Zinc Chloride Market Report Scope & Overview:

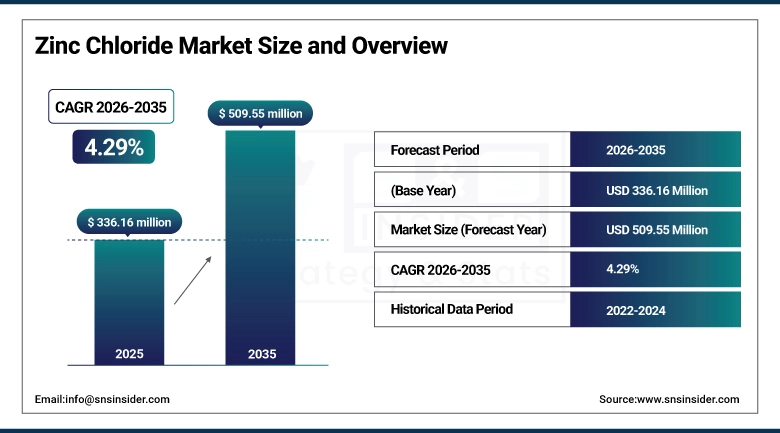

The Zinc Chloride Market size was valued at USD 336.16 Million in 2025 and is projected to reach USD 509.55 Million by 2035, growing at a CAGR of 4.29% during 2026–2035.

Zinc chloride (ZnCl₂) is an inorganic salt produced by reacting zinc metal or zinc oxide with hydrochloric acid. It is sold in powder, liquid solution, and granule forms across four purity grades: high purity, battery, technical, and commercial. Battery grade serves dry cell battery electrolyte requirements. High purity grades are specified in pharmaceutical synthesis and electronics soldering flux. Technical and commercial grades cover water treatment, metallurgical fluxing, and general chemical manufacturing.

Zinc Chloride Market Size and Forecast:

-

Market Size in 2025: USD 336.16 Million

-

Market Size by 2035: USD 509.55 Million

-

CAGR: 4.29% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Zinc Chloride Market - Request Free Sample Report

Key Zinc Chloride Market Trends:

-

Battery-grade zinc chloride procurement is shifting from spot purchasing to long-term supply agreements as dry cell battery manufacturers seek to stabilize input costs against zinc price volatility on the London Metal Exchange.

-

Water treatment applications are gaining volume as aging municipal water infrastructure in North America and Europe undergoes replacement, increasing the number of distribution systems requiring corrosion inhibitor treatment.

-

High-purity zinc chloride demand from the pharmaceutical sector is growing with the expansion of generics manufacturing in India and China, where zinc chloride is used as a Lewis acid catalyst in several API synthesis routes.

-

Liquid zinc chloride solution is gaining share against powder form in applications where on-site dissolution handling is a safety and logistics concern, particularly in water treatment and textile processing facilities.

-

Environmental scrutiny of zinc discharge in textile wastewater is prompting some processors in Western Europe to reduce zinc chloride consumption or substitute alternative mordants, creating modest headwinds in that application segment.

