AI in Telecommunication Market Report Scope & Overview:

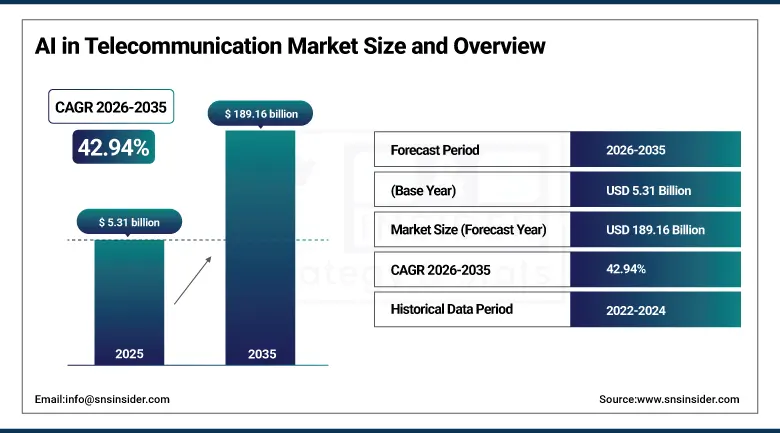

The AI in Telecommunication Market was valued at USD 5.31 billion in 2025 and is expected to reach USD 189.16 billion by 2035, growing at a CAGR of 42.94% from 2026–2035.

The worldwide artificial intelligence in telecommunications market is revolutionizing the telecommunication industry by embedding artificial intelligence into their network, customer relationship management, and process optimization practices. The adoption of AI technology in telecom networks is becoming increasingly common for predictive maintenance, automatic network faults detection, network traffic control, fraud detection, and intelligent customer support systems. The increased deployment of 5G infrastructure and the eventual migration to the 6G network is making networks more complex, necessitating the use of AI technologies for automation and decision-making. Telecoms use AI technology to increase efficiencies, minimize downtime, manage bandwidth allocation, and improve the customer experience. Cloud-native architectures, edge computing, and big data are also driving adoption rates of AI technology in telecommunications networks. Moreover, the demand for autonomous and intelligent networks is fueling market growth prospects worldwide.

In 2025, NVIDIA partnered with T-Mobile, Cisco Systems, and MITRE to develop AI-native wireless network infrastructure for future 6G systems. Additionally, Ericsson launched generative AI-powered telecom management capabilities to automate network optimization and service assurance processes.

Market Size and Forecast

-

Market Size 2026E: USD 7.59 Billion

-

Market Size 2035: USD 189.16 Billion

-

CAGR (2026-2035): 42.94%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on AI in Telecommunication Market - Request Free Sample Report

AI in Telecommunication Market Trends

-

AI-native network architectures are becoming foundational to future 6G telecom infrastructure development and standardization.

-

Telecom AI platform-as-a-service solutions are expanding AI adoption among smaller operators and MVNOs through subscription-based models.

-

Edge AI deployment alongside 5G base stations is enabling ultra-low-latency applications such as autonomous vehicles and immersive XR services.

-

Telecom operators are increasingly adopting AI-driven automation to reduce operational costs and improve network efficiency and profitability.

-

AI is becoming essential for managing complex 5G functions including network slicing, massive MIMO optimization, and dynamic resource allocation.

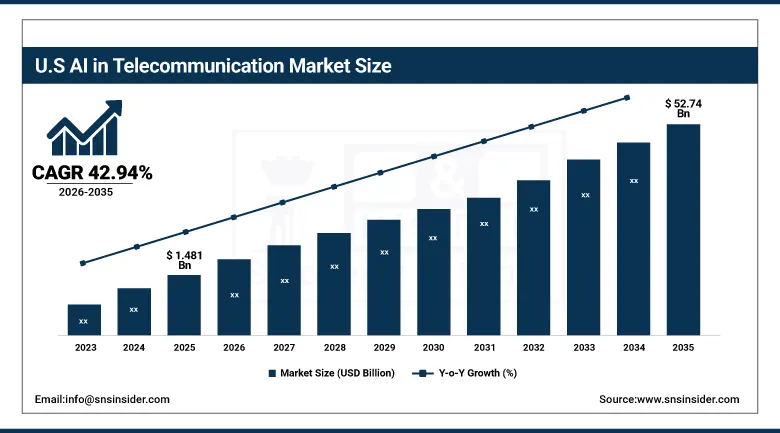

The U.S. AI in Telecommunication Market Size Outlook

The U.S. AI in Telecommunication Market was valued at approximately USD 1.481 billion in 2025 and is expected to reach approximately USD 52.74 billion by 2035, growing at a CAGR of 42.94% during 2026–2035.

