Zeolite Molecular Sieves Market Report Scope & Overview:

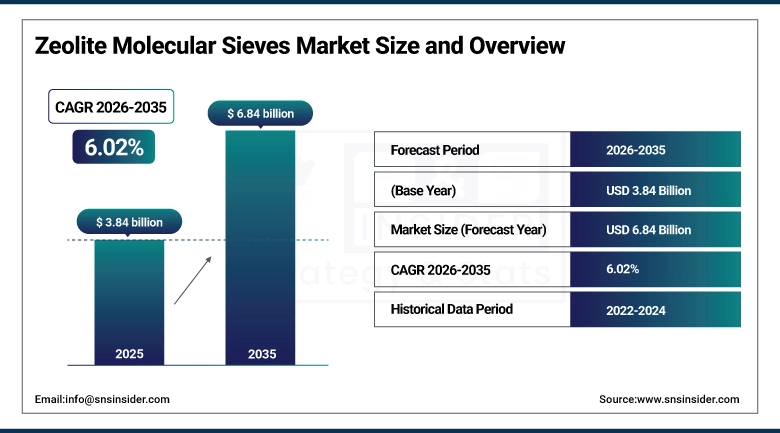

The Zeolite Molecular Sieves Market size was valued at USD 3.84 Billion in 2025 and is projected to reach USD 6.84 Billion by 2035, growing at a CAGR of 6.02% during 2026–2035.

Zeolite molecular sieves are crystalline aluminosilicate materials with uniform pore structures that selectively adsorb molecules by size and polarity. They function as adsorbents, catalysts, and desiccants across petrochemical refining, air separation, water treatment, detergent manufacturing, and pharmaceutical applications. The 3A, 4A, 5A, and 13X types cover the majority of industrial desiccant and separation demand; ZSM-5 and Beta zeolites serve catalytic refinery and chemical synthesis.

Market Size and Forecast:

-

Market Size in 2025: USD 3.84 Billion

-

Market Size by 2035: USD 6.84 Billion

-

CAGR: 6.02% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Zeolite Molecular Sieves Market - Request Free Sample Report

Key Zeolite Molecular Sieves Market Trends

-

Expanding air separation plant construction for industrial oxygen and nitrogen supply is increasing 5A and 13X zeolite consumption as pressure swing adsorption units replace legacy cryogenic systems in mid-scale applications.

-

Phosphate-free detergent regulations in Europe and North America, replacing sodium tripolyphosphate with zeolite 4A as a builder, continue to drive volume demand in household and commercial cleaning product manufacturing.

-

ZSM-5 and Beta zeolite catalyst demand is growing with refinery FCC unit optimization programs and the expansion of petrochemical complexes in Asia Pacific and the Middle East targeting propylene and aromatics production.

-

Water treatment applications in municipal and industrial facilities are adopting zeolite-based ion exchange and adsorption systems for ammonium, heavy metal, and radioactive contaminant removal alongside conventional coagulation processes.

-

Pharmaceutical and biotech sector adoption of zeolite molecular sieves for controlled drug delivery, excipient desiccation, and chromatographic separation is a nascent but fast-growing demand channel with higher unit value than industrial bulk applications.

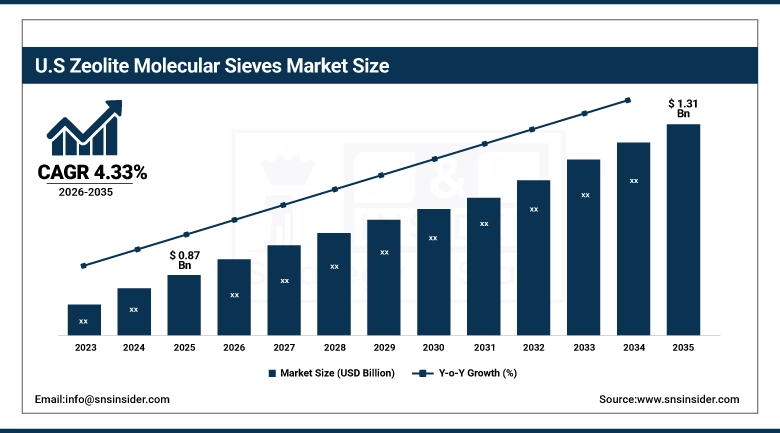

The U.S. Zeolite Molecular Sieves Market size was valued at USD 0.87 Billion in 2025 and is projected to reach USD 1.31 Billion by 2035, growing at a CAGR of 4.33% during 2026–2035. The US market is driven by natural gas dehydration in the upstream oil and gas sector, where 3A and 4A zeolites are the standard desiccant for pipeline specification moisture removal.

