Agriculture 4.0 Market Report Scope and Overview:

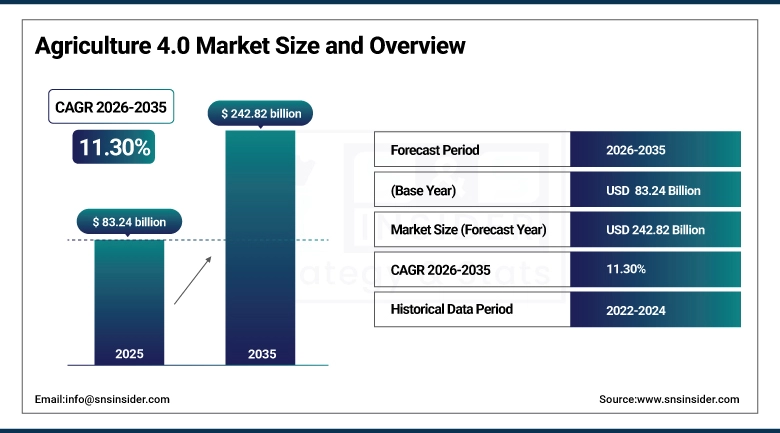

The Agriculture 4.0 Market was valued at USD 83.24 billion in 2025 and is projected to reach USD 242.82 billion by 2035, growing at a CAGR of 11.30% during the 2026–2035 forecast period. The report covers technology adoption rates across farming operations, investment and funding activity in agricultural innovation, and the measurable environmental outcomes of modern precision farming practices.

It is a convergence of several IoT-connected field sensors feeding data into AI-driven crop models, autonomous machinery handling labor-intensive tasks that have historically constrained farm productivity, and cloud platforms tying it all together into management systems that give operators a level of visibility over their land that was simply not possible a decade ago. For most of agricultural history, decisions about when to plant, irrigate, fertilise, or harvest were made on experience and observation.

Market Size and Forecast:

-

Market Size in 2025: USD 83.24 Billion

-

Market Size by 2035: USD 242.82 Billion

-

CAGR: 11.30% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Agriculture 4.0 Market - Request Free Sample Report

Agriculture 4.0 Market Trends:

-

IoT sensors, AI analytics, robotics, and farm automation have moved from experimental deployments to production-scale operations across commercial farming, enabling real-time crop monitoring, predictive disease modeling, and data-driven resource allocation that reduce both input costs and yield variability.

- Mechanized and autonomous equipment is reducing the labor dependency that has been a structural vulnerability in agriculture for years, particularly for tasks like planting, harvesting, and pest management where labor availability is seasonal and increasingly difficult to predict.

- Adoption costs for sophisticated precision agriculture systems remain a genuine barrier for smaller farming operations, and the gap between large commercial farms that can absorb the capital outlay and smaller producers who cannot is widening rather than narrowing in most markets.

- Data security, rural connectivity gaps, and the difficulty of integrating new technology with farm infrastructure that was not designed for digital systems are all slowing adoption in ways that technology improvement alone will not fully resolve without changes to connectivity investment and regulatory frameworks.

- Government incentive programs, cross-sector partnerships between agricultural producers and technology firms, and the growing commercial availability of Big Data tools are collectively creating conditions in which the business case for Agriculture 4.0 adoption is more accessible to a broader range of operators than it was three years ago.

