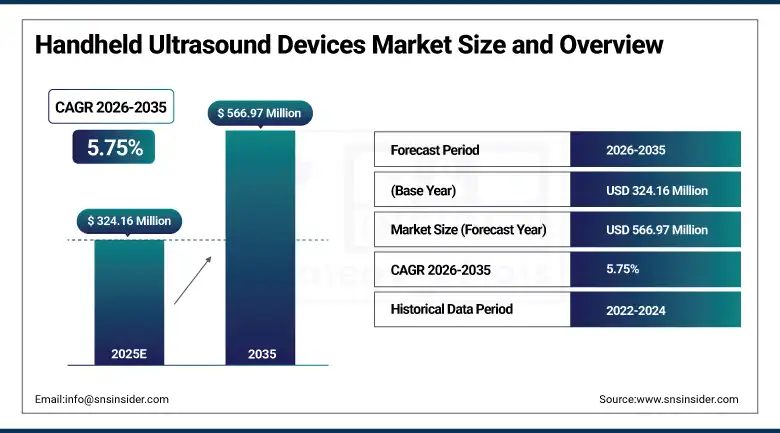

As per the SNS Insider Report titled, Handheld Ultrasound Devices Market by Product Type, by Technology, by Application, by End User, and Region, Global Forecast 2026–2035, “The global Handheld Ultrasound Devices Market was estimated at USD 324.16 Million in 2025, is anticipated to grow to USD 566.97 Million by 2035, registering a CAGR of 5.75% during the forecast period 2026–2035.”

Key Takeaways

-

Portable/Handheld Ultrasound Devices accounted for the largest market share of 45.50% in 2025, driven by their portability, affordability, and growing adoption in point-of-care diagnostics.

-

Wireless/Bluetooth Connected Devices are projected to witness the fastest growth, registering a CAGR of 9.20% during 2026–2035 due to increasing demand for seamless connectivity and real-time data sharing capabilities.

-

3D/4D Ultrasound technology dominated the market with a 36.80% share in 2025 owing to its enhanced imaging capabilities and growing use in prenatal diagnostics and advanced clinical assessments.

-

2D Ultrasound is expected to record the fastest CAGR of 8.60% during the forecast period as healthcare providers seek cost-effective and widely accessible imaging solutions.

-

Obstetrics/Gynecology held the largest application share of 32.40% in 2025, supported by rising demand for fetal monitoring and prenatal imaging services.

-

Trauma applications are anticipated to emerge as the fastest-growing segment with a CAGR of 7.90% through 2035 due to increasing use of portable ultrasound devices in emergency and critical care settings.

-

Hospitals represented the largest end-user segment, accounting for 42.20% of market revenue in 2025 owing to high patient volumes and growing investments in advanced diagnostic technologies.

-

Point-of-Care Clinics are projected to register the fastest CAGR of 8.30% during 2026–2035 as decentralized healthcare delivery models continue to expand globally.

-

North America dominated the Handheld Ultrasound Devices Market with more than 38.10% revenue share in 2025, while Asia Pacific is expected to record the fastest CAGR of 6.96% during the forecast period.

Why Handheld Ultrasound Devices Market is Growing?

The global Handheld Ultrasound Devices Market is witnessing notable growth attributed to the increased adoption of mobile ultrasound solutions that provide fast, affordable, and timely results in various healthcare settings. As there is an increased inclination towards point-of-care diagnostic solutions, healthcare personnel are encouraged to use smaller ultrasound systems that help achieve faster diagnoses and enhance patient outcomes.

Advancements in technology such as miniaturization, wireless technology, and AI-assisted imaging are providing major improvements in the efficacy and functionality of handheld ultrasound devices. They are enabling better diagnostic services by providing advanced imaging at affordable prices throughout hospitals, clinics, emergency units, and even remote healthcare facilities.

There is an increased incidence of chronic disorders, greater utilization of prenatal care services, and increasing use of telemedicine that is helping expand the market size over the forecast period. In addition to this, healthcare institutions are using handheld ultrasounds to make diagnosis easier and save money.

Moreover, the development of healthcare infrastructure and early disease diagnosis are likely to create ample growth opportunities in the market.

Handheld Ultrasound Devices Market Statistics

-

Point-of-care ultrasound adoption is increasing globally as healthcare systems focus on improving diagnostic accessibility and reducing patient wait times.

-

Rising investments in portable medical imaging technologies are supporting the development of compact and highly efficient ultrasound devices.

-

The growing burden of cardiovascular diseases, pregnancy-related complications, and emergency care requirements continues to drive demand for rapid diagnostic imaging solutions.

-

Advancements in wireless communication technologies are enabling seamless integration of handheld ultrasound devices with smartphones, tablets, and cloud-based healthcare platforms.

-

Healthcare providers are increasingly adopting portable imaging tools to support remote patient monitoring and telehealth consultations.

-

Emerging economies are witnessing increased healthcare spending and infrastructure development, creating favorable conditions for market growth.

-

Growing awareness regarding preventive healthcare and early diagnosis is encouraging wider utilization of handheld imaging technologies across diverse medical specialties.

Emerging Trends

There are numerous innovations occurring within the market for Handheld Ultrasound Devices. There have been many developments in the use of artificial intelligence technology for imaging purposes and diagnostic assistance tools.

One of the growing trends that have been identified for handheld ultrasound devices is the use of wireless and smartphone connectivity. With the rise of telemedicine, it has become imperative to have such devices that are more portable and convenient to use.

Another notable trend includes the use of handheld ultrasound devices in areas such as primary care and even home healthcare. These devices offer features including improved battery life, enhanced image resolution, as well as user interface design.

Furthermore, there is a growing trend towards greater need for personalized healthcare and decentralized diagnostic solutions. This is likely to drive further growth in the Handheld Ultrasound Devices Market during the forecast period.

Top 10 Companies

-

GE HealthCare

-

Koninklijke Philips N.V.

-

Siemens Healthineers AG

-

Fujifilm Holdings Corporation

-

Canon Medical Systems Corporation

-

Butterfly Network, Inc.

-

Clarius Mobile Health

-

Samsung Medison Co., Ltd.

-

Mindray Medical International Limited

-

Esaote S.p.A.

About the Author

Get in touch