Zeolite Molecular Sieves Market Growth Drivers:

-

Refinery and Petrochemical Catalyst Demand Anchors the Largest Application Segment as FCC and Hydrocracking Units Consume ZSM-5 and Y-Zeolite Catalysts at Regular Replacement Intervals Across Global Refinery Operations

FCC units use zeolite Y and ZSM-5 as active catalyst components that degrade during operation, requiring continuous fresh catalyst addition a recurring procurement cycle independent of new unit construction. ZSM-5 is also the primary catalyst in propylene maximization FCC operations and methanol-to-olefins units expanding in China and Southeast Asia. Hydrocracking units consuming zeolite bifunctional catalysts are being commissioned in the Middle East and Asia Pacific as refiners upgrade heavy crude processing. Each new FCC or hydrocracker represents a decade-scale catalyst procurement relationship, and combined capacity additions across these regions will generate substantial incremental zeolite demand.

Zeolite Molecular Sieves Market Restraints:

-

Competition from Alternative Adsorbents Including Silica Gel, Activated Alumina, and Activated Carbon Limits Zeolite Penetration in Cost-Sensitive Desiccant Applications Where Pore Selectivity Is Not a Differentiating Requirement

Silica gel and activated alumina serve overlapping desiccant functions in packaging and general moisture control at lower cost than synthetic zeolites. In applications where pore-size selectivity is not required pharmaceutical packaging inserts, consumer goods sachets, electronic storage buyers specify silica gel on price per gram of moisture capacity. Activated carbon competes in gas-phase organic contaminant removal where its high surface area and low cost serve non-polar molecule adsorption needs. Zeolites retain advantages in selective separations and reactive gas dehydration, but these do not extend to all moisture control segments, limiting penetration where the price premium lacks performance justification.

Zeolite Molecular Sieves Market Opportunities:

-

Healthcare and Pharmaceutical Sector Adoption of Zeolite Molecular Sieves for Drug Delivery, Desiccation, and Bioprocess Applications Opens a High-Value Growth Channel with Unit Economics Substantially Above Bulk Industrial Desiccant Markets

Pharmaceutical-grade zeolite is used as desiccant in moisture-sensitive drug packaging, as excipient in controlled-release tablet formulations where pore structure modulates release kinetics, and in bioprocessing chromatography and fermentation gas conditioning. Medical oxygen concentrators for home healthcare consume 13X zeolite in PSA beds, and aging-population home oxygen therapy expansion across North America, Europe, and Asia Pacific grows this channel. Unit prices in pharmaceutical applications run many multiples above commodity desiccant, making pharmaceutical-grade supply strategically attractive for producers meeting USP and EP standards.

Zeolite Molecular Sieves Market Segment Analysis

-

By Product Type / Zeolite Type, 13X Zeolite dominated with 19.38% share in 2025, and Beta Zeolite is expected to grow at the fastest CAGR of 8.02% from 2026 to 2035.

-

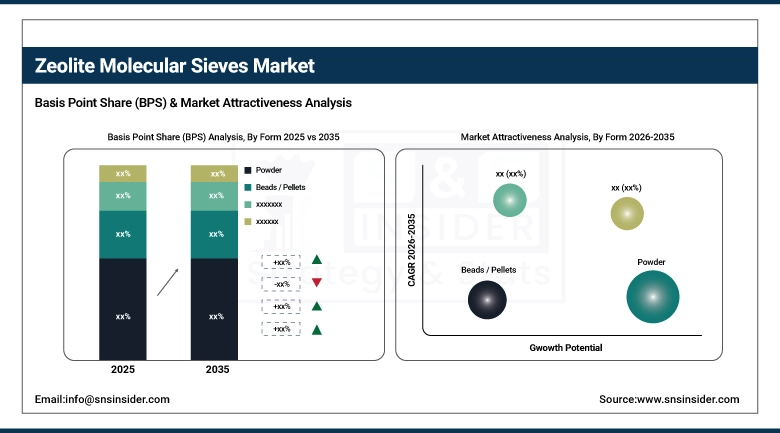

By Form, Powder dominated with 34.18% in 2025, and Granules is expected to grow at the fastest CAGR of 6.61% from 2026 to 2035.

