3nm Process Technology for Semiconductor Market Size

Get More Information on 3nm Process Technology for Semiconductor Market - Request Sample Report

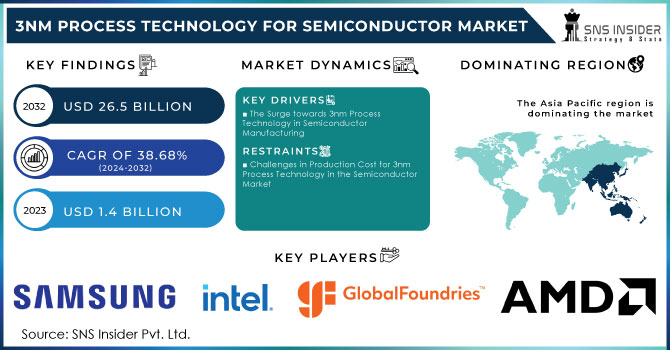

The 3nm Process Technology for Semiconductor Market Size was valued at USD 1.4 Billion in 2023 and is expected to grow to USD 26.5 Billion by 2032 and grow at a CAGR of 38.68% over the forecast period of 2024-2032.

The 3nm process technology for Semiconductor market is at the forefront of a new era in high-performance computing, energy efficiency, and technological advancements. Its development marks a critical leap in microprocessor fabrication, addressing the ever-growing need for faster and more energy-efficient chips across various industries. This transition has significant implications for sectors such as artificial intelligence (AI), cloud computing, mobile devices, automotive technology, and the Internet of Things (IoT).

One of the primary advantages of the 3nm process is its ability to enhance both performance and power efficiency. by reducing transistor size, manufacturers can fit more transistors onto a single chip, leading to a substantial boost in processing power. Specifically, 3nm technology offers a 15-18% increase in performance compared to its predecessor, the 5nm node. Simultaneously, it enables up to a 30% reduction in power consumption. This dual improvement is essential for industries where balancing high performance with energy efficiency is critical. For instance, in cloud computing and AI-driven systems, the ability to process large volumes of data while maintaining lower energy usage is vital for optimizing operational costs and reducing carbon footprints.

TSMC’s Optimism in AI and Automotive Chips in Japan

TSMC is optimistic about the burgeoning demand for AI in Japan, especially as it introduces its 3nm process technology tailored for automotive chips. This move underscores TSMC's focus on meeting the rising needs of advanced automotive applications and AI-driven innovations.

Huawei's Advances in Semiconductor Manufacturing despite US Sanctions

Meanwhile, Huawei is making strides in semiconductor advancements despite US sanctions, focusing on 3nm-class manufacturing. The company, alongside Semiconductor Manufacturing International Co. (SMIC), has patented self-aligned quadruple patterning (SAQP) lithography techniques aimed at producing advanced microchips. This method enhances transistor density, reduces power consumption, and improves performance, crucial for the evolving semiconductor market.

SAQP’s Role in Huawei’s 3nm Ambitions

Although SAQP was initially believed to apply only to 5nm-class chips, Huawei's plans to leverage this technique for 3nm-class technology display its ambition to advance semiconductor fabrication. Despite restricted access to leading-edge lithography tools, Huawei aims to implement SAQP to produce next-generation processors for consumer electronics and AI servers.

China’s Semiconductor Capabilities: Challenges and Potential

The costs of producing 3nm chips using SAQP may be elevated, but this technology is vital for enhancing China’s semiconductor capabilities. Innovations driven by this method could affect supercomputing, military applications, and other sectors, further elevating China's role in the global semiconductor industry.

3nm Process Technology for Semiconductor Market Dynamics

Drivers

-

The Surge towards 3nm Process Technology in Semiconductor Manufacturing

The rapid advancement of 3nm process technology is significantly driven by increasing demand from major tech companies like Intel and Apple, who are preparing to release new products in 2024 that leverage this cutting-edge technology. TSMC, a leading semiconductor manufacturer, has ramped up its 3nm production capacity, which is now operating at 100% capacity to meet this escalating demand. The shift to 3nm technology is not only aimed at enhancing performance but also improving energy efficiency. The introduction of advanced designs, such as Eliyan's chiplet interconnect PHY capable of 64 Gbps data transfer, highlights the critical role of 3nm technology in delivering high-performance solutions for applications like AI and 5G. TSMC’s progress has exceeded expectations, positioning the company as a frontrunner in the semiconductor market. This momentum underscores the vital connection between next-generation chip manufacturing and the innovation requirements of leading tech firms, creating a strong push towards adopting 3nm process technology across various sectors.

Restraints

-

Challenges in Production Cost for 3nm Process Technology in the Semiconductor Market

One significant restraint for the 3nm process technology in the semiconductor market is the high cost of production. The transition to 3nm technology involves substantial investments in advanced fabrication equipment and materials. For example, Samsung's investment in its 3nm production facilities is reportedly around USD 17 Billion, and TSMC is also expected to invest significantly to support its N3 node production, with estimates suggesting costs could reach around USD 40 Billion for the necessary technological advancements and infrastructural costs create barriers to entry for smaller manufacturers and may slow down the adoption of 3nm technology across the industry as companies evaluate the return on investment. Furthermore, as the production scale increases, achieving profitability becomes increasingly complex amid fluctuating market demand for high-performance chips.

