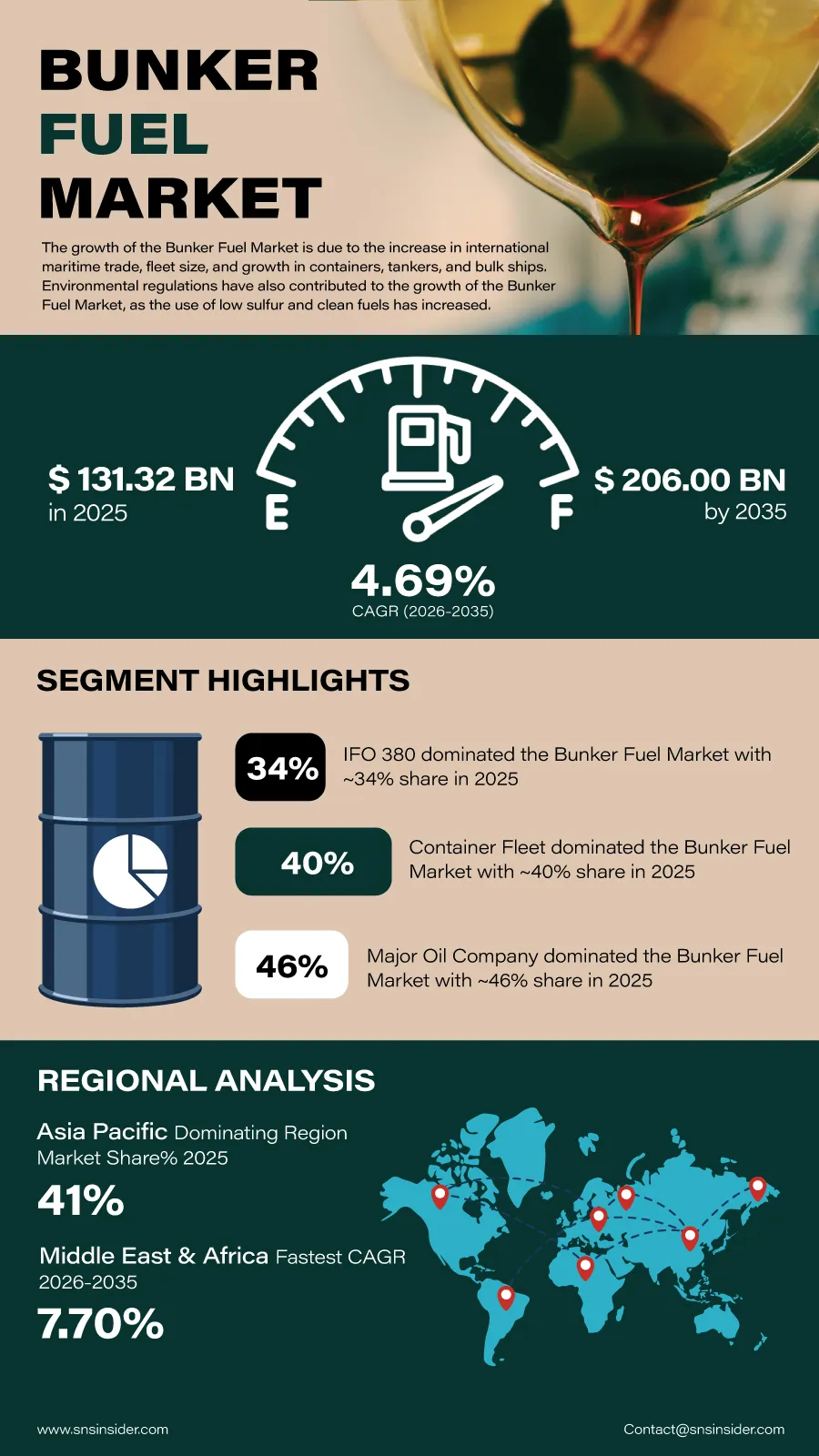

The global Bunker Fuel Market is poised for sustained growth over the coming decade as expanding international maritime trade, increasing fleet deployments, and stricter environmental regulations reshape fuel consumption across the shipping industry. According to a recent study by SNS Insider, the global Bunker Fuel Market size valued at USD 131.32 billion in 2025, is anticipated to grow to USD 206.00 billion by 2035, registering a CAGR of 4.69% over the 2026–2035 forecast period.

Growth in the volume of cargo carried by containers, movement of crude oil, and other bulk commodities leads to increasing demand for marine fuel on main shipping lanes in the world. Shipping firms will continue investing in bunker fuels that are environmentally-friendly and comply with the existing requirements.

