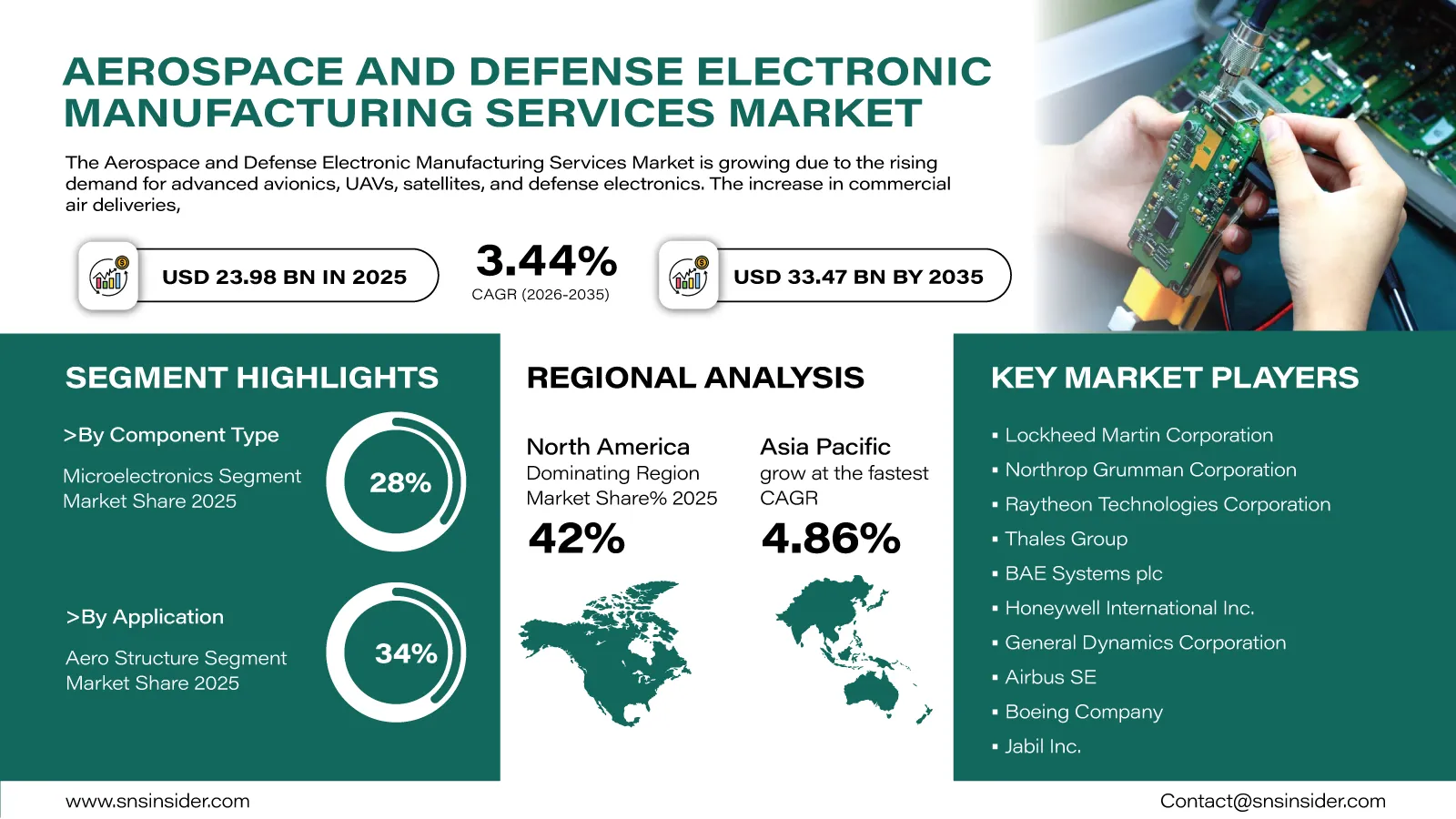

The global Aerospace and Defense Electronic Manufacturing Services (EMS) Market is expected to witness stable long-term growth due to the reliance by aerospace companies, defense agencies, and space organizations on customized EMS services for their advanced aviation and defense technologies. “According to a recent study by SNS Insider, the global Aerospace & Defense Electronic Manufacturing Services Market size valued at USD 23.98 billion in 2025, is anticipated to grow to USD 33.47 billion by 2035, registering a CAGR of 3.44% over the 2026–2035 forecast period.”

Increasing capital being invested in military modernization, airplane manufacturing, satellites launch, and unmanned aerial vehicles is creating changes in the global electronics manufacturing sector. As the technology used in the aviation industry becomes more advanced, companies are opting to use services from electronics manufacturing service providers.

To Get Detailed Insights on the Aerospace & Defense Electronic Manufacturing Services Market – Request a Free Sample Report

This growing reliance on advanced electronic systems, along with the increased complexities and high-quality standards of products, has led to the need for more cooperation between the OEMs and EMS suppliers who can provide mission-critical services.

