Bioactive Materials Market Report Scope & Overview:

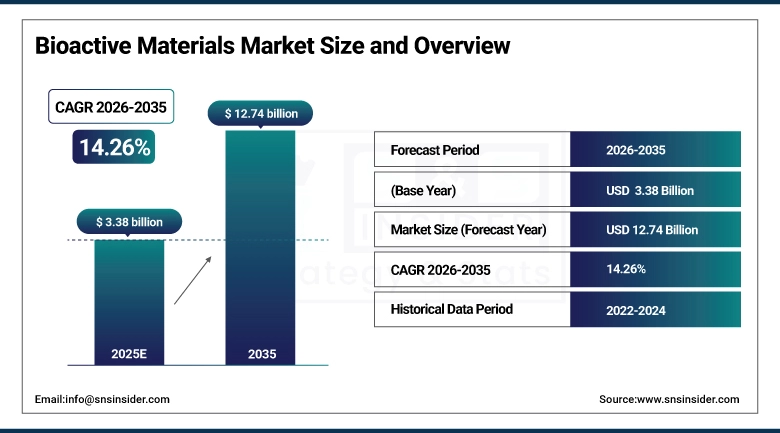

The Bioactive Materials Market size was valued at USD 3.38 Billion in 2025 and is projected to reach USD 12.74 Billion by 2035, growing at a CAGR of 14.26% during 2026–2035.

Bioactive materials occupy a specific and commercially important position in regenerative medicine and surgical reconstruction they are materials that interact with biological tissue in a controlled, constructive way rather than simply occupying space or being tolerated by the body. That distinction between inert implants that the body learns to ignore and bioactive materials that actually direct tissue response is what drives the clinical and commercial interest in this category. Bioactive glass bonds directly to bone and soft tissue. Hydroxyapatite promotes osteoblast adhesion and new bone formation. Bioactive polymers degrade on a schedule that can be calibrated to match tissue regeneration timelines.

Bioactive Materials Market Size and Forecast:

-

Market Size in 2025: USD 3.38 Billion

-

Market Size by 2035: USD 12.74 Billion

-

CAGR: 14.26% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Bioactive Materials Market - Request Free Sample Report

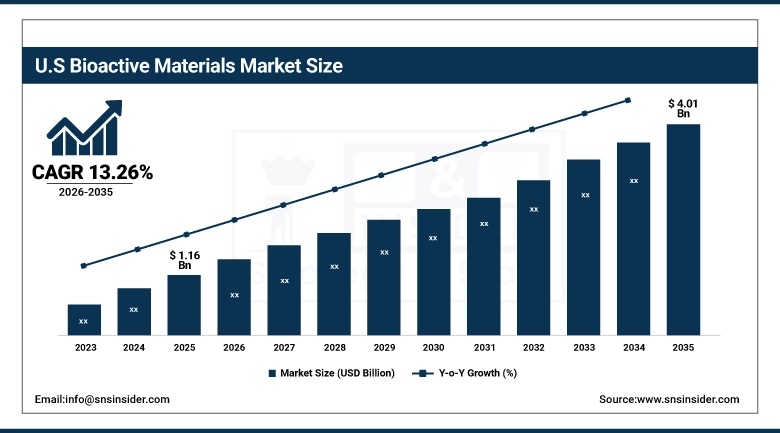

The U.S. Bioactive Materials Market was valued at USD 1.16 Billion in 2025 and is projected to reach USD 4.01 Billion by 2035, growing at a CAGR of 13.26% during 2026–2035. The United States market benefits from the concentration of advanced surgical centers and academic medical institutions that serve as early adopters of regenerative material technologies, a regulatory environment through the FDA that while demanding is well-navigated by established manufacturers, and a reimbursement infrastructure that has progressively recognized the clinical value of bioactive material-based procedures relative to traditional implant approaches.

Key Bioactive Materials Market Trends:

-

Bioactive glass adoption in orthopedics and dental care rises, outperforming synthetic and allograft alternatives.

-

Third-generation bioactive materials shift from research to clinical use, enabling active cellular and molecular responses.

