AI In Media & Entertainment Market Report Scope & Overview:

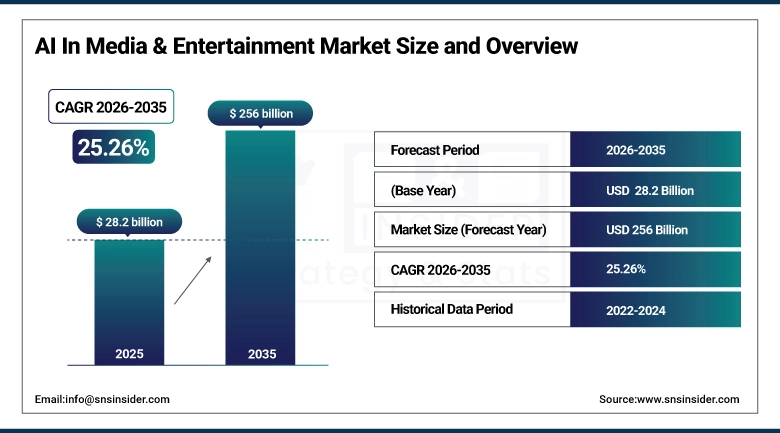

The AI in Media and Entertainment Market was valued at USD 28.2 billion in 2025 and is expected to reach USD 256 billion by 2035, growing at a CAGR of 25.26% from 2026-2035.

The growth of the AI in Media & Entertainment market is driven by the increasing adoption of personalized content recommendations, auto-generative videos, AI ads, and AI audience analytics in the digital entertainment sector. The adoption of technologies such as streaming technologies, gaming technologies, and virtual production solutions is driving the deployment of artificial intelligence in media. There is a shift towards the use of generative AI technologies, content moderation technologies, false content detection technologies, and real-time data analytics tools.

PwC's Global Entertainment & Media Outlook documents that the global E&M industry generated USD 2.7 trillion in revenue in 2025, creating a massive commercial base for AI investment that can generate ROI from even modest percentage improvements in production efficiency or audience engagement.

Goldman Sachs Research estimates that generative AI will eliminate or transform approximately 30% of the tasks currently performed by entertainment industry workers within a decade, while simultaneously enabling production of content types and volumes that current workforce economics cannot support.

AI in Media and Entertainment Market Size and Forecast

-

Market Size in 2025: USD 28.2 Billion

-

Market Size by 2035: USD 256 Billion

-

CAGR: 25.26% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on AI in Media and Entertainment Market - Request Free Sample Report

AI in Media and Entertainment Market Trends

-

Rising demand for personalized content experiences and audience engagement is driving the AI in media and entertainment market.

-

Growing adoption of AI across content creation, recommendation engines, advertising, and video analytics is boosting market growth.

-

Expansion of streaming platforms, digital media consumption, and social media content is fueling AI deployment.

-

Increasing focus on automation, real-time analytics, and targeted content delivery is shaping adoption trends.

-

Advancements in generative AI, machine learning, computer vision, and natural language processing are enhancing creativity and operational efficiency.

-

Rising demand for cost-effective production workflows and immersive entertainment experiences is supporting market expansion.

-

Collaborations between media companies, AI technology providers, and streaming platforms are accelerating innovation and global adoption.

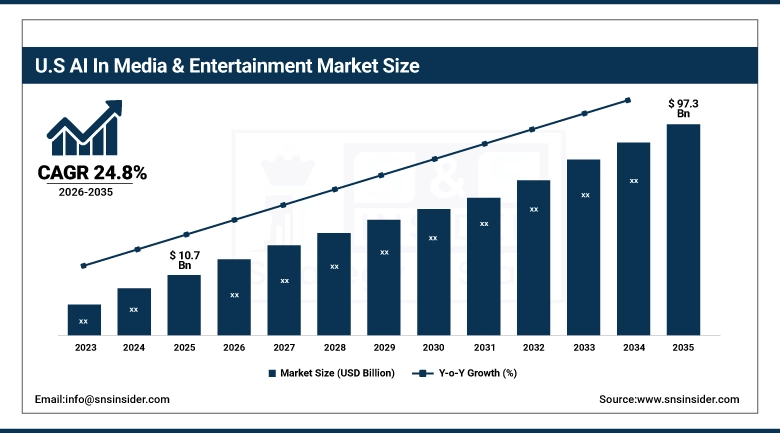

U.S. AI in Media and Entertainment Market was valued at USD 10.7 billion in 2025 and is expected to reach USD 97.3 billion by 2035, growing at a CAGR of 24.8% from 2026-2035.

