Agriculture Analytics Market Report Scope and Overview:

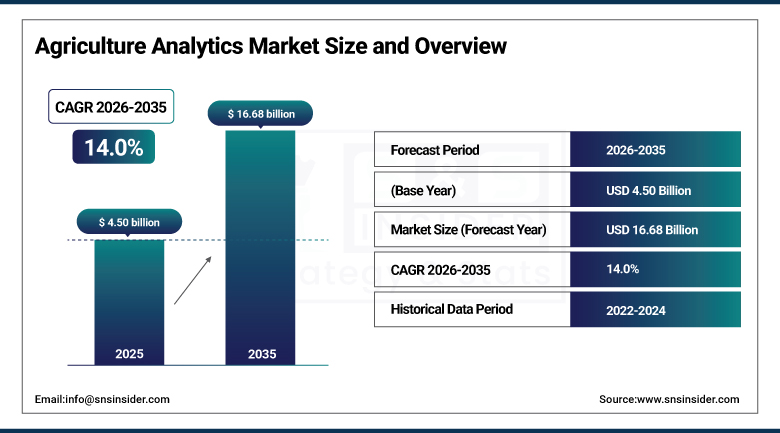

The Agriculture Analytics Market was valued at USD 4.50 Billion in 2025 and is projected to reach USD 16.68 Billion by 2035, registering a CAGR of 14.0% from 2026 to 2035.

The Agriculture Analytics Market is fuelled by the growing use of precision farming, the rising need for data-oriented agriculture, and the increasing requirement for improving the productivity of the crops. Farmers and agribusinesses are using the analytics software to track the quality of the soil, weather conditions, irrigation, and crop performance to make informed decisions. The growing use of IoT devices, drones, satellite imaging, artificial intelligence, and cloud computing technology is enabling real-time monitoring and predictive analytics of farms. Moreover, the growing worries about food security, climate change, and sustainable agriculture practices are boosting the adoption of the agriculture analytics solution. The government’s efforts in digital agriculture along with the need to increase yields at minimal costs are driving the market growth further.

John Deere Operations Center integrated its farm machinery data with EOSDA Crop Monitoring in March 2025, allowing automatic synchronization of field data and improved precision farming mapping, a development that simplifies the use of real-time data from equipment to optimize field-level decision-making across increasingly connected agricultural operations.

Market Size and Forecast

-

Market Size in 2026E: USD 5.13 Billion

-

Market Size by 2035: USD 16.68 Billion

-

CAGR: 14.0% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information Agriculture Analytics Market - Request Free Sample Report

Agriculture Analytics Market Trends

-

Many growers continue lacking the in-house skills needed to interpret complex analytics, pushing demand for managed offerings that guarantee agronomic outcomes.

-

Services continue underpinning platform stickiness by embedding agronomists and data scientists within the decision cycle, deepening customer relationships.

-

Digitization of machinery and implements alongside telemetry pipelines, combined with proven ROI from input optimization, continues driving sustained market growth.

-

Rapid mobile and internet penetration growth in emerging economies continues expanding cloud-based agriculture analytics accessibility well beyond traditionally connected regions.

-

Trimble announced enhancements to its Unity software suite in October 2025, focusing on asset lifecycle management capability that supports farm data integration and operational planning.

U.S. Agriculture Analytics Market Outlook

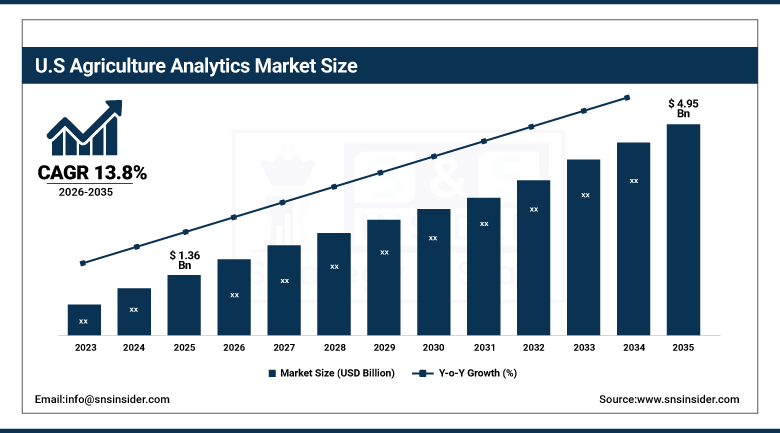

The U.S. Agriculture Analytics Market was valued at approximately USD 1.36 Billion in 2025 and is projected to reach approximately USD 4.95 Billion by 2035, registering a CAGR of approximately 13.8% from 2026 to 2035.