3nm Process Technology for Semiconductor Market Segment Analysis

by Type

The 3nm process technology for semiconductors market prominently features advanced manufacturing techniques, with the FinFET (Fin Field-Effect Transistor) process taking a leading role. In 2023, FinFET accounted for approximately 70% of the revenue share in the 3nm semiconductor market, highlighting its established significance and technological benefits. One of the primary reasons for FinFET's dominance is its superior performance and power efficiency compared to traditional planar transistors. This efficiency is vital for high-performance applications like data centers and artificial intelligence (AI) processing.

Moreover, the scalability of FinFET technology allows for effective downsizing of transistor sizes while preserving performance, which is crucial as the semiconductor industry moves toward smaller nodes. The widespread adoption of FinFET by major players in the industry is fueled by the growing demand for high-performance computing, mobile devices, and advanced AI applications. Substantial investments in research and development have led to further enhancements in FinFET technology, reinforcing its status as the preferred choice for manufacturers aiming to produce next-generation chips. FinFET technology's compatibility with existing manufacturing infrastructure enables companies to upgrade their production capabilities without the need for extensive facility overhauls.

by Application

The 3nm process technology for semiconductors market has significantly reshaped the application landscape, with central processing units (CPUs) commanding the largest revenue share of approximately 45% in 2023. This leadership highlights the vital role of CPUs in the semiconductor ecosystem, especially within high-performance computing environments. Several factors drive the CPU's prominence in the 3nm semiconductor market.

The demand for enhanced performance is ever-increasing, particularly to support advanced applications like cloud computing, gaming, and data analytics. The 3nm process technology enables manufacturers to develop faster and more efficient CPUs that cater to both consumer and business needs.

Energy efficiency is critical, and the 3nm technology allows for significant reductions in power consumption, essential for mobile devices that prioritize battery life. Continuous advancements in CPU design and architecture further fuel the adoption of 3nm technology, with recent product launches showcasing enhanced multi-core architectures and improved thermal management. The rise of artificial intelligence (AI) and machine learning applications creates a demand for powerful CPUs capable of managing complex computations.

3nm Process Technology for Semiconductor Market Regional Outlook

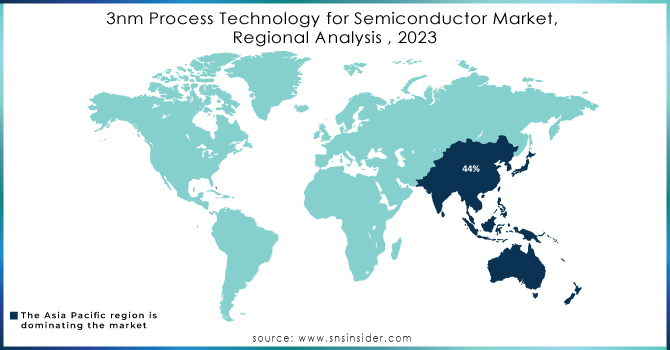

In 2023, the Asia Pacific region established itself as a dominant force in the 3nm process technology for semiconductors, capturing approximately 44% of the market share. The region is home to major semiconductor foundries, particularly in Taiwan, South Korea, and China. Taiwan's top foundries, for instance, have made significant investments in advanced fabrication technologies, expediting the adoption of 3nm processes and enabling the production of high-performance chips for various applications.

Numerous companies in the region have launched products utilizing 3nm technology, including processors for mobile devices and high-performance computing, showcasing notable improvements in speed and energy efficiency. Countries like China are actively pursuing self-sufficiency in semiconductor manufacturing through investments in domestic foundries and research. Meanwhile, industries in Japan, India, and Australia are increasingly adopting 3nm chips for AI, machine learning, and consumer electronics. The commitment to research and development across South Korea and Singapore focuses on innovative designs and manufacturing efficiencies.

North America has established itself as the fastest-growing region in the 3nm process technology for semiconductors, driven by key factors that highlight its significant role in the semiconductor industry. In 2023, the region's growth is fueled by a robust ecosystem comprising technology companies, research institutions, and innovative startups, all contributing to advancements in semiconductor manufacturing. Technological Innovation is at the forefront, with numerous leading semiconductor firms investing heavily in research and development (R&D). These companies are continually pushing the limits of chip performance, power efficiency, and scalability.

Recent product launches, including next-generation processors for data centers and high-performance computing, exemplify how 3nm technology meets the demands of sophisticated applications. The strong demand from key industries such as automotive, telecommunications, and artificial intelligence further propels the adoption of 3nm technology. Efficient chips capable of supporting complex functionalities, like autonomous driving and 5G connectivity, position North America as a crucial player in the global semiconductor market. Government support through funding initiatives and investments in semiconductor manufacturing facilities enhances innovation and infrastructure development. Additionally, a highly skilled talent pool and collaboration between academia and industry facilitate the transfer of knowledge, driving growth in the 3nm sector.