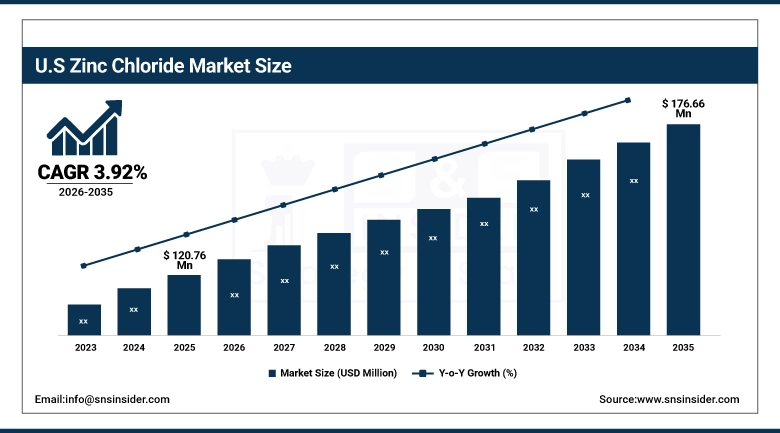

The U.S. Zinc Chloride Market was valued at USD 120.76 Million in 2025 and is projected to reach USD 176.66 Million by 2035, growing at a CAGR of 3.92% during 2026–2035. Dry cell battery manufacturers in the US consume zinc chloride as an electrolyte constituent in carbon-zinc cells still sold in high-volume, low-drain consumer applications remote controls, clocks, toys, and flashlights. Municipal water treatment systems procure zinc chloride for corrosion inhibition in distribution pipe networks. US pharmaceutical manufacturers use high-purity zinc chloride in API synthesis and as a reagent in organic chemistry applications. Domestic production is handled by a small number of specialty inorganic chemical producers, with imports from China supplementing domestic supply during periods of high demand or raw material constraint.

Zinc Chloride Market Growth Drivers:

-

Dry Cell Battery Production Volume Sustains the Largest Single Application Demand for Zinc Chloride as Carbon-Zinc Cells Retain Market Share in High-Volume Low-Cost Consumer Battery Segments Across Asia, Africa, and Latin America

Carbon-zinc batteries remain the dominant chemistry in price-sensitive markets across Asia Pacific, sub-Saharan Africa, and Latin America, where the retail price gap against alkaline is a decisive purchasing factor. Billions of carbon-zinc cells are sold annually through informal retail and small electronics vendors. Each cell contains zinc chloride solution as the active electrolyte, making cell production volume the direct multiplier for zinc chloride demand. Dry cell batteries account for 29.64% of zinc chloride application demand in 2025, valued at USD 99.64 Million. Manufacturing in China, India, and Southeast Asia anchors Asia Pacific as the primary production geography.

Zinc Chloride Market Restraints:

-

Substitution Pressure from Alkaline Batteries in Consumer Electronics Is Gradually Eroding the Volume Base of Carbon-Zinc Battery Production, Reducing Per-Year Zinc Chloride Consumption Growth in the Largest Single Application Segment

Alkaline battery penetration is rising steadily in Southeast Asia, Latin America, and Eastern Europe as incomes grow. Retailers shift shelf space from carbon-zinc to alkaline, and promotional pricing by alkaline producers accelerates urban substitution. Simultaneously, the consumer electronics shift toward rechargeable lithium-ion devices reduces total primary battery volumes in developed markets. Carbon-zinc will not disappear its cost position keeps it in the lowest-price retail tiers globally but volume growth in this segment is structurally limited, constraining the demand contribution from the market’s largest application category.

Zinc Chloride Market Opportunities:

-

Pharmaceutical and High-Purity Chemical Manufacturing Expansion in Asia Pacific Creates Growing Demand for Pharmaceutical-Grade Zinc Chloride as a Lewis Acid Catalyst and Reagent in Organic Synthesis and API Manufacturing Processes

Zinc chloride is a Lewis acid catalyst used in Friedel-Crafts alkylation, dehydration, and condensation reactions in pharmaceutical API, agrochemical intermediate, and specialty chemical synthesis. India’s API manufacturing industry uses it in established synthesis protocols; Chinese fine chemical producers consume high-purity grades at growing volumes tied to pharmaceutical and agrochemical export expansion.

Zinc Chloride Market Segment Analysis:

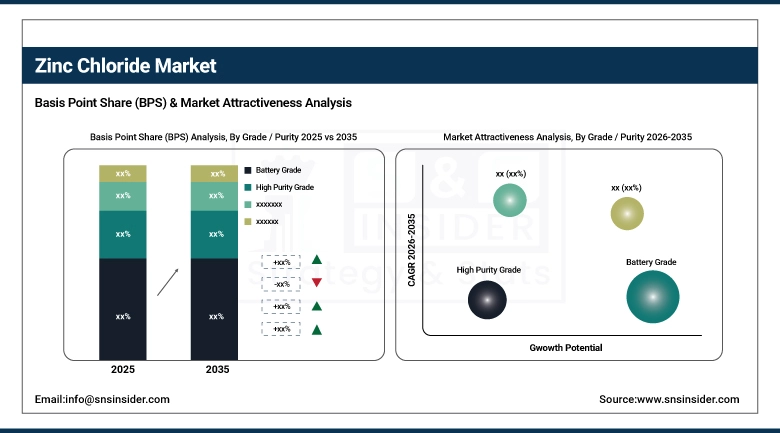

By Grade / Purity: Battery Grade Leads While High Purity Grade Registers the Fastest CAGR Through 2035

Battery Grade dominated with a 28.47% share in 2025, valued at approximately USD 95.70 Million, while High Purity Grade is expected to grow at the fastest CAGR of approximately 5.12% through 2035.

