Alkaline Water Electrolysis Market Report Scope & Overview:

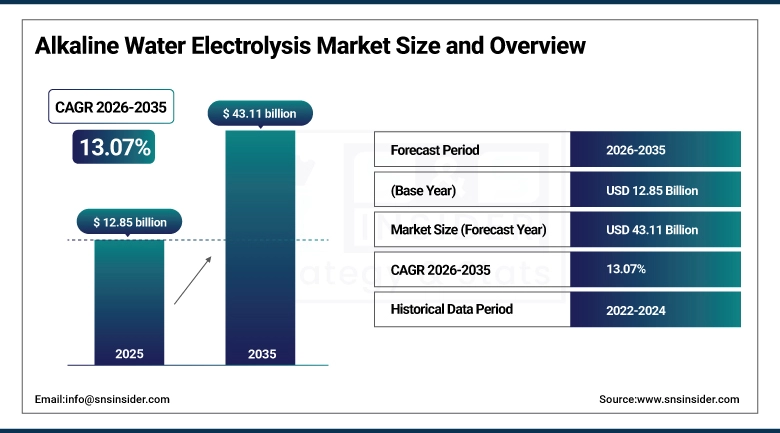

The Alkaline Water Electrolysis Market size was valued at USD 12.85 Billion in 2025 and is projected to reach USD 43.11 Billion by 2035, growing at a CAGR of 13.07% during the forecast period 2026–2035.

The Alkaline Water Electrolysis Market report includes an in-depth analysis of market dynamics, technology developments, and application market trends. Increasing demand for green hydrogen, industrial decarbonization projects, and increasing adoption in renewable energy systems are driving the market growth at a robust pace in 2026-2035.

Global alkaline electrolyzer capacity exceeded multiple gigawatts in 2025 due to large-scale industrial projects and increasing adoption in transportation and utility-scale renewable energy hubs.

Alkaline Water Electrolysis Market Size and Forecast:

-

Market Size in 2025: USD 12.85 Billion

-

Market Size by 2035: USD 43.11 Billion

-

CAGR: 13.07% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Alkaline Water Electrolysis Market - Request Free Sample Report

Alkaline Water Electrolysis Market Trends:

-

A transition to pressurized and advanced alkaline electrolyzers to boost efficiency.

-

Significant government subsidies and regulations (EU Green Deal, Indian National Hydrogen Mission, US IRA credits).

-

Rise in private sector funding and joint ventures between electrolyzer makers and energy companies.

-

A growth trend in the use of alkaline-based electrolyzers powered by renewable energy sources like solar, wind, hydro.

-

A growth trend in the use of alkaline-based electrolyzers powered by renewable energy sources like solar, wind, hydro.

-

There is push to create next-generation catalysts like nickel, cobalt, iron-based alloys to enhance efficiency.

-

There is trend towards retrofitting existing hydrogen plants with alkaline-based systems to enhance accessibility.

U.S. Alkaline Water Electrolysis Market Insights:

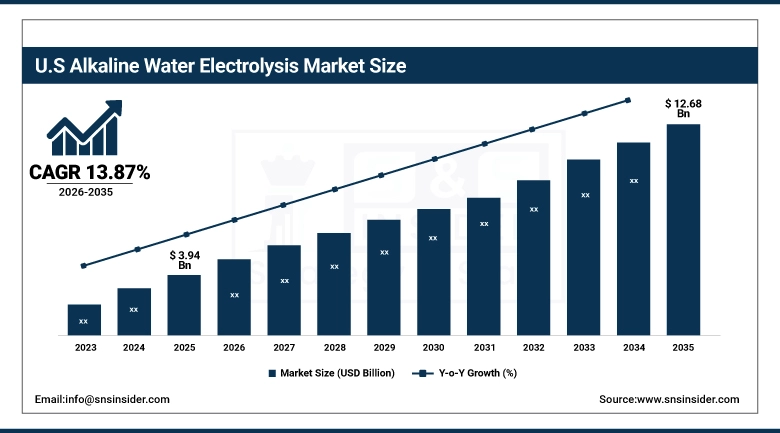

The U.S. Alkaline Water Electrolysis Market is expected to grow from USD 3.94 Billion in 2025 to approximately USD 12.68 Billion by 2035, at a CAGR of 13.87%. The market has strong federal support through DOE-backed hydrogen hubs, federal tax credits through the Inflation Reduction Act, and growing demand from industry for chemicals, steel, and refining. The market has strong growth prospects with the rapid adoption of advanced pressurized alkaline electrolyzers, integration with renewable energy projects, and growth of hydrogen refueling infrastructure for mobility.

