IoT in Product Development Market Report Scope & Overview:

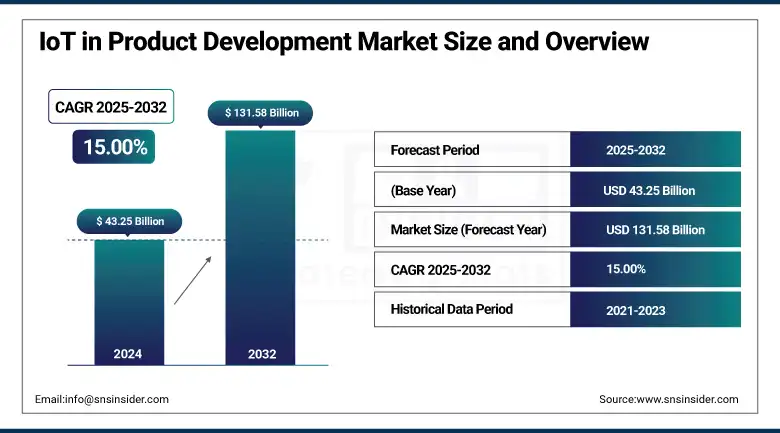

IoT in product development market size was valued at USD 43.25 billion in 2024 and is expected to reach USD 131.58 billion by 2032, growing at a CAGR of 15.00% over 2025-2032.

IoT in product development market growth is propelled by the surging requirement for smart and connected products in different industries. Developments in IoT technologies, such as 5G, AI, and machine learning improve product capabilities to be more intelligent and automated. Businesses also welcome IoT to improve efficiency, reduce costs, and deliver personalized customer experiences. Growing trends toward smart homes, automation in the industry, and wearables additionally increase the market size, leading to enhanced growth with high demand for product development via IoT integration.

To Get more information On IoT in Product Development Market - Request Free Sample Report

For instance, Cognizant introduced an Industrial IoT platform, which integrated over 100 facilities and 1,000+ machines with a goal of USD 100+ million in cost savings, along with profitability advantages within five years.

According to a survey conducted by Capgemini indicated that 65% of customers would involve one interface to access all the connected products, underscoring the criticality of data protection and interoperability in IoT solutions.

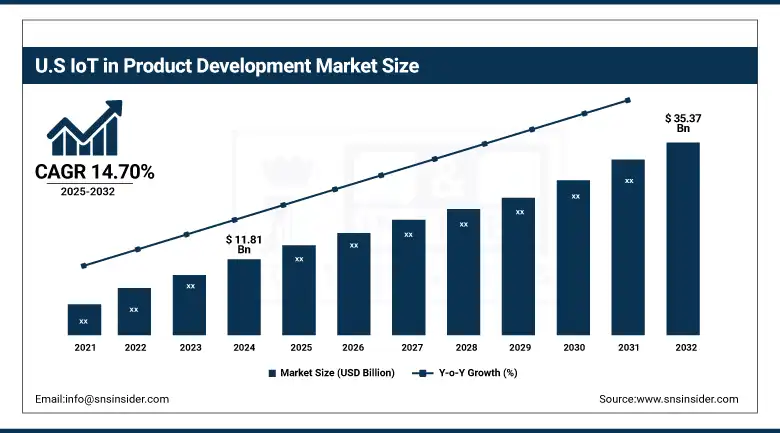

The U.S. IoT in product development market size was valued at USD 11.81 billion in 2024 and is projected to reach a valuation of USD 35.37 billion by 2032, expanding at a CAGR of 14.70% over the 2025-2032.

The U.S. IoT in product development market growth is driven by the surging utilization of internet-connected devices in many sectors, such as automobile, healthcare, and manufacturing. The growth of IoT products is fueled by the surge of 5G, AI, and cloud computing. Moreover, businesses are adopting IoT to automate operations, reduce expenditure, and provide personalized customer experience, thereby propelling the market.

The average U.S. household with internet access had 17 connected devices in 2023. The U.S.-based telecommunication giants such as AT&T and T-Mobile are planning to offer devices that use RedCap, a 5G specification designed for IoT devices. This development will enable effective connectivity for wearables, sensors, and security equipment.

