5G NTN Market Report Scope and Overview:

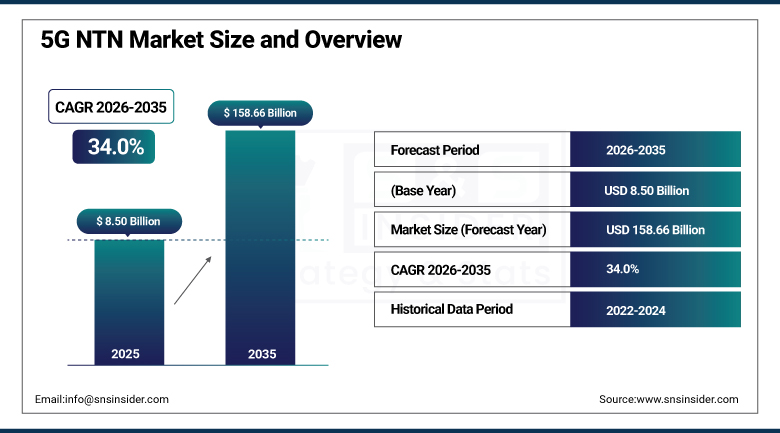

The 5G NTN Market was valued at USD 8.50 Billion in 2025 and is projected to reach USD 158.66 Billion by 2035, registering a CAGR of 34.0% from 2026 to 2035.

The 5G NTN Market is revolutionizing the future of global communications by expanding 5G networks outside terrestrial networks via satellite, high-altitude platform, and airborne solutions. The market is characterized by an increase in demand for ubiquitous connectivity, growth in direct-to-device satellite communications, increased blending of satellite and terrestrial 5G networks, and adoption in defense, maritime, aviation, and enterprise applications in remote areas. Significant growth is being witnessed in the area of low Earth orbit satellite deployment, IoT connectivity, and emergency communications services, considering that governments, telecom operators, and satellite service providers are spending heavily on establishing resilient networks that can provide continuous connectivity in remote regions where building terrestrial networks may not be economical.

T-Mobile continued expanding its Direct-to-Cell satellite service partnership with SpaceX's Starlink constellation throughout 2025, letting standard smartphones connect directly to satellites for text messaging and emergency communication in areas without terrestrial cellular coverage across the United States.

Market Size and Forecast

-

Market Size in 2026E: USD 11.39 Billion

-

Market Size by 2035: USD 158.66 Billion

-

CAGR: 34.0% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America (35.0% share in 2025)

To Get more information On 5G NTN Market - Request Free Sample Report

5G NTN Market Trends

-

Growing convergence of terrestrial and non-terrestrial networks continues enabling seamless handover between cellular and satellite systems.

-

Advancements in beamforming and spectrum sharing technologies continue optimizing satellite capacity for 5G services.

-

Increasing standardization through recent 3GPP releases continues defining NTN architecture, protocols, and interoperability across vendor ecosystems.

-

Rising investment in direct-to-device satellite connectivity continues eliminating the need for specialized user equipment, letting standard smartphones connect directly to satellites.

-

Rapid cost compression in satellite manufacturing and launch services continues making large constellation builds economically viable for a broader pool of operators.

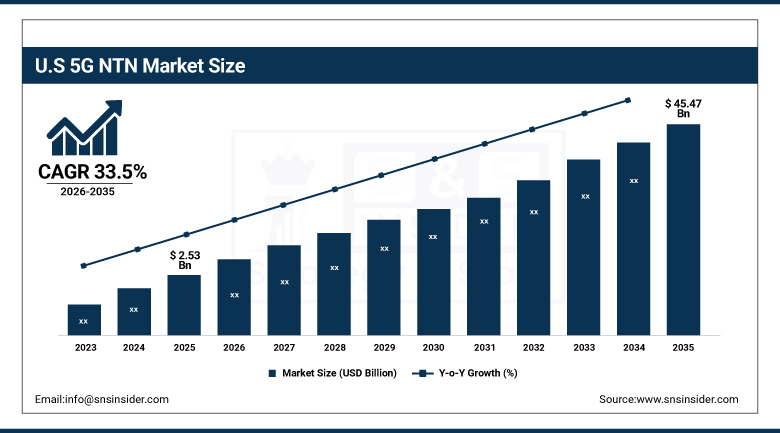

U.S. 5G NTN Market Outlook

The U.S. 5G NTN Market was valued at approximately USD 2.53 Billion in 2025 and is projected to reach approximately USD 45.47 Billion by 2035, registering a CAGR of approximately 33.5% from 2026 to 2035.