-

By Application, Petrochemicals & Refining dominated with 32.86% in 2025, and Pharmaceuticals & Biotech is expected to grow at the fastest CAGR of 8.19% from 2026 to 2035.

-

By End-Use Industry, Petrochemical & Chemical Industry dominated with 24.36% in 2025, and Healthcare & Pharmaceuticals is expected to grow at the fastest CAGR of 8.00% from 2026 to 2035.

By Form – Powder Form Leads While Granules Register the Fastest CAGR Through 2035

Powder form holds the leading position within the form segmentation, widely used in detergent manufacturing as a phosphate builder replacement and in catalyst preparation where fine particle size is essential for extrusion into formed bodies. Granules register the fastest growth, gaining preference in water treatment and pharmaceutical handling environments where the physical form offers practical advantages over powder in terms of dust control, flow characteristics, and dosing precision.

By Product Type / Zeolite Type – 13X Zeolite Leads the Market While Beta Zeolite Drives the Fastest Growth Through 2035

13X Zeolite holds the leading share within the product type segmentation, driven by its wide pore aperture and high adsorption capacity for water, carbon dioxide, hydrogen sulfide, and mercaptans, which make it the standard choice in natural gas purification, air pre-purification, and medical oxygen concentrators. Beta Zeolite is growing fastest, supported by expanding specialty chemical and petrochemical synthesis applications where its large pore structure and strong acidity deliver superior catalytic performance.

By Application – Petrochemicals & Refining Lead While Pharmaceuticals & Biotech Drive the Fastest Growth Through 2035

Petrochemicals and refining hold the dominant application share, anchored by fluid catalytic cracking and hydrocracking operations that consume zeolite catalysts on continuous replacement cycles across global refinery networks. Pharmaceuticals and biotech is growing fastest, driven by expanding use of molecular sieves in medical oxygen concentration, moisture-sensitive drug packaging, controlled-release tablet formulations, and bioprocessing environments where precise adsorption selectivity and high purity specifications are mandatory.

By End-Use Industry – Petrochemical & Chemical Industry Leads While Healthcare & Pharmaceuticals Registers the Fastest CAGR Through 2035

Petrochemical and chemical industry holds the leading end-use share, sustained by consistent zeolite catalyst and adsorbent procurement across refining, gas processing, and chemical synthesis operations that collectively represent the largest volume demand base. Healthcare and pharmaceuticals registers the fastest growth, propelled by rising medical oxygen concentrator deployments, pharmaceutical-grade desiccant requirements in drug packaging, and expanding bioprocess applications where zeolite molecular sieves meet stringent purity and performance standards.

