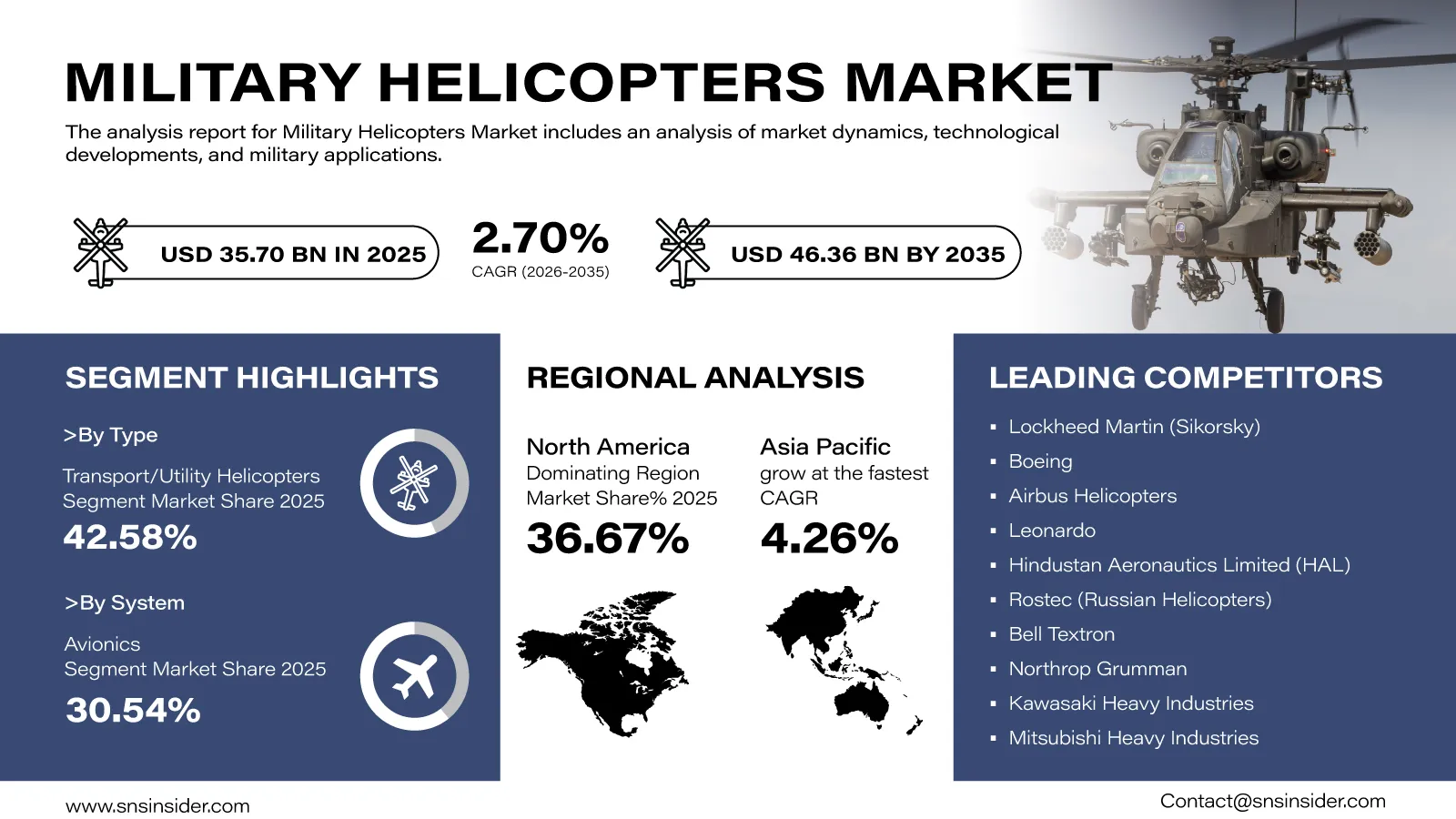

The global Military Helicopters Market is expected to witness steady expansion over the coming decade as defense organizations strengthen aerial mobility capabilities and accelerate investments in next-generation rotorcraft technologies. “According to a recent study by SNS Insider, the global Military Helicopters Market size valued at USD 35.70 billion in 2025, is anticipated to grow to USD 46.36 billion by 2035, registering a CAGR of 2.70% over the 2026–2035 forecast period.”

Across the globe, governments still emphasize defense readiness as part of their efforts to meet new security threats, which have resulted in an increased need for helicopters that can be used in combat, troops transportation, natural disaster situations, reconnaissance, and humanitarian relief missions.

To Get Detailed Insights on the Military Helicopters Market – Request a Free Sample Report

The development of modern military tactics is increasingly necessitating the use of helicopters that are flexible in their operations and equipped with sophisticated avionics. As such, there is a steady demand for helicopters across both mature and newly emerging defense markets.

