Agentive AI in Healthcare Market Report Scope & Overview:

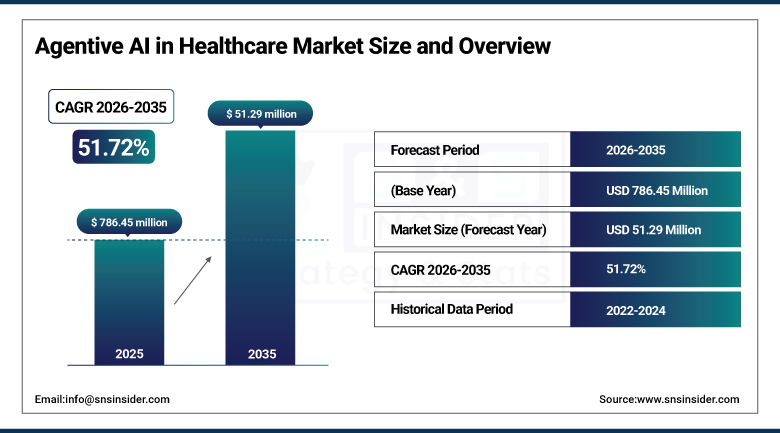

The Agentive AI in Healthcare Market was estimated at USD 786.45 million in 2025 and is expected to reach USD 51.29 billion by 2035 and grow at a CAGR of 51.72% over the forecast period of 2026-2035.

The Agentive AI in Healthcare Market encompasses the rapidly expanding ecosystem of autonomous and semi-autonomous artificial intelligence systems deployed across clinical, administrative, and operational healthcare workflows to perceive environmental inputs, reason over complex multi-variable datasets, plan and execute multi-step action sequences, and adapt behavior based on feedback without requiring continuous human guidance for each decision or task. Agentive AI systems distinguished from narrower AI applications by their capacity for goal-directed autonomous action across extended task sequences involving real-world consequences are being deployed across an extraordinarily broad spectrum of healthcare contexts, including clinical decision support systems that autonomously monitor patient data streams and proactively escalate anomalous findings to clinicians, administrative workflow automation platforms that independently execute multi-step revenue cycle management, prior authorization, and claims processing sequences.

The structural drivers of the Agentive AI in Healthcare Market extraordinary growth trajectory reflect a convergence of healthcare system urgency and technological maturation that is creating conditions for exceptionally rapid adoption. The global healthcare workforce crisis characterized by projected shortages of 18 million healthcare workers by 2030 according to the World Health Organization, physician burnout rates exceeding 60% in major studies, and administrative burden consuming over 34% of physician time in U.S. hospitals according to the American Medical Association creates intense operational pressure on healthcare organizations to deploy intelligent automation that can perform clinical and administrative tasks with reduced human labor inputs.

Market Size and Forecast

-

Market Size in 2025: USD 786.45 Million

- Market Size by 2035: USD 51.29 Billion

- CAGR: 51.72% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026–2035

- Historical Data: 2022–2024

To Get more information on Agentive AI in Healthcare Market - Request Free Sample Report

Agentive AI in Healthcare Market Trends

- Rapid deployment of multi-agent AI orchestration frameworks in hospital systems that coordinate networks of specialized clinical AI agents monitoring agents, diagnostic reasoning agents, care coordination agents, and documentation automation agents into integrated clinical intelligence platforms capable of managing end-to-end patient care workflows with minimal human intervention, representing a fundamental architectural evolution from siloed point AI solutions toward comprehensive agentic care management systems.

- Accelerating integration of agentive AI into revenue cycle management operations, where autonomous agents independently execute prior authorization submissions, claims scrubbing, denial management, and underpayment recovery workflows that collectively represent hundreds of billions of dollars in administrative cost and revenue leakage for health systems annually, creating some of the clearest and most immediately quantifiable return on investment cases in healthcare AI deployment.

- Growing deployment of AI-powered remote patient monitoring agents that continuously analyze multi-modal patient data streams from wearable devices, home monitoring equipment, and electronic health records to proactively identify clinical deterioration patterns, predict adverse events, and trigger care team interventions before emergency escalation is required, enabling health systems to manage growing populations of high-risk patients at home with AI-augmented clinical oversight.

