AI Assistant Market Report Scope & Overview

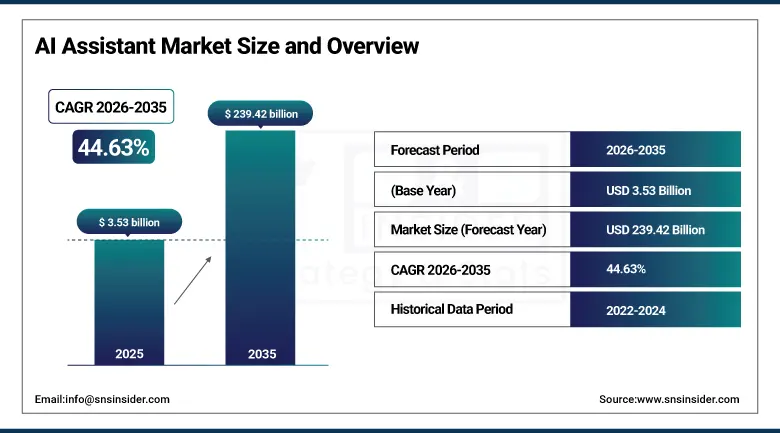

The AI Assistant Market was valued at USD 3.53 billion in 2025 and is expected to reach USD 239.42 billion by 2035, growing at a CAGR of 44.63% from 2026–2035.

The global AI assistant market is in the midst of an explosive commercial expansion that is simultaneously the fastest-growing and most strategically consequential segment of the enterprise software industry, driven by the convergence of large language model capability breakthroughs that have made conversational AI genuinely useful across a vastly broader range of professional and consumer tasks than earlier AI systems could address, the extraordinary scale of enterprise digital transformation investment directing capital toward AI-powered productivity tools as the highest-return near-term technology investment category, and the social normalisation of AI assistant usage proceeding at a pace that substantially outstrips the adoption curves of every previous enterprise technology platform from the personal computer through the smartphone. Microsoft’s striking finding that 75% of global knowledge workers are now using AI at work, with 46% having started within the preceding six months, captures both the extraordinary adoption velocity and the recency concentration of a market still in the early majority adoption phase despite having already reached extraordinary usage scale in absolute terms. IBM’s finding that two-thirds of AI leaders report more than 25% improvement in revenue growth rate attributable to AI adoption provides the executive-level business case that is converting boardroom enthusiasm for AI into committed budget allocation for AI assistant platform licensing, integration services, and organisational change management that together constitute the commercial opportunity the market’s extraordinary growth trajectory represents.

Microsoft’s May 2025 Build conference announcement that GitHub Copilot was being transformed into a fully autonomous AI coding assistant, and the simultaneous launch of Windows AI Foundry for enterprise-grade AI application deployment, represents the most significant product evolution milestone in the AI assistant market to date, demonstrating that the category is progressing from AI-assisted human workflows to AI-agentic autonomous execution that redefines the commercial boundaries of what ‘AI assistant’ means.

Market Size and Forecast

- Market Size In 2026E: USD 5.11 Billion

- Market Size By 2035: USD 239.42 Billion

- CAGR: 44.63% From 2026 To 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information on AI Assistant Market - Request Free Sample Report

AI Assistant Market Trends

- AI assistants are rapidly evolving from task support tools to autonomous AI agents capable of executing multi-step workflows independently.

- Growing adoption of multimodal AI assistants is enabling unified processing of text, voice, images, data, and code across enterprise applications.

- Rising demand for industry-specific AI assistants is improving accuracy and compliance in healthcare, legal, finance, HR, and software development sectors.

- Enterprises are increasingly implementing AI governance frameworks focused on privacy, compliance, bias detection, and output verification.

- Expanding integration of AI assistants with CRM, ERP, and workflow automation platforms is improving enterprise productivity and operational efficiency.