-

Tissue engineering R&D grows as bioactive scaffolds enhance cartilage, spine, and craniofacial repair outcomes.

Bioactive Materials Market Growth Drivers:

-

Growing demand for regenerative surgery and limits of traditional implants are driving bioactive material use.

The commercial case for bioactive materials is built on a clinical problem that conventional implants have not fully solved: the interface between an implant and the surrounding biological tissue. Metallic and ceramic implants that do not actively engage with tissue biology depend on mechanical fixation, press-fit, or cement to maintain stability, and each of those approaches carries failure modes that become more visible as patient populations age and implant longevity expectations extend. Bioactive materials change the equation by forming a chemical bond with bone or soft tissue not a mechanical connection, but a biological one that grows stronger over time rather than loosening. For orthopedic applications, this matters in spinal fusion, long bone fracture repair, and revision arthroplasty where the quality of the bone-implant interface determines whether a procedure succeeds or requires revision.

Bioactive Materials Market Restraints:

-

Complex manufacturing, long regulations, and inconsistent reimbursement across regions are hindering bioactive material market growth.

The manufacturing of clinical-grade bioactive materials particularly bioactive glass and hydroxyapatite ceramics involves controlled processes where small variations in composition, sintering temperature, particle size distribution, and surface chemistry can produce materials with meaningfully different biological performance. Maintaining the consistency required for regulatory approval and clinical reliability at commercial production volumes is technically demanding and capital-intensive in ways that commodity medical material manufacturing is not.

Bioactive Materials Market Opportunities:

-

Third-generation bioactive materials, tissue engineering, and healthcare investments in emerging markets are driving new growth opportunities.

The distinction between first and second-generation bioactive materials which focused on biocompatibility and osteoconduction respectively and the third generation currently entering clinical use is significant for commercial potential. Third-generation materials are designed to activate genes that stimulate tissue regeneration, essentially programming a biological response rather than simply providing a scaffold for it. This capability is extending bioactive material application from hard tissue repair into soft tissue engineering, controlled drug release, and wound management in ways that create entirely new market segments rather than competing for share in established ones.

Bioactive Materials Market Segment Analysis:

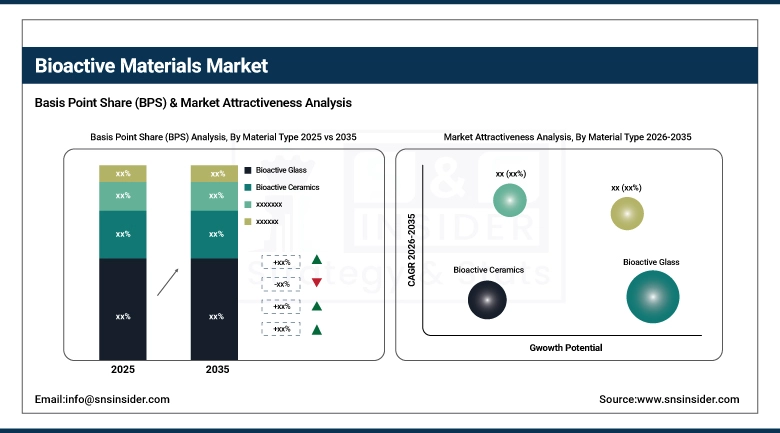

By Material Type: Bioactive Glass Leads and Grows Fastest While Bioactive Ceramics Maintain Strong Second Position Through 2035

Bioactive Glass dominated with a 32.4% share in 2025, valued at approximately USD 1.09 Billion, and is also expected to grow at the fastest CAGR of approximately 15.01% through 2035.

Bioactive glass holds market leadership on both share and growth rate because its clinical performance breadth is unmatched among the material type options: it bonds to both hard and soft tissue, has documented antibacterial properties that reduce post-surgical infection risk, and can be manufactured in forms ranging from granules and powder to custom-shaped scaffolds and fiber-reinforced composites. The clinical evidence base for bioactive glass in orthopedic and dental applications is deep and continues to expand with each cycle of long-term outcome studies.

