Food Processing Equipment Market Report Scope & Overview:

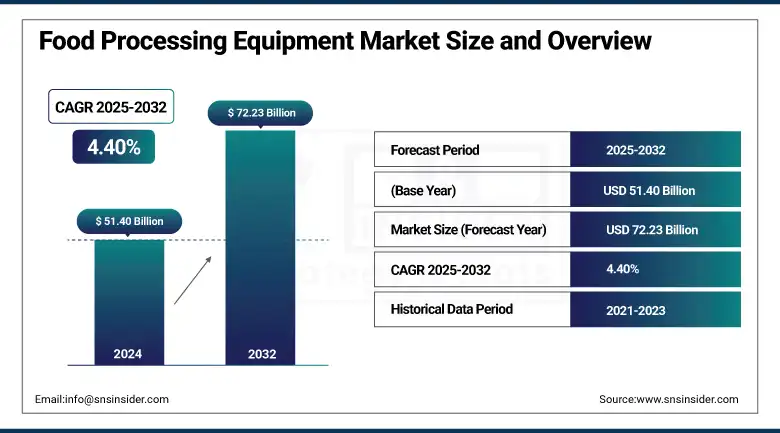

The food processing equipment market size was valued at USD 51.40 billion in 2024 and is expected to reach USD 72.23 billion by 2032, growing at a CAGR of 4.40% over the forecast period of 2025-2032.

The food processing equipment market is gaining fantastic momentum as the demand for packaged and processed foods is on the rise, new developments in food processing technology, and insufficient labor available for food processing. Due to increasing consumer preference for ready-to-eat products, the food processing equipment market growth can be traced back. The trends observed in the market are changing, and manufacturers are slowly moving toward energy-efficient and multifunctional equipment. The food processing equipment market research report provides analysis for the global market based on key drivers, including emerging economies, induced industrialization, and dietary shifts.

To Get more information On Food Processing Equipment Market - Request Free Sample Report

“In March 2025, Marel introduced upgraded modules for its Innova Food Processing Software that provide real-time control and data-based automated processes across meat and seafood lines.”

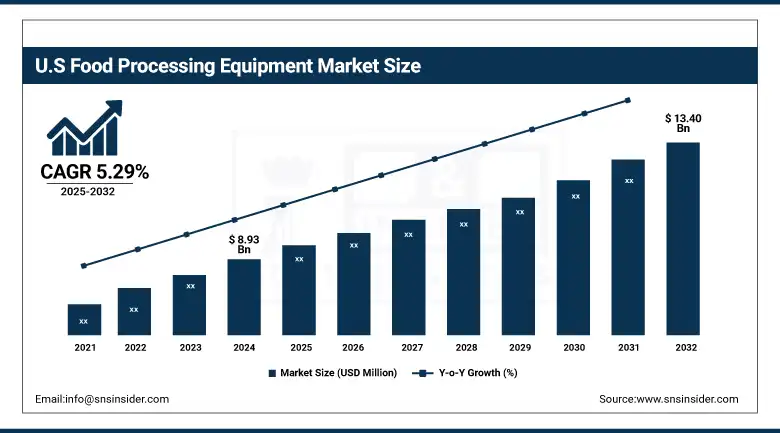

The U.S. food processing equipment market size was valued at USD 8.93 billion in 2024 and is expected to reach USD 13.40 billion by 2032, growing at a CAGR of 5.29% over the forecast period of 2025-2032.

With growing demand for automation and efficiency in food production, the U.S. food processing equipment market is witnessing continual growth. Today, smart technologies and sustainability are undeniably among the leading key food processing equipment market trends. To meet changing consumer and regulatory expectations, food processing equipment companies are making innovation a priority in the U.S.

Food Processing Equipment Market Dynamics:

Drivers:

-

Rising Automation and Digital Integration Across Processing Facilities Accelerate the Growth of the Food Processing Equipment Market

Automation technologies that have been used in food processing in the U.S. and, in other regions globally, are compelling the vast majority of food processors in industrial countries of the world to reevaluate their existing in-house operations. Using digital systems, increases efficiency, minimizes labor costs, and strengthens traceability while complying with food safety regulations. As a result, these transformations are contributing to the demand for industrial food processing machines, including but not limited to precision slicers, automated conveyors, and smart packaging systems. As per current food processing equipment market analysis, the incorporation of intelligent technologies has become the basic level of expectation among the top food processing equipment companies. This trend not only reflects the restraint of food processing equipment market trends, but also reflects the fact that manufacturing enterprises are seeking the same productivity and sustainable development.

“In January 2025, a New AI fish processing system by BAADER Group automates filleting and sorting at high throughput with record precision and reduced labor dependency, while enhancing yield.”