The U.S. AI Assistant Market Outlook

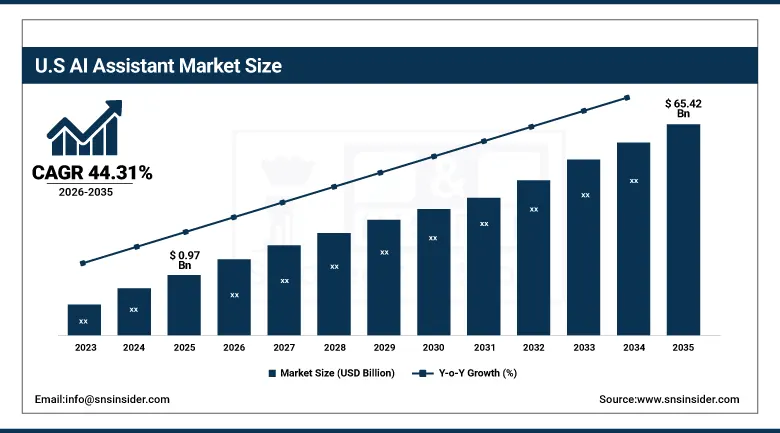

The U.S. AI assistant market was valued at approximately USD 0.97 billion in 2025 and is expected to reach approximately USD 65.42 billion by 2035, growing at a CAGR of 44.31%, anchored by the world’s largest enterprise software market whose concentration of technology-forward organisations across financial services, healthcare, retail, and professional services generates the most commercially sophisticated and highest-value AI assistant adoption environment globally.

The United States AI assistant market is characterised by the extraordinary breadth and depth of enterprise adoption across every major industry vertical, with Microsoft’s Copilot for Microsoft 365 achieving commercial penetration across tens of millions of U.S. knowledge workers through existing enterprise licensing relationships, Google’s Gemini for Workspace achieving comparable penetration across the substantial U.S. enterprise installed base, and OpenAI’s ChatGPT Enterprise securing a rapidly growing Fortune 500 customer base through direct sales engagements. The startup ecosystem’s contribution to the U.S. market is equally important, with vertical specialist companies including Glean for enterprise search and knowledge management, Harvey for legal AI, Abridge for clinical documentation, and Moveworks for IT service management collectively representing the growing commercial evidence base for vertical-specific AI assistant value propositions that general-purpose platforms struggle to match across regulated industry contexts.

The rapid convergence of AI assistant capability toward agentic task execution across coding, research, document management, and workflow orchestration is creating a category redefinition moment where the distinction between AI assistant and AI agent is collapsing into a unified autonomous capability layer that enterprise platform vendors including Microsoft, Salesforce, and ServiceNow are competing to own as the primary productivity and automation infrastructure layer for the modern enterprise.

AI Assistant Market Segment Analysis

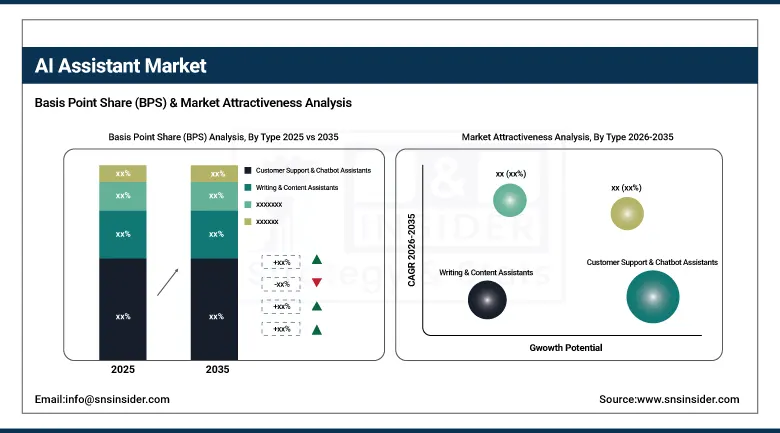

- By type, customer support and chatbot assistants led the market in 2025 with the largest revenue share driven by universal enterprise demand for 24/7 automated customer engagement that reduces contact centre costs while improving response consistency; personal productivity assistants are the fastest-growing type driven by the growing adoption of AI tools for schedule management, email drafting, task prioritisation, meeting summarisation, and workflow coordination representing the highest-frequency daily use cases for knowledge worker AI assistant adoption.

- By integration type, SaaS-native assistants dominated with approximately 34% share in 2025, reflecting the commercial advantage of AI assistants delivered within enterprise software platforms where employees already work, enabling workflow-embedded assistance without context switching; API-based assistants are the fastest-growing integration type at a CAGR of approximately 48.23% driven by enterprise demand for customisable, developer-friendly assistant integrations embedded within proprietary workflows and existing enterprise systems.