By Form: Powder Leads the Bioactive Materials Market While Coatings Register the Fastest CAGR Through 2035

Powder dominated with a 34.2% share in 2025, valued at approximately USD 1.15 Billion, while Coatings are expected to grow at the fastest CAGR of approximately 15.15% through 2035.

Powder form maintains its leading position because of its versatility across surgical applications it can be mixed to a paste for void filling, compacted for grafting, or used as a loose particulate in socket preservation, covering the broadest range of clinical needs from a single product format. Powder also carries the lowest manufacturing complexity among the form types, which supports the widest range of manufacturers and price points. Coatings are the fastest-growing form because they address a large and established implant base: metallic orthopedic and dental implants already in clinical use can be upgraded in biological performance through the application of hydroxyapatite or bioactive glass surface coatings without requiring implant redesign. As coating deposition technologies improve and the clinical evidence supporting coated implant performance over uncoated equivalents accumulates, the segment is expanding both in new implant manufacturing and in the retrofit coating of established implant designs.

By Application: Orthopedic Surgery Leads Bioactive Materials Demand While Tissue Engineering Drives the Fastest Growth Through 2035

Orthopedic Surgery dominated with a 36.7% share in 2025, valued at approximately USD 1.24 Billion, while Tissue Engineering is expected to grow at the fastest CAGR of approximately 15.77% through 2035.

Orthopedic surgery's leadership reflects the depth and maturity of bioactive material use in bone void filling, spinal fusion, and fracture management applications where the clinical case is well-established, reimbursement is generally available, and the surgical technique for bioactive material use is part of standard training. The global volume of orthopedic procedures ensures that even modest per-case bioactive material adoption rates generate large absolute procurement volumes. Tissue Engineering is growing fastest because it represents the frontier of what bioactive materials can do: scaffold systems that guide the regeneration of cartilage, tendon, and complex tissue structures are moving from laboratory research into clinical trials and early commercial deployment, with each successful clinical result opening a new application area that generates its own procurement demand. The long-term growth potential of tissue engineering as a clinical discipline is substantially larger than traditional hard tissue repair, and bioactive materials are central to its technical execution.

By End-User: Hospitals & Clinics Lead Market While Biotechnology & Pharmaceutical Companies Record Fastest CAGR Through 2035

Hospitals & Clinics dominated with a 46.8% share in 2025, valued at approximately USD 1.58 Billion, while Biotechnology & Pharmaceutical Companies are expected to grow at the fastest CAGR of approximately 16.41% through 2035.

Hospitals and clinics are the primary procurement channel for bioactive materials used in surgical applications orthopedic, spinal, and dental procedures all generate direct institutional purchasing of bone graft substitutes, void fillers, and scaffold materials through hospital supply chains and surgical center procurement programs. The scale and consistency of hospital procurement make it the market's volume foundation. Biotechnology and pharmaceutical companies are growing fastest because they are the commercial vehicle for third-generation bioactive material development drug-eluting scaffold systems, gene-activating biomaterials, and precision fermentation-produced biological matrices are all being developed within biotech and pharma R&D frameworks rather than traditional medical device structures, and their commercial launch creates an entirely new purchasing category that is growing from a small base at a rate the established end-user segments cannot match.

Bioactive Materials Market Regional Analysis:

