Mechanical Control Cables Market Report Scope & Overview:

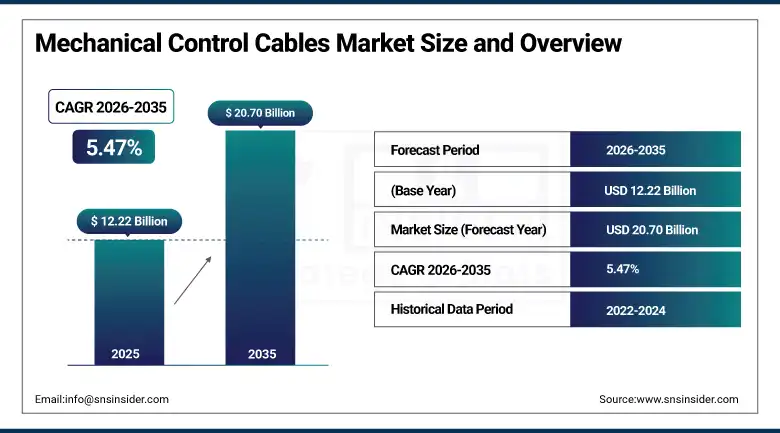

The Mechanical Control Cables Market was valued at USD 12.22 Billion in 2025 and is expected to reach USD 20.70 Billion by 2035, growing at a CAGR of 5.47% from 2026–2035.

Mechanical Control Cables Market Overview

Change has been witnessed in the mechanical control cables industry on a global scale. This include the evolution in the design of mechanical control cables, increased utilization of mechanical control cables across different sectors. Mechanical control cables are essential components whose function is to transmit motion and force from control input mechanisms to output mechanisms using either tension, compression, or both. These changes have been experienced because of an increased demand for military airplanes as a result of ongoing political conflicts around the world, increased demand for commercial aircraft to cater to increased auto production levels in developing countries, as well as industrial automation.

In March 2023, Triumph Group's Actuation Products & Services division in France secured a contract from Kopter, a Leonardo Company, for the production of control cables for the Kopter AW09 helicopter, leveraging Triumph's expertise in flexball cable architecture. This contract demonstrates the commercial momentum of helicopter-specific mechanical control cable development whose precision engineering requirements for rotary-wing aircraft create premium procurement relationships that sustain above-commodity pricing for technically qualified suppliers capable of meeting aerospace certification standards.

Mechanical Control Cables Market Size and Forecast

-

Market Size in 2026E: USD 12.89 Billion

-

Market Size by 2035: USD 20.70 Billion

-

CAGR: 5.47% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Mechanical Control Cables Market - Request Free Sample Report

Mechanical Control Cables Market Trends

-

Lightweight cable materials adoption is increasing in aerospace due to fuel efficiency mandates and emissions reduction requirements globally.

-

Corrosion-resistant cables using advanced alloys and polymer coatings are extending service life in marine and harsh industrial environments significantly.

-

Smart mechanical cables with embedded sensors enable real-time tension monitoring and predictive maintenance for aviation and industrial applications.

-

UAV and autonomous vehicle growth is driving demand for lightweight, high-precision pull-pull cable systems with compact actuator designs.

-

Defense modernization programs and fighter aircraft development are increasing procurement of advanced mechanical control cables globally.

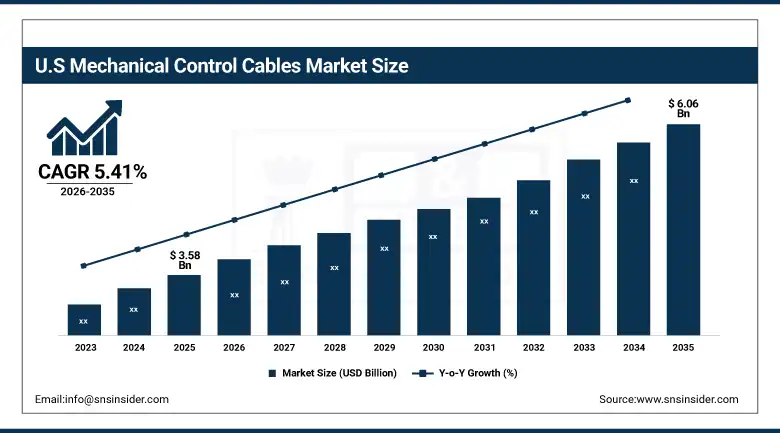

The U.S. Mechanical Control Cables Market Outlook

The U.S. Mechanical Control Cables Market was valued at approximately USD 3.58 Billion in 2025 and is expected to reach approximately USD 6.06 Billion by 2035, growing at a CAGR of approximately 5.41%.