Demand across the United States continued to be shaped by aggressive carrier investment in direct-to-device satellite partnerships, a deep concentration of leading satellite operators and chipset manufacturers, and strong defense sector demand for resilient, satellite-enabled communication infrastructure. Rising deployment of low Earth orbit satellite constellations by domestic operators continued reinforcing the country's position as both an early adopter and a genuine innovation hub for 5G NTN technology. Growing adoption across aviation, maritime, and remote enterprise applications added further layers of sustained domestic demand well beyond the technology's original emergency-communication use case.

AST SpaceMobile continued expanding its constellation of BlueBird satellites throughout 2025, designed to enable direct broadband cellular connectivity from space to standard, unmodified smartphones, targeting American carrier partnerships aimed at closing rural and remote connectivity gaps across the United States.

5G NTN Market Segment Analysis

-

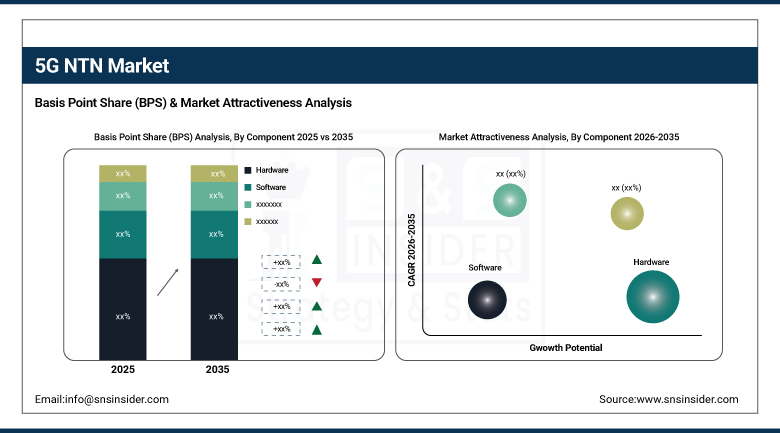

By Component, Hardware segment dominated the 5G NTN Market in 2025 with 49% share; Services segment is the fastest growing segment.

-

By Platform, LEO Satellite segment dominated the market in 2025 with 46% share; LEO Satellite segment is also the fastest growing segment.

-

By Location, Urban segment dominated the market in 2025 with 52% share; Remote segment is the fastest growing segment.

-

By Application, Enhanced Mobile Broadband (EMBB) segment dominated the market in 2025 with 48% share; Massive Machine-Type Communications (MMTC) segment is the fastest growing segment.

-

By End-Use, Aerospace & Defense segment dominated the market in 2025 with 34% share; Maritime segment is the fastest growing segment.

By Component, Hardware Dominates the 5G NTN Market While Services Emerge as the Fastest-Growing Component Segment

The Hardware segment dominated the 5G NTN Market in 2025 due to massive spending on satellite payloads, onboard communication devices, phased array antennas, ground stations, and user terminals. The development of satellite constellations in the low earth orbit would have necessitated substantial spending on hardware for creating a reliable non-terrestrial communication infrastructure. Increasing use of advanced RF devices, beamforming, and satellite gateways in commercial and government networks has boosted hardware revenues, which are expected to contribute the highest share of total revenues.

The Services segment is the fastest growing in the 5G NTN Market owing to the rising need for satellite network integration, deployment, maintenance, optimization, cyber security, and managed connectivity services. The increasing commercialization of non-terrestrial networks has been driving the need for consultancy, system integration, and lifecycle management services in aviation, maritime, and enterprise markets. Regular software upgrades, performance management, and regulatory compliance services have become crucial as more operators are expanding their NTN networks globally.

By Platform, LEO Satellites Dominate the 5G NTN Market and Register the Fastest Growth

The LEO Satellite segment dominated the 5G NTN Market because of the fast communication speeds, high throughput capacity, and global coverage that they offered. The rapid launching of large LEO satellites facilitated broadband connections even in underserved and hard-to-reach areas. High levels of investment by commercial satellite providers, together with their ability to support direct-to-device communications and improve spectrum efficiency, boosted the use of LEO satellites in consumer, enterprise, defense, and emergency communication applications.