- By deployment, cloud-based AI assistants dominated with approximately 60% share in 2025 driven by natural alignment of AI assistant platforms with cloud infrastructure; hybrid AI assistants are the fastest-growing deployment model as regulated enterprises in financial services, healthcare, and government implement architectures combining cloud model inference with on-premises data handling to satisfy simultaneously AI capability requirements and data sovereignty obligations.

Customer Support Assistants Lead Type Segment, Personal Productivity Grows Fastest

Customer support and chatbot assistants retained the dominant type position in the AI assistant market in 2025, reflecting the universal enterprise need for customer engagement capability across every industry vertical and the extraordinary return on investment that AI-powered customer support automation delivers through contact centre cost reduction, 24/7 service availability, and consistent query resolution quality that human agent performance variability cannot guarantee at scale. The segment’s commercial maturity is evidenced by the breadth of industry adoption: financial institutions deploying AI assistants for account enquiry and loan application guidance, healthcare providers using AI for appointment scheduling and insurance pre-authorisation, telecommunications companies automating service troubleshooting and plan recommendation, and retail operators deploying AI for order tracking and returns processing all represent active customer support AI assistant deployments whose combined volume defines the segment’s market-leading position.

Personal productivity assistants are the fastest-growing type segment at a CAGR driven by the knowledge worker population’s progressive discovery that AI assistance for the high-frequency, cognitive-load-intensive administrative tasks that consume a substantial proportion of professional working time, including email composition, meeting preparation and summarisation, document drafting, research synthesis, presentation creation, and task management, delivers tangible and immediately experienced productivity improvements that build the personal habit formation and positive reinforcement cycles sustaining high daily active usage over time.

SaaS-Native Assistants Lead Integration Type, API-Based Grows Fastest

SaaS-native assistants retained the dominant integration type position with approximately 34% share in 2025, a dominance rooted in the commercial advantages of delivering AI capability within the familiar enterprise software environments where knowledge workers spend the majority of their productive working time, eliminating the context-switching friction and adoption barrier of introducing a separate AI tool that employees must proactively access rather than encountering naturally within their existing workflow. Microsoft’s Copilot integration within the full Microsoft 365 productivity suite, spanning Word, Excel, PowerPoint, Teams, Outlook, and SharePoint, represents the most commercially significant SaaS-native assistant deployment in market history, having achieved tens of millions of licensed seat deployments through enterprise agreements that made AI assistant access a procurement upgrade rather than a new product acquisition. Salesforce’s Agentforce AI platform embedding within Sales Cloud and Service Cloud, ServiceNow’s AI capabilities within enterprise service management workflows, and SAP’s Joule AI assistant embedded within ERP and HCM processes collectively represent the breadth of SaaS-native assistant deployment across enterprise business application categories where workflow-embedded AI assistance is delivering the highest commercial value.

API-based assistants are the fastest-growing integration type at a CAGR of approximately 48.23% through 2035, propelled by the developer ecosystem’s extraordinary productivity in building specialised AI assistant applications on top of foundation model APIs from OpenAI, Anthropic, Google, and Cohere, whose flexible, consumption-priced API access enables organisations to build customised AI assistant experiences tailored to their specific workflows, data environments, and user needs without the constraints of SaaS-native product feature sets. The API-based model’s particular commercial advantage for enterprise AI assistant deployment is the ability to fine-tune, constrain, and customise foundation model behaviour to reflect proprietary business knowledge, maintain compliance with data handling requirements, and integrate with internal systems and data sources that SaaS-native assistants cannot natively access, creating AI assistant experiences whose accuracy, relevance, and compliance alignment substantially exceed what general-purpose SaaS assistant products deliver for specialised professional contexts.