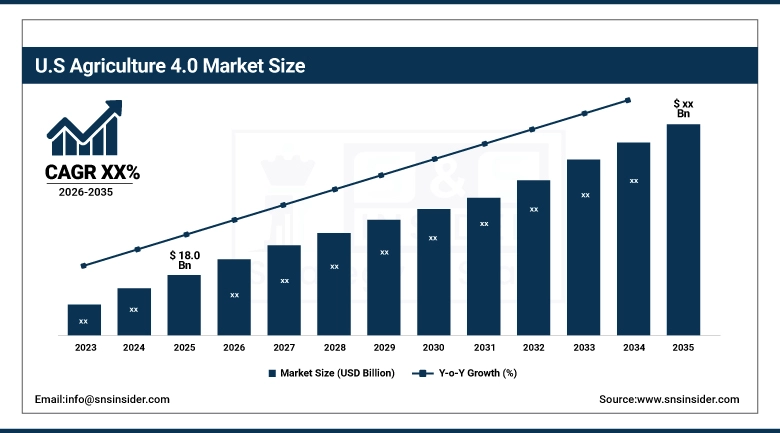

The U.S. Agriculture 4.0 market was estimated at approximately USD 18 Billion in 2025. Precision farming technologies, AI-based analytics, IoT-enabled field equipment, and autonomous machinery have all reached levels of commercial maturity in the United States that are well ahead of most comparable economies. The concentration of large commercial farming operations gives the U.S. market a procurement scale that makes technology investment viable at per-farm economics that do not work for smallholder agriculture, and the digital infrastructure across rural America, while still uneven, has improved enough to support connected systems across a significant share of the country's agricultural land.

Agriculture 4.0 Market Growth Drivers:

-

IoT, AI, Robotics, and Automation Are Delivering Measurable Operational Improvements Across Farming Operations, Making the Technology Investment Case Increasingly Difficult to Ignore

The productivity argument for Agriculture 4.0 technologies has been made for years, but it has taken time for the commercial evidence to accumulate to a point where it drives widespread adoption rather than early-adopter experimentation. That evidence is now available across a range of crop types, geographies, and farming scales, and it is consistent: precision agriculture systems that use real-time sensor data to guide irrigation, fertilization, and pest management decisions reduce input costs, improve yield consistency, and lower the environmental impact of farming operations relative to conventional approaches applied at field scale without spatial differentiation. Mechanized and robotic equipment handles tasks that human labor performs slowly and inconsistently seeding at precise spacing and depth, harvesting at optimal timing, monitoring for early signs of disease across large areas with a reliability that holds up in conditions where human labor availability does not. AI-driven predictive systems take sensor data and historical records and produce forward-looking assessments of crop health trajectories and climate-related risk that give farm managers time to intervene before problems become costly.

Agriculture 4.0 Market Restraints:

-

High Adoption Costs, Skilled Labor Shortages, Data Security Risks, and Uneven Rural Connectivity Are Collectively Slowing the Pace of Agriculture 4.0 Deployment Across Smaller Farming Operations

The barriers to Agriculture 4.0 adoption are not primarily technical. The technology works. The problem is that the cost structure of deploying it does not work for a large proportion of the world's farming operations. A comprehensive precision agriculture setup field sensor, connected equipment, software platforms, data infrastructure requires upfront capital that large commercial farms can finance against projected efficiency gains but that smaller and mid-scale operators often simply do not have access to. That capital barrier is reinforced by a skills problem: operating and maintaining AI-integrated farm management systems requires technical capability that most agricultural workforces do not currently carry, and building it takes time that technology adoption timelines do not always accommodate. Data security is an increasingly serious concern as farming operations push more operational data into cloud systems and data-sharing arrangements with input suppliers and platform providers the exposure is real, and regulatory frameworks in most agricultural markets have not kept pace with the rate at which farm data is being collected and used commercially. Rural connectivity gaps compound all of this.

Agriculture 4.0 Market Opportunities:

-

Big Data Analytics, Sustainability Mandates, Government Support Programs, and Cross-Sector Technology Partnerships Are Opening Material Growth Pathways for Agriculture 4.0 Across Established and Emerging Markets

The growing commercial availability of Big Data and analytics tools is changing what is possible at the farm management level. Farmers who previously made resource allocation decisions based on generalized field averages can now work from spatial data that identifies variation within fields and guides input application at the resolution of individual rows or zones, reducing waste and improving outcomes simultaneously. That capability is increasingly accessible at price points that mid-scale operators can consider rather than only the largest commercial farms. Sustainability requirements from food retailers, export markets, and institutional buyers are generating demand pull for technology that can document and reduce the environmental footprint of production precision agriculture systems that demonstrably reduce fertilizer runoff, irrigation overuse, and pesticide application are finding commercial traction through their sustainability credentials as much as their productivity arguments. Government programs in developing economies are actively subsidizing technology access for smallholder farmers, recognizing that food security goals cannot be met without productivity improvements at that scale.