The LEO Satellite segment is also the fastest growing due to growing number of launches of satellite constellations that enable direct-to-smartphone connections and high-speed broadband. Technological innovations within satellite production, reusable launch vehicles, and inter-satellite laser links are decreasing costs and improving performance. Growing need for connectivity in the transportation sector, disaster recovery efforts, industrial operations, and rural broadband projects boosts the growth of LEO-based non-terrestrial communication systems.

By Location, Urban Areas Dominate the 5G NTN Market While Remote Areas Witness the Fastest Growth

The Urban segment dominated the 5G NTN Market due to high demand for uninterrupted broadband connections and reliable communication networks in densely populated cities. The Non-terrestrial networks support the terrestrial 5G networks through enhanced coverage, decreased congestion, and reliable fallback in case of disruption of communication. More applications of the smart city technology, connected mobility, public safety, and enterprise communications in urban areas with heavy network traffic drove the growth of the market share of NTNs.

The Remote segment is the fastest growing in the 5G NTN Market owing to the expansion of connectivity into underserved and isolated regions without terrestrial infrastructure by governments and network operators. 5G NTN allows for reliable broadband connectivity in mining, energy, agriculture, healthcare, education, and emergency services in remote regions. Initiatives toward digital inclusion, lower cost of deployment of satellites, and demand for reliable communication in difficult-to-reach places drive the adoption of NTNs in remote regions.

By Application, Enhanced Mobile Broadband (eMBB) Dominates the 5G NTN Market While Massive Machine-Type Communications (mMTC) Records the Fastest Growth

The Enhanced Mobile Broadband (EMBB) segment dominated the 5G NTN Market due to increase in the need for fast Internet, video streaming, and broadband internet outside the coverage of the terrestrial network. Satellite-enabled broadband communication provides consumers' communication, enterprises, transportation, and emergency communication in tough conditions. Increasing deployment of low-earth orbit satellites and the use of direct device technology increased the uptake of EMBB by offering better user experience in various geographical locations.

The Massive Machine-Type Communications (MMTC) segment is the fastest growing billions of IoT devices that require connectivity. The NTN supported by satellite ensures effective communication of the smart agriculture, environment monitoring, logistics, utility management, and industrial automation in remote places. Growth in the use of connected sensors, asset tracking, and machine-to-machine communication, in addition to the expansion of IoT, is leading to faster growth of MMTC application globally.

By End-Use, Aerospace & Defense Dominates the 5G NTN Market While Maritime Emerges as the Fastest-Growing End-Use Segment

The Aerospace & Defense segment dominated the 5G NTN Market due to increased demand for reliable and constant connectivity through satellites in military and aerospace operations. Satellite-based 5G offers intelligence gathering, surveillance, field-to-field connections, command and control, and unmanned system operation beyond terrestrial connectivity. Increased investments and modernizations in defense and satellite communications in aerospace and national security organizations contributed to their adoption in the industry.

The Maritime segment is the fastest growing in the 5G NTN Market because ship operators demand high-speed and reliable internet even in oceans where terrestrial network is not accessible. Satellite 5G provides ship tracking, communication between the crew, predictive maintenance, cargo tracking, navigation and safety operations. Digitalization in commercial shipping, offshore drilling, autonomous ships, and global maritime logistics is increasing demand for non-terrestrial communication services.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|