Cloud-Based Deployment Dominates, Hybrid Grows Fastest

Cloud-based AI assistants retained the dominant deployment position with approximately 60% of the market in 2025, reflecting the natural alignment of AI assistant platforms with cloud infrastructure whose scalability, model update frequency, and multimodal processing requirements are best served by cloud-native delivery that eliminates the hardware procurement, maintenance, and upgrade cycles that on-premises deployment imposes. The cloud deployment model’s commercial advantages including predictable subscription pricing, continuous feature updates without deployment effort, and consumption-based scaling that matches infrastructure cost to actual usage are particularly well-matched to AI assistant products whose rapid capability evolution and usage pattern unpredictability make fixed-capacity on-premises infrastructure both economically inefficient and capability-constraining. Major cloud AI assistant deployments including Microsoft’s Copilot delivered through Azure AI infrastructure, Google’s Gemini for Workspace on Google Cloud, and OpenAI’s ChatGPT Enterprise on its custom cloud infrastructure collectively define the cloud-delivered AI assistant commercial standard that on-premises and hybrid alternatives are measured against.

Hybrid AI assistants are the fastest-growing deployment model as regulated enterprises in financial services, healthcare, and government implement architectures that combine cloud model inference with on-premises data handling to satisfy simultaneously the capability requirements of advanced AI models and the data sovereignty requirements of their regulatory environments, creating a deployment pattern whose commercial adoption is being driven by the growing availability of hybrid AI assistant architectures from major vendors including Microsoft’s Azure AI hybrid configurations, IBM’s watsonx on-premises deployment options, and Anthropic’s enterprise deployment frameworks that support data residency requirements.

Regional Analysis

|

Region |

Major Country |

Share Within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America AI Assistant Market Insights

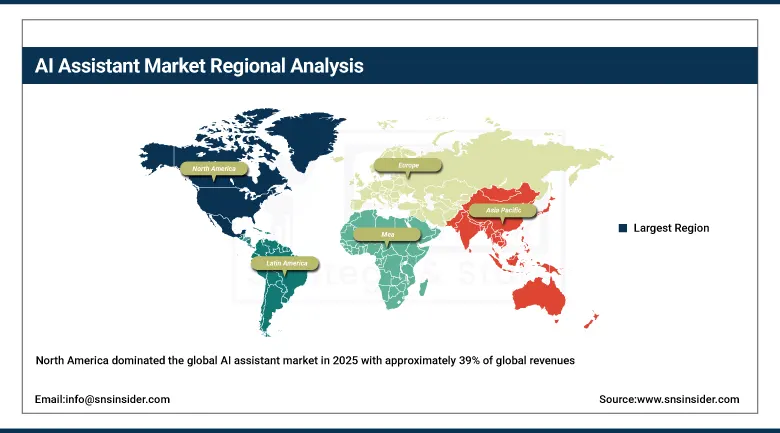

North America dominated the global AI assistant market in 2025 with approximately 39% of global revenues, the United States accounting for approximately 87.4% of North American revenues, driven by the world’s largest concentration of technology-forward enterprises whose aggressive AI adoption culture, deep Microsoft and Google ecosystem penetration, and willingness to commit substantial per-seat AI assistant licensing budget have made the U.S. both the largest and most commercially sophisticated AI assistant market globally. The concentration of major AI assistant vendors including Microsoft, Google, OpenAI, Anthropic, and Salesforce in U.S. headquarters creates a self-reinforcing innovation and adoption advantage where the most advanced product features are consistently available to U.S. enterprise customers earliest, and where the feedback loops between enterprise customer requirements and product development are shortest and most commercially productive. Canada contributes approximately 12.6% of North American AI assistant revenues through a technology sector with growing AI adoption particularly in financial services, e-commerce, and government, supported by strong AI research ecosystems in Toronto, Montreal, and Vancouver.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe AI Assistant Market Insights

Europe is a sophisticated and rapidly growing AI assistant market whose regulatory environment, anchored by the EU AI Act’s risk-based governance framework for AI systems deployed in consequential professional and public sector contexts, is simultaneously creating the compliance infrastructure that enables confident enterprise AI adoption and the governance standards that distinguish Europe as the world’s most regulated AI deployment environment. Germany accounts for approximately 22.3% of European AI assistant revenues as the region’s largest national market, where large industrial and financial sector corporations are adopting AI assistants for manufacturing process documentation, engineering knowledge management, financial reporting automation, and customer service within the governance frameworks that EU AI Act compliance and German industrial data sovereignty requirements establish. The European AI assistant market is being shaped by the growing differentiation between U.S.-origin foundation model assistants that must demonstrate GDPR data processing compliance and emerging European AI assistant providers including Aleph Alpha and Mistral AI whose European data residency and multilingual capability create compelling alternative positioning in markets where data sovereignty is a primary procurement consideration.