-

Increasing Consumption of Packaged and Processed Foods Fuels Demand for Advanced Food & Beverage Processing Equipment

Rising urban population, changing lifestyles, and the consumer trend to prefer ready-to-eat and packaged meals are some of the major factors boosting the demand for efficient equipment. This is particularly evident in the developing world, where a growing middle class leads to changing dietary patterns as disposable income rises. Consequently, firms are updating machines to fulfill manufacturing requirements that are volume-based, hygienic, and safety-compliant. This upsurge will also favor the food sorting machines market, pushing processors toward the adoption of optical sorters for quality assurance. Leading companies are investing in technology upgrades, which is a clear sign of changing food processing equipment market trends, reflecting the above market shifts.

Restraints:

-

High Capital Investment and Operational Costs Restrain Small and Medium Enterprises from Adopting Industrial Food Processing Machines

Although the feat comes with several advantages, the one major challenge that prevails in the food processing machinery market is the cost barrier for small and medium-sized enterprises (SMEs). Complexity in adopting rather higher upfront investment, coupled with continuous maintenance and skilled labor needed to operate new-age systems, is deterring the customers who have budget constraints. Such barriers limit emerging markets from penetrating, while modernization becomes limited to big corporations. As per in-depth food processing equipment market analysis, this cost-associated constraint hampers competitiveness within the market and also prolongs technological transitions. Food processing equipment companies are increasingly focused on innovation, but must develop scalable, cost-effective solutions to support wider adoption among all business sizes.

Food Processing Equipment Market Segmentation Analysis:

By Mode of Operation

The automatic segment held the largest revenue share of over 52.42% in 2024, owing to the efficiency of the along and accuracy along with reduced reliance on manual labor. They allow for high-speed automatic operations, maintain a consistent product quality, and adhere to safety standards, making them suitable for large-scale production environments. With growing demand and demand for sustainability, many companies are focusing on automation technologies. According to the latest market analysis on the food processing equipment market, automation is an indispensable component of the food processing machinery market on the back of consistent growth and demand across end-use verticals, which in turn has impacted the market positively.

The semi-automatic segment is expected to grow at a CAGR of 4.17% during 2025-2032 due to Low capital investment, greater flexibility, and ease of integration into small- and medium-scale operations. This operating mode has great attraction, specifically for the growing economies and startups that want dependable processing without the high capital investments in automation. Cost-sensitive regions are modernising food systems with semi-automatic solutions, which provide a transitional pathway into the food & beverage processing equipment landscape, providing a stable market development across different scales of operation.

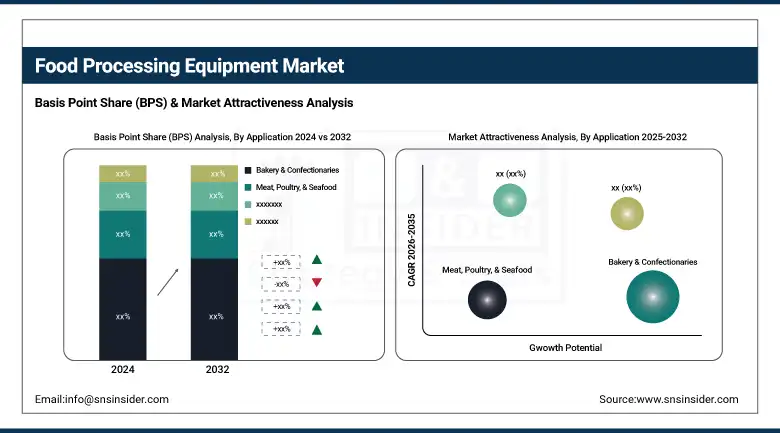

By Application

The bakery & confectioneries segment contributed 22% of the food processing equipment market share in terms of revenue, in 2024, owing to an increase in consumer demand for packaged snacks, artisan baked goods, and high-quality confectionery. The convenience-oriented lifestyle, along with rising urbanization and seasonal consumption habits, supports sustainable production volumes in this category. This application area is the backbone of manufacturing operations across the new and old food processing value chain and is therefore backed by the investments from the top players of Companies.

The grains segment is projected to increase at a moderate CAGR on account of the increasing need for whole grain and gluten-free products, coupled with increased agricultural production in emerging countries. The growing attention towards health and nutrition is responsible for pushing the demand for minimally processed grains more rapidly, with the manufacturers adopting modern solutions. This segment is also aided by innovations concerning sustainable processing, along with the rising demand for plant-based food ingredients, which will leverage equipment upgrades and the entry of new players into the global food processing equipment market.

By Type

In 2024, the food processing equipment market revenue share was led by the processing segment, accounting for 55% share, as processing represents the heart of the value-added food supply chain, including fundamental operations, such as mixing, blending, cutting, or cooking between the staple foods category. Its pan-control is further facilitated with a digital incorporation of process controls and sanitation technologies that sustain superior output quality and compliance with the regulations of safety. As per the latest food processing equipment market analysis, processing equipment is the backbone of the production line, and many food processing equipment companies invest a lot of money in enhancing the productivity and throughput of the processing equipment.

