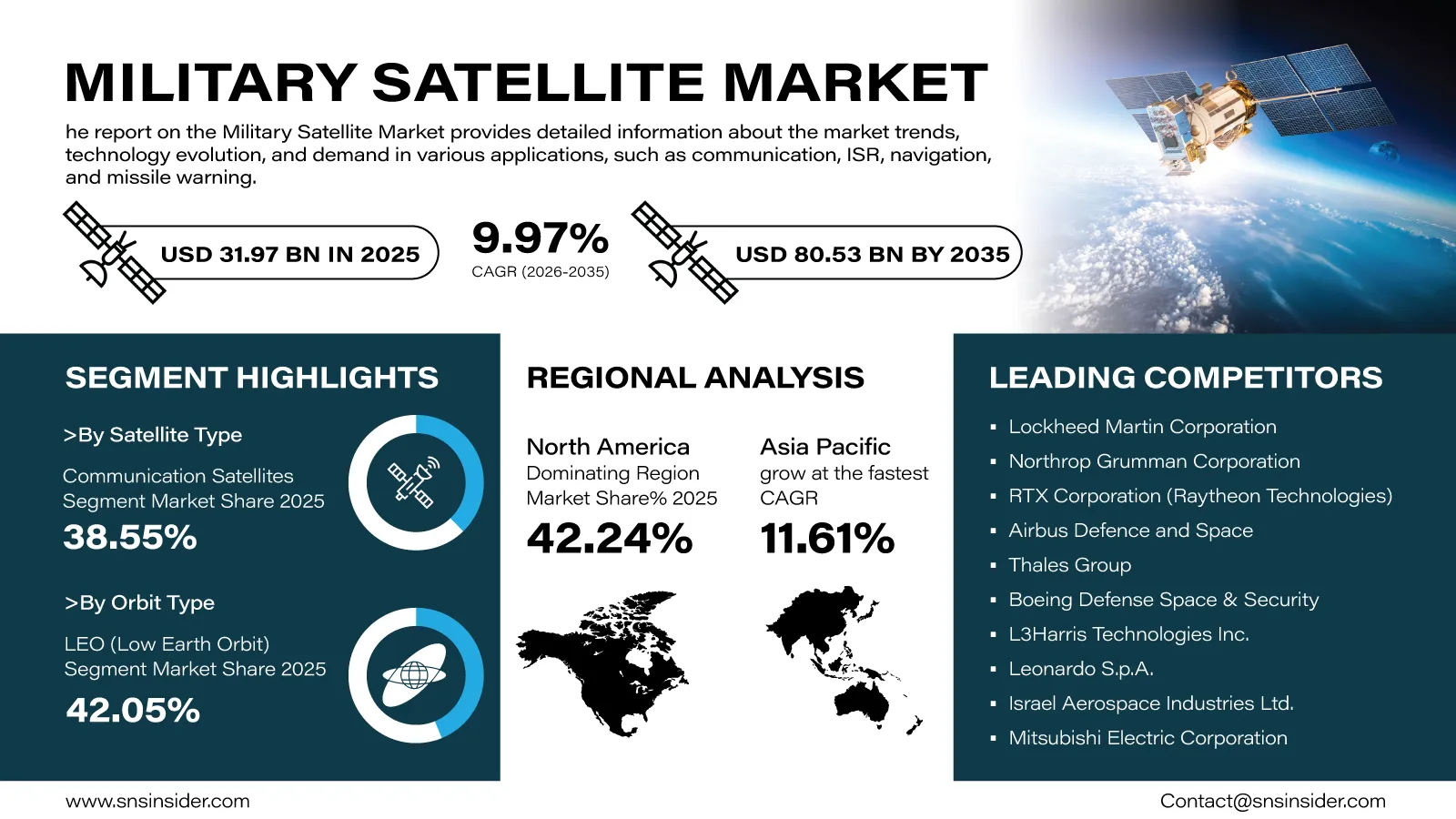

The global Military Satellite Market is expected to witness sustained expansion over the next decade as governments intensify investments in space-based defense infrastructure to strengthen national security, intelligence gathering, and strategic communication capabilities. “According to a recent study by SNS Insider, the global Military Satellite Market size valued at USD 31.97 billion in 2025, is anticipated to grow to USD 80.53 billion by 2035, registering a CAGR of 9.97% over the 2026–2035 forecast period.”

The increasing political instability globally and the critical role that satellites play in the current military strategies have led to an increase in the development of advanced satellite systems all over the world. The development of platforms that provide secure communication and quick threat detection is on the rise.

To Get Detailed Insights on the Military Satellite Market – Request a Free Sample Report

As operations in the military become more data-dependent, there is now a growing emphasis on robust satellite infrastructures that can facilitate uninterrupted connectivity and intelligence. The development trend that has emerged from this situation is the continuous deployment of advanced technology solutions.