Battery grade leads because dry cell battery manufacturers globally specify this grade across carbon-zinc production in China, India, and Indonesia. It meets electrochemical requirements without the additional cost of pharmaceutical purification. High purity grows fastest as pharmaceutical synthesis, soldering flux, and specialty textile applications require tighter heavy metal limits and assay specifications than battery grade provides. Technical grade covers metallurgical and wood preservation uses; commercial grade serves bulk chemical and agricultural applications where purity requirements are minimal.

By Form: Liquid / Solution Leads While Liquid / Solution Also Registers the Fastest CAGR Through 2035

Liquid / Solution dominated with a 46.58% share in 2025, valued at approximately USD 156.58 Million, while Liquid / Solution is also expected to grow at the fastest CAGR of approximately 4.81% through 2035.

Liquid solution leads because water treatment utilities, textile processors, and chemical manufacturers prefer aqueous zinc chloride that meters directly into process streams without dissolution steps. Water treatment is served almost exclusively by liquid solution at utility-specified concentrations for controlled distribution system dosing. Powder holds 34.72% share, serving battery electrolyte preparation and pharmaceutical reagent applications where solid-state handling is standard. Granules serve metallurgical flux and wood preservation uses where physical form aids controlled application rates.

By Application: Dry Cell Batteries Lead While Water Treatment Registers the Fastest CAGR Through 2035

Dry Cell Batteries dominated with a 29.64% share in 2025, valued at approximately USD 99.64 Million, while Water Treatment is expected to grow at the fastest CAGR of approximately 5.54% through 2035.

Dry cell batteries dominate because carbon-zinc cell production in China, India, and Indonesia consumes zinc chloride electrolyte at volumes exceeding any other single application. The segment grows at 3.73% CAGR, below market average due to alkaline substitution headwinds. Water treatment grows fastest at 6.13% CAGR (USD 56.54 Million to USD 96.61 Million by 2035) as North American municipal programs expand zinc orthophosphate treatment.

By End-Use Industry: Electronics & Batteries Lead While Electronics & Batteries Also Registers Among the Fastest CAGRs Through 2035

Electronics & Batteries dominated with a 24.92% share in 2025, valued at approximately USD 83.77 Million, and it is also expected to grow at a CAGR of approximately 5.05% through 2035.

Electronics and batteries lead by aggregating dry cell battery manufacturing and PCB soldering flux consumption, the two largest volume applications in the industrial supply chain. Chemical industry at 21.38% is the second-largest, consuming zinc chloride across catalyst, reagent, and intermediate manufacturing.

Zinc Chloride Market Regional Analysis:

North America Zinc Chloride Market Insights

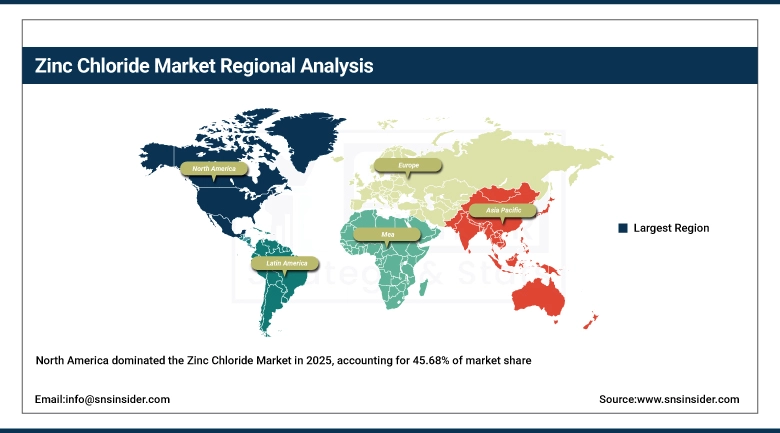

North America dominated the Zinc Chloride Market in 2025, accounting for 45.68% of market share, valued at USD 153.56 Million, and is projected to reach USD 228.89 Million by 2035 at a CAGR of 4.11% during the forecast period.

