AI in Oncology Market Overview:

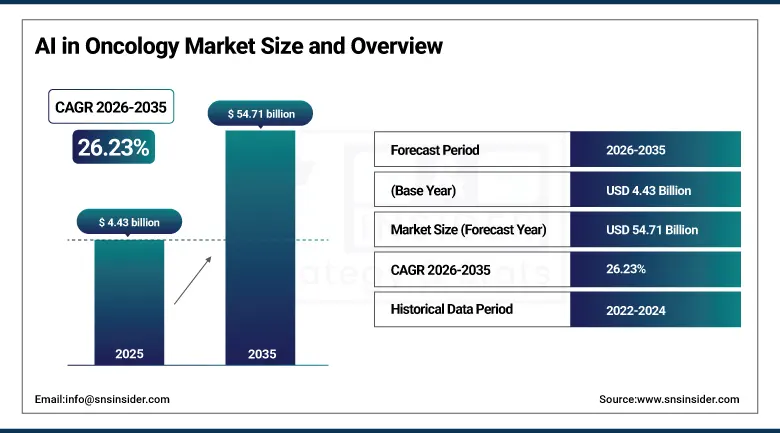

The AI in oncology Market size was valued at USD 4.43 billion in 2025 and is expected to reach USD 54.71 billion by 2035, growing at a CAGR of 26.23% over the forecast period of 2026-2035.

The global AI in oncology market has seen rapid development driven by the rising incidence of cancer, growing demand for precision treatment, and advances in AI technologies. While more than 20 million new cases of cancer are diagnosed each year globally, with lung cancer still the leading cause of cancer death, diagnostic performance is crucial to healthcare systems. AI in oncology plays a central role in early detection, risk stratification, and personalized treatment, with programs achieving diagnostic accuracy of over 90% in image-based cancer detection.

In May 2025, DeepScribe partnered with Flatiron Health to deliver ambient AI solutions tailored for oncology documentation to over 4,200 providers in Flatiron’s network.

Key Market Size and Forecast:

-

Market Size in 2025: USD 4.43 Billion

-

Market Size by 2035: USD 54.71 Billion

-

CAGR: 26.23% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on AI in oncology Market - Request Free Sample Report

Key Market Trends:

-

Rising adoption of AI-driven diagnostic tools for early cancer detection and personalized treatment.

-

Increasing integration of genomics, imaging, and clinical data to enable precision oncology.

-

Growing demand for AI-powered clinical trial optimization and patient recruitment platforms.

-

Expansion of AI-based radiology and pathology solutions in hospitals and cancer centers.

-

Rising investments by healthcare providers and pharmaceutical companies in AI research and development.

-

Collaborations between AI startups and major healthcare institutions to accelerate oncology innovation.

-

Government initiatives and supportive regulations fostering AI adoption in oncology diagnostics and treatment planning.

-

Azra AI recently launched an AI oncology platform in 2025 that integrates real-world patient data and genomic profiling to optimize clinical trial enrollment and precision treatment recommendations.

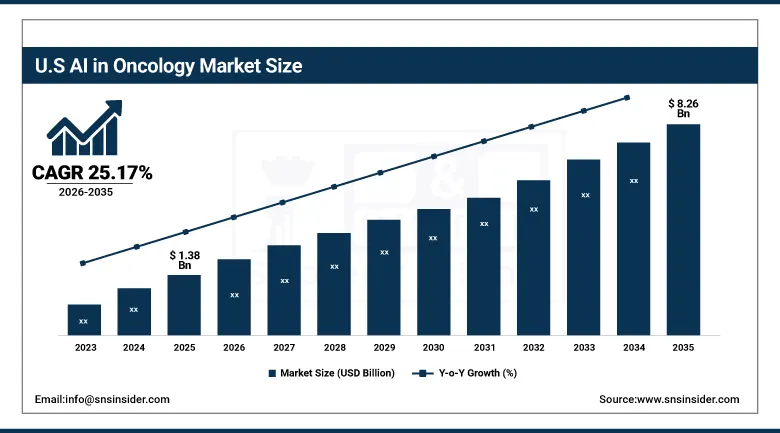

The U.S. AI in oncology market size was valued at USD 1.38 billion in 2025 and is projected to reach USD 8.26 billion by 2035, growing at a CAGR of 25.17%, driven by increasing investments in AI R&D, adoption of precision medicine, and deployment of AI solutions in leading cancer centers like MD Anderson and Memorial Sloan Kettering. Rising digital healthcare infrastructure and cross-border tech investments further accelerate market expansion.