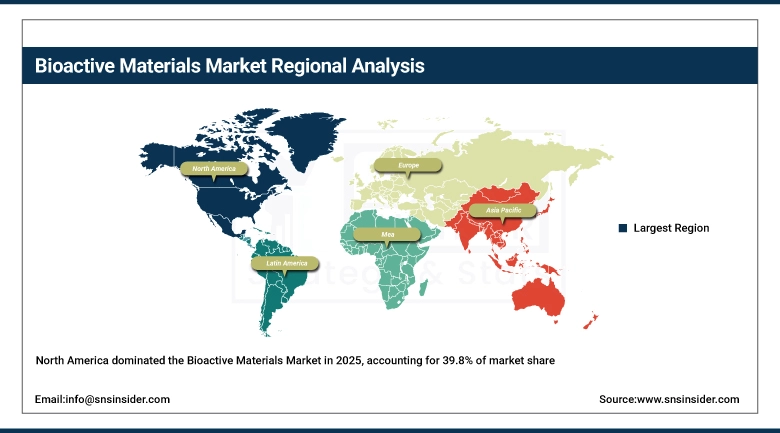

North America Bioactive Materials Market Insights

North America dominated the Bioactive Materials Market in 2025, accounting for 39.8% of market share, valued at USD 1.34 Billion, and is projected to reach USD 4.74 Billion by 2035 at a CAGR of 13.49% during the forecast period. The region's market leadership is grounded in the concentration of advanced surgical centers that serve as early adoption sites for new bioactive material technologies, a well-developed medical device regulatory pathway that provides commercial clarity for product launches, and a reimbursement environment that has increasingly recognized bioactive material procedures as cost-effective alternatives to repeat intervention. Strong academic-industry collaboration in bioactive material research at institutions including MIT, Johns Hopkins, and UC San Francisco is generating a pipeline of next-generation products that maintains North America's position at the technical frontier of the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Bioactive Materials Market Insights

The U.S. market is supported by the world's highest per-capita rates of orthopedic and dental surgical procedures, a hospital procurement environment that actively evaluates and adopts clinical innovations when outcome evidence supports them, and a commercial infrastructure of distributors, surgical reps, and group purchasing organizations that can scale new product adoption efficiently across the surgical community.

Europe Bioactive Materials Market Insights

Europe held a 27.4% share of the Bioactive Materials Market in 2025, valued at USD 0.93 Billion, and is expected to reach USD 3.33 Billion by 2035 at a CAGR of 13.70% during the forecast period. European demand is anchored by a strong tradition of bioactive glass research and clinical application, particularly in the UK and Germany where the foundational work on bioactive glass by Professor Larry Hench and its subsequent clinical development created early institutional expertise that translated into above-average adoption rates. The CE marking regulatory pathway, while rigorous, has been navigated by the established European bioactive material manufacturers efficiently enough that product availability in the European market is generally strong.

Germany Bioactive Materials Market Insights

Germany leads the European market, supported by a large and technically sophisticated orthopedic and dental implant industry that has been among the earliest adopters of bioactive surface coating technologies for metallic implants.

Asia Pacific Bioactive Materials Market Insights

Asia Pacific is expected to grow at the fastest CAGR of approximately 16.66% from 2026 to 2035, rising from USD 0.76 Billion in 2025 to USD 3.56 Billion by 2035. The region's growth leadership reflects several converging factors: rapidly expanding hospital infrastructure in China, India, and Southeast Asia that is increasing surgical procedure volumes; government healthcare investment programs that are improving patient access to advanced surgical treatments; and the rapid maturation of domestic bioactive material manufacturers in China and Japan that are producing products competitive in quality with Western imports at lower price points. Japan has operated a sophisticated bioactive ceramic clinical sector for decades, and its experience is informing adoption patterns in neighboring markets.

China Bioactive Materials Market Insights

China is the dominant national market within Asia Pacific, driven by the scale of its expanding surgical infrastructure, government investment in domestic medical device manufacturing capability, and a large and aging population generating growing orthopedic and dental surgery volumes. Chinese manufacturers have made significant technical progress in hydroxyapatite and bioactive glass production over the past decade, and domestically produced products now supply a meaningful share of the local market that was previously served by imports.

Latin America and Middle East & Africa Bioactive Materials Market Insights

Latin America held approximately 6.1% of the global Bioactive Materials Market in 2025, valued at USD 0.21 Billion, and is expected to reach USD 0.65 Billion by 2035 at a CAGR of 12.21% during the forecast period. Brazil and Mexico are the primary markets, with demand concentrated in private surgical centers serving insured populations with access to advanced implant materials. Public healthcare procurement of premium bioactive materials remains limited by budget constraints across most Latin American markets, which constrains the total addressable volume below what procedure counts alone would suggest. Middle East & Africa held approximately 4.8% of market share in 2025, valued at USD 0.16 Billion, and is expected to reach USD 0.47 Billion by 2035 at a CAGR of 13.09%. Gulf state hospital investment is the primary driver, with UAE and Saudi Arabia building advanced surgical infrastructure that procures bioactive material products for orthopedic and dental programs at institutional scale. South Africa leads the African continent's adoption within a primarily private hospital system. Infrastructure limitations across most of Sub-Saharan Africa continue to constrain adoption to a small number of urban tertiary care centers.