North America’s lead reflects large water treatment infrastructure, dry cell battery distribution, pharmaceutical chemical procurement, and galvanizing industry consumption. US municipal water systems are the single largest concentration of zinc chloride corrosion inhibition demand, with thousands of utilities running zinc orthophosphate programs under EPA Lead and Copper Rule compliance. Steel galvanizers, flux producers, and chemical manufacturers add further volume through domestic producers including Zaclon LLC and American Elements.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Zinc Chloride Market Insights

The United States accounts for 78.64% of North American demand in 2025. The U.S. Zinc Chloride Market was valued at USD 120.76 Million in 2025 and is projected to reach USD 176.66 Million by 2035, growing at a CAGR of 3.92% during 2026–2035. EPA Lead and Copper Rule requirements and aging pipe replacement programs provide a multi-decade water treatment demand base tied to infrastructure spending cycles.

Europe Zinc Chloride Market Insights

Europe held a 20.92% share of the Zinc Chloride Market in 2025, valued at USD 70.32 Million, and is expected to reach USD 116.38 Million by 2035 at a CAGR of 5.21% during the forecast period. European demand is distributed across water treatment in the UK, France, and Germany, textile processing in Italy, Spain, and Eastern Europe, pharmaceutical chemical manufacturing in Germany and Switzerland, and electronics flux applications in electronics manufacturing hubs across Germany, Poland, and the Czech Republic. REACH regulations governing zinc compound use in industrial applications require downstream user documentation and exposure assessments, adding compliance costs for European zinc chloride users but not eliminating consumption in essential applications.

Germany Zinc Chloride Market Insights

Germany leads the European zinc chloride market through its pharmaceutical chemical industry, electronics manufacturing base, and galvanizing sector. German pharmaceutical and fine chemical companies including Merck KGaA consume high-purity zinc chloride in synthesis applications. The country’s automotive and machinery manufacturing sectors generate demand through galvanizing flux applications in surface treatment operations serving industrial component supply chains.

Asia Pacific Zinc Chloride Market Insights

Asia Pacific is expected to grow at a CAGR of approximately 5.29% from 2026 to 2035, rising from USD 65.25 Million in 2025 to USD 108.89 Million by 2035. China dominates regional consumption through carbon-zinc battery manufacturing the world’s largest concentration alongside textile processing, pharmaceutical API synthesis, and agricultural chemical manufacturing. India’s API manufacturing growth adds pharmaceutical-grade zinc chloride demand at above-average rates. Southeast Asian textile producers in Vietnam, Bangladesh, and Indonesia consume zinc chloride in fabric processing, with volume growing alongside apparel export production expansion.

China Zinc Chloride Market Insights

China is the dominant Asia Pacific market and a major producer. Battery manufacturers supplying carbon-zinc cells to domestic and African export markets are the primary consumption anchor. Weifang Dongfangsheng Chemical, Hisky Zinc Industry, Tianjin Nanping Chemical, and Jiangsu Shenlong Zinc Industry supply zinc chloride across battery, textile, pharmaceutical, and chemical applications from Shandong, Tianjin, and Jiangsu production bases.

Latin America and Middle East & Africa Zinc Chloride Market Insights

Latin America held approximately 8.11% of the global Zinc Chloride Market in 2025, valued at USD 27.26 Million, and is expected to reach USD 32.41 Million by 2035 at a CAGR of 1.76% during the forecast period. Brazil and Mexico are the primary markets, with carbon-zinc battery consumption and textile processing as the main demand drivers. The region’s below-average CAGR reflects the faster substitution of carbon-zinc batteries by alkaline in Latin American urban retail markets relative to Asia Pacific. Middle East & Africa held approximately 5.88% of market share in 2025, valued at USD 19.77 Million, and is expected to reach USD 22.98 Million by 2035 at a CAGR of 1.53% during the forecast period. Sub-Saharan African markets continue to consume carbon-zinc batteries in volume, but regional zinc chloride procurement is largely handled through import rather than domestic production.