The domestic farmers and agribusinesses also continued adopting data-based methods for optimization of their activities. The larger operations had the ability to use analytics technology to monitor and optimize different functions within the farms, showing how larger agricultural businesses can use data-based solutions to deal with the complexities involved in farming. The strong network infrastructure and high rates of technology adoption also continued driving the cloud-based analytics segment within the country, although data standardization issues between original equipment manufacturers were a real concern despite the upward momentum of the domestic market.

Trimble continued expanding its integrated farm data platform capability throughout 2025, targeting American farmers and agribusinesses seeking connected asset lifecycle management and operational planning tools capable of consolidating equipment telemetry, field data, and agronomic decision-making into unified, cloud-based dashboards.

Agriculture Analytics Market Segment Analysis

-

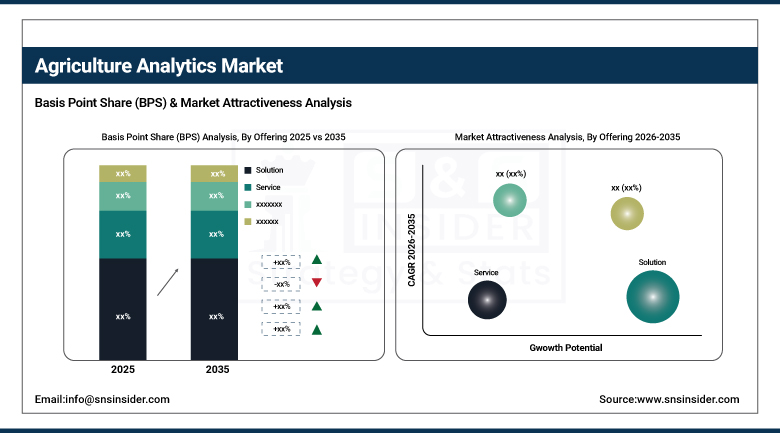

By Offering, Solution segment dominated the Agriculture Analytics Market in 2025 with 66% share; Service segment is the fastest growing segment.

-

By Agriculture Type, Precision Farming segment dominated the market in 2025 with 43% share; Vertical Farming segment is the fastest growing segment.

-

By Field Size, Large segment dominated the market in 2025 with 49% share; Medium segment is the fastest growing segment.

-

By Deployment, Cloud segment dominated the market in 2025 with 64% share; Cloud segment is the fastest growing segment.

By Offering, Solutions Dominate the Agriculture Analytics Market While Services Register the Fastest Growth Driven

The Solution segment dominated the Agriculture Analytics Market in 2025 owing to increased adoption of sophisticated analytical platforms for crop monitoring, farm management, and efficiency enhancement. The adoption of integrated solutions in order to gather, process, and analyze the agriculture data to make more informed decisions is being practiced by farmers and agriculture companies. The solutions help in improving resource management, field condition monitoring, and enabling precision farming techniques. Increased need for data-driven agriculture and efficient farming operations is further fueling the adoption of agriculture analytics solutions.

The Service segment is the fastest growing segment due to an increase in the need for consulting, implementation, integration, and maintenance services of the agriculture analytics platforms. There is a requirement for farmers to receive the necessary expertise in order to utilize the agricultural analytics platforms and also analyze the data. Increasing need for the digital farming technologies and the changing needs in the agricultural industry are driving the demand for agriculture analytics services.

By Agriculture Type, Precision Farming Dominates the Agriculture Analytics Market While Vertical Farming Emerges as the Fastest-Growing Segment

The Precision Farming segment dominated the Agriculture Analytics Market in 2025 due to wide adoption of technology-based solutions to enhance crop yield and resources efficiency. The analytical solutions in precision farming are used by agricultural producers to track their soils' condition, optimize irrigation and fertilization processes and maximize field performance. The solutions allow making right decisions based on real-time information and predictive analytics. The increasing importance of sustainable farming and maximization of agricultural products are the main drivers for adoption of analytical solutions in precision farming.

The Vertical Farming segment is the fastest growing segment due to high demand for controlled agriculture, efficient land use and round-the-year food production. The analytical solutions assist farmers to control environment, optimize resource consumption and increase crop yield in vertical farming facilities. The rising urbanization rates, insufficient land for farming, and increasing investment in advanced technologies encourage users to adopt such solutions. The importance of sustainable agricultural production is the driving factor for the segment growth.

By Field Size, Large Farms Dominate the Agriculture Analytics Market While Medium Farms Witness the Fastest Growth

The Large segment dominated the Agriculture Analytics Market in 2025 because of the availability of more finances, large areas of arable lands, and digital farming technology adoption rate. The Large farms produce a lot of data that needs advanced analytics platforms in order to enhance productivity, optimization of the resource utilization and enhance efficiency. Large farms have the capacity to adopt precision agriculture technologies. Focus on enhancing production continues to foster the adoption of analytics in agriculture.