- Extraordinary commercial momentum in agentic AI for drug discovery and development, where AI agents autonomously design molecular compound libraries, predict ADMET properties, analyze high-throughput screening data, generate research hypotheses, and execute multi-step experimental planning workflows, compressing drug development timelines that historically required five to seven years to complete initial target-to-lead stages into twelve to eighteen months through AI-accelerated experimental cycle management.

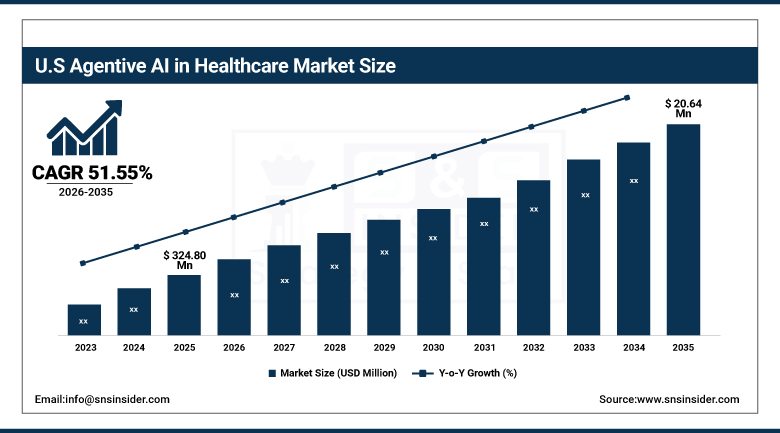

U.S. Agentive AI in Healthcare Market was valued at USD 324.80 million in 2025 and is expected to reach USD 20.64 billion by 2035, growing at a CAGR of 51.55%.

The United States commands global leadership in the Agentive AI in Healthcare Market, driven by the country uniquely favorable combination of advanced digital health infrastructure, aggressive venture capital investment ecosystem, supportive regulatory environment for healthcare AI innovation, and healthcare system economic pressures that create compelling return on investment cases for agentive AI adoption. Over 170 U.S. hospital systems had deployed agent-based AI solutions for clinical decision support and administrative automation as of 2025, demonstrating the transition from pilot programs to production-scale institutional deployment that characterizes genuine market maturation.

The U.S. market benefits from the concentrated presence of technology industry leaders including Microsoft, NVIDIA, Google Health, Amazon Web Services Health AI, Oracle Health, and IBM Watson Health that are deploying substantial R&D investment in healthcare-specific agentive AI platform development. Regulatory advancement from the FDA Digital Health Software Precertification program and the agency 2024 guidance on AI and machine learning-based software as medical devices is providing compliance clarity that is enabling health systems to make confident procurement decisions for clinical AI applications.

Agentive AI in Healthcare Market Segment Analysis

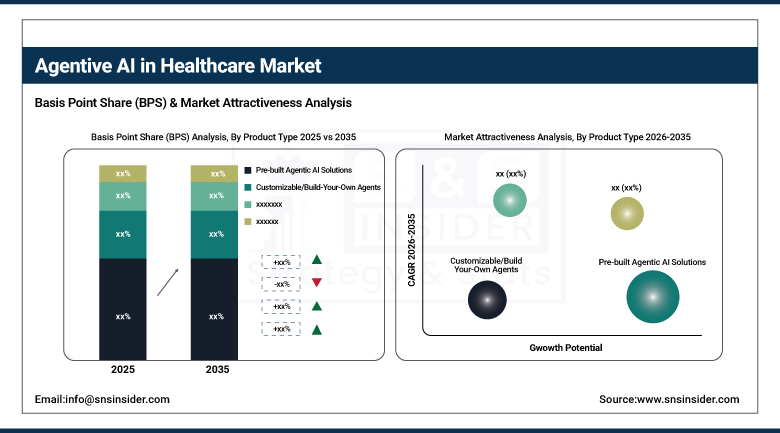

- By Product Type, Pre-built Agentic AI Solutions dominated with approximately 52.5% share in 2025; Customizable/Build-Your-Own Agents are the fastest-growing product type at a CAGR of approximately 54.3%.