Defense Modernization and Aircraft Production Expand Industry Opportunities

Governments across the globe have been increasing their budgets on defense spending as airlines ramp up their capacity to cope with growing number of passengers. This combination is causing a consistent demand for sophisticated electronic components for use in various airplanes, satellite, radar systems, communications, and automatic defense systems.

On the other hand, outsourcing has become a major business practice for aerospace organizations that want to make their production more efficient through cost savings. EMS suppliers have been improving their services on PCB assembling, electronics integration, testing, and certifications in order to fulfill complicated demands of aerospace industry.

Furthermore, technological advancements are changing the way production is conducted. Increasing automation, inspection system, digitized manufacturing, and intelligent production are contributing to the increased level of quality as well as production flexibility of EMS companies.

Key Market Insights Highlight Evolving Industry Demand

Under the service type, the most lucrative category was PCB Assembly Services, which held around 28% share of the total revenue generated in 2025 due to increasing demand for electronic assembly solutions among aerospace and defense systems.

The System Integration Services segment is estimated to exhibit the fastest growth rate, considering that future generation aircrafts and defense platforms will need advanced system integration of avionics, communication, navigation and intelligent electronic systems.

By end user, the Commercial category made up nearly 44% of market revenue in 2025 due to continued production of aircraft and increase in airline fleet sizes across the globe. In addition, the Military category is expected to grow the fastest owing to rising government spending on advanced combat aircraft, surveillance systems and defense upgrades.

The microelectronics segment is the largest component segment with market share of around 28%, considering their crucial applications in avionics, navigation, sensor, and control applications. The semiconductor manufacturing services are estimated to witness the fastest growth rate, since there is an increased adoption of high-performance computing in aerospace systems.

In applications, Aero Structure dominated with around 34% share of industry revenue in 2025, while satellite electronics manufacturing is expected to be among the fastest growing markets.

An Infographic Representation of the Global Aerospace & Defense Electronic Manufacturing Services Market

Advanced Electronics Continue to Transform Aerospace Manufacturing

Artificial Intelligence, Internet of Things, advanced sensors, and smart communication systems are quickly making their way into commercial and defense platforms within the aerospace industry. This development is creating the need for manufacturing partners that can provide support for ever more sophisticated electronic designs.

EM companies have been setting up advanced automation, testing systems, and engineering services that conform to the high standards that exist in the aerospace industry. The need for such services has increased as airplanes and defense platforms need more reliability, traceability, and manufacturing accuracy.

Increased use of autonomous aircrafts, connected avionics systems, electronic warfare equipment, and satellite systems is likely to further boost the demand for specialized manufacturing services that can support complex electronics designs.

Regional Markets Present Strong Growth Prospects

The share of North America in the total revenue from the global Aerospace and Defense Electronic Manufacturing Services market in 2025 was nearly 42%. It was due to heavy defense expenditure, well-developed aerospace manufacturing industries, and having many aircraft and defense producers in the region. Further development of cutting-edge aircraft solutions will only reinforce its dominance.

The Asia Pacific region is estimated to show the highest growth rate at a CAGR of 4.86% over the period up to 2035. The growth in the production of aircrafts, defense budget expansion, satellite initiatives, and industrialization in countries, such as China and India are offering many opportunities for local EMS providers.

Europe also maintains a strong market position through ongoing investments in aerospace innovation, research activities, and advanced defense manufacturing capabilities. Meanwhile, Latin America and the Middle East continue expanding aerospace infrastructure and strengthening international manufacturing partnerships.

Industry Participants Strengthen Manufacturing Capabilities

Competition across the Aerospace and Defense Electronic Manufacturing Services Market remains centered on expanding production capacity, improving manufacturing precision, and supporting increasingly sophisticated aerospace electronics. Companies continue investing in automation technologies, engineering expertise, and strategic partnerships to address evolving customer requirements across commercial aviation, defense, and space applications.

Key companies operating in the global Aerospace and Defense Electronic Manufacturing Services Market include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, Thales Group, BAE Systems plc, Honeywell International Inc., General Dynamics Corporation, Airbus SE, Boeing Company, Jabil Inc., Celestica Inc., Sanmina Corporation, Benchmark Electronics, Inc., Plexus Corp., Kimball Electronics, Inc., Creation Technologies LP, Integrated Micro-Electronics, Inc., NEO Tech Inc., Absolute EMS, Inc., and Sonic Manufacturing Technologies.

An SNS Insider analyst Santosh Bhul commented, "Growing investments in aerospace modernization, defense electronics, satellite technologies, and intelligent avionics continue to reshape the global EMS landscape. Manufacturers that strengthen precision engineering capabilities, quality assurance, and advanced integration services will be well positioned to capture long-term opportunities across both commercial and defense aerospace markets."

About the Author

Get in touch