North America |

United States |

81.60% |

|

Europe |

Germany |

24.20% |

|

Asia Pacific |

China |

31.85% |

|

Middle East and Africa |

UAE |

26.75% |

|

Latin America |

Brazil |

34.50% |

North America 5G NTN Market Insights

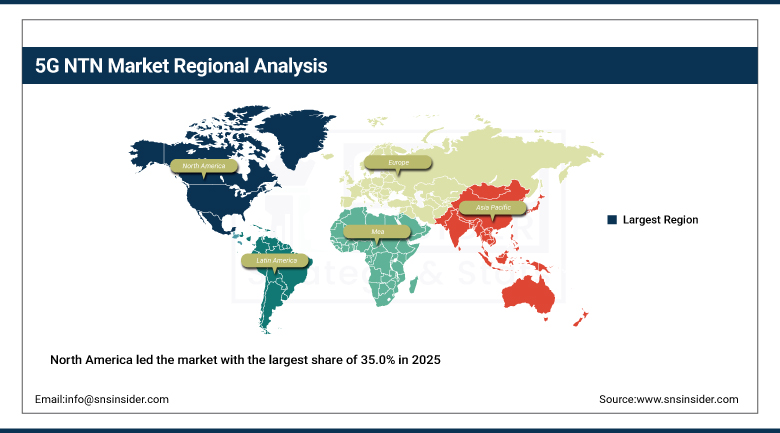

North America led the market with the largest share of 35.0% in 2025. The growing demand for high-speed connectivity, particularly in remote and underserved areas, has propelled adoption of NTN solutions, and a deep concentration of leading satellite operators, chipset manufacturers, and defense contractors headquartered across the continent continued reinforcing this dominant regional position.

The United States accounted for roughly 81.60% of regional revenue, anchored by aggressive carrier investment in direct-to-device satellite partnerships and substantial domestic satellite manufacturing and launch capability. Canada added further regional demand through its own growing remote connectivity initiatives, and that combined strength kept the continent the largest addressable market for 5G NTN vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe 5G NTN Market Insights

Europe held a meaningful share of global revenue, supported by growing government investment in satellite communication sovereignty and continued expansion of the European Space Agency's connectivity initiatives across the region's major economies. Regulatory momentum around spectrum allocation for satellite broadband continued removing historically significant barriers to NTN commercialization across the continent.

Germany led demand at roughly 24.20% of European revenue, supported by its substantial aerospace and defense manufacturing base. The UK and France contributed substantial additional demand, and continued European investment in satellite communication sovereignty should keep regional demand for 5G NTN technology climbing through the forecast period.

Asia Pacific 5G NTN Market Insights

Asia Pacific is advancing at the fastest pace among all regions tracked in this report, driven by rapid satellite constellation deployment, expanding rural connectivity initiatives, and growing government-backed investment in domestic satellite manufacturing capability across the region's largest economies. That combination of manufacturing scale and genuine connectivity need across vast underserved rural populations kept the region's growth trajectory well ahead of every other region tracked in this report.

China led the pack, supported by substantial government investment in domestic satellite constellation development and rural connectivity infrastructure. Japan and India contributed meaningful additional demand, with India's vast underserved rural population and Japan's advanced satellite manufacturing capability both reinforcing the region's position as the fastest-growing market tracked in this report.

MEA and Latin America 5G NTN Market Insights

The Middle East and Africa and Latin America both showed steady growth, driven by expanding rural and remote connectivity initiatives, growing government focus on digital inclusion, and rising demand for resilient communication infrastructure across both areas. As these markets continued building out modern telecommunications infrastructure, 5G NTN technology proved a genuinely efficient way to reach populations that terrestrial networks had never adequately served.

The UAE led Middle East and Africa demand, supported by the country's advanced satellite communication infrastructure and substantial digital inclusion investment. Saudi Arabia contributed further demand through its own rural connectivity programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing rural and remote connectivity needs continuing to anchor regional demand for 5G NTN technology.

Market Dynamics

Growth Drivers: Rising Demand for Ubiquitous Connectivity and Direct-to-Device Expansion

The industry is driven by rising demand for ubiquitous connectivity, expansion of direct-to-device satellite communications, increasing integration of satellite and terrestrial 5G infrastructure, and growing adoption across defense, maritime, aviation, and remote enterprise applications. As the number of connected devices and data-intensive applications continues to rise, the need for robust and reliable connectivity in remote or challenging-to-reach areas continues driving adoption of NTN technologies.

Rising investment in direct-to-device satellite connectivity continues reinforcing this driver, as this capability eliminates the need for specialized user equipment and lets standard smartphones connect directly to satellites for emergency services and basic connectivity. Increasing standardization through recent 3GPP releases continues defining NTN architecture, protocols, and interoperability, and that combination of consumer-facing accessibility and technical standardization is exactly what keeps demand climbing at such a rapid, sustained pace.

Restraints: High Constellation Deployment Costs and Spectrum Coordination Complexity

The substantial capital investment required for satellite constellation design, manufacturing, and launch continues posing a genuine restraint on faster market-wide expansion, particularly for smaller operators without the capital budgets that established satellite companies and major telecom carriers can commit. That cost profile has kept large-scale constellation deployment concentrated among a comparatively small number of well-resourced operators.