Zeolite Molecular Sieves Market Report Analysis

North America Zeolite Molecular Sieves Market Insights

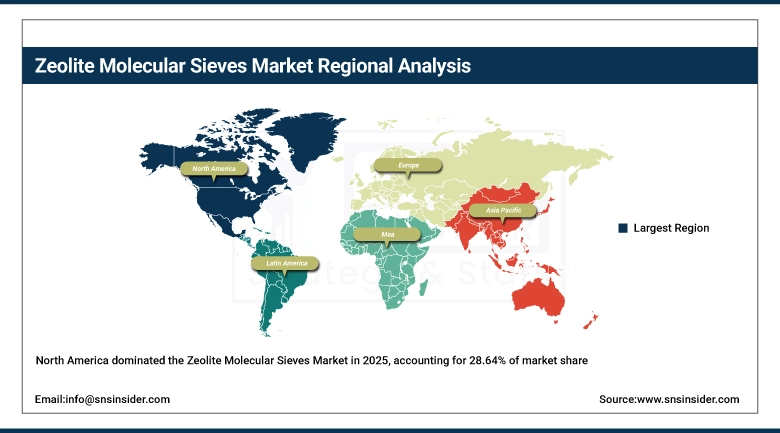

North America accounted for 28.64% of the Zeolite Molecular Sieves Market in 2025, valued at USD 1.10 Billion, and is projected to reach USD 1.72 Billion by 2035 at a CAGR of 4.66% during the forecast period. North America’s market is anchored by the US upstream and midstream natural gas industry, which consumes 3A and 4A zeolites for pipeline dehydration across the Permian Basin, Appalachian, and offshore Gulf Coast production areas. Refinery FCC and hydrocracking catalyst demand at US refineries among the world’s largest by throughput provides steady zeolite catalyst procurement. Industrial air separation plants serving steel mills, chemical plants, and medical gas distributors in the US and Canada consume 5A and 13X zeolites in PSA adsorber vessels. Domestic production is concentrated among Zeolyst International, PQ Corporation, and Honeywell UOP, with additional supply from European and Asian producers through established distribution networks.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Zeolite Molecular Sieves Market Insights

The United States accounts for 78.64% of North American demand in 2025. The U.S. Zeolite Molecular Sieves Market was valued at USD 0.87 Billion in 2025 and is projected to reach USD 1.31 Billion by 2035, growing at a CAGR of 4.33% during 2026–2035. US leadership reflects large refining throughput, extensive gas processing infrastructure, and an established industrial gas sector. Canada contributes through oil sands gas processing and natural gas dehydration in western Canada.

Europe Zeolite Molecular Sieves Market Insights

Europe held a 24.18% share of the Zeolite Molecular Sieves Market in 2025, valued at USD 0.93 Billion, and is expected to reach USD 1.55 Billion by 2035 at a CAGR of 5.31% during the forecast period. European demand is supported by a large detergent manufacturing sector consuming zeolite 4A as a phosphate builder replacement under EU phosphate restrictions, refinery zeolite catalyst demand at major Western European refineries, and a well-developed pharmaceutical industry consuming pharmaceutical-grade desiccant and catalyst-grade zeolites. Germany, France, the UK, and the Netherlands host the primary manufacturing and consumption operations. BASF SE and Clariant AG are significant European zeolite producers with global supply positions, supporting both domestic European demand and international export markets.

Germany Zeolite Molecular Sieves Market Insights

Germany leads the European market through BASF’s Ludwigshafen zeolite manufacturing, refinery FCC and hydrocracking catalyst demand, and a detergent industry formulating phosphate-free products with zeolite 4A for several decades. German pharmaceutical and specialty chemical manufacturers add a premium-value demand channel consuming high-purity zeolite grades in synthesis and purification.

Asia Pacific Zeolite Molecular Sieves Market Insights

Asia Pacific grows at 7.34% CAGR, rising from USD 1.22 Billion in 2025 to USD 2.46 Billion by 2035, both the largest and fastest-growing region. China drives demand through FCC catalyst, detergent manufacturing, PSA air separation, and pharmaceutical applications. India’s PSA medical oxygen capacity additions following COVID-19-related supply shortages are a significant 13X zeolite demand driver. Japan and South Korea contribute through specialty chemical and pharmaceutical applications at above-commodity unit values.

China Zeolite Molecular Sieves Market Insights

China is the dominant Asia Pacific market and the world’s largest zeolite producer and consumer. FCC catalyst consumption is driven by refining capacity ranked second globally by throughput. Hengye Group, Shanghai Jiuzhou Chemicals & Materials, and Luoyang Jalon Micro-Nano New Materials supply both domestic demand and export markets. Gas processing, petrochemical, and PSA air separation capacity additions continue to add zeolite demand through 2035.

Latin America (LATAM) and Middle East & Africa (MEA) Zeolite Molecular Sieves Market Insights

Latin America held 7.36% of the global market in 2025 at USD 0.28 Billion, reaching USD 0.55 Billion by 2035 at 6.87% CAGR. Brazil and Mexico drive demand through refinery catalyst procurement, gas processing dehydration, and detergent manufacturing. Middle East & Africa held 8.10% at USD 0.31 Billion in 2025, growing to USD 0.56 Billion at 6.20% CAGR. Saudi Arabia, UAE, and Kuwait refinery and petrochemical expansions adding FCC and hydrocracking capacity are the primary regional zeolite catalyst growth driver alongside gas export infrastructure dehydration applications.