The U.S. is the world's most commercially significant mechanical control cables market within North America's dominant 33.64% global revenue position. Triumph Group, Loos & Co., Bergen Cable Technology, Orscheln Products, and Cablecraft Motion Controls collectively define the commercial U.S. mechanical control cable supply landscape. The U.S. aerospace and Defense sector's extraordinary procurement scale, Boeing and Lockheed Martin's production programmes, and the U.S. Navy's marine vessel fleet create consistent high-value mechanical control cable procurement. The automotive sector's above-average domestic production quality specification and the agricultural equipment industry's Midwestern manufacturing base create additional commercial demand that sustains North America's market leadership.

In October 2023, Cablecraft Motion Controls introduced a new line of upgraded push-pull assemblies with greater flexibility and corrosion resistance, designed for use in aerospace and Defense applications where cable performance reliability under extreme temperature, vibration, and fluid exposure conditions directly determines system operational safety and mission readiness. The product introduction reflects the commercial differentiation strategy of specialised cable manufacturers whose aerospace-qualified product portfolio sustains premium pricing relative to industrial-grade commodity alternatives.

Mechanical Control Cables Market Segment Analysis

-

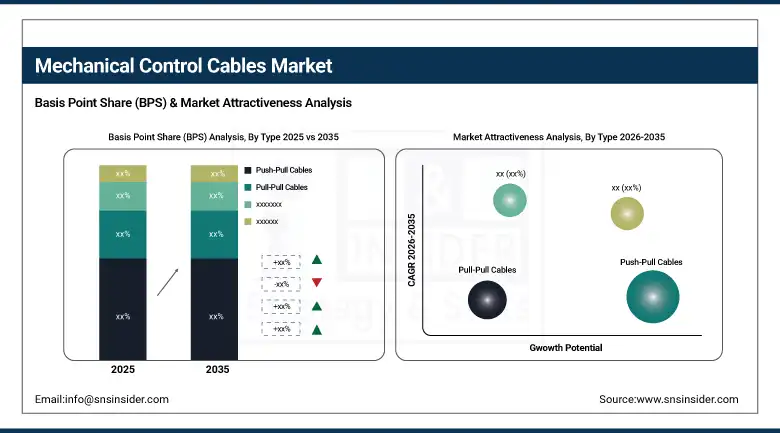

By Type, the push-pull cables segment dominated the mechanical control cables market with 62.15% share in 2025, while the pull-pull cables segment is the fastest growing.

-

By Material, the wire material segment dominated the mechanical control cables market with approximately 52% share in 2025, while the jacket/fiber material segment is the fastest growing.

-

By Application, the engine control segment dominated the mechanical control cables market with approximately 38% share in 2025, while the brake control segment is the fastest growing.

-

By End Use, the commercial segment dominated the mechanical control cables market with approximately 60% share in 2025, while the defense segment is the fastest growing.

-

By Platform, the aerial segment dominated the mechanical control cables market with approximately 45% share in 2025, while the marine segment is the fastest growing.

By Type, push-pull dominates, pull-pull grows fastest

Push-pull cables retained the dominant type position with 62.15% of the mechanical control cables market in 2025. Their commercial primacy reflects the universal application compatibility that bidirectional force transmission capability provides across the most commercially significant control cable deployment contexts. Automotive throttle control systems whose engine speed regulation requires precise throttle plate actuation in both opening and closing directions, aerospace engine control systems whose power lever movement creates both push and pull cable loads, and marine throttle systems whose remote engine control requires the same bidirectional actuation collectively sustain push-pull cable's dominant procurement volume.

Pull-pull cables are the fastest-growing type at 6.07% CAGR because the UAV industry's lightweight actuator requirement, aerospace applications requiring tension-only control in space-constrained installations, and the growing demand for compact, low-friction cable systems collectively create above-average pull-pull procurement growth. Each new UAV platform whose control surface actuation requires minimal weight and compact routing creates pull-pull cable specification whose commercial aggregate grows with the extraordinary expansion of the unmanned aerial vehicle market across military, commercial, and consumer applications.