Key Market Dynamics:

Drivers:

-

Rising Demand for Precision Oncology and AI-Driven Clinical Tools Propel the Market Expansion

Rising complexity in cancer, adoption of personalized approach, and increasing requirement for quick and accurate diagnosis are driving the global AI in oncology market. Cancer diagnosis is transformed with AI algorithms providing up to 95% accuracy in detecting malignancies in CT and PET scans, and decreasing interpretation time by more than 50%. Hospital EMRs now include AI-enabled clinical decision support tools, and use of such tools at comprehensive cancer centers has grown 42% in the past three years from 2021-2024. By combining multi-omics and real-world evidence with patient genomics into AI, oncologists can personalize treatment regimens and improve outcomes.

In April 2025, Tempus signed expanded strategic agreements with AstraZeneca and Pathos to develop the largest multimodal foundation model in oncology globally, aiming to accelerate AI-powered drug discovery and precision treatment.

Demand is boosted by higher R&D expenditure, and global AI on cancer-related clinical trials has grown 4.7x over the last six years. There is also regulatory backing, and more than 30 cancer-related AI devices were approved by the U.S. FDA to use AI between 2019 and 2024, and organizations, such as CDSiC and ASCO, have produced prescriptive guidelines to promote ethical use of AI. AI in oncology companies is also enjoying significant funding support. AI drug discovery platforms bagged over USD 2.3 billion in investment in 2023 alone. The accelerating importance of cutting down on doctor burnout and decision fatigue has led to greater reliance on AI for planning treatments and reporting on radiology, an evolution that has helped keep alive the expanding AI in oncology market.

Restraints:

-

Data Privacy, Infrastructure Gaps, and Clinical Validation Challenges Hamper the Market Growth

Data privacy is one major hurdle, and 85% of healthcare leaders identify HIPAA and GDPR compliance as barriers to implementing AI at scale. AI is dependent on large, high-quality labeled datasets, however, hidden, fragmented EHR systems and non-standardized cancer registries block effective data transfer. Tumor detection sensitivity decreased by 21% in underrepresented populations, a 2023 study found, as AI algorithms often learn from non-diverse data, underpinning diagnostic inaccuracies among ethnic groups. Furthermore, clinical validation is incomplete, and only 12% of the oncological AI tools in the clinical trials are at the Phase III stage. Differences in infrastructure are also a barrier due as over 50% of mid-tier hospitals in developed countries describe a lack of GPU servers and IT resources to deliver AI solutions in real time.

From a regulatory perspective, although the FDA has approved AI tools, evolving SaMD (Software as a Medical Device) guidelines introduce compliance ambiguity. Furthermore, physician skepticism remains 40% of oncologists polled had reservations about AI interpretability and patient confidence. The resulting combined constraints may slow down holistic adoption and the speed of uptake of AI in the oncology market despite strong promise and high need.