Defense Modernization Programs Continue to Create Long-Term Market Opportunities

Modernizing militaries is one of the main concerns for many nations working to increase the efficiency of their operations as well as the effectiveness of their fleets. Many governments are spending considerable amounts of money in procuring rotorcrafts, upgrading their fleets and maintaining them.

With increased focus on rapid response capabilities, there has been a heightened need for versatile helicopters that would be used not only for carrying passengers but also for performing special operations, performing rescues and transporting materials.

Moreover, aircraft manufacturers are developing more efficient and cost-effective technologies and solutions such as advanced propulsion systems, intelligent mission management systems and digital maintenance solutions, thus creating more opportunities for further innovation in the helicopter industry.

Key Market Insights Highlight Evolving Procurement Priorities

In the helicopter market, transport and utility helicopters were responsible for generating 42.58% of the revenue in the helicopter market by 2025 because of their importance in transporting troops, logistical operations, humanitarian services, and medevac activities.

On the other hand, attack helicopters are expected to have the highest growth rate until 2035. This is because of the need for precise strikes and modernization of combat aviation units.

As far as helicopter systems are concerned, avionics had a revenue share of 30.54% in 2025. This was because of the use of digital cockpits, navigation aids, and communications technology. Also, airframe systems are expected to have the highest growth rate because of the use of advanced structural designs and lightweight composite materials.

When helicopter applications are considered, combat operations have a market revenue share of 45.82%. This is attributed to the investments being made in battlefield support and tactical aviation. On the contrary, the transport and logistic applications are projected to have the highest growth rate because of the need for mobility and rapid deployment.

Within weight categories, medium helicopters (4–8 tons) maintained market leadership with a 44.71% revenue share, while light helicopters are expected to register the fastest growth due to their versatility, lower operating costs, and suitability for reconnaissance and training missions.

An Infographic Representation of the Global Military Helicopters Market

Technological Innovation and Mission Flexibility Drive Future Procurement

Military defense forces have realized the need for airplanes that can cope with various operating conditions without affecting their performance. Therefore, modern military helicopters are being developed with advanced electronic warfare equipment, situational awareness, autonomous flying abilities, and communications systems.

Life-cycle support is an important issue in today's procurement process. Armed forces are looking for those platforms which have better maintainability, greater availability, and low life-cycle cost, yet they perform well in their missions for a long period of time.

The partnership between government bodies, aerospace industries, and defense companies is continually accelerating the transfer of technology and development programs for multilateral procurement.

Regional Markets Present Strong Growth Prospects

North America captured 36.67% share of worldwide revenues in the Military Helicopters Market in 2025 owing to increased spending on defense, significant fleet modernization efforts, and presence of major aerospace companies. Further spending on next generation military aviation technologies and vertical lift aircraft programs is anticipated to aid the region in retaining its dominant position in the market.

The Asia Pacific region is set to dominate the market with the highest growth rate at a 4.26% CAGR from 2025 to 2035 due to high geopolitical tension in the region, higher defense spending, local production initiatives, and greater procurement of multirole helicopters.

Across Europe, multinational defense cooperation and modernization programs continue supporting demand for advanced military rotorcraft, while emerging economies in Latin America and the Middle East are steadily expanding helicopter procurement to strengthen border security, disaster response, and national defense capabilities.

Leading Manufacturers Focus on Next-Generation Rotorcraft Development

The competitive landscape remains highly dynamic as global aerospace companies continue investing in advanced rotorcraft technologies, digital avionics, mission systems, and sustainable propulsion concepts. Manufacturers are strengthening international partnerships while expanding production capabilities to address evolving defense requirements worldwide.

Key companies operating in the global Military Helicopters Market include Lockheed Martin (Sikorsky), Boeing, Airbus Helicopters, Leonardo, Hindustan Aeronautics Limited (HAL), Rostec (Russian Helicopters), Bell Textron, Northrop Grumman, Kawasaki Heavy Industries, Mitsubishi Heavy Industries, Embraer Defense, Korea Aerospace Industries (KAI), AVIC, Saab AB, Turkish Aerospace Industries (TAI), Israel Aerospace Industries (IAI), General Dynamics, BAE Systems, MD Helicopters, and Enstrom Helicopter Corporation.

An SNS Insider analyst Santosh Bhul commented, "Global defense priorities continue to emphasize fleet modernization, operational flexibility, and advanced mission capabilities. Manufacturers investing in next-generation rotorcraft technologies, digital avionics, and lifecycle support solutions are expected to strengthen their competitive position as military aviation programs evolve across international markets."

About the Author

Get in touch