Alkaline Water Electrolysis Market Growth Drivers:

-

Rising global demand for green hydrogen and industrial decarbonization are key drivers of Alkaline Water Electrolysis Market growth.

Heavy industries such as steel plants, chemical plants, and fertilizers increasingly prefer to use alkaline electrolyzers. This is because they are cost-effective and mature. Government policies such as subsidies, tax credits, and hydrogen missions (EU Green Deal, US Inflation Reduction Act, India’s National Green Hydrogen Mission) are boosting the adoption of alkaline electrolyzers.

More than 55% of industrial hydrogen projects worldwide employed alkaline electrolyzers in 2025.

Alkaline Water Electrolysis Market Restraints:

-

High capital costs and operational challenges are key restraints of Alkaline Water Electrolysis Market growth.

The cost of investment for electrolyzer systems is relatively higher. The cost of maintenance is higher as well. The efficiency is relatively lower compared to PEM electrolysis. The response time is relatively slower. This makes it less suitable for applications that require flexibility, such as mobility.

More than 40% of hydrogen projects across the globe, as of 2025, have reported that high capital costs and efficiency limitations are major challenges to adopting alkaline electrolyzers.

Alkaline Water Electrolysis Market Opportunities:

-

Rising global investments in green hydrogen infrastructure and renewable integration are creating significant opportunities for the Alkaline Water Electrolysis Market.

Emerging economies like India, the Middle East, and South America are driving the growth in this sector with cost advantages and government support. The hydrogen fueling infrastructure and mobility sector is expected to show promising growth, especially with the increase in fuel cell vehicles. The technological developments in pressurized alkaline electrolyzers, advanced catalysts, and monitoring have created opportunities to increase efficiency, even to gigawatt scales.

By 2030, over 50% of hydrogen mobility projects in the world are expected to include alkaline electrolyzers, making transportation one of the fastest-growing sectors in terms of opportunity, apart from regional dynamics.

Alkaline Water Electrolysis Market Segmentation Analysis:

-

By Application, Power Generation & Industrial Use (steel, chemicals, refineries) held the largest market share of 47.46% in 2025, while Transportation (fuel cells, mobility) are expected to grow at the fastest CAGR of 16.87% during 2026–2035.

-

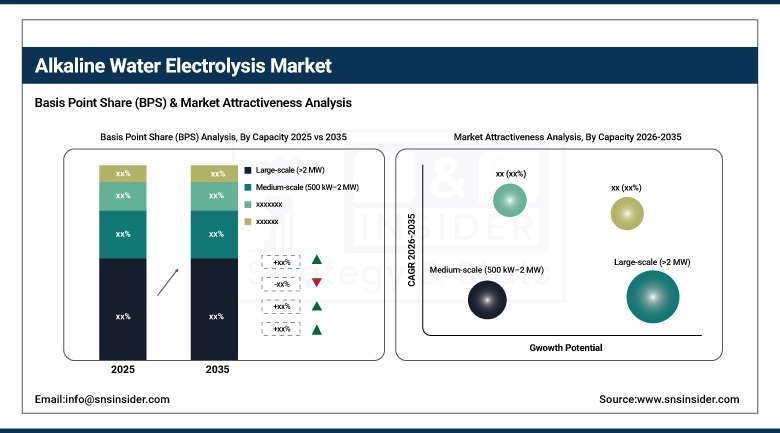

By Capacity, Large-scale (>2 MW) dominated with 56.55% market share in 2025, whereas Small-scale (<500 kW) are projected to record the fastest CAGR of 16.99% through 2026–2035.

-

By technology Type, Traditional Alkaline Electrolyzers (liquid electrolyte) accounted for the highest market share of 66.12% in 2025, while Advanced Alkaline Electrolyzers (pressurized, improved efficiency) are expected to grow at the fastest CAGR of 15.71% during the forecast period.