The Artificial Intelligence (AI) for Media and Entertainment Market in the U.S. has been experiencing strong growth due to the high usage of AI-based platforms in digital streaming, digital advertising, games, and content production. There has been an increase in investments in generative AI, audience analysis, virtual production, and personalized entertainment from technology companies and media houses.

The Motion Picture Association's 2024 Economic Contribution study documents that the U.S. film, television, and streaming industry supports 2.4 million jobs and generates USD 229 billion in economic output annually a commercial base whose AI productivity potential at even 10-15% cost reduction represents USD 20+ billion in annual efficiency opportunity.

The Interactive Advertising Bureau documents that U.S. digital advertising reached USD 225 billion in 2025, with AI-optimized targeting and creative generation growing as a proportion of total digital ad spend.

AI in Media and Entertainment Market Segment Analysis

-

By Solution, Hardware/Equipment segment dominated the AI in Media and Entertainment Market in 2025 with ~58% share; Services segment fastest growing (CAGR).

-

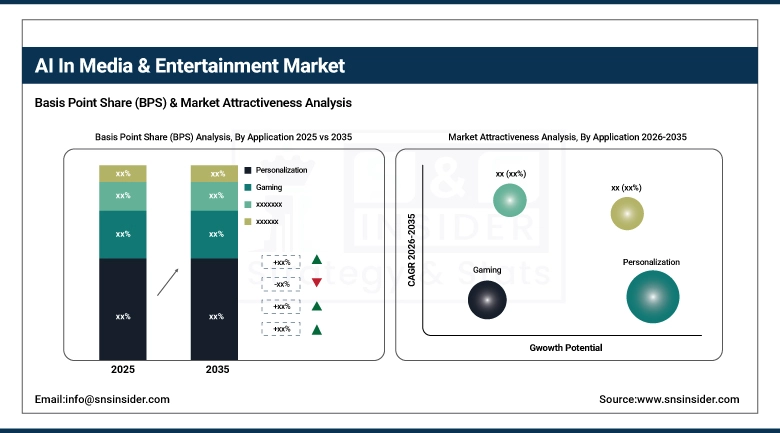

By Application, Personalization segment dominated the AI in Media and Entertainment Market in 2025 with ~27% share; Fake Story Detection segment fastest growing (CAGR).

By Application, Personalization segment dominates the AI in Media & Entertainment Market, Fake Story Detection segment expected to grow fastest

Personalization segment dominated the AI in Media and Entertainment Market owing to the increasing requirement for personalized content recommendations, targeting, and user-oriented experience on streaming platforms and digital media channels. AI-based personalization techniques allow media houses to perform analysis of consumer behavior and optimize customer engagement to retain users effectively with intelligent recommendation systems. Moreover, the fast emergence of OTT services, digital advertising, and interactive content has increased the prevalence of personalization technologies within the media industry.

Netflix's 2024 annual report discloses that the company invests over USD 1 billion annually in recommendation system development and AI infrastructure that drives content discovery - the largest single technology investment disclosure from a streaming company specifically for AI-powered personalization. Spotify's Wrapped annual campaign - powered by listening data analytics and AI pattern recognition - consistently generates the social media engagement that demonstrates the consumer resonance of personalized media experience at population scale.

The Fake Story Detection segment is anticipated to register the highest growth rate during the forecast period in the AI in Media and Entertainment Market on account of growing incidents of misinformation and fake news. With the growing prevalence of deepfakes, manipulation of videos, and misleading information on digital media and social networking platforms, media players have started using AI to detect the veracity of such content to ensure regulatory compliance and build credibility around their brands.

By Solution, Hardware/Equipment segment dominates the AI in Media & Entertainment Market, Services segment expected to grow fastest.

The Hardware/Equipment sub-segment is expected to dominate the AI in Media and Entertainment market because of the widespread use of AI-driven chips, GPU, smart camera, broadcasting equipment, and supercomputers in media and entertainment companies. Firms are focusing highly on investing in innovative hardware products that can help achieve efficient real-time rendering, video analysis, animations, gaming, and immersive content. The rising need for high processing speed has also supported the dominant position of hardware and equipment products in the market.