By Material, wire dominates, jacket/fiber grows fastest

Wire material retained the dominant material position with approximately 52% of the mechanical control cables market in 2025. High-tensile stainless steel wire's combination of tensile strength, corrosion resistance, and dimensional stability under cyclic loading creates the performance foundation for mechanical control cables across the most demanding aerospace, marine, and automotive applications. The wire material's dominance reflects the fundamental mechanical performance advantage of metallic wire constructions whose modulus of elasticity, fatigue strength, and operating temperature range collectively create specification preference in safety-critical applications where cable performance predictability determines system reliability.

Jacket and fiber material is the fastest-growing category because the aerospace industry's thermal protection requirements, the marine sector's chemical resistance needs, and the automotive industry's abrasion and fluid resistance requirements are creating growing demand for advanced polymer and composite fiber jacket constructions whose performance improvement over conventional PVC and nylon alternatives sustains premium specification. Each new aircraft type whose fuel system routing creates fire-resistance cable jacket requirements and each offshore marine application whose chemical exposure creates fluoropolymer jacket specification create structured jacket material procurement growth that compounds with aerospace and marine production expansion.

By End Use, commercial dominates, Defense grows fastest

The commercial end-use segment retained the dominant position with approximately 60% of the mechanical control cables market in 2025. Commercial procurement encompasses the automotive industry's throttle, brake, and transmission cable demand, the commercial aviation sector's aircraft cable replacement and new-build procurement, the industrial machinery sector's control system cable requirements, and the marine and agricultural equipment industries' combined cable consumption whose aggregate creates the most commercially broad-based demand category. Automotive's scale as the largest single end-use sub-segment within commercial reflects the extraordinary global vehicle production volume whose mechanical control cable content per vehicle creates procurement that compounds with automotive output growth, particularly in Asia Pacific’s rapidly expanding vehicle production base.

Defense is the fastest-growing end-use segment because NATO member states' progressive increase of Defense spending toward 2% GDP targets, the U.S. Department of Defense’s next-generation military aircraft procurement programmes, and Indo-Pacific military modernization investment are collectively creating above-average military aviation mechanical control cable procurement growth. Each new fighter aircraft, military transport, and helicopter programme creates cable procurement whose per-aircraft technical specification and certification requirement creates premium commercial relationships that commodity industrial cable suppliers cannot satisfy. The F-35's multi-national production programme and various next-generation military aircraft developments collectively represent the most commercially certain Defense cable procurement pipeline.

By Application, engine control dominates, brake control grows fastest

Engine control retained the dominant application position with approximately 38% of the mechanical control cables market in 2025. Throttle control cables whose precise transmission of pilot or driver input to engine management systems defines the most safety-critical and highest-volume mechanical control cable application across automotive, aerospace, and marine platforms. Each combustion engine vehicle, piston aircraft, and marine vessel with remote engine control creates engine control cable procurement whose aggregate across global automotive, aviation, and marine production volumes creates the market’s largest single application revenue category.

Brake control is the fastest-growing application because regulatory mandates for improved braking performance, the commercial vehicle industry's brake system upgrade investment, and the aviation sector's carbon brake adoption are creating above-average brake cable demand growth. Each new vehicle model whose NCAP safety rating requirement drives braking performance improvement creates brake control cable specification upgrade investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Mechanical Control Cables Market Insights

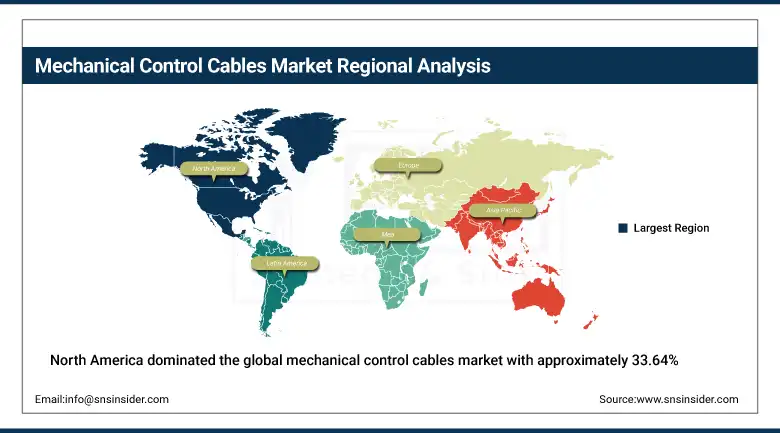

North America dominated the global mechanical control cables market with approximately 33.64% of global revenues in 2025, driven by advanced manufacturing capabilities, a well-established automotive industry, and the growing demand for high-quality mechanical control cables in aerospace, Defense, and industrial applications. The United States accounts for approximately 87.4% of North American revenues through Triumph Group, Loos & Co., Bergen Cable Technology, Orscheln Products, and Cablecraft Motion Controls’ commercial operations.