- By Agent Type, Single-Agent Systems dominated with approximately 47.2% share in 2025; Multi-Agent Systems are the fastest-growing agent type driven by complex healthcare workflow orchestration requirements.

- By Technology, Machine Learning held the largest technology share of approximately 38.1% in 2025; Smart Virtual Assistants are the fastest-growing technology segment driven by patient-facing and provider support applications.

- By Application, Administrative Workflow Automation led the market in 2025; Clinical Decision Support is the fastest-growing application segment driven by diagnostic AI performance breakthroughs.

- By End User, Hospitals & Health Systems dominated with the largest revenue share in 2025; Pharmaceutical & Life Sciences is growing at exceptional rates driven by AI-accelerated drug discovery investment.

By Product Type: Pre-built Solutions dominate, Customizable fastest-growing

Pre-built Agentic AI Solutions dominated the market with approximately 52.5% share in 2025, reflecting healthcare organizations preference for immediately deployable AI platforms with validated clinical performance, established regulatory compliance documentation, and pre-built integrations with major EHR systems including Epic, Oracle Cerner, and MEDITECH that dramatically reduce the implementation timeline and technical resource requirements for production deployment. Pre-built solutions including Notable administrative AI platform, Corti clinical decision support agent, and Aidoc radiology AI orchestration system offer healthcare organizations functional agentive AI capabilities accessible through standardized subscription agreements without requiring internal AI engineering talent to develop or maintain custom AI systems, dramatically reducing the barrier to adoption for health systems with limited digital innovation capacity.

Customizable and Build-Your-Own Agent platforms are expected to grow at the fastest CAGR of approximately 54.3% during the forecast period, driven by large integrated health systems, academic medical centers, and major pharmaceutical companies that have sufficient internal AI engineering capacity and strategic AI differentiation objectives to justify developing proprietary healthcare AI agent platforms tailored to their specific clinical protocols, data models, patient population characteristics, and competitive positioning requirements.

By Agent Type: Single-Agent Systems dominate, Multi-Agent fastest-growing

Single-Agent Systems dominated the market with approximately 47.2% share in 2025, reflecting the natural starting point for most healthcare organizations’ AI deployment journeys—deploying specialized, task-focused AI agents for well-defined, high-value use cases including appointment scheduling automation, medical billing code suggestion, radiology image prioritization, and clinical note generation where the bounded task scope makes single-agent system design technically tractable and the ROI case straightforward to validate. Single-agent deployments offer healthcare organizations lower implementation complexity, more predictable behavior, and clearer accountability for AI actions compared to multi-agent systems, making them the preferred initial deployment approach for health systems establishing their AI operational capabilities, governance frameworks, and staff training programs before advancing to more complex multi-agent architectures.

Multi-Agent Systems are the fastest-growing agent type during the forecast period, driven by the expanding ambition of healthcare AI deployment from automating discrete tasks to orchestrating comprehensive clinical and administrative workflows that require coordination across multiple specialized AI capabilities, data sources, and organizational systems. Multi-agent healthcare platforms enable division of cognitive labor that mirrors the collaborative workflows of clinical teams with specialized agents monitoring data streams, reasoning over evidence bases, communicating care recommendations, coordinating logistics, and generating documentation creating AI-managed care workflows that can match or exceed human team performance on specific well-defined care management tasks while operating continuously without fatigue or attention lapses that characterize human performance in monitoring-intensive clinical roles.