The United States represents the most commercially advanced AI in Telecommunication market, characterised by the world's largest and most technically sophisticated telecom AI deployment programmes at AT&T, Verizon, and T-Mobile, the most active AI technology vendor ecosystem serving telecom operators with purpose-built network intelligence solutions, and the most extensive 5G network deployment providing the operational context that makes AI network management a commercial necessity rather than an optional enhancement. U.S. telecom operators are among the world's highest-spending deployers of AI for both network operations and customer management, recognising that AI automation is the primary lever for reducing the operating expense intensity that has historically constrained telecom industry profitability improvement despite revenue growth.

AT&T's deployment of AI-powered network operations platforms managing its nationwide 5G and fibre network at AI-automated speed and scale, combined with Verizon's AI customer analytics programmes reducing churn and improving service personalisation across its 100-plus million subscriber bases, confirm that the largest U.S. telecom operators have committed to AI as a strategic operational transformation tool rather than a tactical cost reduction programme.

AI in Telecommunication Market Segment Analysis

-

According to Component, Solutions dominated in 2025 through deployment of integrated AI platforms for network management, fraud detection, and customer analytics; Services is growing rapidly as telecom operators engage AI system integrators and managed AI service providers for implementation and ongoing optimisation support.

-

In terms of Technology, Machine Learning dominated as the foundational AI technology enabling network optimisation, churn prediction, and fraud detection across the broadest range of telecom applications; Natural Language Processing is the fastest-growing technology driven by conversational AI customer service and voice analytics adoption.

-

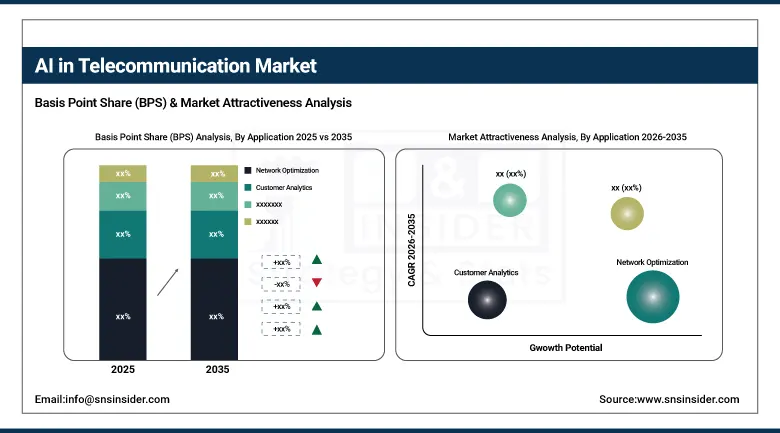

By Application, Network Optimization dominated as the largest and most commercially validated AI telecom application; Customer Analytics is growing rapidly through churn prediction, personalised offer generation, and real-time service recommendation applications.

-

By Deployment, Cloud dominated as the preferred AI deployment model enabling scalable compute access and rapid model update cycles; Cloud is simultaneously the fastest-growing deployment through expanding telecom cloud transformation and multi-cloud AI infrastructure adoption.

By Application: network optimization dominates, customer analytics grows alongside

Network Optimization retained the dominant application position in the AI in Telecommunication Market in 2025, reflecting the fundamental commercial priority that network performance quality and operational efficiency represent for telecom operators whose financial model depends on maximising revenue per unit of network investment. AI network optimisation encompasses a comprehensive range of applications from autonomous radio resource management adjusting antenna power, tilt, and beamforming parameters to maximise coverage quality, through traffic prediction and load balancing distributing user sessions across available network capacity to prevent congestion, to intelligent network slicing management allocating 5G network resources dynamically to enterprise slice customers based on real-time service level agreement monitoring.

Customer Analytics represents a rapidly growing application segment, driven by the telecom industry's recognition that AI-powered customer intelligence provides the single most powerful lever for improving the key financial metrics of subscriber lifetime value, churn rate, and ARPU that determine telecom operator profitability. AI customer analytics platforms that predict churn with 85 to 90% accuracy enable targeted retention investment on the specific subscribers at highest risk of defection, dramatically improving retention programme cost-effectiveness relative to broad offer discounts applied to the entire subscriber base.

By Deployment: Cloud deployment dominates and grows fastest due to scalability, flexibility, and lower infrastructure costs.