Canada contributes approximately 12.6% of North American revenues through its aerospace manufacturing sector’s Bombardier and CAE-linked cable procurement, the marine industry’s vessel control cable demand, and the automotive manufacturing sector’s consistent cable procurement from domestic and joint venture OEM facilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Mechanical Control Cables Market Insights

Europe is a technically sophisticated mechanical control cables market where Airbus’ aircraft production, the automotive OEM sector’s manufacturing scale, and Defense procurement under increased European NATO commitments create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive industry’s brake and engine control cable procurement, the aerospace sector’s Airbus Hamburg and Bremen production facilities, and the industrial machinery sector’s control system cable requirements.

The United Kingdom and France are significant secondary markets where BAE Systems’ military aircraft programmes, Airbus’ Toulouse and Bristol operations, and the automotive manufacturing sector’s cable procurement create consistent commercial demand. Triumph Group’s French Actuation Products division, whose Kopter AW09 helicopter cable contract demonstrates, sustains European aerospace cable supply capability.

Asia Pacific Mechanical Control Cables Market Insights

Asia Pacific is the fastest-growing regional mechanical control cables market at 6.45% CAGR, driven by China’s booming automotive and aviation sectors, India’s rapidly expanding vehicle production and Defense modernization, Japan’s precision manufacturing, South Korea’s automotive and shipbuilding industries, and the region’s extraordinary manufacturing growth. China accounts for approximately 44.8% of Asia Pacific revenues through its position as the world’s largest automotive producer, the rapidly expanding domestic commercial aviation fleet, and the government’s Defense industry modernization creating military cable procurement.

India represents the most commercially dynamic emerging market within Asia Pacific where the Make in India initiative’s Defense manufacturing investment, the rapidly growing domestic automotive sector’s cable demand, and the aviation sector’s fleet expansion create above-average mechanical control cable procurement growth that compounds with India’s industrial development trajectory.

MEA & Latin America Mechanical Control Cables Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its Defense procurement for Saudi Arabian Air Force fleet maintenance, ARAMCO’s industrial equipment cable demand, and Vision 2030’s manufacturing development. Brazil leads Latin American revenues at approximately 44.2% through Embraer’s commercial and Defense aircraft cable procurement, the large automotive manufacturing sector’s consistent demand, and the offshore energy industry’s marine cable requirements. Growing Defense spending across the Gulf and Latin American automotive expansion collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Military aviation modernization and commercial aircraft fleet expansion creating structured aerospace cable demand

Military aviation modernization is the mechanical control cables market’s most commercially certain near-term growth driver. NATO member states’ progressive achievement of 2% GDP Defense spending targets, the U.S. Department of Defense’s multi-decade F-35 production programme, and Indo-Pacific military aviation modernization collectively create military aircraft production and upgrade procurement whose mechanical control cable content creates structured demand that compounds with Defense budget growth. Each new military aircraft delivered and each legacy aircraft undergoing avionics and system upgrade creates mechanical control cable procurement whose combined commercial scale sustains above-average revenue growth for aerospace-qualified cable suppliers.

Commercial aircraft fleet expansion driven by air travel demand recovery and emerging market aviation growth creates consistent new-build and MRO mechanical control cable procurement. Each aircraft delivered by Boeing and Airbus creates new-build cable procurement, and each aircraft in service creates ongoing MRO replacement demand whose aggregate across the global commercial fleet of over 25,000 active passenger aircraft creates the most commercially consistent mechanical control cable revenue stream.

Restraints: Electronic fly-by-wire displacement and raw material cost volatility

Electronic fly-by-wire and drive-by-wire system adoption in new vehicle and aircraft platforms creates a structural substitution trend that progressively displaces mechanical control cables from applications where electronic actuation’s precision, configurability, and weight advantage creates specification preference. Each new aircraft type that specifies full fly-by-wire architecture for primary flight controls reduces the mechanical cable content per aircraft, creating a per-unit revenue headwind that moderate production volume growth cannot fully offset in the most advanced platform categories.

