Zero Turn Mower Market Report Scope & Overview:

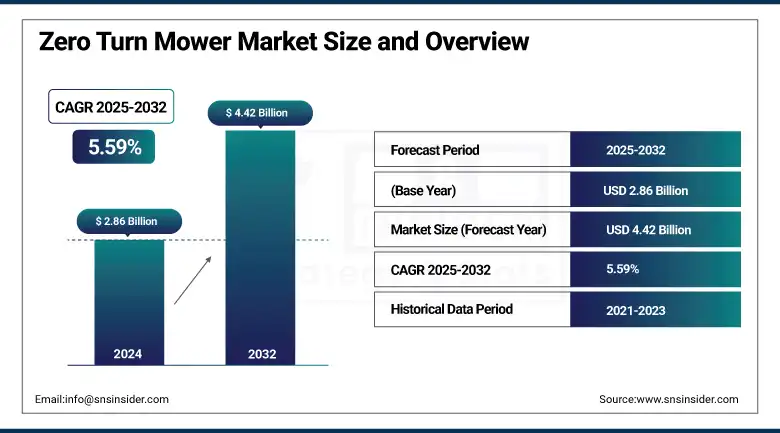

The Zero Turn Mower Market size was valued at USD 2.86 billion in 2024 and is expected to reach USD 4.42 billion by 2032, growing at a CAGR of 5.59% over the forecast period of 2025-2032.

The Zero Turn Mower Market is experiencing robust growth, driven by increasing demand for efficient turf-care equipment across residential, commercial, and municipal sectors. These mowers are high-speed mowers with high maneuverability, making them the best option for maintaining large lawns, golf courses, and large sports grounds with precision and less time to operate. The adoption is being driven by the increasing trend of landscaping and aesthetic use of lawns, particularly in urban and suburban areas. Furthermore, the increasing use of commercial landscaping services and the rising number of golf courses globally are expected to drive the market growth during the forecast period.

To Get more information On Social Zero Turn Mower Market - Request Free Sample Report

Zero Turn Mower Market trends are being determined to an extent by technological developments including electric and hybrid zero-turn mowers industry, advanced cutting decks, and smart control systems that help efficient operation in an eco-friendly state and enhance user convenience. The largest market segment is North America, and Asia-Pacific will be a fast-growing market in the future, with the rapid development of agricultural and landscaping mechanization. The leading market players, such as John Deere, Toro, Husqvarna, and Cub Cadet, are focusing on R&D for advancements in efficiency, ergonomics, and eco-friendliness. The Zero Turn Mower Market growth is primarily attributed to the changing user preferences, rise in expenditure on Garden maintenance, and overall innovations on turf-care equipment that enhance productivity with minimum labor dependency.

For instance, Altoz launched two new zero-turn mowers for 2025: the TRX 766 i and XP 610 RDi. The TRX 766 i features a rugged tracked system, ideal for difficult terrains like slopes and wetlands, powered by a 38.5 hp Kawasaki engine. The XP 610 RDi is a wheeled model with a rear-discharge deck and 29.5 hp engine, built for clean, efficient mowing on flat surfaces. Both models include 14-gallon tanks and advanced operator comfort features.

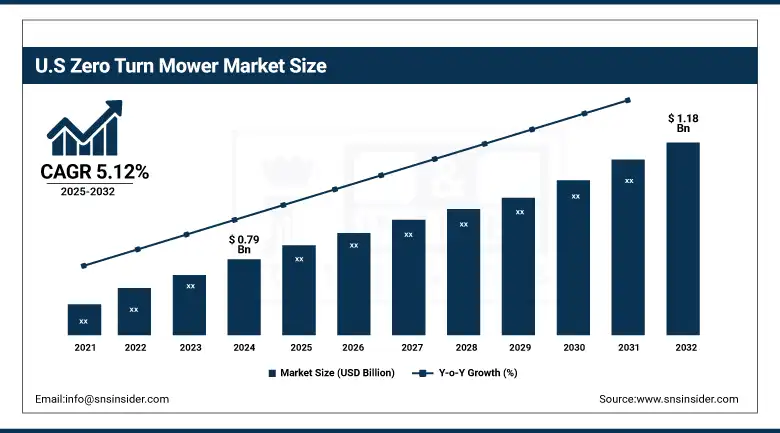

The U.S. dominates the North American zero-turn mower market, reaching USD 0.79 billion in 2024 and is projected to hit USD 1.18 billion by 2032 at a 5.12% CAGR. High demand for effective lawn care, both in commercial and residential sectors, drives growth. The expansion of the market is further complemented by technological advancements and the presence of key manufacturers.