Cloud deployment retained the dominant position in the AI in Telecommunication Market in 2025 and is simultaneously the fastest-growing deployment mode, reflecting the ideal alignment between cloud computing's scalable, elastic compute infrastructure and the AI workload characteristics of telecom network intelligence applications that require high-performance processing for model training, rapid model deployment across distributed network management systems, and continuous real-time inference at the speed that network optimisation and fraud detection applications require. Cloud-based AI platforms provide telecom operators with access to the latest AI model architectures and training infrastructure without capital investment in dedicated AI servers, enabling smaller and mid-size operators to access enterprise-grade AI capabilities that were previously economically accessible only to the largest global telecom companies.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

~82% |

|

Europe |

United Kingdom |

~27% |

|

Asia Pacific |

China |

~45% |

|

Middle East & Africa |

UAE |

~28% |

|

Latin America |

Brazil |

~43% |

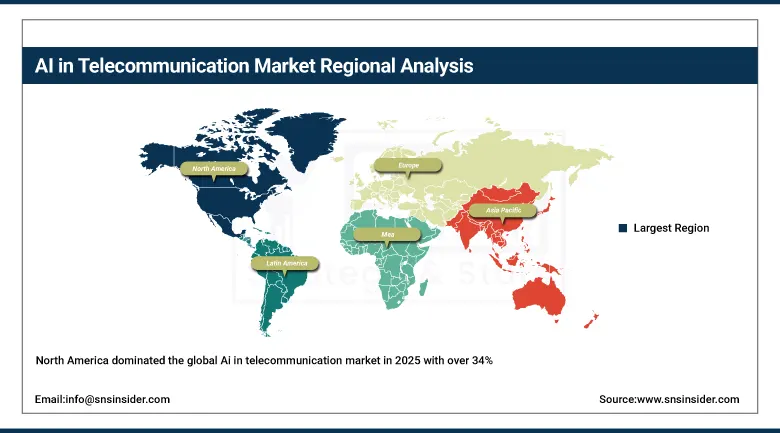

North America AI in Telecommunication Market Insights

North America dominated the global Ai in telecommunication market in 2025 with over 34% of global revenues, led by the United States at approximately 82% of North American revenues. U.S. market leadership is sustained by the world's most technically advanced 5G network deployments creating AI network management necessity, the largest enterprise telecom AI technology vendor ecosystem, and the most extensive operator AI deployment investment by AT&T, Verizon, and T-Mobile whose combined subscriber bases and network scales justify the largest per-operator AI investment programmes globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe AI in Telecommunication Market Insights

Europe represents a growing telecom AI market anchored by Deutsche Telekom's T-Systems AI network management programme, Vodafone's AI customer analytics platform, and Orange's AI-powered network operations that collectively represent the most active European telecom AI investment programmes. EU AI Act regulatory requirements for high-risk AI systems deployed in critical communications infrastructure are creating compliance investment that adds to the commercial AI adoption cost structure but simultaneously builds operator AI governance capability that supports sustainable long-term AI programme development.

Asia Pacific AI in Telecommunication Market Insights

Asia Pacific is projected to grow at the fastest regional CAGR, driven by China's world-leading 5G deployment with over 3 million 5G base stations creating the largest single national AI network management requirement globally, Japan's sophisticated telecom AI research ecosystem led by NTT and SoftBank, South Korea's AI telecom innovation at Samsung and SK Telecom, and India's rapidly expanding telecom digitalization investment as Jio and Airtel deploy AI at massive scale across India's enormous subscriber base.

Latin America and MEA AI in Telecommunication Market Insights

Latin America and MEA are growing telecom AI markets driven by network modernization investment and 5G rollout that creates AI management requirements across expanding network architectures. Brazil leads Latin American telecom AI through Claro and Vivo's network optimization programmes, while the UAE and Saudi Arabia's world-class 5G infrastructure investments by Etisalat and STC are creating advanced telecom AI deployment contexts in the Gulf's premium network markets.

Market Dynamics

Growth Drivers: 5G network complexity requiring AI-automated management and telecom industry opex reduction imperative driving AI adoption as structural operational necessity

The primary structural growth drivers for the AI in Telecommunication Market are the 5G network architecture's fundamental AI dependency for managing network slicing, massive MIMO, and edge computing resource allocation at the dynamic speeds that 5G service quality requires, combined with the telecom industry's structural operating cost reduction imperative that makes AI automation the primary financial lever for improving profitability in an industry where ARPU growth is limited by competitive pricing dynamics while network investment and operating costs continue escalating. The documented 90% telecom industry AI adoption rate confirms that AI in telecom has transitioned from competitive differentiation to operational survival requirement.

The combination of nearly 90% telecom AI adoption as of 2024 with 48% at experimentation stage and 41% at active deployment stage confirms that the AI in Telecom market is at the transition from early adoption to mainstream scaling that historically drives the most rapid market revenue growth phase. As operators move from isolated AI pilots to enterprise-wide AI platform deployment across network operations, customer management, and revenue assurance, the per-operator AI investment multiplies dramatically, sustaining the AI in Telecommunication Market's exceptional 42.94% CAGR through the 2026 to 2035 forecast period.