By Application: Administrative Workflow Automation leads, Clinical Decision Support fastest-growing

Administrative Workflow Automation led the Agentive AI in Healthcare Market by application in 2025, reflecting both the maturity of administrative AI solutions relative to clinical AI and the extraordinary scale of the administrative cost burden that creates compelling, immediately quantifiable ROI cases for health system AI investment. U.S. healthcare administrative costs are estimated at USD 950 billion to USD 1.8 trillion annually representing 34% of total healthcare expenditure with prior authorization processing, claims submission and denial management, medical coding and documentation, and patient scheduling collectively consuming healthcare system resources that agentive AI can materially reduce. Leading administrative AI platforms including Thoughtful Automation, Waystar, and R1 RCM AI solutions are demonstrating 40-70% reductions in administrative labor requirements for targeted revenue cycle workflows, generating compelling health economic cases for adoption that have driven accelerating health system procurement.

Clinical Decision Support is the fastest-growing application segment during the forecast period, driven by breakthrough demonstrations of clinical AI performance including Microsoft MAI-DxO multi-agent diagnostic system achieving 85.5% diagnostic accuracy on complex cases versus 20% human physician accuracy, and Google Med-PaLM 2 demonstrating expert-level performance on U.S. Medical Licensing Examination questions, that are transforming clinical leadership perception of AI from cautious skepticism to active implementation planning.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~87% |

|

Europe |

Germany |

~26% |

|

Asia Pacific |

China |

~41% |

|

Middle East & Africa |

UAE |

~32% |

|

Latin America |

Brazil |

~43% |

North America Agentive AI in Healthcare Market Insights

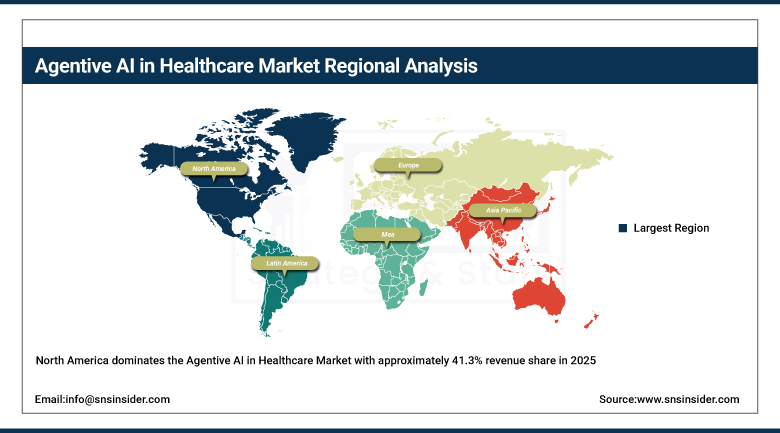

North America dominates the Agentive AI in Healthcare Market with approximately 41.3% revenue share in 2025, anchored by the United States unparalleled combination of advanced digital health infrastructure including the world highest EHR penetration rates, concentrated technology industry R&D investment in healthcare AI from Microsoft, NVIDIA, Google, and Amazon, a mature and well-capitalized venture ecosystem that has funded over USD 4 billion in healthcare AI companies over 2023–2025, and healthcare system economic pressures that create the strongest global commercial incentives for AI-driven administrative and clinical efficiency improvement. The U.S. regulatory environment, while evolving, provides clearer compliance pathways for healthcare AI than most markets through FDA digital health guidance frameworks and the HIPAA-compliant AI deployment certification standards that major healthcare AI vendors have developed. Canada is a rapidly growing secondary market, particularly in public health system AI pilots and telemedicine agent-based care applications, supported by the federal government Pan-Canadian Health Data Strategy and provincial health authority investments in AI-enabled care delivery transformation.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Agentive AI in Healthcare Market Insights

Europe accounted for approximately 25.7% of global Agentive AI in Healthcare Market revenue in 2025, with Germany, the United Kingdom, France, and the Netherlands as the primary national markets. Germany leads European market development through large-scale hospital digitization programs funded under the Hospital Future Act (KHZG), which allocated EUR 4.3 billion for digital health infrastructure including AI-based clinical decision support systems, and the DiGA digital health application program that provides a regulatory pathway for AI-powered digital therapeutics and clinical support tools that is among the most progressive clinical AI approval frameworks globally. The United Kingdom NHS AI Lab and NHSX digital health innovation programs are generating large-scale clinical AI deployment initiatives, including the NHS England national rollout of AI-assisted radiology triage tools and clinical documentation automation.