IoT in Product Development Market Dynamics:

Drivers:

-

Increasing Consumer Need for Intelligent and Networked Products across various Application Segments is Driving IoT-Focused Product Development Initiatives

Consumer demand is rapidly changing to smart, connected products, which is propelling IoT-enabled product development across sectors, such as consumer electronics, healthcare, automotive, and industrial. Smart homes, wearables, and intelligent appliances are going mainstream, addressing the user needs for convenience and automation. These products help manufacturers accumulate useful information for future innovation. As ecosystems expand for the internet of things, developers must focus on integration, interoperability, and user-centered design. This creates the demand for IoT platform investment, positioning IoT as a key cornerstone for future product strategies.

According to research, annual shipments of wireless devices for industrial automation applications are expected to increase from 10.7 million units in 2023. Furthermore, the IoT devices are projected to generate 73.1 zettabytes of data per annum, necessitating robust cloud and edge computing solutions.

Restraints:

-

Enduring Data Security Threats and Regulatory Uncertainty are Constraining Confidence in Large-Scale IoT Product Development and Market Penetration

Security flaws in IoT devices expose critical risks, particularly for those products that manage sensitive information. Unpatched software, exposed interfaces, and weak encryption represent potential vulnerabilities to attackers. The focus on consumption of security have been ramped up due to breaking news of data breaches, targeted hacking, and the public becoming more aware of the same. Further complexities arise due to the fast-changing global data protection laws that drive up the cost of compliance and expose companies to more legal vulnerabilities. Until such security and compliance issues are resolved through collaborative models, supported by enhanced open standards and compliance, businesses will be reluctant to implement IoT solutions in volume.

According to research, approximately 25% of IoT devices are vulnerable to attacks, highlighting the need for enhanced cybersecurity measures. IoT-related security breaches are increasing by 18% annually, emphasizing the importance of investing in secure IoT infrastructures.

Opportunities:

-

Smart Cities and Urban Infrastructure Projects Abundance is Driving Government and Private Sector Demand for Product Solutions Based on IoT

Gigantic opportunities for IoT product innovation exist in transportation, utilities, waste management, and public safety in smart cities. The age of the connected citizen, along with governments and city planners are looking for connected solutions, which makes them more sustainable, citizen-centric, and efficient, further creating the demand for IoT devices including air quality sensors, smart streetlights, connected vehicles, and smart meters. Developers can benefit by partnering with municipalities and technology companies to develop end-to-end solutions. While cities extend their investments in digital infrastructure to push urban life through IoT devices, as per the initial estimates there will be a heightened need for safe, modular IoT devices.

Capgemini's study shows that citizens who participated in smart city programs are more satisfied with city living, especially concerning health-related items, such as air quality. Still, data privacy is of high concern, with 63% of global citizens giving priority to personal data privacy over better urban services.

For instance, Wipro launched IoT solutions for connected and smart indoor and outdoor lighting, bridging IoT and big data. Partnerships with organizations, such as Cisco are made to offer energy-efficient and people-centric lighting solutions for industries including smart cities.

Challenges:

-

Interoperability and Standards Fragmentation Across Devices and Platforms are Hampering Seamless IoT Integration in Product Development Cycles

The absence of cross-industry standards while developing the IoT products leads to issues regarding interoperability in devices from various manufacturers caused by incompatible data structures and protocols. This fragmentation heightens the cost and complexity of development with middleware and special integrations required. Developers make use of proprietary solutions, and thus scalability and reach to market is constrained. With no common communication frameworks, time-to-market suffers, innovation diminishes, and developing smooth multi-vendor environments becomes problematic. While customer demands increase for interoperable products, the absence of harmonized standards is one of the biggest hurdles to seamless and scalable integration of IoT products.

For instance, Infosys has adjusted its revenue guidance for FY24 to 1-2.5%, down from the earlier 1-3.5%, citing weak decision-making and deal ramp-ups. This indicates a cautious approach toward IoT investments amid integration challenges.

Similarly, HCL Technologies reduced its growth guidance to 5-6% for FY24 from the previously projected 6-8%. This adjustment reflects the broader industry trend of tempered expectations in IoT integration progress.