Space Defense Modernization Opens New Growth Opportunities

Global priorities for military protection are fast shifting to include space-based capabilities in efforts to safeguard infrastructure and gain an advantage over potential adversaries. The military satellites have become an integral part of the defense infrastructure, playing a key role in command and control, surveillance, and secure communication in the terrestrial, aerial, maritime, cyber, and space environments.

With the rise in LEO satellite constellation launches, military communications will also be transformed, offering low-latency, resilient, and high coverage compared to the traditional satellite systems. In addition, innovations in artificial intelligence, on-board data processing, satellite autonomy, and satellite-to-satellite links have contributed to the efficiency of military operations and reduced reaction time.

Collaboration between the defense agencies and commercial space firms is also fostering technological innovation, providing shortened timelines and increased capacity to manufacture satellites in response to increasing demands globally.

Key Market Insights Highlight Evolving Defense Priorities

The communication satellites segment constituted 38.55% of global market revenue in 2025, due to the important functions that the satellites play in ensuring safe command, coordination, and information exchange during defense operations.

The early warning satellites will be the fastest-growing segment between 2026 and 2035, growing at a 13.35% CAGR due to continued investment in advanced missile detection and space-based threat warning systems.

In terms of the orbit type, low earth orbit (LEO) satellites accounted for 42.05% of market revenue in 2025, due to their capability in ensuring fast communication, high-quality images, and superior surveillance abilities. Also, the LEO satellites will be the fastest-growing segment during the forecast period at a 11.95% CAGR.

In terms of application, military communication accounted for 30.85% of market revenue in 2025, driven by increased demand for military satellites for secure communications. Missile detection and early warning systems will grow the fastest at a 17.45% CAGR over the next decade.

Air Force was the largest user segment of the military satellite market in 2025, accounting for 27.12% of market revenue. Space and defense agencies will grow the fastest over the next decade as countries form special agencies for space commands and indigenous military satellites.

An Infographic Representation of the Global Military Satellite Market

Advanced Space Capabilities Become Central to National Security

The defense establishments around the globe are investing heavily into building a robust space network to increase operational resilience by ensuring that they have reliable access to necessary intelligence amid dynamic security scenarios. Modern military operations involve satellite-assisted monitoring, navigation, reconnaissance, and secure communication.

Constant innovations in terms of payload technologies, synthetic aperture radars, optical imagers, encryption technologies, and AI-based analytical solutions help satellite services evolve beyond traditional uses. All these advances allow defense organizations to be able to detect emerging threats quickly and assist in the faster formulation of military strategy.

As nations pursue greater space autonomy, investments in resilient satellite networks and distributed architectures are expected to remain a long-term priority for defense modernization initiatives.

Regional Markets Demonstrate Strong Investment Momentum

North America is expected to maintain its dominant standing, holding 42.24% share in the total revenue of the Military Satellite Market by 2025. High military spending, strong aerospace industry, investments in military security programs, and existence of major satellite companies support the dominance of North America.

Asia Pacific is anticipated to witness a strong rise in the pace of regional growth, achieving a CAGR of 11.61% over the period till 2035. Growth in defense spending, increase in political tension, local development of satellites, and modernization of military systems in China, India, Japan, and Southeast Asia fuel regional growth.

Growing investments across Europe, Latin America, and the Middle East are also supporting market expansion as governments strengthen surveillance capabilities, border security initiatives, and strategic communications infrastructure through advanced satellite deployments.

Industry Participants Focus on Next-Generation Space Technologies

The competitive landscape remains highly dynamic as aerospace manufacturers and defense technology providers accelerate investments in resilient satellite platforms, advanced payloads, secure communications, and space-based intelligence systems. Companies continue expanding research efforts to deliver more capable, reliable, and scalable satellite solutions aligned with evolving defense requirements.

Key companies operating in the global Military Satellite Market include Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation (Raytheon Technologies), Airbus Defence and Space, Thales Group, Boeing Defense Space & Security, L3Harris Technologies Inc., Leonardo S.p.A., Israel Aerospace Industries Ltd., Mitsubishi Electric Corporation, Ball Corporation, General Dynamics Corporation, OHB SE, Sierra Space Corporation, Maxar Technologies Inc., Saab AB, BAE Systems plc, China Aerospace Science and Technology Corporation (CASC), Indian Space Research Organisation (ISRO), and Korea Aerospace Industries Ltd.

An SNS Insider analyst Santosh Bhul commented, "Growing emphasis on resilient space infrastructure, secure military communications, and real-time intelligence capabilities is reshaping defense investment priorities worldwide. Organizations that continue advancing satellite technologies, AI-enabled mission capabilities, and resilient space architectures will be well positioned to capitalize on the long-term growth opportunities emerging across the global Military Satellite Market."

About the Author

Get in touch