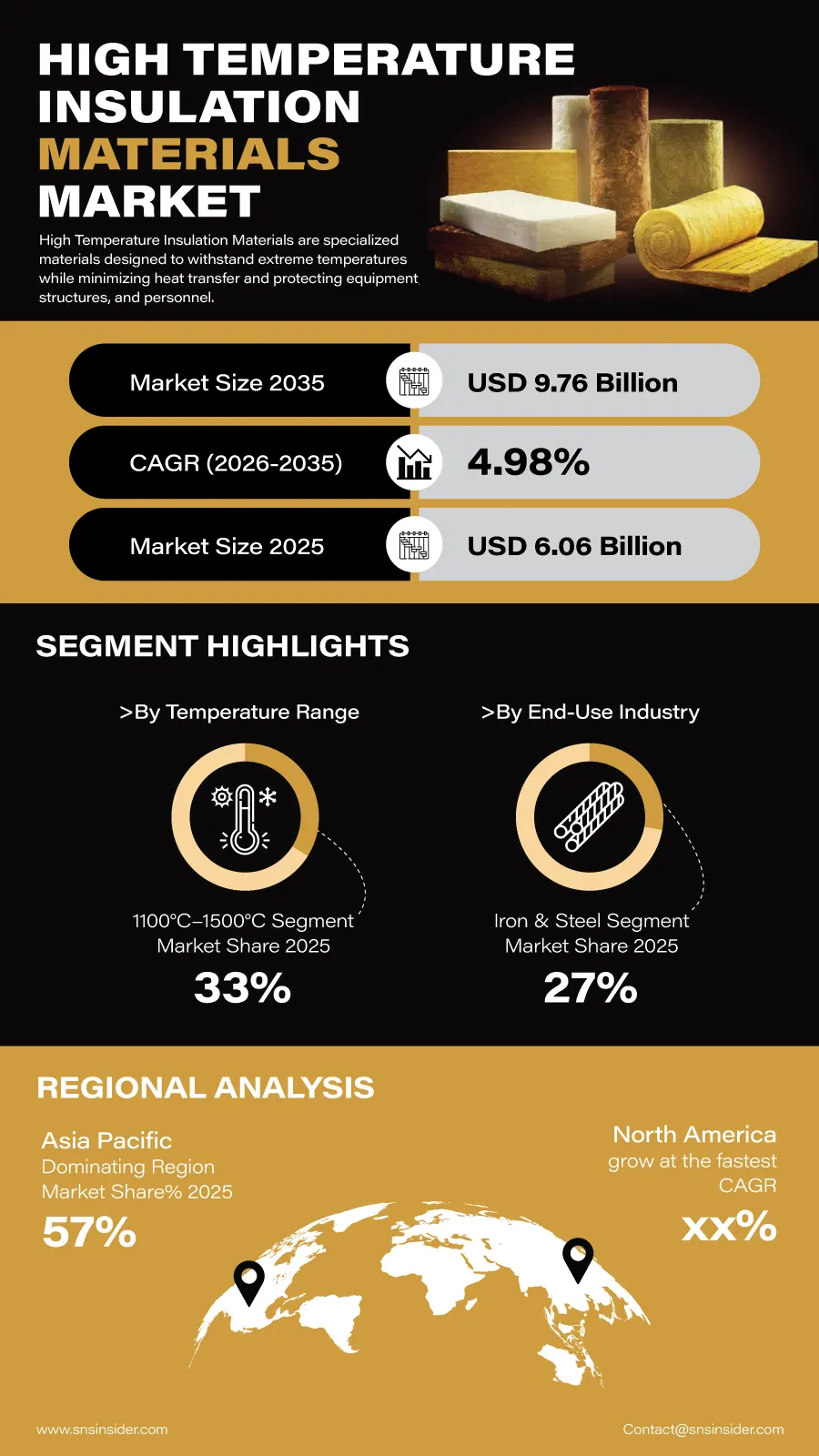

The global High Temperature Insulation Materials market will see significant growth through the next decade owing to rising demands for energy efficiency, process optimization, and safety in the manufacturing processes operating under high temperatures. According to a recent study by SNS Insider, the global High Temperature Insulation Materials Market size valued at USD 6.06 billion in 2025, is anticipated to grow to USD 9.76 billion by 2035, registering a CAGR of 4.98% over the 2026–2035 forecast period.

Rapid industrial growth in the steel, cement, glass, petrochemicals, and power generation industries is driving the growth in demand for thermal insulation materials that are able to handle extreme temperature operations. The adoption of new-age insulation solutions by manufacturers helps them to enhance heat retention capacity and cut down energy losses.

To Get Detailed Insights on the High Temperature Insulation Materials Market – Request a Free Sample Report

Increasing focus on reducing carbon emissions and increasing efficiency in industrial operations is another factor pushing the growth in investments in high-performance insulation materials.