The Medium segment is the fastest growing segment due to increased awareness about precision agriculture and availability of digital technologies at affordable costs. There is also a rising focus on improving farm productivity by optimizing farm activities such as irrigation, fertilizer application, and monitoring of crops using advanced analytics platform. The competition and need for efficient utilization of resources continues to promote adoption of analytics technology in agriculture.

By Deployment, Cloud Deployment Dominates the Agriculture Analytics Market and Records the Fastest Growth

The Cloud segment held a dominant share of the Agriculture Analytics Market in 2025 owing to its scalability, accessibility, and cost-efficient mode of deployment. An increasing preference among the agricultural enterprises is observed for cloud-enabled platforms for collecting and analysing farming data generated through various locations. Cloud platforms facilitate smooth integration with connected devices and provide real-time data monitoring along with data management. Digital transformation trends and rising usage of smart farming technology further augment the growth potential of cloud deployment in agriculture. The Cloud segment is witnessing the highest growth rate on account of rising demand for flexible and remotely accessible platforms for agriculture analytics.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.35% |

|

Europe |

Germany |

24.10% |

|

Asia Pacific |

China |

30.90% |

|

Middle East and Africa |

UAE |

26.45% |

|

Latin America |

Brazil |

34.55% |

North America Agriculture Analytics Market Insights

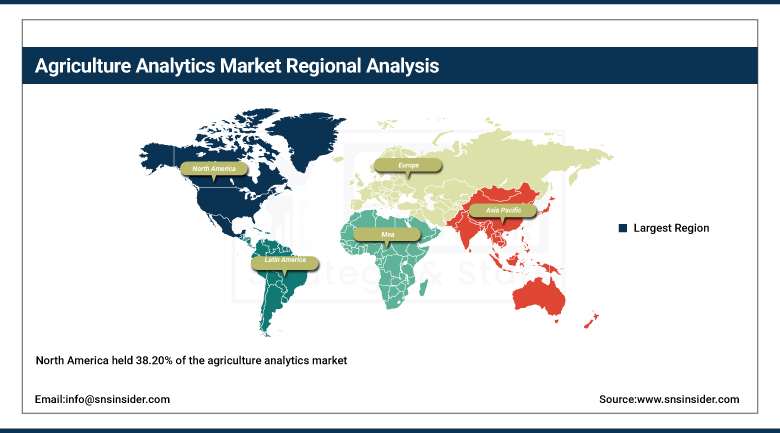

North America held 38.20% of the agriculture analytics market, primarily because farmers and agribusinesses across the continent continued increasingly embracing data-driven approaches for optimizing their operations. That combination of established precision agriculture adoption and mature farm technology infrastructure kept the continent firmly positioned as the market's clear leader by a considerable margin over every other region tracked in this report.

The United States accounted for roughly 80.35% of regional revenue, anchored by strong data-driven farming adoption and substantial agricultural technology investment. Canada added further regional demand through its own growing precision agriculture sector, and that combined strength kept North America the largest addressable market for agriculture analytics vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Agriculture Analytics Market Insights

Europe held a meaningful share of global revenue, supported by robust network infrastructure and high technology adoption rates that initially propelled cloud-based agriculture analytics adoption across the region's major agricultural economies. Continued regulatory emphasis on sustainable farming practices kept reinforcing steady European demand throughout the year.

Germany led demand at roughly 24.10% of European revenue, supported by its substantial agricultural technology manufacturing and adoption base. France and the UK contributed substantial additional demand, and continued European investment in precision farming technology should keep regional demand climbing through the forecast period.

Asia Pacific Agriculture Analytics Market Insights

Asia Pacific is anticipated to witness the fastest growth, with a CAGR of 15.25% during the forecast period. The increased adoption of advanced farming technologies, fueled by population growth and rising agricultural demands, continues contributing to regional market growth well ahead of every other region tracked in this report.

China led the pack, supported by its massive agricultural sector and rapidly growing domestic precision farming technology adoption. India and Southeast Asian economies contributed meaningful additional demand, with rapid mobile and internet penetration growth continuing to reinforce Asia Pacific's position as the fastest-growing market tracked in this report.

MEA and Latin America Agriculture Analytics Market Insights

The Middle East and Africa and Latin America both showed steady growth, driven by expanding agricultural technology investment, growing precision farming adoption, and rising government focus on food production efficiency across both areas. As these markets continued developing modern agricultural technology infrastructure, agriculture analytics adoption grew correspondingly from a considerably smaller base than in more mature markets.

The UAE led Middle East and Africa demand, supported by growing agricultural technology investment tied to the region's food security agenda. Saudi Arabia contributed further demand through its own agricultural modernization programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing large-scale farming operations continuing to anchor regional demand for agriculture analytics.