AI in Oncology Market Segmentation Analysis:

By Component Type

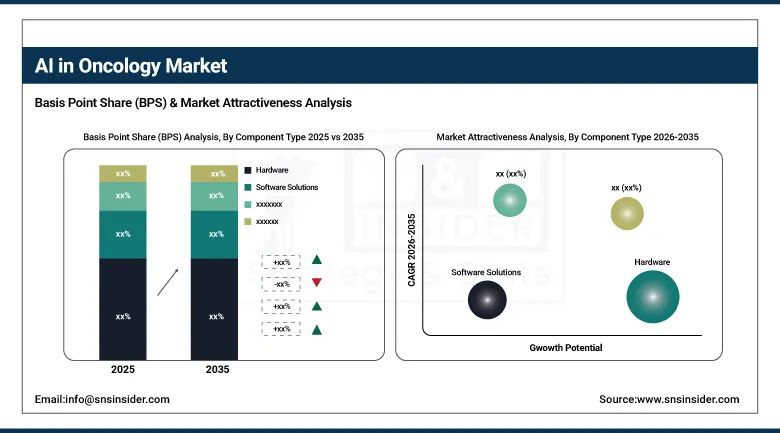

In 2025, hardware is the leading category under the AI in oncology market, which was valued at 40.2% AI in oncology market share of revenue. This leadership is driven by the growing need for high-performance computing infrastructure, including GPUs, AI chips, and edge devices that can immediately process complex oncology datasets in real-time. Significant investment in AI-ready imaging equipment and data storage systems by hospitals and research centres was driving hardware adoption.

On the other hand, software solutions is expected to be the fastest-growing segment in the market, as AI-based solutions are increasingly being integrated with diagnostic platforms, workflow assistance, and decision support platforms. There is growing use of cloud-based AI software that analyzes multifaceted data (genomics and radiomics) to improve prediction and treatment planning for a broad range of oncology use cases.

By Cancer Type

In 2025, breast cancer was the largest segment of the AI in oncology market, accounting for an AI in oncology market share of 21.3%. The growth is attributed to the increasing number of mammography and digital breast tomosynthesis for early detection and classification, bolstered by AI algorithms. Additionally, breast cancer also benefits from high levels of screening programs and public awareness, resulting in a larger number of diagnoses.

For instance, in March 2025, Vanderbilt University Medical Center researchers announced their leadership in an AI-driven oncology workshop at AACR 2025, emphasizing advancements in deep learning for cancer research.

Meanwhile, the prostate cancer segment is expected to be the fastest growing, driven by the increase in AI-assisted MRI interpretation and image-guided biopsy optimization. AI is now facilitating accurate tumor mapping and risk grouping, enhancing clinical judgments and patient proactive outcomes in the management of prostate cancer.

By Application

In 2025, the most widespread application of AI in oncology was diagnostics, which occupied 37.3% of the total AI in oncology market. The prevalence of diagnostics is supported by the ever-increasing demand for accurate, point-of-care (POC), and high-throughput cancer detection devices. AI-augmented radiology and pathology systems also shorten diagnosis time and cut error rates, and can help clinicians find tumors at earlier stages.

The increase in use of AI tools to tailor drug dosing, predict toxicity, and assess responses to treatment, on the other hand, means that the chemotherapy category is projected to grow the fastest. This assists oncologists in personalizing the regimens and minimizing the side effects for enhanced patient care in chemotherapy-based treatment strategies.

By End Use

Hospitals dominated the AI in oncology market with the largest share of 49.3% during the forecast period due to the wide usage of AI-based imaging solutions, diagnostic tools, and treatment planning systems in hospitals. Hospitals act as the central access points for cancer diagnosis, treatment, and surgery, and are the single largest adopters of AI.

The highest growth rate is projected in the surgical centers and medical institutes with the rising demand for AI-powered robotic surgery systems, AI-enhanced intraoperative imaging systems, and AI-based precision oncology platforms. In addition, their ability to adopt emerging technologies and involvement in clinical research facilitate the wider adoption of AI in these specialized settings.

