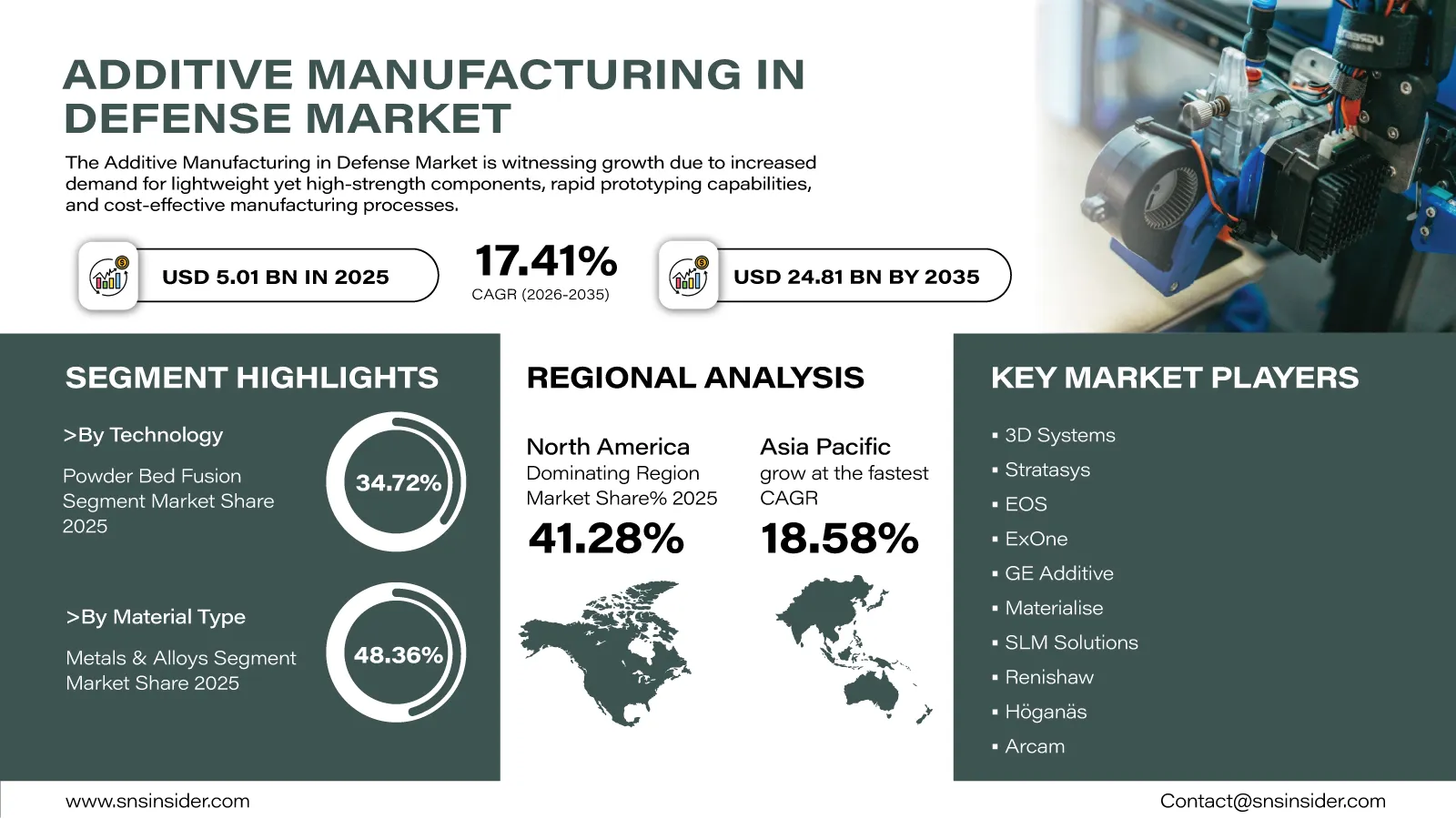

The global Additive Manufacturing in Defense Market is expected to witness significant growth in the coming decade due to the increasing use of advanced manufacturing techniques by defense companies in order to enhance their preparedness and modernize equipment quickly. “According to a recent study by SNS Insider, the global Additive Manufacturing in Defense Market size valued at USD 5.01 billion in 2025, is anticipated to grow to USD 24,800 billion by 2035, registering a CAGR of 17.41% over the 2026–2035 forecast period.”

Increased tensions between nations, rising military spending, and advancements in future-ready military equipment have motivated military organizations to adopt additive manufacturing in their production and maintenance processes. The technology has been accepted due to its potential to significantly reduce time in manufacturing cycles, lessen dependence on traditional supply chain systems, and produce vital components quickly.