Asia Pacific AI Assistant Market Insights

Asia Pacific is the fastest-growing regional AI assistant market at a CAGR of approximately 47.04%, driven by China’s extraordinary pace of AI development and enterprise adoption, India’s rapidly growing technology services sector deploying AI assistants both for internal productivity and as a core component of AI-augmented services delivered to global clients, Japan and South Korea’s sophisticated enterprise markets with growing AI assistant adoption across manufacturing and financial services, and the dynamic Southeast Asian digital economy whose young, technology-forward business community is adopting AI assistant tools at adoption rates reflecting both the tools’ productivity value and the region’s cultural enthusiasm for technology adoption. China accounts for approximately 61.7% of Asia Pacific AI assistant revenues through the domestic AI assistant ecosystem centred on Baidu’s Ernie Bot, Alibaba’s Tongyi Qianwen, Tencent’s Hunyuan, and ByteDance’s Doubao, whose deployments across China’s enormous enterprise and consumer digital platforms reach hundreds of millions of users.

Latin America and MEA AI Assistant Market Insights

Latin America and the Middle East and Africa are rapidly emerging AI assistant markets where growing enterprise technology adoption, expanding digital economy infrastructure, and the availability of AI assistant platforms in Spanish, Portuguese, and Arabic are creating the conditions for accelerated AI assistant adoption beyond the English-language enterprise markets where adoption has historically concentrated. Brazil accounts for approximately 44.2% of Latin American AI assistant revenues through its large enterprise technology sector, a growing startup ecosystem with AI-first product development culture particularly in São Paulo’s fintech and e-commerce sectors, and the progressive adoption of Microsoft Copilot and Google Gemini within the Brazilian enterprise installed base. Saudi Arabia leads Middle East and Africa revenues at approximately 38.4% of the regional total, driven by Vision 2030’s digital government transformation directing AI adoption across government ministries, financial sector digital transformation creating AI assistant demand in banking and insurance, and a young digitally engaged workforce whose professional productivity expectations are aligned with AI tool adoption.

Market Dynamics

Growth Drivers: Large language model capability breakthroughs enabling genuinely useful AI assistance across knowledge work categories, enterprise productivity investment creating committed AI assistant budget allocation, and platform ecosystem integration reducing adoption friction

The primary structural growth drivers for the AI assistant market are the demonstrable and quantifiable productivity improvements that enterprise AI assistant deployment delivers across the knowledge work categories that constitute the majority of enterprise labour cost, combined with the rapid platform ecosystem integration by Microsoft, Google, and Salesforce that embeds AI assistant capability within the enterprise tools where the majority of professional work already occurs, reducing the adoption friction that historically slowed enterprise software adoption. The competitive pressure among enterprises that have deployed AI assistants against those that have not is creating a distinct productivity and innovation velocity differential that CEOs and CFOs are increasingly citing in earnings calls as both a current competitive advantage and a strategic imperative for laggards to close, translating boardroom awareness of AI’s potential into operational budget allocation for AI assistant deployment that is the most reliable commercial demand driver in the market’s growth trajectory. The generative AI capability advancement pace, consistently delivering new model capability milestones at quarterly intervals across reasoning, coding, multimodal processing, and agentic task execution, is simultaneously expanding the range of knowledge work tasks that AI assistants can address effectively and shortening the credibility half-life of sceptical positions that AI cannot reliably assist with specific professional task categories.

Restraints: Data privacy and intellectual property risk concerns limiting enterprise deployment scope, AI hallucination accuracy limitations requiring human oversight workflows, and workforce resistance to AI adoption creating deployment friction

A significant restraint on the AI assistant market is the data privacy and intellectual property risk that enterprise legal and compliance teams identify when evaluating AI assistant deployment, particularly for cloud-hosted foundation model services whose training data provenance, output copyright ownership, and customer data use policies raise legitimate concerns requiring adequate contractual and technical safeguards. The AI hallucination problem, where language models confidently generate plausible-sounding but factually incorrect outputs, creates a quality assurance requirement for human review of AI assistant outputs in consequential professional contexts including legal documentation, medical guidance, financial advice, and regulatory submissions, adding oversight labour cost that partially offsets productivity savings and limiting the return on investment calculus in high-accuracy-requirement contexts.