Competitive Landscape for Zeolite Molecular Sieves Market:

BASF SE is a global leader in zeolite catalyst and adsorbent production, supplying zeolite-based FCC catalysts, hydroprocessing catalysts, and desiccant molecular sieves through its Catalysts division. BASF’s zeolite manufacturing at its Ludwigshafen, Germany, and US facilities serves global refinery, chemical, and adsorbent customers with products spanning Y-zeolite, ZSM-5, and Beta zeolite catalyst systems alongside 3A, 4A, and 13X desiccant grades.

- In February 2025, BASF announced expanded zeolite catalyst production capacity at its Iselin, New Jersey facility, targeting growing FCC catalyst demand from North American and Latin American refineries upgrading to higher propylene and light olefin yield configurations.

Honeywell International Inc. (UOP) supplies zeolite molecular sieves through its UOP process technology business, which holds leading positions in zeolite adsorbent supply for paraxylene separation, natural gas dehydration, and air separation applications. UOP’s adsorbent portfolio includes ADS-series and MOLSIV molecular sieves manufactured at its Baton Rouge, Louisiana facility, supplying global refinery, petrochemical, and gas processing customers under long-term adsorbent supply and bed change-out service agreements.

- In April 2025, Honeywell UOP introduced a new 13X molecular sieve formulation with improved CO₂ adsorption capacity targeting PSA air pre-purification units at cryogenic air separation plants, with projected performance improvements of 8–12% in bed cycle duration compared to the prior-generation product.

Zeolite Molecular Sieves Market Key Players:

-

BASF SE

-

Honeywell International Inc. (UOP)

-

Tosoh Corporation

-

Arkema Group

-

Zeochem AG

-

Axens

-

KNT Group

-

Chemiewerk Bad Köstritz GmbH

-

Zeolyst International

-

Union Showa K.K.

-

PQ Corporation

-

Kuraray Co., Ltd.

-

Albemarle Corporation

-

Hengye Group

-

Shanghai Jiuzhou Chemicals & Materials

-

Sorbead India Pvt. Ltd.

-

Tricat Group

-

Luoyang Jalon Micro-Nano New Materials

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.84 Billion |

| Market Size by 2035 | USD 6.84 Billion |

| CAGR | CAGR of 6.02% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type / Zeolite Type (3A Zeolite, 4A Zeolite, 5A Zeolite, 13X Zeolite, ZSM-5 Zeolite, Beta Zeolite, and Others) • By Form (Powder, Beads / Pellets, Granules, and Sheets / Disks) • By Application (Petrochemicals & Refining, Water Treatment, Air Separation (Oxygen/Nitrogen Production), Detergents & Cleaning Agents, Pharmaceuticals & Biotech, and Others) • By End-Use Industry (Oil & Gas, Petrochemical & Chemical Industry, Water Treatment Industry, Detergents & Household Cleaning, Healthcare & Pharmaceuticals, Automotive & Industrial Manufacturing, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Clariant AG, Honeywell International Inc. (UOP), Tosoh Corporation, Arkema Group, W. R. Grace & Co., Zeochem AG, Axens, KNT Group, Chemiewerk Bad Köstritz GmbH, Zeolyst International, Union Showa K.K., PQ Corporation, Kuraray Co., Ltd., Albemarle Corporation, Hengye Group, Shanghai Jiuzhou Chemicals & Materials, Sorbead India Pvt. Ltd., Tricat Group, Luoyang Jalon Micro-Nano New Materials |

Frequently Asked Questions

Asia Pacific dominated the Zeolite Molecular Sieves Market in 2025 with a 31.72% share.

13X Zeolite dominated the Zeolite Molecular Sieves Market with a 19.38% share in 2025.

The key drivers of the Zeolite Molecular Sieves market are refinery and petrochemical FCC catalyst demand, industrial air separation and natural gas dehydration adsorbent consumption, phosphate-free detergent formulation adoption, and growing pharmaceutical-grade zeolite applications in drug delivery and medical oxygen concentration.

The Zeolite Molecular Sieves Market size was USD 3.84 Billion in 2025 and is expected to reach USD 6.84 Billion by 2035.

The Zeolite Molecular Sieves Market is expected to grow at a CAGR of 6.02% from 2026–2035.

Get in Touch