To Get Detailed Insights on the Additive Manufacturing in Defense Market – Request a Free Sample Report

Companies producing military gear are increasingly embracing industrial 3D printing as a way of speeding up the design process while at the same time increasing flexibility. The ability to produce complicated pieces with less wastage of materials is becoming a major benefit for military aviation, naval, and ground defense applications.

Defense Modernization Programs Accelerate Adoption of Advanced Manufacturing

Military organizations from leading economies are beginning to emphasize on using digital manufacturing techniques for increasing their operational readiness. Additive manufacturing has been identified as an ability which will help in increasing the rate of prototyping, localized manufacturing and logistics management, especially when dealing with older defense systems that need replacement of hard-to-find components.

Another way the technology is helping with modernization is through redesigning old components and improving their performance while cutting down on their weight. This is contributing to better fuel economy, reliability, and cost savings in the maintenance of defense assets.

With continued investment in the development of resilient manufacturing ecosystems by the defense organizations, there will be a lot of collaborations between government, research institutes, and technology firms in the years to come.

Key Market Insights Highlight Technology Transformation

On account of technology, Powder Bed Fusion held a share of 34.72% in the global market revenue for the year 2025, owing to its ability to create extremely durable metal parts needed in aerospace and defense sector. In contrast, Binder Jetting is expected to achieve the highest CAGR of 18.14% through the forecast period, driven by advancements in terms of production speed and cost efficiency in volume manufacturing.

Amongst material types, Metals & Alloys contributed a share of 48.36% in the market revenue in 2025, as defense manufacturers keep giving preference to strong materials for application in aircraft, ships and vehicles used in military. On the other hand, Composites are projected to achieve the highest CAGR of 18.17%, owing to rising focus on lightweight structures.

The segment of Aircraft & Aerospace Parts was leading amongst all component types, contributing 36.48% of overall market revenue in the year 2025. Nonetheless, weaponry & ammunition is likely to grow at the highest CAGR in the forecast period, due to adoption of additive manufacturing techniques for producing specialized parts.

In terms of end user, Air Force & Aerospace Divisions contributed a share of 37.25% in the market revenue in 2025, whereas Defense Research & Development Organizations are estimated to achieve the highest CAGR of 18.07%.

An Infographic Representation of the Global Additive Manufacturing in Defense Market

Supply Chain Resilience and Operational Readiness Remain Strategic Priorities

Increasingly, defense agencies are placing emphasis on developing manufacturing capabilities that increase operational flexibility while cutting dependence on long procurement processes. Additive manufacturing allows military operators to manufacture qualified parts near the deployment site thus reducing equipment idle time.

In addition, manufacturers are increasing investments in printing materials, automation, and quality control systems that comply with military standards. Improved technologies for metal printing, composite fabrication, and digital engineering are continuously increasing the number of defense applications that are suitable for additive manufacturing.

With increasing complexity of military systems, customization needs for high performance parts will be continuously increasing the demand for this type of technology.

Regional Markets Continue Expanding Through Strategic Investments

In 2025, North America held a 41.28% share of worldwide revenue in the Additive Manufacturing in Defense Market. This market’s growth in North America can be attributed to well-funded research activities by governments in the region, mature defense industrial infrastructure, and wide-ranging applications of additive manufacturing technology in aerospace and defense industries.

On the other hand, Asia Pacific is anticipated to register the fastest growth rate with a CAGR of about 18.58% from 2025 to 2035. Growth in the region is driven by ongoing modernization programs, enhanced capabilities for domestic manufacturing and technological advancements by governments in China, India, Japan, and South Korea.

With governments emphasizing indigenous defense production and advanced manufacturing capabilities, the region is expected to become a significant contributor to future market expansion.

Industry Participants Focus on Innovation and Strategic Collaboration

Competition across the global Additive Manufacturing in Defense Market continues to intensify as technology developers, aerospace manufacturers, and defense contractors invest in advanced production capabilities. Companies are focusing on expanding printable material portfolios, improving manufacturing precision, and accelerating qualification processes to meet evolving military requirements.

Key companies operating in the global Additive Manufacturing in Defense Market include 3D Systems, Stratasys, EOS, ExOne, GE Additive, Materialise, SLM Solutions, Renishaw, Höganäs, Arcam, Markforged, Desktop Metal, Optomec, Voxeljet, HP, Trumpf, Raytheon Technologies, Boeing, Airbus, and Lockheed Martin.

An SNS Insider analyst Santosh Bhul commented, "The growing emphasis on defense modernization, resilient supply chains, and digital manufacturing is transforming additive manufacturing into a strategic capability for military organizations worldwide. Companies that advance material innovation, production scalability, and certified manufacturing processes will be well positioned to capitalize on long-term defense investment opportunities."

About the Author

Get in touch