AI in Oncology Market Regional Insights:

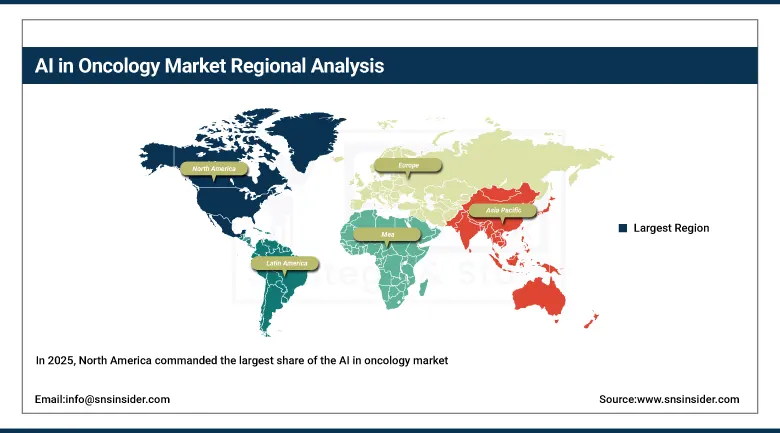

North America Dominates AI in Oncology Market in 2025

In 2025, North America commanded the largest share of the AI in oncology market, driven by high healthcare digitization, presence of leading AI oncology players, and early adoption of AI-enabled precision medicine solutions. Advanced hospitals and cancer centers leverage AI for diagnostics, treatment planning, and clinical research, which accelerates adoption across the region. Increasing investments in AI startups and partnerships between technology firms and healthcare institutions further boost market growth. Cross-border collaborations are gradually expanding AI-based oncology capabilities into Mexico, enhancing regional presence.

The United States is the dominating country in North America’s AI in oncology market. Valued at USD 1.38 billion in 2025, the U.S. benefits from a robust AI R&D ecosystem with over USD 48 billion in oncology-focused research, supportive government policies like FDA’s Software Precertification Program, and widespread integration of AI in leading cancer centers such as MD Anderson and Memorial Sloan Kettering. These factors create a strong adoption environment for AI platforms in diagnostics, radiology, and digital pathology, ensuring the U.S. remains the regional leader in oncology AI solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe AI in Oncology Market Insights, 2025

Europe held the second-largest share in the AI in oncology market in 2025, driven by robust national healthcare systems, EU digital health regulations, and cooperative R&D initiatives such as Horizon Europe. Countries are rapidly integrating AI in hospital oncology workflows, diagnostics, and treatment planning, enhancing efficiency and clinical outcomes.

Germany dominates Europe’s market due to its established medical device industry, active AI integration in radiotherapy planning, and strong collaborations between healthcare providers and AI companies, improving clinical accuracy and research capabilities.

Asia-Pacific Leads Fastest-Growing AI in Oncology Market 2026-2035

Asia-Pacific is expected to grow at the fastest CAGR over 2026–2035, fueled by rising cancer prevalence, government-backed AI initiatives, expanding digital health infrastructure, and the need for enhanced diagnostic accuracy. Increased adoption of AI-assisted surgical oncology and precision medicine platforms is driving market expansion.

China is the regional leader, boasting aggressive AI policies and investments in hospital AI platforms, with the health AI industry surpassing USD 10 billion in 2024. Tencent and Alibaba, along with other domestic tech players, are deploying oncology-focused AI solutions. India, Japan, and South Korea are accelerating AI integration through precision oncology centers, robotics, and machine learning applications, strengthening the region’s growth trajectory.

Middle East & Africa and Latin America AI in Oncology Market Insights, 2025

In 2025, Middle East & Africa showed steady AI adoption in oncology, driven by increasing digital health initiatives, government partnerships, and investments in smart healthcare infrastructure. Countries like Saudi Arabia and UAE are piloting AI-assisted cancer diagnostics and treatment platforms.

Latin America is growing gradually with Brazil and Mexico leading adoption through hospital-based AI projects in radiology and oncology. Expansion of AI infrastructure, regional partnerships, and rising awareness of precision oncology solutions are enhancing the market for AI-driven oncology tools.

Key Market Players:

Prominent AI in oncology companies operating in the market are Azra AI, IBM, Siemens Healthcare GmbH, Intel Corporation, GE HealthCare, NVIDIA Corporation, Digital Diagnostics Inc., ConcertAI, Median Technologies, PathAI, and MVision AI.

