-

Fortress Building Products

-

Fritz EGGER GmbH & Co. OG

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.13 Billion |

| Market Size by 2035 | USD 11.97 Billion |

| CAGR | CAGR of 2.77% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Pressure-Treated Wood, Redwood, Cedar, Tropical Hardwood, Wood-Plastic Composites (WPC), and Others (Thermally Modified Wood, Acetylated Wood)) • By Application (Floor Decking (Patios, Balconies, Rooftops), Railing, Wall / Cladding, and Others) • By End-Use (Residential and Non-Residential (Commercial, Hospitality, Public Infrastructure)) • By Construction Type (New Construction, Repair & Remodeling, and Replacement / Renovation) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Trex Company, Inc.; The AZEK Company Inc.; Fiberon; UFP Industries, Inc.; West Fraser Timber Co. Ltd.; Weyerhaeuser Company; Stora Enso Oyj; UPM-Kymmene Corporation; Metsä Group; James Hardie Industries plc; Accsys Technologies PLC; Thermory AS; Kebony ASA; Setra Group AB; Moelven Industrier ASA; Vetedy Group; Novowood; Silvadec; Fortress Building Products; Fritz EGGER GmbH & Co. OG. |

Frequently Asked Questions

North America dominated the Wooden Decking Market in 2025.

Pressure-Treated Wood dominated the Wooden Decking Market

Rising residential outdoor living trends, increasing home renovation activities, and growing demand for durable, low-maintenance composite decking materials are driving the Wooden Decking Market.

The Wooden Decking Market size was USD 9.13 Billion in 2025 and is expected to reach USD 11.97 Billion by 2035.

The Wooden Decking Market is expected to grow at a CAGR of 2.77% from 2026 to 2035.

Get in Touch