Pre-processing is anticipated to hold the highest CAGR over 2025-2032 due to strict hygiene standards imposed by various industries and a growing inclination toward waste minimization and raw material optimization. Automation is also increasing in pre-processing jobs, such as washing, peeling, and sorting to reduce human error and provide consistency. The modern equipment used for pre-processing is in demand with increased consumer demand for ready-to-cook and clean-label foods. In addition, the scope of the food sorting machines market is expected to be significant, finding applications as a solution of control & materials, and this is on the rise due to innovations that support the manufacturing processes, due to its rapid growth potential in the full market landscape of scope.

Food Processing Equipment Market Regional Outlook:

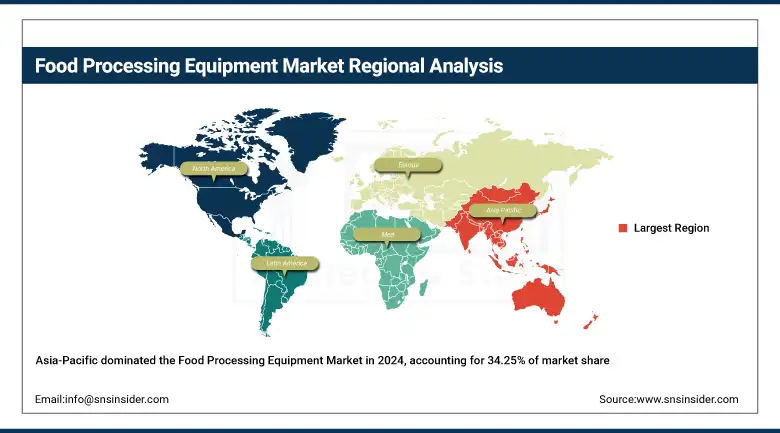

Asia-Pacific held the largest revenue share of approximately 34.25% in the food processing equipment market in 2024, owing to the huge population pool in the region, rising middle-class income, along rapidly growing demand for packaged and processed foods. The increasing adoption is driven by quick urbanization along with those in governments promoting infrastructure development within industrial sectors and increasing capital put forth by the global corporate food industries within nations like China, India, and Japan, among others. Moreover, mounting affordable manufacturing centers and increasing infrastructure, creating a central point for Companies and their strategic expansion in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

The North American market is projected to register the maximal CAGR of nearly 5.69% over 2025-2032 due to technological advancement, strong regulatory framework, consumer preference for healthy, organic, and clean-label products, coupled with rising consumer awareness for the. There is a rapid acceptance of smart food processing machinery market solutions and food manufacturing automation in the region. In addition to this, repairs to equipment are being upgraded due to sustainability practices and the demand for energy-efficient systems. North America, with its strong investment in research and development and product development, retains its lead in the adoption of advanced food & beverage processing equipment technologies.

Automation, sustainability, and stringent food safety regulations drive the European food processing equipment market. Its manufacturing ecosystem is most developed in Germany, which tops the rankings in the region. For instance, a new optical food sorter powered by AI raises the bar for quality control. Equipment design and market competitiveness are all being driven by Europe, and specifically, the push towards energy-efficient solutions.

Key Players in Food Processing Equipment Market are:

The major players operating in the market are BAADER Group, Marel, Bühler AG, GEA Group Aktiengesellschaft, The Middleby Corporation, Tetra Laval International S.A., Alfa Laval, Krones AG, JBT Corporation, and SPX Flow Inc.

Recent Developments

-

November 2024 - Middleby expands Food Processing Equipment portfolio by acquiring The Vollrath Company, enhancing its capabilities in commercial foodservice solutions.

-

March 2024 - GEA launched InsightPartner to help food manufacturers optimize equipment performance and achieve ambitious sustainability goals through data-driven insights.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 51.40 Billion |

| Market Size by 2032 | USD 72.23 Billion |

| CAGR | CAGR of 4.40% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Mode of Operation (Automatic, Semi-automatic) • By Application (Bakery & Confectionaries, Meat, Poultry & Seafood, Beverage, Dairy, Fruit, Nut & Vegetable, Grains, Others) • By Type (Processing, Pre-processing) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BAADER Group, Marel, Bühler AG, GEA Group Aktiengesellschaft, The Middleby Corporation, Tetra Laval International S.A., Alfa Laval, Krones AG, JBT Corporation, SPX Flow Inc. |

Frequently Asked Questions

Asia-Pacific dominated the food processing equipment market in 2023.

The Automatic Systems segment dominated the food processing equipment market.

The major growth factor of the food processing equipment market is the rising demand for packaged and ready-to-eat food products, driven by technological advancements and automation.

The food processing equipment market size was USD 51.40 billion in 2024 and is expected to reach USD 72.23 billion by 2032.

The food processing equipment market is expected to grow at a CAGR of 4.40% from 2024-2032.

Get in Touch