Zero Turn Mower Market Dynamics:

Drivers:

-

Smart and Sustainable Technological Innovations Propel Growth in the Zero-Turn Mower Market

Technological innovation is a key driver in the zero-turn mower market, as manufacturers increasingly introduce advanced features to enhance efficiency and user convenience. Battery-powered and electric zero-turn mowers are gaining traction due to their low emissions, quieter operation, and reduced maintenance needs. Additionally, AI-enabled models with GPS navigation, telematics, and smartphone integration are transforming mowing into a smarter, more precise task. These innovations not only improve operational control and fuel efficiency but also appeal to environmentally conscious consumers and commercial users seeking automation.

For instance, Honda unveiled an all-electric zero-turn mower prototype, signaling a shift toward sustainable and intelligent lawn care solutions. Such advancements are expected to drive broader adoption across residential and commercial segments.

Restraints:

-

High Ownership Costs Hinder Adoption of Zero Turn Mowers Among Budget Buyers

High initial and operating costs are a major restraint in the zero turn mower market, particularly affecting small-scale users and cost-sensitive buyers. Commercial-grade zero turn mowers are equipped with advanced features, robust engines, and durable components, which significantly increase their price, often ranging from several thousand to over ten thousand dollars per unit. In addition to the upfront investment, ongoing costs, such as fuel, regular maintenance, replacement parts, and repairs further add to the financial burden. This makes them less attractive for residential users with smaller lawns or limited budgets. The high total cost of ownership can deter potential customers, especially when more affordable alternatives including push or traditional ride-on mowers are available for lighter lawn care needs.

Zero Turn Mower Market Segmentation Analysis:

By Cutting Width

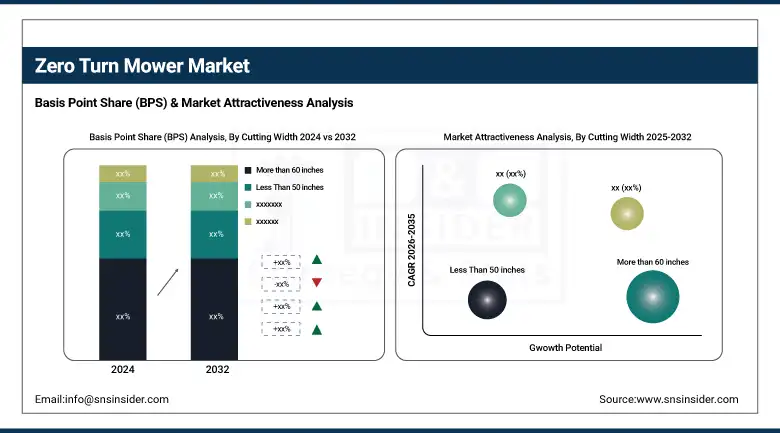

The more than 60 inches dominated the market, accounting for 45% of the zero turn mower market share. These are commonly used in large-scale commercial applications for places, such as sports fields, golf courses, municipal parks, and large estate grounds. This is where efficiency and promptness are needed. The wide decks help cover more area in fewer passes, thus saving time and fuel. At times designed to be more heavy-duty, these machines tend to feature reinforced frames, a powerful engine, and durable components built to withstand the long wear and tear of the toughest conditions.

The 50 to 60 inches cutting width category is the fastest-growing segment in the zeroturn mower market. This series is a perfect combination of efficiency, price, and versatility, making it a popular option for a variety of residential and light commercial applications. Designed for a larger space, these mowers are capable of tackling rougher ground, but are great for lawns of medium size, with the benefit of being able to easily navigate smaller areas as well. There are also lower-priced options with strong performance compared to larger commercial-grade units. The increasing adoption of them is also aided by how they fit in with house garages and trailers. And as homeowners and small businesses continue the search for high performance at lower prices, this segment is likely to see even more rapid growth in the next few years.

By Application

The commercial segment dominated the zero-turn mower market in 2024, accounting for 62% of the total market share. Landscaping contractors, municipalities facility management firms are the reason for this leadership behind the switch to zero-turn mowers. For commercial users, operational efficiency, time savings, and cut quality are must-haves that zero-turn mowers can provide with their maneuverability and faster mowing speeds when compared with traditional tractors. You will typically find these mowers running in shopping centers, campuses, sports arenas, and corporate landscapes where visual aesthetic and a polished appearance are paramount. This continues to provide strength to the largest segment, as the trend of outsourcing landscape maintenance to professionals continues to increase.

The residential segment is witnessing the fastest growth in the zero-turn mower market, due to increased construction of suburban houses, a rising trend of landscaping services, and growing disposable income. High efficiency lawn care equipment is rising among homeowners willing to invest in the maintenance of their properties, with zero turn mowers declared the best as these lawn mowers are quicker to fold to operate with less effort. Zero-turn mowers offer a greater level of speed and accuracy compared to the usual mowers, enabling homeowners to obtain a professional finish.