The Services segment is the fastest-growing in the AI in Media and Entertainment Market, driven by increasing demand for AI-related consulting, deployment, integration, maintenance, and managed services. With media companies leveraging AI for automation, content moderation, audience analysis, and recommendation systems, service providers see many opportunities. Constant innovations in cloud-based AI platforms and the rising demand for customized AI solutions in broadcasting, gaming, and digital entertainment sectors drive growth in the services segment.

AI in Media and Entertainment Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Asia Pacific |

China |

42% |

|

Europe |

United Kingdom |

26% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

50% |

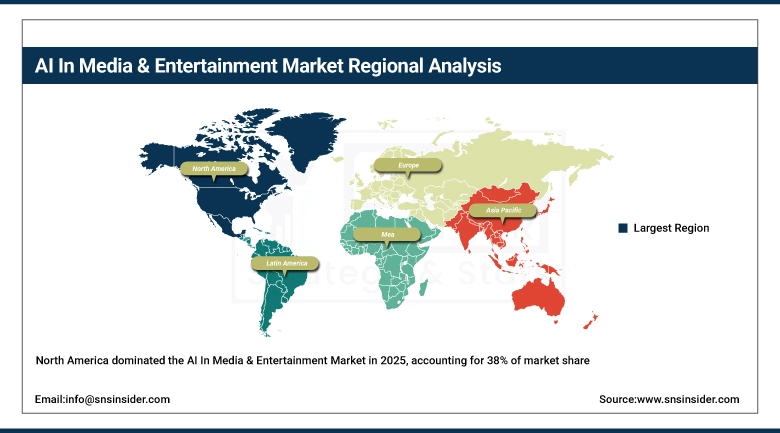

North America AI in Media & Entertainment Market Insights

North America held around 38% share of the AI in Media & Entertainment market owing to the presence of several top-tier technology organizations along with robust digital infrastructure and increased use of artificial intelligence within the streaming, gaming, and broadcasting sectors. There is considerable expenditure on various generative AI technologies, cloud computing solutions, virtual production, and audience analytics platforms within this geographic segment. Media & entertainment organizations based in the U.S. and Canada are fast adopting AI to enable personalized content distribution, automated production processes, and smart advertising campaigns.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific AI in Media & Entertainment Market Insights

Asia Pacific is the fastest-growing regional AI in Media and Entertainment Market owing to rapid digitization, internet usage, and increased consumption of entertainment via online media. Adoption of OTT service providers, mobile gaming, social media applications, and AI-based streaming services will fuel growth of the AI in Media & Entertainment market in the Asia Pacific region. Government organizations, along with other private enterprises, are extensively utilizing artificial intelligence technology to develop their digital media capabilities. The availability of large consumer bases, increased use of smartphones, and rising demand for personalized entertainment solutions will further drive the adoption of AI in the media and entertainment sector in the Asia Pacific region.

South Korea's government-funded AI content creation initiative the K-Content AI Support Program - provides subsidies for small and medium entertainment companies deploying AI tools, sustaining adoption beyond the large conglomerate players who would invest regardless of subsidy.

Europe AI in Media & Entertainment Market Insights

In the Europe Artificial Intelligence in Media & Entertainment Market, there is constant growth due to the growing use of AI-enabled systems that recommend content, automate production processes in media, and support advanced advertising technologies. Media organizations in Europe are using artificial intelligence for increased engagement with audiences, optimized broadcast processes, and enhanced streaming experience in digital space. Additionally, the increased demand for personalized content and the increasing presence of OTT services, along with a greater emphasis on AI content moderation and fake media detection, is aiding the growth of the market.

Middle East & Africa and Latin America AI in Media & Entertainment Market Insights

Middle East and Africa’s AI in Media & Entertainment sector is thriving due to high digital content consumption rates, government-led smart city projects, and increasing use of AI technology in personalized content and automation. The Latin American AI in Media & Entertainment sector is thriving due to increasing reach of streaming platforms, mobile-first consumer behavior, and high demand for local content. Increased investments are being made in AI-based analytics, recommendations, and advertising solutions to improve viewer experience and monetization while gradually transforming the media industry eco-system into a digital one.