Asia Pacific Agentive AI in Healthcare Market Insights

Asia Pacific is the fastest-growing regional Agentive AI in Healthcare Market, expected to grow at approximately 56.4% CAGR during the forecast period, driven by the extraordinary scale of AI investment in China healthcare sector under national AI development strategies, India rapidly expanding digital health ecosystem under the National Digital Health Mission, and the advanced healthcare technology adoption environments of Japan, South Korea, and Singapore. China represents the largest national market within Asia Pacific, with major healthcare AI companies including Ping An Good Doctor, Alibaba Health, and WeDoctor deploying agentic AI across virtual primary care, chronic disease management, and hospital operational efficiency applications at scales that are generating the largest single-country volumes of healthcare AI clinical data outside the United States.

Latin America & Middle East and Africa Agentive AI in Healthcare Market Insights

Latin America and the Middle East & Africa represent rapidly developing Agentive AI in Healthcare Markets where healthcare system modernization investment, growing awareness of clinical AI capabilities, and acute healthcare workforce shortages are creating adoption incentives. Brazil leads Latin American market development as the region largest and most digitally advanced healthcare economy, with major hospital networks, the largest private health insurance market in the developing world, and a growing domestic health AI startup ecosystem. The Middle East is among the most proactive emerging market regions for healthcare AI adoption, led by the UAE national AI strategy that positions the country as a regional AI leader and Saudi Arabia Vision 2030 healthcare transformation program that includes substantial investment in digital health and clinical AI infrastructure across the Kingdom hospital network expansion.

Growth Drivers: Healthcare workforce crisis, AI capability maturation, administrative cost burden, and digital health infrastructure expansion creating structural demand for agentive AI deployment.

The primary structural growth drivers for the Agentive AI in Healthcare Market are the convergence of healthcare system operational necessity and AI technology maturation that has simultaneously created urgent demand for intelligent automation and delivered AI platforms capable of meeting that demand at clinical and administrative performance levels that justify deployment confidence. The global healthcare workforce shortage projected to reach 18 million by 2030 combined with physician burnout rates exceeding 60% and administrative burden consuming over one-third of clinical time creates existential operational pressure on health systems that cannot be resolved through conventional workforce expansion alone, making AI-powered clinical and administrative automation a strategic necessity rather than an elective technology investment.

Restraints: Data privacy and AI accountability concerns, integration complexity with legacy systems, AI bias risks, and regulatory uncertainty constraining deployment velocity.

The Agentive AI in Healthcare Market faces meaningful constraints on adoption velocity and penetration depth despite its extraordinary growth trajectory. A 2024 U.S. Government Accountability Office survey found that 60% of healthcare providers expressed hesitation to rely on AI agents for clinical decisions due to interpretability and auditability concerns reflecting a fundamental challenge in autonomous AI systems where the inability to explain AI reasoning in clinically transparent terms creates medicolegal risk that makes clinicians reluctant to act on AI recommendations without independent verification that partially defeats the efficiency purpose of autonomous deployment. HIPAA and GDPR compliance frameworks were not designed with agentive AI multi-step autonomous data access patterns in mind, creating compliance uncertainty around AI agents that independently access and process patient data across multiple system interactions in ways that differ structurally from the human user data access patterns these frameworks originally contemplated.

Opportunities: Precision medicine AI agents, autonomous clinical trial management, global health equity applications, and AI-native care delivery model creation driving long-term market expansion.

The Agentive AI in Healthcare Market presents transformative long-term growth opportunities that extend well beyond efficiency optimization of existing healthcare workflows into the creation of fundamentally new models of care delivery that would be impossible without AI agent capabilities. The development of truly personalized medicine AI agents that integrate genomic, proteomic, metabolomic, and longitudinal clinical data to generate individualized treatment optimization recommendations for complex conditions including cancer, rare diseases, and treatment-resistant mental health disorders represents a therapeutic category that current non-AI clinical practice cannot address at the precision levels these technologies enable, creating a large new market for clinical AI that generates demonstrable health outcome improvements rather than purely administrative efficiency gains.