Market Dynamics

Growth Drivers: Food Production Efficiency Demand and Precision Farming Technology Convergence

The evolution toward data-centric, precision-driven agriculture is propelled by the need to enhance food production efficiency and sustainability for a growing global population. Key technologies such as precision agriculture software, IoT in farming, and AI for crop management continue enabling the collection and analysis of vast datasets related to soil conditions, weather patterns, and crop health.

Digitization of machinery and implements and telemetry pipelines, alongside proven ROI from input optimization, continue serving as major factors driving sustained market growth. That combination of genuine productivity necessity and demonstrated economic return is exactly what keeps demand climbing at such a sustained pace across virtually every major farming operation this market serves.

Restraints: Data Interoperability Gaps and Skills Shortages

Data interoperability and standardization gaps across original equipment manufacturers and platforms continue posing a genuine restraint on faster market-wide adoption, as farmers increasingly operate equipment and software from multiple vendors that don't always integrate seamlessly with one another. That fragmentation keeps genuine, unified farm data management a meaningfully more complex undertaking than simple analytics tool adoption alone would suggest.

Cybersecurity, data ownership, and privacy concerns among growers continue posing a further restraint, as farmers increasingly hesitate to share sensitive operational data with third-party analytics platforms without genuine clarity around data ownership and usage rights. That trust gap keeps some potential customers cautious about full-scale analytics platform adoption despite genuine productivity benefits.

Opportunities: Livestock Analytics Expansion and Small Farm Market Democratization

Livestock analytics expansion represents a genuinely significant opportunity, as this application category's fastest-growing status among all segments tracked in this market reflects genuine demand for sensor-based health monitoring and feeding optimization capability. Vendors offering genuinely proven, livestock-specific analytics technology stand to capture meaningful share as this application category continues expanding well beyond the market's traditional crop-focused stronghold.

Small farm market democratization offers a second substantial opportunity, as this farm-size category's fastest-growing status reflects genuine demand from smaller operations increasingly able to access affordable, cloud-based analytics tools. Vendors that can deliver genuinely cost-effective, easy-to-deploy solutions stand to capture meaningful share as agriculture analytics technology continues expanding beyond its traditional large-farm stronghold.

Recent Developments:

-

March 2025: John Deere Operations Center integrated its farm machinery data with EOSDA Crop Monitoring, allowing automatic synchronization of field data and improved precision farming mapping.

-

October 2025: Trimble announced enhancements to its Trimble Unity software suite with new capabilities focusing on asset lifecycle management, supporting farm data integration and operational planning.

-

2025: Bayer continued expanding its digital farming and predictive analytics platform, targeting large-scale farming operations seeking integrated crop management and yield optimization capability.

Agriculture Analytics Market key players are:

-

Deere & Company

-

Trimble Inc.

-

Bayer AG

-

Corteva Agriscience

-

CNH Industrial N.V.

-

AGCO Corporation

-

Raven Industries

-

Climate Corporation

-

Farmers Edge

-

Granular, Inc.

-

Arable Labs, Inc.

-

Iteris, Inc.

-

PrecisionHawk

-

Taranis

-

Prospera Technologies

-

Descartes Labs

-

Gro Intelligence

-

OneSoil

Agriculture Analytics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.50 Billion |

| Market Size by 2035 | USD 16.68 Billion |

| CAGR | CAGR of 14.0% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Offering (Solution, Service) • By Agriculture Type (Livestock Farming, Aquaculture Farming, Precision Farming, Vertical Farming, Others) • By Field Size (Small, Medium, Large) • By Deployment (On-premise, Cloud) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Deere & Company, Trimble Inc., IBM Corporation, Bayer AG, Corteva Agriscience, CNH Industrial N.V., AGCO Corporation, Raven Industries, Climate Corporation, Farmers Edge, Granular, Inc., Arable Labs, Inc., Iteris, Inc., PrecisionHawk, Taranis, CropX Technologies, Prospera Technologies, Descartes Labs, Gro Intelligence, OneSoil |

Frequently Asked Questions

The Agriculture Analytics Market is expected to grow at a CAGR of approximately 14.0% from 2026 to 2035, based on triangulated secondary research estimates.

The Agriculture Analytics Market was valued at approximately USD 4.50 Billion in 2025, based on triangulation across multiple independent research sources.

The major growth factor is the need to enhance food production efficiency and sustainability for a growing global population, combined with digitization of machinery and telemetry pipelines.

The Solutions segment dominated the Agriculture Analytics Market by component, representing an estimated 67.6% of revenue in 2025.

North America dominated the Agriculture Analytics Market in 2025, holding an estimated 35.9% share of total global market revenue.

Get in Touch