Competitive Landscape for Zinc Chloride Market:

TIB Chemicals AG

TIB Chemicals AG is a German specialty inorganic chemical producer with zinc chloride among its core product lines, supplying pharmaceutical-grade, technical-grade, and commercial-grade material to European customers across pharmaceutical manufacturing, water treatment, and electronics applications. The company’s European manufacturing base provides logistics advantages to customers in Germany, Benelux, and Central Europe relative to import alternatives from Asia.

In March 2025, TIB Chemicals expanded its zinc chloride production line at its Mannheim facility, adding capacity for pharmaceutical-grade material to serve growing demand from German and Swiss API manufacturers requiring batch documentation and Certificate of Analysis standards aligned with EU GMP requirements for pharmaceutical excipients and reagents.

Zaclon LLC

Zaclon LLC, based in Cleveland, Ohio, is a US producer of zinc chloride supplying battery manufacturers, water treatment utilities, and industrial customers across North America. The company’s production from domestic raw materials serves customers requiring US-origin supply documentation, including federal water treatment programs and defense-related manufacturing applications subject to Buy American procurement requirements.

In January 2025, Zaclon LLC announced supply agreements with two major US municipal water authorities for liquid zinc chloride solution delivery under multi-year contracts structured around the EPA Lead and Copper Rule Revisions implementation timeline, securing volume commitments from utilities expanding corrosion inhibitor treatment programs to meet the 2024 rule’s enhanced compliance requirements.

Zinc Chloride Market Key Players:

-

TIB Chemicals AG

-

Zaclon LLC

-

Global Chemical Co., Ltd.

-

Pan-Continental Chemical Co., Ltd.

-

Eurocontal SA

-

Weifang Dongfangsheng Chemical Co., Ltd.

-

Hisky Zinc Industry Co., Ltd.

-

Tianjin Nanping Chemical Co., Ltd.

-

Jiangsu Shenlong Zinc Industry Co., Ltd.

-

Xiamen Ditai Chemicals Co., Ltd.

-

Vijaychem Industries

-

Merck KGaA

-

Zinc Nacional

-

Airedale Chemical Company Limited

-

S.A. Lipmes

-

Vinipul Inorganics Private Limited

-

Suchem Industries

-

Hindustan Zinc Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 336.16 Million |

| Market Size by 2035 | USD 509.55 Million |

| CAGR | CAGR of 4.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade / Purity (High Purity Grade, Battery Grade, Technical Grade, and Commercial Grade) • By Form (Powder, Liquid / Solution, and Granules / Pellets) • By Application (Dry Cell Batteries, Water Treatment, Chemical Synthesis / Catalyst, Metallurgical Fluxes & Galvanizing, Textile Processing, Pharmaceuticals, and Others) • By End-Use Industry (Chemical Industry, Electronics & Batteries, Agriculture, Pharmaceuticals & Healthcare, Textile Industry, Oil & Gas, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | TIB Chemicals AG, Zaclon LLC, American Elements, Global Chemical Co., Ltd., Pan-Continental Chemical Co., Ltd., Eurocontal SA, Weifang Dongfangsheng Chemical Co., Ltd., Hisky Zinc Industry Co., Ltd., Tianjin Nanping Chemical Co., Ltd., Jiangsu Shenlong Zinc Industry Co., Ltd., Xiamen Ditai Chemicals Co., Ltd., Vijaychem Industries, Merck KGaA, Zinc Nacional, Airedale Chemical Company Limited, S.A. Lipmes, Flaurea Chemicals, Vinipul Inorganics Private Limited, Suchem Industries, Hindustan Zinc Limited |

Frequently Asked Questions

North America dominated the Zinc Chloride Market in 2025 with a 45.68% share.

Battery Grade dominated the Zinc Chloride Market with a 28.47% share in 2025.

Carbon-zinc dry cell battery production sustaining zinc chloride electrolyte demand across Asia Pacific and developing markets, water treatment infrastructure expansion in North America driving corrosion inhibitor procurement, and pharmaceutical-grade zinc chloride growth in API synthesis are the primary drivers.

The Zinc Chloride Market size was USD 336.16 Million in 2025 and is expected to reach USD 509.55 Million by 2035.

The Zinc Chloride Market is expected to grow at a CAGR of 4.29% from 2026–2035.

Get in Touch