Competitive Landscape for Bioactive Materials Market:

SCHOTT AG is a German specialty glass and glass-ceramic manufacturer headquartered in Mainz with a dedicated bioactive glass business that supplies clinical-grade bioactive glass products to the global medical device and bone graft substitute markets. The company produces Bioglss® 45S5 and related silicate-based bioactive glass compositions in powder and granule forms under its SCHOTT Nexterion and specialty materials platforms, supplying both finished medical device manufacturers and direct surgical end-users.

In February 2025, SCHOTT AG announced an expansion of its bioactive glass powder production capacity at its Mainz facility, adding processing lines specifically configured for medical-grade particle size fractionation to meet the tightening specifications required for advanced scaffold and coating applications.

Stryker Corporation is one of the world's largest medical technology companies, with a significant bioactive materials business operating through its orthopedic and spine divisions. The company's bone graft and void filler portfolio includes calcium phosphate-based bioactive ceramic products used in orthopedic, spinal, and trauma reconstruction procedures across its global hospital customer base.

In January 2025, Stryker announced the commercial launch of an enhanced version of its TriGen® bioactive bone void filler incorporating a modified hydroxyapatite-tricalcium phosphate ratio designed to improve resorption kinetics in load-bearing orthopedic applications.

Bioactive Materials Market Key Players:

-

SCHOTT AG

-

Mo-Sci Corporation

-

Stryker Corporation

-

BonAlive Biomaterials Ltd.

-

Noraker

-

Synergy Biomedical LLC

-

Medtronic plc

-

Dentsply Sirona Inc.

-

Johnson & Johnson

-

Kyocera Corporation

-

Baxter International Inc.

-

Smith & Nephew plc

-

Biomatlante

-

Arthrex Inc.

-

Matexcel

-

Aap Implantate AG

-

Corning Incorporated

-

Merck KGaA

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.38 Billion |

| Market Size by 2035 | USD 12.74 Billion |

| CAGR | CAGR of 14.26% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Bioactive Glass, Bioactive Ceramics (Hydroxyapatite, Tricalcium Phosphate), Bioactive Polymers, Bioactive Composites, and Others) • By Form (Powder, Moldable / Putty, Granules, Coatings, and Others) • By Application (Orthopedic Surgery, Dental Care, Tissue Engineering, Wound Healing, and Drug Delivery Systems) • By End-User (Hospitals & Clinics, Dental Clinics / Laboratories, Biotechnology & Pharmaceutical Companies, and Research & Academic Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SCHOTT AG, Mo-Sci Corporation, NovaBone Products LLC, Stryker Corporation, BonAlive Biomaterials Ltd., Noraker, Synergy Biomedical LLC, Zimmer Biomet Holdings Inc., Medtronic plc, Dentsply Sirona Inc., Johnson & Johnson, Kyocera Corporation, Baxter International Inc., Smith & Nephew plc, Biomatlante, Arthrex Inc., Matexcel, Aap Implantate AG, Corning Incorporated, Merck KGaA. |

Frequently Asked Questions

The Bioactive Materials Market is expected to grow at a CAGR of 14.26% from 2026-2035.

The Bioactive Materials Market size was USD 3.38 Billion in 2025 and is expected to reach USD 12.74 Billion by 2035.

North America dominated the Bioactive Materials Market in 2025.

Bioactive Glass dominated the Bioactive Materials Market.

Rising demand for regenerative medicine, increasing orthopedic and dental procedures, and growing adoption of bioactive implants for faster healing are driving market growth.

Get in Touch