Agriculture 4.0 Market Segment Analysis:

By Component

Hardware led the agriculture 4.0 market with approximately 56% revenue share in 2025. The dominance of hardware reflects where the capital in precision agriculture actually goes: drones, sensors, GPS-guided machinery, automated irrigation systems, and the robotics platforms that carry out field operations are expensive to manufacture, specify, and install, and they represent the tangible capability that the rest of the agriculture 4.0 stack depends on. Without the hardware layer, the data does not get collected and the automation does not execute. The services segment is expected to grow at the fastest CAGR of approximately 13.37% between 2026 and 2035. As more farming operations bring sophisticated hardware and software systems online, the demand for the services that make those systems work integration, training, ongoing analytics support, system maintenance, and the consulting work that helps operators understand what their data is actually telling them grows proportionally.

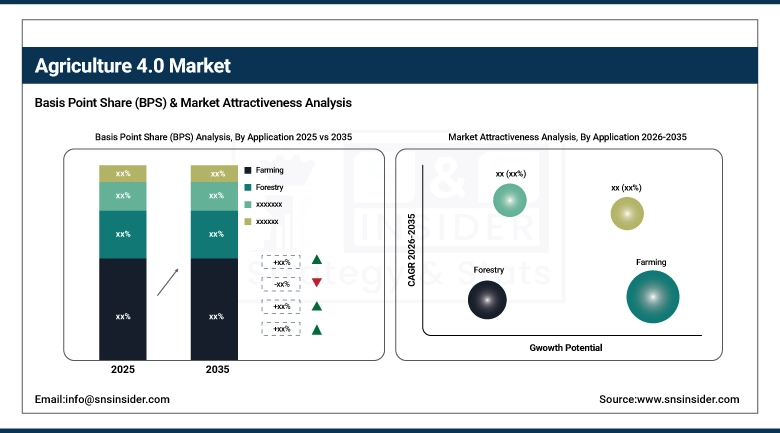

By Application

Farming led the agriculture 4.0 market with approximately 25% revenue share in 2025. The concentration of investment in farming applications reflects the scale of the productivity problem that precision agriculture is addressing crop production across large commercial acreages is where the return on technology investment is most clearly quantifiable, and it is where the commercial and political pressure to improve output efficiency is most acute. Smart Greenhouse is expected to grow at the fastest CAGR of approximately 13.77% from 2026 to 2035. Controlled environment agriculture addresses the constraints that outdoor farming cannot: weather unpredictability, seasonal growing limitations, and the pest and disease exposure that comes with producing in open-air conditions.

By End-Use

Agro-forestry led the agriculture 4.0 market with approximately 40% revenue share in 2025. The category's scale reflects the breadth of land management practices it covers and the growing policy emphasis on integrated farming systems that incorporate trees to improve soil health, carbon sequestration, and biodiversity outcomes alongside crop and livestock production. Remote sensing and precision agriculture tools have made managing agro-forestry systems at commercial scale significantly more practical than it was under conventional methods. The fishing segment is expected to grow at the fastest CAGR of approximately 13.00% during 2026 to 2035. Global seafood demand is rising while wild-catch fisheries face increasing pressure, which is driving investment in aquaculture technology that can produce more output with better control over resource use.

Agriculture 4.0 Market Regional Analysis:

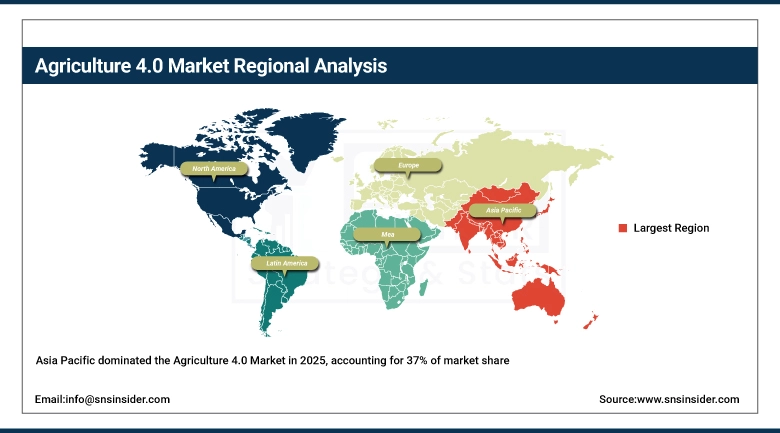

Asia Pacific Agriculture 4.0 Market Insights

Asia Pacific dominated the agriculture 4.0 market with approximately 37% revenue share in 2025. The region's leadership reflects both scale and diversity: China and India alone account for a substantial share of global agricultural land and labor, and both countries are running active government programs to bring precision agriculture and smart farming technology into their production systems at a pace that is difficult for any other region to match on aggregate volume. The food security imperative is not abstract in Asia Pacific it is a policy priority backed by real investment. Affordable technology availability, particularly in sensor hardware and mobile connectivity, has lowered the access threshold for smallholder farmers in a way that the cost structure of Agriculture 4.0 in developed markets has not.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Agriculture 4.0 Market Insights

Europe is expected to grow at the fastest CAGR of approximately 13.02% from 2026 to 2035. The European growth story is less about catching up and more about going deeper. European agriculture has a sophisticated infrastructure and a regulatory environment that has been pushing toward precision, sustainability, and traceability for longer than most other regions. What is accelerating now is the combination of EU sustainability mandates that are turning technology adoption from a competitive advantage into a compliance requirement, consumer demand for documented food origin and production practices that feeds directly through retail supply chains to farms, and a well-developed research and innovation ecosystem that is producing the next generation of Agriculture 4.0 applications faster than many other geographies.

North America Agriculture 4.0 Market Insights

North America holds a significant share of the agriculture 4.0 market, built on a foundation of large commercial farming operations that can absorb technology investment at scale, strong agricultural research infrastructure at both university and corporate levels, and a government policy environment in the U.S. and Canada that has supported precision agriculture through both funding programs and favorable regulatory treatment of autonomous and AI-driven farming systems. The challenge in North America is extending adoption beyond the large-scale commercial operations where the economics are clearest into the mid-scale farming sector, where the investment case is harder to make without financing support.

Latin America and Middle East & Africa Agriculture 4.0 Market Insights

Latin America is building Agriculture 4.0 adoption on the foundation of its large-scale crop production base, particularly in Brazil and Argentina, where the farm sizes and export-oriented production economics create a natural case for precision agriculture investment. IoT-based monitoring and precision input management are finding commercial traction in soy, corn, and sugarcane production, and government programs are providing framework support that is helping mid-scale producers access technology that would otherwise be out of reach. The Middle East and Africa are approaching Agriculture 4.0 from a different angle: the imperative is resource efficiency more than scale productivity. Water scarcity is the defining constraint for agriculture across much of the Middle East, and smart irrigation systems, soil moisture monitoring, and AI-driven water management tools are attracting investment precisely because the alternative continuing to farm with conventional water use patterns is not sustainable.

Competitive Landscape for Agriculture 4.0 Market:

AGCO Corporation is headquartered in Duluth, Georgia, and has built its position as one of the world's leading agricultural equipment manufacturers through a portfolio of brands that includes Fendt, Massey Ferguson, and Valtra. Founded in 1990, the company generated USD 14.4 Billion in revenue in 2023 with approximately 27,900 employees. AGCO's strategic direction in Agriculture 4.0 runs through its Fendt brand in particular, which has been at the commercial frontier of autonomous tractor development and precision agriculture integration.

In February 2025, AGCO Corporation and SDF Group entered a strategic partnership to strengthen AGCO's position in the low-to-mid horsepower tractor segment. Under the agreement, production of proprietary tractors up to 85 horsepower was set to begin in mid-2025, expanding AGCO's product reach into a market tier where demand from smallholder and mid-scale farming operations is substantial in both emerging and established markets.

Bayer AG operates in the agriculture 4.0 space primarily through its Crop Science division, which covers seeds, crop protection products, and digital farming tools under the Climate FieldView platform and related offerings. The company's position in agriculture combines deep biological and chemical expertise with a growing data and analytics capability built through acquisition and partnership.