Restraints: Data privacy regulatory complexity limiting AI training data utilisation, high AI implementation integration cost with legacy network management systems, and AI model explainability challenges in regulated telecom environments

A significant restraint is the data privacy regulatory complexity under GDPR, CCPA, and equivalent national regulations that limits telecom operators' ability to utilise subscriber call records, location data, and service usage information for AI training without explicit consent or anonymisation processing that reduces the data volume and precision available for AI model development. Legacy network management system integration with modern AI platforms requires extensive API development, data pipeline construction, and operational process redesign that create multi-year implementation programmes with uncertain timelines and cost overruns that complicate the AI business case for risk-averse telecom operators.

Opportunities: 6G AI-native network architecture, telecom AI platform-as-a-service, and edge AI for ultra-low latency network applications

The 6G standardisation process, where AI-native network design is a foundational architectural principle rather than an overlay feature, creates the most structurally significant AI in telecom opportunity through the forecast period as 6G commercial deployments beginning around 2030 mandate AI integration at every network layer. Telecom AI platform-as-a-service offerings enabling smaller operators and MVNOs to access enterprise-grade AI network management and customer analytics capabilities at subscription cost structures compatible with their operating budgets represent a market democratization opportunity that substantially expands the total addressable market beyond the world's largest 50 telecom operators. Edge AI deployment co-located with 5G base stations enabling sub-millisecond AI inference for autonomous vehicle networks, industrial automation connectivity, and immersive XR applications creates a premium AI infrastructure service category commanding the highest per-compute-unit pricing in telecom AI.

Recent Developments:

-

2025: AT&T expanded its AI network operations platform deployment across its nationwide 5G network, with AI-automated radio resource management and predictive network maintenance programmes delivering documented reductions in network incidents and maintenance costs across its service territory.

-

2025: Ericsson launched its expanded AI-native network management software suite for 5G operators, providing autonomous network optimization, predictive maintenance, and energy efficiency management capabilities integrated with its RAN and core network management platforms.

-

2025: Nokia advanced its AVA AI network operations platform with enhanced large language model integration for natural language network management interface, enabling operator engineers to query network status and request optimization actions through conversational AI interaction rather than traditional command-line or GUI-based management tools.

AI in Telecommunication Market Key Players are:

-

IBM Corporation

-

Cisco Systems Inc.

-

Microsoft Corporation

-

NVIDIA Corporation

-

Amazon Web Services Inc.

-

Google LLC (Alphabet)

-

Ericsson AB

-

Nokia Corporation

-

Huawei Technologies Co. Ltd.

-

ZTE Corporation

-

AT&T Inc.

-

Verizon Communications Inc.

-

T-Mobile US Inc.

-

SAP SE

-

Amdocs Ltd.

-

Subex Ltd.

-

Cognizant Technology Solutions Corporation

-

Accenture plc

-

Infosys Ltd.

-

Mavenir Systems Inc.

AI in Telecommunication Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.31 Billion |

| Market Size by 2035 | USD 189.16 Billion |

| CAGR | CAGR of 42.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Technology (Machine Learning, Natural Language Processing, Computer Vision, Context-Aware Computing, Others) • By Application (Network Optimization, Customer Analytics, Virtual Assistance, Fraud Detection, Network Security, Predictive Maintenance, Others) • By Deployment (Cloud, On-Premises) • By End-User (Telecom Operators, Enterprises, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Cisco Systems Inc., Microsoft Corporation, NVIDIA Corporation, Amazon Web Services Inc., Google LLC (Alphabet), Ericsson AB, Nokia Corporation, Huawei Technologies Co. Ltd., ZTE Corporation, AT&T Inc., Verizon Communications Inc., T-Mobile US Inc., SAP SE, Amdocs Ltd., Subex Ltd., Cognizant Technology Solutions Corporation, Accenture plc, Infosys Ltd., and Mavenir Systems Inc. |

Frequently Asked Questions

Ans: North America dominated with over 34% of global revenues in 2025, led by the United States at approximately 82% of North American revenues.

Ans: Cloud deployment dominated and is simultaneously the fastest-growing mode, reflecting the ideal alignment between cloud computing's scalable elastic compute infrastructure and telecom AI workload requirements for high-performance model training.

Ans: The AI in Telecommunication Market was valued at USD 5.312 billion in 2025.

Ans: The AI in Telecommunication Market is expected to grow at a CAGR of 42.94% from 2026 to 2035.

Ans: The 5G network architecture's fundamental dependency on AI-automated management for network slicing, massive MIMO, and edge computing resource allocation, combined with the telecom industry's structural operating cost reduction imperative making AI automation the primary financial lever for profitability improvement.

Get in Touch