Raw material cost volatility for stainless steel, titanium alloys, and specialty polymer jacketing creates production cost uncertainty that limits mechanical control cable manufacturer margin predictability. Each metals price cycle creates input cost variation whose downstream impact on cable pricing and margin sustains commercial uncertainty for manufacturers whose long-term supply contracts limit the pace of input cost pass-through to downstream customers.

Opportunities: UAV market expansion and smart cable technology development

UAV market expansion represents the most commercially dynamic near-term growth opportunity for pull-pull cable systems whose lightweight and compact design create specification preference in unmanned aerial vehicle actuator applications. Each new UAV platform that specifies mechanical cable actuation for control surface, landing gear, or payload deployment creates pull-pull cable procurement whose commercial aggregate grows with the extraordinary global UAV market expansion across military, commercial delivery, agricultural, and inspection applications.

Smart mechanical cable technology whose embedded sensor capability enables real-time tension monitoring, predictive wear detection, and digital maintenance data integration represents the most commercially premium product development direction. Each smart cable deployment in safety-critical aerospace or industrial applications whose condition monitoring prevents unplanned failure creates operational value that sustains premium pricing relative to conventional passive cable alternatives.

Recent Developments:

-

2026: Hi-Lex Corporation strengthened its global automotive cable production network in 2026 with enhanced corrosion-resistant and low-friction control cable systems supporting rising electric and hybrid vehicle demand.

-

2025: Triumph Group expanded its aerospace mechanical control cable systems portfolio in 2025, focusing on lightweight push-pull cable assemblies for next-generation military and commercial aircraft platforms.

-

2025: LEONI AG advanced its automotive control cable manufacturing capabilities in 2025 by integrating high-precision motion control systems and lightweight material technologies for electric vehicle throttle and transmission applications.

Mechanical Control Cables Market key players are:

-

Triumph Group Inc.

-

Loos & Co. Inc.

-

Bergen Cable Technology Inc.

-

Cablecraft Motion Controls

-

Orscheln Products LLC

-

Tyler Madison Inc.

-

Wescon Controls

-

Glassmaster Controls Company Inc.

-

Kongsberg Automotive ASA

-

Dunlop Aircraft Tyres Ltd

-

Hi-Lex Corporation

-

Suprajit Engineering Ltd.

-

AeroControlex (Parker Hannifin)

-

Crane Aerospace & Electronics

-

Elliott Manufacturing Co. Inc.

-

Carl Stahl Sava Industries

-

Sievert Larson Rigg

-

Grand Rapids Controls LLC

-

Dura Automotive Systems LLC

-

LEONI AG

Mechanical Control Cables Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.22 Billion |

| Market Size by 2035 | USD 20.70 Billion |

| CAGR | CAGR of 5.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Push-Pull Cables, Pull-Pull Cables) • By Material (Wire Material, Jacket/Fiber Material) • By Application (Engine Control, Auxiliary Control, Brake Control, Landing Gear, Others) • By End Use (Commercial, Defense, Non-Aero Military) • By Platform (Aerial, Land, Marine) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Triumph Group Inc., Loos & Co. Inc., Bergen Cable Technology Inc., Cablecraft Motion Controls, Orscheln Products LLC, Tyler Madison Inc., Wescon Controls, Glassmaster Controls Company Inc., Kongsberg Automotive ASA, Dunlop Aircraft Tyres Ltd, Hi-Lex Corporation, Suprajit Engineering Ltd., AeroControlex (Parker Hannifin), Crane Aerospace & Electronics, Elliott Manufacturing Co. Inc., Carl Stahl Sava Industries, Sievert Larson Rigg, Grand Rapids Controls LLC, Dura Automotive Systems LLC, LEONI AG |

Frequently Asked Questions

The Mechanical Control Cables Market is expected to grow at a CAGR of 5.47% from 2026 to 2035.

The Mechanical Control Cables Market was valued at USD 12.22 Billion in 2025.

Military aviation modernization driven by increased Defense spending and geopolitical tensions creating above-average aerospace cable procurement.

Push-Pull Cables dominated the Mechanical Control Cables Market with 62.15% share in 2025.

North America dominated the Mechanical Control Cables Market with approximately 33.64% of global revenues in 2025.

Get in Touch