In June 2024, Bayer Vietnam expanded its Forward Farming project in the Mekong Delta, a program focused on sustainable rice production that works directly with farming communities to introduce practices that reduce input use and environmental impact. The expansion was conducted in partnership with the National Agricultural Extension Center and reflects Bayer's approach of embedding technology adoption within broader sustainability and community engagement frameworks in markets where farmer trust and local institutional relationships are essential to commercial progress.

Agriculture 4.0 Market Key Players:

-

AGCO Corporation (Fendt 1000 Vario Tractor, Massey Ferguson MF 6700 S Tractor)

-

Bayer AG (Bayer CropScience Seeds, XtendiMax Herbicide)

-

CNH Industrial (Case IH Magnum Series Tractors, New Holland T7 Series Tractors)

-

Corteva Agriscience (Corteva Pioneer Seeds, Rynaxypyr Insecticide)

-

Cropx Inc. (CropX Soil Sensor, CropX Irrigation Management System)

-

Deere & Company (John Deere 8R Series Tractors, John Deere 2020 Planter)

-

IBM (IBM Watson Decision Platform for Agriculture, IBM Blockchain for Agriculture)

-

Kubota Corporation (Kubota M7 Series Tractors, Kubota SCL1000)

-

Saga Robotics AS (Thorvald Agricultural Robot, Thorvald Autonomous Weeding System)

-

Syngenta Crop Protection AG (Syngenta Vayego Insecticide, Syngenta Lumivia Insecticide)

-

Trimble Inc. (Trimble Ag Software, Trimble GFX-750 Display)

-

Yara International (YaraLiva Calcinit Fertilizer, YaraVita Trace Element Fertilizers)

-

AG Leader Technology (AgFiniti Cloud, InCommand 1200 Display)

-

BASF SE (BASF Fungicide, BASF Herbicide)

-

Monsanto, now part of Bayer (Roundup Herbicide, Dekalb Seeds)

-

Raven Industries (Raven Viper 4+, Raven Omnistar GPS System)

-

Valmont Industries (Valmont Irrigation Systems, Valley Center Pivot)

-

Zymergen (Bio-based Crop Protection, Microbial Growth Stimulators)

-

Topcon Positioning Systems (Topcon X20 Field Computer, Topcon GNSS Receiver)

-

Lemken (Lemken Solitair Seed Drill, Lemken Rubin Disc Harrow)

-

Dole Food Company (Dole Organic Bananas, Dole Fresh Vegetables)

-

PrecisionHawk (PrecisionHawk Drone, PrecisionHawk Data Analytics)

|

Report Attributes |

Details |

|---|---|

| Market Size in 2025 | USD 83.24 Billion |

| Market Size by 2035 | USD 242.82 Billion |

| CAGR | CAGR of 11.30% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Component (Hardware, Software, Services) |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

|

Company Profiles |

AGCO Corporation, Bayer AG, CNH Industrial, Corteva Agriscience, CropX Inc., Deere & Company, IBM, Kubota Corporation, Saga Robotics AS, Syngenta Crop Protection AG, Trimble Inc., Yara International, AG Leader Technology, BASF SE, Monsanto (now part of Bayer), Raven Industries, Valmont Industries, Zymergen, Topcon Positioning Systems, Lemken, Dole Food Company, PrecisionHawk. |

Frequently Asked Questions

ANS: Europe is expected to grow at the fastest CAGR of about 13.02% from 2026-2035.

ANS: The hardware segment dominated the Agriculture 4.0 Market with a revenue share of about 56% in 2025.

ANS: The Smart Greenhouse segment is expected to grow at the fastest CAGR of about 13.77% from 2026-2035.

ANS: The Agriculture 4.0 Market Size was valued at USD 83.24 billion in 2025 and is expected to reach USD 242.82 billion by 2032, growing at a CAGR of 11.30% from 2026-2035.

ANS: The CAGR from 2026-2035 for the Agriculture 4.0 Market is 11.30%.

Get in Touch