Recent Developments:

- June 2025: Microsoft introduced MAI-DxO, a multi-agent AI diagnostic system that achieved 85.5% accuracy on complex clinical diagnostic cases using New England Journal of Medicine case study datasets more than four times the 20% accuracy rate of human physicians on the same cases while reducing diagnostic process costs by approximately 20%, representing one of the most significant clinical AI performance demonstrations to date and accelerating health system investment in clinical diagnostic AI globally.

- June 2025: IQVIA launched advanced agentic AI solutions built on NVIDIA AI technology infrastructure to automate clinical trial workflows including automated literature review, AI-assisted patient recruitment, remote site monitoring, and multi-source data review, demonstrating the life sciences sector accelerating adoption of multi-agent orchestration frameworks to compress drug development timelines and reduce trial operational costs.

Agentive AI in Healthcare Market Key Players

- NVIDIA Corporation

- Microsoft Corporation (MAI-DxO, Azure Health AI)

- Oracle Health (Cerner)

- Thoughtful Automation

- Hippocratic AI

- Cognigy

- Amelia (IPsoft)

- Beam AI

- Momentum AI

- Notable Health

- Google Health (Med-PaLM 2)

- IBM Watson Health

- AWS Health AI (Amazon)

- Infermedica

- Tempus AI

- PathAI

- Viz.ai

- Aidoc

- Corti

- Autonomize AI

Agentive AI in Healthcare Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 786.45 Million |

| Market Size by 2035 | USD 51.29 Billion |

| CAGR | CAGR of 51.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Pre-built Agentic AI Solutions, Customizable/Build-Your-Own Agents) •By Agent Type (Single-Agent Systems, Multi-Agent Systems, Hybrid Agent Systems) •By Technology (Machine Learning, Smart Virtual Assistants, Natural Language Processing, Computer Vision, Others) •By Application (Clinical Decision Support, Administrative Workflow Automation, Revenue Cycle Management, Remote Patient Monitoring, Drug Discovery & Development, Others) •By End User (Hospitals & Health Systems, Payers & Insurance Companies, Pharmaceutical & Life Sciences, Telehealth Providers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA Corporation, Microsoft Corporation (MAI-DxO, Azure Health AI), Oracle Health (Cerner), Thoughtful Automation, Hippocratic AI, Cognigy, Amelia (IPsoft), Beam AI, Momentum AI, Notable Health, Google Health (Med-PaLM 2), IBM Watson Health, AWS Health AI (Amazon), Infermedica, Tempus AI, PathAI, Viz.ai, Aidoc, Corti, Autonomize AI |

Frequently Asked Questions

Ans: Clinical Decision Support is the fastest-growing application segment, driven by breakthrough clinical AI performance demonstrations including Microsoft MAI-DxO system achieving 85.5% diagnostic accuracy on complex cases exceeding human physician performance by over four times that are fundamentally transforming health system confidence in AI-assisted clinical reasoning.

Ans: Asia Pacific is expected to grow at the fastest CAGR of approximately 56.4% during 2026–2035, driven by extraordinary AI investment in China healthcare sector, India rapidly expanding digital health ecosystem under the National Digital Health Mission, and advanced healthcare technology environments in Japan, South Korea, and Singapore.

Ans: Pre-built Agentic AI Solutions dominated with approximately 52.5% market share in 2025, driven by healthcare organizations preference for immediately deployable platforms with validated clinical performance, pre-built EHR integrations, and established regulatory compliance documentation that reduces implementation complexity and accelerates time-to-value.

Ans: The Agentive AI in Healthcare Market was valued at USD 786.45 million in 2025 and is expected to reach USD 51.29 billion by 2035.

Ans: The Agentive AI in Healthcare Market is expected to grow at an exceptional CAGR of 51.72% from 2026 to 2035, reflecting the compounding effect of healthcare AI capability advancement, accelerating health system adoption, and expanding clinical and administrative AI deployment scope.

Get in Touch