Competitive Landscape of AI in Oncology Market:

Azra AI

Azra AI is a U.S.-based clinical research and AI healthcare company focused on oncology, offering AI-driven platforms for precision cancer treatment and clinical trial optimization. The company specializes in integrating patient data, genomics, and imaging analytics to accelerate oncology research and improve therapeutic outcomes. Its role in the AI in oncology market is critical, enabling pharmaceutical companies and healthcare providers to identify suitable patients, optimize treatment plans, and streamline clinical trials.

-

In 2025, Azra AI launched an enhanced AI oncology platform that combines genomic profiling with real-world patient data, enabling predictive analytics for faster clinical trial enrollment and personalized treatment recommendations.

IBM

IBM is a U.S.-based technology and AI leader providing AI-powered healthcare solutions, including oncology-focused platforms for diagnostics, treatment planning, and precision medicine. The company leverages its Watson Health AI framework to analyze imaging, genomic, and clinical data, assisting oncologists in personalized decision-making. Its role in the AI in oncology market is substantial, improving diagnostic accuracy, optimizing therapy options, and accelerating research workflows in hospitals and cancer centers.

-

In 2025, IBM expanded Watson for Oncology with advanced natural language processing (NLP) algorithms to integrate unstructured medical records and genomic data for better predictive insights and treatment recommendations.

Siemens Healthcare GmbH

Siemens Healthcare GmbH, based in Germany, is a leading provider of medical imaging and AI-driven healthcare solutions. The company develops oncology-focused AI software for radiology, diagnostics, and treatment planning, integrating machine learning to enhance accuracy and workflow efficiency. Its role in the AI in oncology market is vital, supporting hospitals with advanced imaging analysis, precision radiotherapy planning, and predictive analytics for cancer care.

-

In 2025, Siemens Healthcare introduced AI-enabled radiotherapy planning tools that reduce treatment planning time and improve dose accuracy, enhancing outcomes in oncology centers across Europe and Asia.

Intel Corporation

Intel Corporation is a U.S.-based global semiconductor and technology company delivering AI hardware and software solutions for healthcare, including oncology applications. Intel specializes in AI accelerators, GPUs, and edge-computing solutions that power AI-driven cancer diagnostics and clinical decision support systems. Its role in the AI in oncology market is significant, providing the infrastructure to deploy scalable AI platforms in hospitals, research centers, and clinical trials worldwide.

In 2025, Intel launched a specialized AI hardware platform optimized for oncology analytics, enabling faster genomic processing, high-throughput imaging analysis, and real-time predictive insights for cancer treatment.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.22 Billion |

| Market Size by 2035 | USD 54.71 Billion |

| CAGR | CAGR of 26.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type (Software Solutions, Hardware, and Services) • By Cancer Type (Breast Cancer, Lung Cancer, Prostate Cancer, Colorectal Cancer, Brain Tumor, and Others) • By Application (Diagnostics (Pathology, Cancer Radiology), Radiation therapy (Radiotherapy), Research & Development (Drug design, development process, etc.), Chemotherapy, and Immunotherapy) • By End Use (Hospitals, Surgical Centers & Medical Institutes, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Azra AI, IBM, Siemens Healthcare GmbH, Intel Corporation, GE HealthCare, NVIDIA Corporation, Digital Diagnostics Inc., ConcertAI, Median Technologies, PathAI, and MVision AI. |

Frequently Asked Questions

Ans: North America dominated the AI in Oncology market.

Ans: Data privacy is one major hurdle. 85% of healthcare leaders identify HIPAA and GDPR compliance as barriers to implementing AI at scale.

Ans: Rising complexity in cancer, adoption of personalized approach, and increasing requirement for quick and accurate diagnosis are driving the global AI in oncology market.

Ans: The AI in oncology market size was valued at USD 4.43 billion in 2025 and is expected to reach USD 54.71 billion by 2035, growing at a CAGR of 26.23% over the forecast period of 2026-2035.

Ans: The AI in Oncology market is anticipated to grow at a CAGR of 26.23% from 2026 to 2035.

Get in Touch