Spectrum coordination complexity between satellite and terrestrial network operators continues posing a further restraint, as sharing frequency bands across different jurisdictions and technology platforms requires genuine regulatory coordination that remains an ongoing, evolving process. That complexity keeps some cross-border deployment scenarios more technically and legally complicated than pure terrestrial 5G rollout ever required.

Opportunities: Consumer Direct-to-Device Services and Emerging Market Connectivity Gaps

Rising investment in direct-to-device satellite connectivity represents a genuinely significant opportunity, as satellite emergency services become a standard smartphone feature and drive genuinely substantial numbers of potential users toward basic satellite connectivity services. Vendors positioned early in consumer-facing direct-to-device technology stand to capture meaningful share as this capability continues expanding from emergency-only use cases into everyday connectivity.

Closing connectivity gaps across emerging markets offers a second substantial opportunity, as government initiatives aimed at bridging the digital divide continue creating fresh demand for satellite-enabled rural and remote connectivity infrastructure. Vendors with proven, cost-effective NTN technology stand to capture meaningful share as developing economies increasingly view satellite connectivity as a genuinely practical way to leapfrog the terrestrial infrastructure build-out that wealthier nations required decades to complete.

Recent Developments:

-

2025: AST SpaceMobile continued expanding its constellation of BlueBird satellites, designed to enable direct broadband cellular connectivity from space to standard, unmodified smartphones for carrier partners worldwide.

-

2025: Apple continued expanding its satellite emergency messaging capability across additional iPhone models and regions, building on its original satellite SOS feature to include broader messaging and roadside assistance functionality.

-

2024: Qualcomm continued advancing its 5G NTN chipset portfolio, enabling smartphone manufacturers to integrate satellite connectivity capability directly into mainstream mobile device designs without requiring specialized hardware.

5G NTN Market key players are:

-

Space Exploration Technologies Corp. (SpaceX)

-

Nokia Corporation

-

Ericsson AB

-

Huawei Technologies Co., Ltd.

-

Thales Alenia Space

-

Lockheed Martin Corporation

-

OneWeb (Eutelsat Group)

-

Amazon.com, Inc. (Project Kuiper)

-

Viasat, Inc.

-

Intelsat S.A.

-

Telesat Corporation

-

SoftBank Group Corp.

-

Airbus Defence and Space

-

SKY Perfect JSAT Corporation

-

Gilat Satellite Networks Ltd.

-

Cobham SATCOM

-

ST Engineering iDirect

-

AST SpaceMobile, Inc.

5G NTN Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.50 Billion |

| Market Size by 2035 | USD 158.66 Billion |

| CAGR | CAGR of 34.0% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services.) • By Platform (UAS Platform, LEO Satellite, MEO Satellite, GEO Satellite.) • By Location (Urban, Rural, Remote, Isolated.) • By Application (Enhanced Mobile Broadband (EMBB), Ultra Reliable and Low Latency Communications (URLLC), Massive Machine-Type Communications (MMTC).) • By End-Use (Maritime, Aerospace & Defense, Government, Mining, Others.) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Space Exploration Technologies Corp. (SpaceX), Qualcomm Technologies, Inc., Nokia Corporation, Ericsson AB, Huawei Technologies Co., Ltd., Thales Alenia Space, Lockheed Martin Corporation, OneWeb (Eutelsat Group), Amazon.com, Inc. (Project Kuiper), Viasat, Inc., Intelsat S.A., Telesat Corporation, SoftBank Group Corp., Airbus Defence and Space, Boeing Company, SKY Perfect JSAT Corporation, Gilat Satellite Networks Ltd., Cobham SATCOM, ST Engineering iDirect, AST SpaceMobile, Inc. |

Frequently Asked Questions

The 5G NTN Market is expected to grow at a CAGR of approximately 34.0% from 2026 to 2035, based on triangulated secondary research estimates.

The 5G NTN Market was valued at approximately USD 8.50 Billion in 2025, based on triangulation across multiple independent research sources.

The major growth factor is rising demand for ubiquitous connectivity, expansion of direct-to-device satellite communications, and increasing integration of satellite and terrestrial 5G infrastructure.

The Hardware segment dominated the 5G NTN Market by component, representing the largest share of revenue in 2025.

North America dominated the 5G NTN Market in 2025, holding an estimated 35.0% share of total global market revenue.

Get in Touch