IoT in Product Development Market Segmentation Analysis:

By Service Type

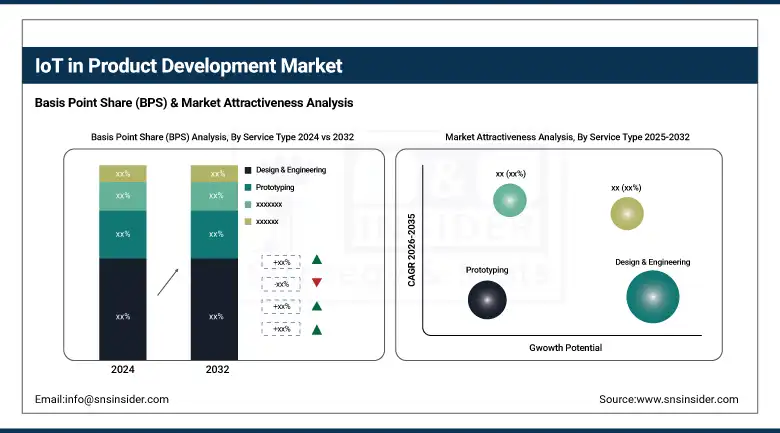

Design & Engineering segment led the IoT in product development market in 2024 with a 38% revenue share as it was so instrumental in designing IoT capability. Companies were more interested in smart product design to enable connectivity, data transfer, and remote control from the very beginning. Early-stage alignment with IoT architecture greatly impacted product viability, lifecycle efficiency, and speed to market and therefore was at the heart of development investment.

Prototyping is anticipated to expand at the fastest rate of 17.61% CAGR over 2025-2032 due to the necessity for real-time iterative product testing. Prototyping solutions that are IoT-enabled offer rapid feedback cycles, allowing developers to experiment with networked features, enhance performance, and reduce time-to-market. Growing numbers of intelligent devices across industries and emphasis on agile development methodologies have also fueled the need for IoT-enabled dynamic prototyping environments.

By Component

Hardware segment dominated the IoT in product development market in 2024 with 45% share in terms of revenue since IoT is still concentrated on physical products. Demand for sensors, embedded systems, and connectivity modules increased since firms had been eager to implement real-time data capability within products. Hardware's irreplaceable role in facilitating data acquisition, processing, and edge computing still grounds its leadership in the IoT value chain.

Software segment is expected to grow at the fastest CAGR of 16.57% during 2025-2032, fueled by the expanding role of analytics, automation, and interoperability across IoT systems. As products are making themselves smarter and interconnected, software platforms spanning from firmware to cloud analytics are necessary for device management, security, and real-time insights. This move toward intelligence-based product capability supports the swift growth in software investments.

By End-Use

Manufacturing dominated the IoT in product development market share in 2024 with a 28%, driven by leveraging smart technologies widespread with applications to increase operational efficiency and minimize downtime. Predictive maintenance, real-time asset tracking, and automated quality control are now at the core of all advanced manufacturing plants courtesy of IoT-based solutions. The industry's robust emphasis on Industry 4.0 and infusion of IoT in product and process design entrenched its market leadership.

Healthcare is anticipated to expand at the highest CAGR of 17.67% during 2025-2032, owing to growing demand for connected medical devices, remote patient monitoring solutions, and, personalized patient care. IoT in healthcare enables timely diagnosis, accurate data accumulation, and improved clinical decision support. Due to the growing demographics of an elderly society, higher chronic disease prevalence, and the changing regulations surrounding digital health, the momentum of IoT adoption within the health sector is driving transformation both in the way care is delivered and in how medical products are innovated.

Regional Analysis:

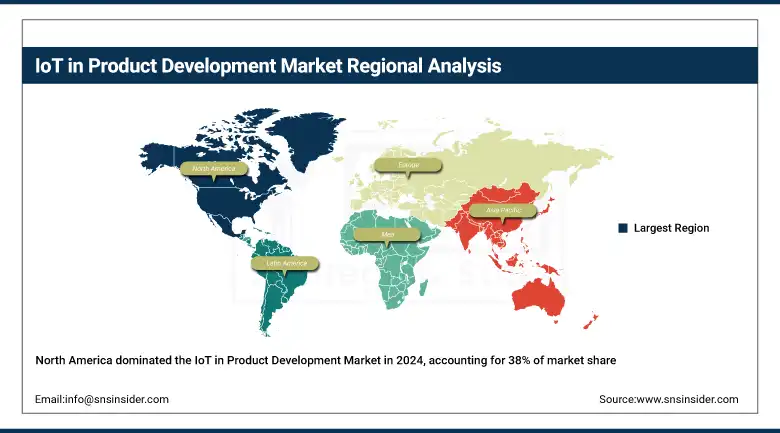

North America led the IoT in product development market in 2024 with 38% revenue, benefitting from its breed of technology ecosystem and vast landscape of elite IoT innovators. Significant R&D investment, fast adoption of many emerging manufacturing technologies, and complex regulatory frameworks have enabled product IoT capabilities to move faster than have been seen in many other industries. While tech unicorns and startups have achieved regional ubiquity, a high-intensity climate for IoT-fueled innovation has emerged. The U.S. dominates the IoT in Product Development Market due to advanced infrastructure, strong R&D investment, tech-driven enterprises, and early adoption across industrial and consumer sectors.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is expected to grow at the fastest CAGR of 17.48% over the forecast period, driven by rapid industrialization, increased demand for consumer electronics, and smart infrastructure development led by governments. China, India, and South Korea are investing heavily in IoT technologies to facilitate digital transformation in manufacturing, healthcare, and urbanization. The region has a huge talent pool, cheap production, and increasing startup activity, further driving its growth curve.

China dominates the IoT in product development market trend due to strong government backing, advanced manufacturing, large-scale IoT adoption, tech innovation, and smart infrastructure investments.

Europe is well represented in the IoT in product development market owing to its emphasis on Industry 4.0, high regulatory standards, innovation-led economies, robust automotive, and industrial bases, and favorable digital transformation policies in member states. Germany dominates the IoT in product development market due to Industry 4.0 leadership, strong manufacturing, advanced automation, and significant industrial IoT investments.

The Middle East & Africa and Latin America have a presence in the IoT in product development market due to the increasing smart city projects, industrial automation growth, connectivity escalation, and initiatives by the government to accelerate digital transformation and innovation.

Key Players:

IoT in product development market companies include N-iX, CHI Software, DataArt, Syberry, iTechArt Group, Provectus, Transition Technologies PSC, Softeq, ITRex Group, Yalantis, Cognizant Technology Solutions, Tata Consultancy Services (TCS), Capgemini, Accenture, Wipro, HCL Technologies, Persistent Systems, Luxoft, EPAM Systems, and Infosys.

Recent Developments:

-

June 2024, Wipro partnered with Siemens to integrate PAVE360 digital twin technologies, aiming to accelerate automotive software development and validation through enhanced engineering and simulation capabilities.

-

August 2024, Wipro expanded its collaboration with Dell Technologies to launch an AI-Ready Platform, combining Dell’s AI Factory and NVIDIA tools for scalable enterprise AI solutions.

-

July 2024, Cognizant unveiled the Neuro Edge platform, enabling real-time AI processing at the edge to improve decision-making in healthcare, manufacturing, and automotive industries.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 43.25 Billion |

| Market Size by 2032 | USD 131.58 Billion |

| CAGR | CAGR of 15.00% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Design & Engineering, Connected Hardware & Firmware Development, Prototyping, Manufacturing Support) • By Component (Hardware, Software, Services) • By End Use (Manufacturing, Automotive, Healthcare, Consumer Electronics, Aerospace & Defense, Energy & Utilities, BFSI, IT & Telecommunication) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | N-iX, CHI Software, DataArt, Syberry, iTechArt Group, Provectus, Transition Technologies PSC, Softeq, ITRex Group, Yalantis |

Frequently Asked Questions

North America held the largest share, accounting for 38% of the market revenue in 2024.

Manufacturing led with a 28% revenue share, driven by the adoption of IoT for operational efficiency.

Design & Engineering led with a 38% revenue share due to its critical role in IoT integration.

Smart cities are driving demand for IoT solutions in urban infrastructure, creating opportunities for product developers.

IoT in Product Development Market was valued at USD 43.25 billion in 2024 and is expected to reach USD 131.58 billion by 2032, growing at a CAGR of 15.00% from 2025-2032.

Get in Touch