AI in Media & Entertainment Market Growth Drivers:

-

Rising Demand for Personalized Streaming Experiences and AI-Based Audience Analytics Accelerates Intelligent Content Delivery Across Media Platforms

The rising tendency toward individualized entertainment has led to a widespread application of artificial intelligence in the sphere of media and entertainment platforms. The streaming platforms, broadcast companies, and even digital media use AI to process data related to users' behavior, consumption habits, content preferences, and other important characteristics. In particular, AI-based recommender systems help retain customers, maximize watch time, and ensure that users receive personalized content that increases their satisfaction level. Predictive analytics, which media and entertainment platforms use to enhance advertising techniques and audience targeting, is also based on artificial intelligence. The rise of OTT services, digital gaming, and social media entertainment creates additional grounds for using AI solutions.

AI in Media & Entertainment Market Restraints:

-

Growing Concerns Regarding Deepfake Misuse, Copyright Violations, and Ethical Challenges Limit Trust and Regulatory Acceptance Across Media Ecosystems

The widespread misuse of AI-produced content and the use of deepfakes technology has led to ethical and legal challenges for the media and entertainment industry. The technology allows for highly realistic manipulation of audio, video, and images and, therefore, poses significant problems such as those associated with spreading misinformation, identity theft, fake news distribution, and defamation. Media corporations are under increasing pressure to uphold integrity and credibility in digital content creation. Moreover, legal disputes surrounding copyright ownership rights of AI-generated content present challenges to publishing and production companies. New laws concerning digital content are being enacted by governments, which would make using AI technologies more difficult and costly.

AI in Media & Entertainment Market Opportunities:

-

Expanding Integration of Generative AI in Virtual Production and Immersive Entertainment Experiences Creates New Revenue Streams Across Digital Media Platforms

The fast-paced development of generative AI is offering many growth opportunities for media and entertainment firms that build immersive digital products. Through the use of AI technology, firms can create realistic virtual characters, AI music, automated stories, digital avatars, and immersive game worlds. Many entertainment companies have been making efforts towards building their virtual studios using AI. With an increase in the usage of AR, VR, and metaverse entertainment platforms, there has been an increased demand for smart content generating systems. This can be done through the use of AI-based immersive technologies, which allow companies to adopt new forms of monetization such as personalized advertisements and subscriptions among others.

Recent Developments:

-

2026: OpenAI launched Sora Studio, enabling broadcasters to generate 4K AI videos from text and image prompts within minutes. Discovery Networks adopted the platform for multilingual promotional content generation across 50 international markets simultaneously.

-

2025: Spotify expanded its AI DJ feature across 100 global markets using GPT-4-powered mood-adaptive playlist generation. The platform improved skip-rate reduction and increased listening session duration through personalized music sequencing and contextual recommendation capabilities.

-

2025: Amazon Prime Video introduced AI Production Assistant for independent creators, automating graphics, descriptions, and promotional asset generation from uploaded videos. The tool reduced documentary post-production marketing asset creation time from weeks to only several hours.

AI in Media and Entertainment Market Key Players

Some of the AI in Media and Entertainment Market Companies

-

Amazon Web Services

-

IBM

-

Microsoft

-

Google

-

NVIDIA

-

Oracle

-

Adobe

-

Accenture

-

Cognizant

-

Wipro

-

Veritone

-

Synthesia

-

GrayMeta

-

Pixellot

-

PlaySight Interactive

-

Gravity Media

-

EMG

-

Production Resource Group

-

TAIT

-

Valossa Labs

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.2 Billion |

| Market Size by 2035 | USD 256 Billion |

| CAGR | CAGR of 25.26% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (Hardware/Equipment, Services) • By Application (Gaming, Fake Story Detection, Plagiarism Detection, Personalization, Production Planning and Management, Sales and Marketing) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amazon Web Services, IBM, Microsoft, Google, NVIDIA, Oracle, Adobe, Accenture, Cognizant, Wipro, Veritone, Synthesia, GrayMeta, Pixellot, PlaySight Interactive, Gravity Media, EMG, Production Resource Group, TAIT, Valossa Labs |

Frequently Asked Questions

North America dominated with approximately 38% share in AI in Media and Entertainment Market.

Personalization dominated the AI in Media and Entertainment Market with approximately 27% share in 2025, while Fake Story Detection is the fastest growing segment during the forecast period.

Hardware/Equipment dominated the AI in Media and Entertainment Market with approximately 58% share in 2025.

The AI in Media and Entertainment Market was valued at USD 28.2 billion in 2025.

The AI in Media and Entertainment Market is expected to grow at a CAGR of 25.26% from 2026 to 2035.

Get in Touch