Need Any Customization Research On 3nm Process Technology for Semiconductor Market - Inquiry Now

Key players

Some of the Major players in 3nm Process Technology for Semiconductor Market who provide product and offering:

-

Taiwan Semiconductor Manufacturing Company (CPUs, GPUs, mobile processors, custom chips)

-

Samsung Electronics (Exynos processors, memory chips, semiconductor solutions)

-

Intel Corporation (Core processors, Xeon processors, chipsets)

-

GlobalFoundries (Custom chips for automotive and IoT)

-

Advanced Micro Devices (Ryzen processors, EPYC server chips, Radeon GPUs)

-

Qualcomm (Snapdragon processors, AI chips, automotive solutions)

-

Broadcom Inc. (Networking processors, wireless communication chips)

-

NVIDIA Corporation (GeForce GPUs, AI processors, data center accelerators)

-

Apple Inc. (A-series chips for iPhones, M-series chips for Macs)

-

Texas Instruments (Analog chips, embedded processors, digital signal processors)

-

Micron Technology (DRAM, NAND flash memory)

-

Infineon Technologies (Power semiconductors, automotive solutions)

-

MediaTek (SoCs for mobile devices, smart TVs, IoT)

-

STMicroelectronics (Microcontrollers, sensors, power management chips)

-

ON Semiconductor (Power management, sensors, automotive solutions)

-

Renesas Electronics (Microcontrollers, automotive ICs, power semiconductors)

-

SK hynix (Memory chips, DRAM, NAND flash)

-

Western Digital (Storage solutions, SSDs)

-

Marvell Technology Group (Networking processors, storage solutions)

-

Analog Devices (Analog chips, mixed-signal ICs)

List of Suppliers:

-

ASML

-

Applied Materials

-

Lam Research

-

KLA Corporation

-

Tokyo Electron Limited Micron Technology

-

STMicroelectronics

-

Infineon Technologies ON Semiconductor

-

NXP Semiconductors Others

Recent Development

-

On October 10, 2024, Eliyan Corporation announced a major advancement in the semiconductor sector with the successful delivery of its first silicon for the NuLink™-2.0 PHY, fabricated using a 3nm process. This groundbreaking achievement establishes a new benchmark in chiplet interconnect technology, achieving an industry-leading performance of 64Gbps per bump for die-to-die PHY solutions.

-

On July 18, 2024, Monica Chen and Jessie Shen from DIGITIMES Asia reported that TSMC's monthly production of 3nm chips is projected to increase to 125,000 wafers in the latter half of the year, rising from the current output of 100,000 wafers. This increase in production capacity is attributed to the foundry's rapid expansion efforts.

-

On September 2, 2024, Swarajya Staff reported that China's leading chipmaker, SMIC, is advancing in semiconductor production by developing 5-nanometer chips through alternative methods like quadruple patterning. Although SMIC's technology lags behind TSMC's leading-edge solutions by a generation, this progress marks a significant achievement for China's semiconductor sector. However, acquiring EUV lithography machines remains crucial for its long-term competitiveness.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.4 Billion |

| Market Size by 2032 | USD 26.5 Billion |

| CAGR | CAGR of 38.68% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (GAA (Gate All Around) Technology, FinFET Process) • by Application (CPU, GPU, Mining Chip, Other) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Taiwan Semiconductor Manufacturing Company, Samsung Electronics, Intel Corporation, GlobalFoundries, Advanced Micro Devices, Qualcomm, Broadcom Inc., NVIDIA Corporation, Apple Inc., Texas Instruments, Micron Technology, Infineon Technologies, MediaTek, STMicroelectronics, ON Semiconductor, Renesas Electronics, SK hynix, Western Digital, Marvell Technology Group, and Analog Devices & Others |

| Key Drivers | • The Surge towards 3nm Process Technology in Semiconductor Manufacturing |

| RESTRAINTS | • Challenges in Production Cost for 3nm Process Technology in the Semiconductor Market |

Frequently Asked Questions

Challenges include the high cost of research and development, the complexity of manufacturing at such a small scale, and ensuring that semiconductor fabs are equipped with the necessary technology to produce chips at 3nm efficiently.

Ans: 3nm process technology refers to an advanced semiconductor manufacturing node that enables the creation of smaller, more powerful, and energy-efficient chips, crucial for applications in AI, 5G, and high-performance computing.

Ans: Taiwan Semiconductor Manufacturing Company, Samsung Electronics, Intel Corporation, GlobalFoundries, Advanced Micro Devices, Qualcomm, Broadcom Inc., NVIDIA Corporation, Apple Inc., Texas Instruments, Micron Technology, Infineon Technologies, MediaTek, STMicroelectronics, ON Semiconductor, Renesas Electronics, SK hynix, Western Digital, Marvell Technology Group, and Analog Devices & Others

Ans: The 3nm Process Technology for Semiconductor Market grow at a CAGR of 13.44% over the forecast period of 2024-2032.

Ans: 3nm Process Technology for Semiconductor Market size was valued at USD 1.4 Billion in 2023 and is expected to grow to USD 26.5 Billion by 2032

Get in Touch