Zero Turn Mower Market Regional Outlook:

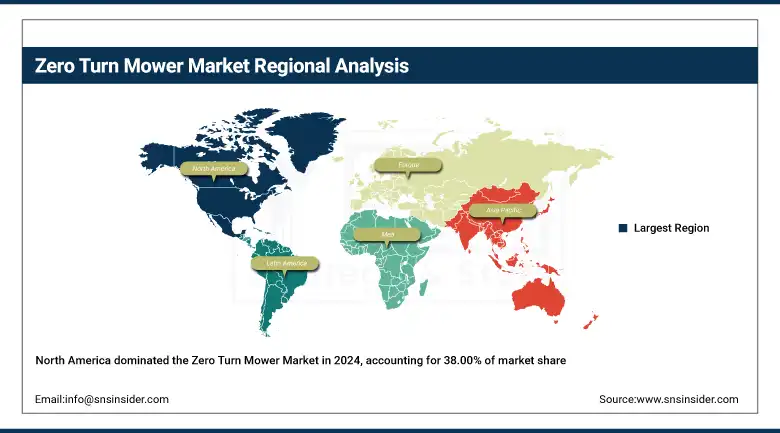

North America held the dominant share in the zero turn mower market, accounting for 38.00% in 2024. This dominance is driven by the widespread use of zero-turn mowers across residential lawns, commercial landscaping services, golf courses, and municipal maintenance projects. The U.S. and Canada lead the pack in lawn care culture, sustained by high consumer spending levels, large yard sizes, and established commercial landscaping industries. Also, John Deere, Toro, and Hustler are the major players in this region with a wide product portfolio. Continued adoption, which is driven by government initiatives (green space development) and the growing trend, will keep the lawn and garden spend growing, and will keep North America as the bellwether leader in this category.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is projected to be the fastest-growing region in the zero turn mower market, due to rising urbanization, growing interest toward landscaping aesthetics, and thriving real estate development in emerging economies. With a focus on infrastructure and green urban spaces, China, India, and Australia demand turf and lawn maintenance equipment even more. With landscaping now an integral aspect when it comes to property value for residential and commercial lands, more and more people are opting for effective and time-saving machinery, such as zero turn mowers. Sales, particularly in developing countries, are further propelled by an upsurge in disposable income levels and knowledge of lawn care techniques.

Australia dominates the Asia Pacific zero turn mower market due to its widespread use in residential lawns, golf courses, and public parks. The country’s large property sizes and strong landscaping culture drive consistent demand. Zero-turn mowers are favored for their efficiency and maneuverability in maintaining vast green spaces. Local availability, favorable climate, and rising gardening trends further support market growth in Australia.

Europe maintains a significant share in the zero-turn mower market, supported by strong adoption across municipal services, public parks, sports fields, and institutional facilities. The maintenance of well-groomed green spaces is a priority in countries such as Germany, the U.K., and several domestic areas, which in turn drives continuous demand for advanced lawn maintenance solutions. Residential use is middle range as property sizes are typically smaller than in North America, but commercial and public sector use is strong. Top trends, such as the eco-conscious consumers and stringent emission regulations, are propelling the adoption of electric and hybrid zero-turn mowers. High value through technological innovation and an ingrained distribution network continues to ensure Europe remains an indispensable part of the global distribution of goods.

Zero Turn Mower Companies are:

ESCO Group LLC, MCE, NMC CAT, Fortus, Beri Udyog, John Deere, Kennametal Inc, Caterpillar Inc, CASE Construction Equipment, and Komatsu Ltd.

Recent Developments:

In October 2024: Kennametal Inc. introduced the HARVI II TE 5-flute solid carbide end mills, featuring reinforced cores designed to boost metal removal rates and extend tool life, further strengthening its portfolio of tools for heavy-duty outdoor equipment.

In May 2024: ESCO Group LLC expanded its ground-engaging tools range with the launch of next-generation excavator and wheel-loader buckets, engineered to enhance wear resistance and operational efficiency in construction and mining applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.86 Billion |

| Market Size by 2032 | USD 4.42 Billion |

| CAGR | CAGR of 5.59% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Cutting Width (Less Than 50 inches, 50 to 60 inches, More than 60 inches) • By Application (Residential, Commercial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | ESCO Group LLC, MCE, NMC CAT, Fortus, Beri Udyog, John Deere, Kennametal Inc, Caterpillar Inc, CASE Construction Equipment, Komatsu Ltd. |

Frequently Asked Questions

Ans: The North America region dominated the zero-turn mower market in 2024.

Ans: The “than 60 inches” segment dominated the zero-turn mower market.

Ans: Smart and Sustainable Technological Innovations Propel Growth in the Zero-Turn Mower Market

Ans: The zero-turn mower market was USD 2.86 billion in 2024 and is expected to reach USD 4.42 billion by 2032.

Ans: The zero-turn mower market is expected to grow at a CAGR of 5.59% from 2025-2032.

Get in Touch