To Get Detailed Insights on the Bunker Fuel Market – Request a Free Sample Report

At the same time, shipping business will witness a shift towards more eco-efficient shipping practices in terms of fuels. Increasing adoption of very low sulfur fuel oil (VLSFO), marine gas oil (MGO), liquefied natural gas (LNG), and biofuels will become an important trend in the market.

Clean Marine Fuel Transition Creates New Growth Opportunities

The adoption of more stringent environmental policies is pushing fuel suppliers and shipping firms to increase diversity in their marine fuel mixes. With increasing focus on the reduction of sulfur emissions and overall environmental performance, there will be an increased need for clean fuel that can satisfy emerging policy compliance standards.

There are also investments in LNG bunkering, biofuel manufacturing, and fuel management systems which create new sources of revenue through the entire process of marine fuels. Partnerships between shipping companies, fuel suppliers and port operators also work to improve global bunkering networks and increase security of supply for fuel.

In addition, the upgrade of major ports and development of international shipping routes create a favorable environment for the growth in the use of bunker fuel due to increasing global trade volumes.

Key Market Insights Highlight Shifting Demand Patterns

In terms of fuel grades, IFO 380 is estimated to hold nearly 34% of market share in 2025 owing to its widespread use by large oceangoing ships on long distance international routes. At the same time, marine gas oil (MGO) and marine diesel oil (MDO) will register the highest CAGR up to 2035 owing to increasing adoption of lower sulfur content fuel in order to meet international emission norms.

Considering the end users, container ships are estimated to account for nearly 40% of revenue share in 2025 supported by growing international trades and shipments. Tanker ships are expected to become the fastest growing category owing to rising shipment of crude oil, petroleum and other liquid commodities internationally.

In terms of vendor types, major oil companies are estimated to hold nearly 46% market share in 2025 owing to their high refining capacity and strong business relationship with commercial ship operators. Independent distributors are expected to grow at the highest pace over the forecast period due to rising demand for flexible fuel sources and low sulfur fuel solution.

An Infographic Representation of the Global Bunker Fuel Market

Sustainability and Digitalization Transform Marine Fuel Supply

The bunker fuel industry is increasingly embracing technological innovation to improve operational efficiency and environmental performance. Suppliers are investing in advanced fuel blending systems, digital inventory management platforms, and predictive logistics tools that optimize fuel availability while reducing operational costs.

Shipping companies are simultaneously adopting intelligent voyage planning, emissions monitoring, and fuel optimization technologies to improve fleet performance and comply with evolving international environmental regulations. These developments are expected to strengthen demand for premium marine fuel solutions capable of supporting both regulatory compliance and operational reliability.

Regional Markets Demonstrate Strong Growth Potential

Asia Pacific is expected to account for 41% of the global market value in 2025, due to the existence of large international shipping centres, along with the presence of extensive ports and maritime activities in this region, according to reports. Nations such as China, Singapore, and Japan continue to occupy important positions in the world of shipping, which ensures demand for bunker fuel from container ships, tankers, and bulk carriers.

Middle East & Africa is likely to be the fastest growing regional market, recording a compound annual growth rate of 7.70% over the period from 2026 to 2035. Higher spending on port development, oil exports, maritime logistics and marine fuels drives regional growth, with a location on the most important shipping routes further boosting market potential.

Investments in sustainability in the maritime sector are on the rise, and bunker fuel demand is unlikely to fall anytime soon.

Industry Participants Focus on Cleaner Marine Fuel Innovation

Competition in the bunker fuel market is growing and leading suppliers are investing in cleaner fuel technologies, global distribution networks and decarbonisation efforts. Companies are forging stronger partnerships with shipping operators and producing alternative marine fuels that allow for reduced greenhouse gas emissions and adherence to international environmental standards.

Key companies operating in the global Bunker Fuel Market include Exxon Mobil Corporation, BP Plc, Royal Dutch Shell Plc, TotalEnergies SE, Chevron Corporation, Gazpromneft Marine Bunker LLC, World Kinect Corporation, Bunker Holding, KPI OceanConnect, Peninsula Petroleum, Cockett Marine Oil, Glencore, Trafigura, Vitol, Mercuria Energy Group, Aegean Marine Petroleum Network, Chemoil, Sentek Marine, Minerva Bunkering, and GAC Bunker Fuels.

An SNS Insider analyst Santosh Bhul commented, “The continued expansion of global maritime trade, combined with the industry's transition toward cleaner marine fuels, is creating significant opportunities across the bunker fuel value chain. Companies that invest in sustainable fuel innovation, resilient supply infrastructure, and strategic global partnerships will be well positioned to capitalize on future market growth.”

About the Author

Get in touch