Opportunities: Vertical AI assistant specialisation creating premium market segments in healthcare and financial services, agentic AI workflow automation extending AI value to end-to-end process execution, and emerging market language model development creating new regional market access

The vertical AI assistant specialisation opportunity represents the most commercially defensible and highest-margin growth segment within the broader AI assistant market, as enterprises in regulated industries including healthcare, financial services, legal, and pharmaceutical are willing to pay premium pricing for AI assistants whose domain-specific training, regulatory compliance architecture, and professional accuracy standards demonstrably outperform general-purpose alternatives. Agentic AI assistant platforms executing multi-step workflows autonomously, including research, analysis, writing, decision recommendation, and system interaction without requiring human instruction at each step, represent the next commercial frontier whose realisation will dramatically expand the proportion of knowledge work that AI assistance addresses from the individual task level to the business process level whose end-to-end automation creates order-of-magnitude larger productivity returns.

Recent Developments

- 2025: Microsoft announced at Build 2025 that GitHub Copilot was being transformed into a fully autonomous AI coding assistant capable of executing multi-step development tasks independently, and launched Windows AI Foundry for enterprise-grade AI application deployment, marking the AI assistant market’s transition from task assistance to autonomous agentic execution.

- 2025: OpenAI launched GPT-4o enhancements that substantially improved real-time voice interaction quality, multimodal reasoning across text, images, and code within unified conversations, and released an expanded ChatGPT Enterprise feature set including enhanced admin controls, audit logging, and domain-specific GPT deployment capabilities addressing enterprise governance requirements.

- 2025: Google expanded Gemini for Google Workspace with new deep research and agentic task execution capabilities across Gmail, Docs, Sheets, and Meet, enabling autonomous multi-step workflow execution that extends AI assistant value from individual task support to workflow-level automation across the Google Workspace enterprise customer base.

AI Assistant Market Key Players are:

- Microsoft Corporation (Copilot)

- Google LLC (Gemini)

- OpenAI Inc. (ChatGPT)

- Anthropic PBC (Claude)

- Salesforce Inc. (Agentforce)

- IBM Corporation (watsonx)

- Amazon Web Services (Alexa for Business)

- Apple Inc. (Siri)

- Cohere Inc.

- Glean Technologies Inc.

- Jasper AI Inc.

- Copy.ai

- Harvey AI

- Abridge Inc.

- Moveworks Inc.

- Writer Inc.

- Mistral AI SAS

- Aleph Alpha GmbH

- Baidu Inc. (Ernie Bot)

- Alibaba Cloud (Tongyi Qianwen)

AI Assistant Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.53 Billion |

| Market Size by 2035 | USD 239.42 Billion |

| CAGR | CAGR of 44.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Customer Support & Chatbot Assistants, Writing & Content Assistants, Code Assistants, Personal Productivity Assistants, Others) •By Integration Type (SaaS-Native Assistants, API-Based Assistants, Browser Extension Assistants, Others) •By Deployment (Cloud-Based, On-Premises, Hybrid) •By End User (BFSI, Healthcare, IT & Telecom, Retail & E-Commerce, Education, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft Corporation (Copilot), Google LLC (Gemini), OpenAI Inc. (ChatGPT), Anthropic PBC (Claude), Salesforce Inc. (Agentforce), IBM Corporation (watsonx), Amazon Web Services (Alexa for Business), Apple Inc. (Siri), Cohere Inc., Glean Technologies Inc., Jasper AI Inc., Copy.ai, Harvey AI, Abridge Inc., Moveworks Inc., Writer Inc., Mistral AI SAS, Aleph Alpha GmbH, Baidu Inc. (Ernie Bot), Alibaba Cloud (Tongyi Qianwen) |

Frequently Asked Questions

Customer support and chatbot assistants dominated the AI assistant market in 2025.

The AI assistant market is expected to grow at a CAGR of 44.63% from 2026 to 2035.

Get in Touch