Industrial Energy Efficiency Initiatives Continue to Support Market Expansion

Modernization of manufacturing processes is being actively practiced by industries in order to optimize the usage of energy and minimize the cost of operations. Materials used for thermal insulation in furnaces, boilers, kilns, reactors and other types of equipment in industries contribute to minimizing thermal losses thereby increasing the productivity of industries along with reducing the fuel costs.

Various government policies related to conservation of energy and carbon reduction in industries have further helped in the process. Agencies are continuously motivating industries to adopt advanced systems of thermal management for improving the efficiency and minimizing the emission of greenhouse gases.

Economies that are emerging in the world are making huge investments in their industrial infrastructure especially in manufacturing, petrochemical processing and power generation segments. This trend is expected to result in an increased demand for insulation materials.

Key Market Insights Highlight Shifting Demand Patterns

Segmentation based on material, ceramic fibers will represent almost 40% of market revenue by 2025 because of the material’s outstanding heat resistance, lightweight, and usage in various industries including steel, glass, cement, and petrochemicals. Besides, the ceramic fibers segment is projected to register the highest CAGR through 2035 as a result of growing demand for insulation that can withstand extreme temperatures.

Segmentation by temperature range, insulation materials for 1100°C-1500°C will make up almost 33% of market revenue by 2025 thanks to their extensive utilization in industrial furnaces, kilns, and heat treatment equipment. In addition, the 1700°C and higher segment is expected to experience the fastest CAGR through 2035 because of adoption of ultrahigh-temperature technology in aerospace, metallurgy, and manufacturing industries.

The segment of end-use industry will be dominated by iron and steel as the segment will make up almost 27% of market revenue by 2025 because of ongoing thermal management needs for high-temperature manufacturing processes. Also, the petrochemicals segment will show the highest growth rate thanks to ongoing refinery capacity expansions and investments in chemical processing.

Segmentation according to the application shows that industrial equipment will comprise almost 38% of market revenue by 2025 because of extensive insulation requirements in furnaces, ovens, boilers, and kilns. In turn, energy and power equipment will experience the highest CAGR through 2035 driven by investments in energy generation facilities and thermal energy systems.

An Infographic Representation of the Global High Temperature Insulation Materials Market

Advanced Materials Continue to Transform Industrial Thermal Management

Material development is still one of the main areas of concern for the industry because manufacturers are producing insulation that can provide better thermal performance and durability, as well as greater resistance to harsh working conditions. Ceramic material engineering, refractory development, and innovative lightweight insulation are contributing toward better equipment reliability and less maintenance needs for the industries.

Manufacturers are now forming more cooperation with equipment manufacturers and engineering firms to produce custom insulation systems according to changing manufacturing processes.

Regional Markets Demonstrate Strong Industrial Demand

The Asia Pacific region is forecasted to lead the global market share with more than 57% market revenue by 2025, owing to high rates of industrialization, increased production capacity, and higher demands from the steel, cement, glass, and petrochemical industries. The continued investments in infrastructure development and initiatives to modernize industries will further consolidate the region’s market position.

The North American region is one of the key markets, owing to highly developed industrial infrastructure, regulatory efforts towards energy efficiency, and rising adoption of highly efficient insulation systems for use in aerospace, energy, and manufacturing industries. Europe also holds an appreciable market presence with industries spending money on reducing emissions and adopting new industrial equipment.

With the increase in the focus on improving efficiencies in industrial operations worldwide, the demand for thermal insulation systems is expected to stay resilient during the forecast period.

Industry Participants Focus on Product Innovation and Sustainable Manufacturing

The competitive landscape continues to be very dynamic as manufacturers invest in advanced technologies of insulation, material engineering and increased production capacity. Companies are seeking to improve their competitive positioning through product durability, thermal efficiency, lightweight construction and environmentally sustainable manufacturing processes.

Key companies operating in the global High Temperature Insulation Materials Market include 3M Company, Morgan Advanced Materials plc, Unifrax LLC, Luyang Energy-Saving Materials Co., Ltd., RHI Magnesita GmbH, Isolite Insulating Products Co., Ltd., ADL Insulflex Inc., Almatis GmbH, Aspen Aerogels Inc., Pyrotek Inc., Insulcon Group, Knauf Insulation GmbH, M.E. Schupp Industriekeramik GmbH & Co. KG, Skamol A/S, Rath Group AG, Pacor Inc., Calderys, BNZ Materials Inc., Zircar Zirconia Inc., and Mitsubishi Chemical Holdings Corporation.

An SNS Insider analyst Santosh Bhul commented, “Industrial decarbonization, rising energy efficiency requirements, and continuous investments in advanced manufacturing are creating long-term opportunities for high-temperature insulation materials. Companies that focus on innovative thermal protection technologies, material performance, and sustainable product development will be well positioned to benefit from evolving industrial demand worldwide.”

About the Author

Get in touch