-

By Installation Type, On-site Industrial Installations dominated with a 58.72% share in 2025, while Utility-scale Renewable Integration (solar, wind, hydro) are anticipated to expand at the fastest CAGR of 16.64 % through 2026–2035.

-

By End User, Industrial (steel, chemicals, fertilizers) held the largest share of 56.34% in 2025, while Transportation & Mobility Providers are expected to grow at the fastest CAGR of 18.64% during the forecast period.

By Application, Power Generation & Industrial Use Dominate While Transportation Grows Rapidly:

The Power Generation & Industrial Use (Steel, Chemicals, Refineries) segment is the largest in the Market, given the importance of this segment in the fight against climate change, where industries like steel, chemicals, and refineries are key targets. In 2025, industrial hydrogen projects represented over 55 percent of global alkaline electrolyzer deployments, underscoring the preference of industrial actors to deploy cost-effective, proven technology with large-scale potential.

The Transportation (fuel cells, mobility) segment is growing at the fastest rate, primarily due to the growing trend of hydrogen fuel cell vehicles, buses, and heavy-duty trucks, in addition to hydrogen fuel cell infrastructure. The segment saw a surge in adoption in 2025, with transportation-related deployments, mainly in North America and Europe, where hydrogen mobility initiatives are being supported by governments to accelerate penetration.

By Capacity, Large-scale (>2 MW) Projects Dominate While Small-scale (<500 kW) Grows Rapidly:

The Large-scale (>2 MW) segment has the dominant Market Share within the Market due to its inherent importance to industrial hydrogen production for steel, chemicals, and refinery applications. Large-scale installations accounted for more than 60% of global capacity in 2025, as industrial operators prefer this technology due to its maturity, cost-effectiveness, and ability to produce hydrogen at scale.

The Small-scale (<500 kW) segment is growing at a fastest rate due to growing energy needs for distributed hydrogen production. This segment has witnessed a huge uptake in North America and Europe as commercial entities, microgrids, and hydrogen refueling stations are integrating small-scale electrolyzer technologies.

By Technology Type, Traditional Alkaline Electrolyzers Dominate While Advanced Alkaline Electrolyzers Grow Rapidly:

The Traditional Alkaline Electrolyzers (liquid electrolyte) segment holds a larger share in the Market due to its maturity, reliability, and cost-effectiveness in large-scale hydrogen production. In 2035, traditional systems accounted for more than 80% of global installations due to the strong preference among industrial operators for traditional systems with decades of operational experience.

The Advanced Alkaline Electrolyzer segment recorded the fastest growth in 2025, driven by its suitability for projects requiring flexible operations, higher hydrogen purity, and reduced operating costs. In addition, the segment benefited from increasing adoption in renewable energy integration projects, where efficiency and scalability are critical for large-scale green hydrogen production.

By Installation Type, On-site Industrial Installations Dominate While Utility-scale Renewable Integration Grows Rapidly:

The On-site Industrial Installations segment holds the dominant share of the Alkaline Water Electrolysis Market, as this type of installation is common in heavy industries like steel, chemical, and refinery plants. This type of installation indicates a strong preference among operators of these heavy industries for a cost-effective method of hydrogen production.

The Utility-scale Renewable Integration, including solar, wind, and hydro, is fastest growing market share of the growing Alkaline Water Electrolysis Market, as there has been a strong uptake of this type of installation, especially during 2025, with a focus on utility-scale projects, especially in Europe and North America, which have a high presence of renewable energy hubs.

By End User, Industrial Applications Dominate While Transportation & Mobility Providers Grow Rapidly:

The Industrial segment (Steel, Chemicals, Fertilizers) is the dominant market leader in the Alkaline Water Electrolysis Market due to their existing involvement in hydrogen production and decarbonization of heavy industries. With the passage of time, it will continue to reflect the strong reliance of industrial operations on alkaline electrolysis for cost-effective hydrogen production solutions that are integrated into industrial operations.

The Transportation & Mobility Providers segment is the fastest-growing segment of the market due to the increased adoption of hydrogen-fueled vehicles, buses, and heavy-duty trucks. Adoption is seen in more advanced countries where government-supported hydrogen mobility projects are driving market penetration.

Alkaline Water Electrolysis Market Regional Analysis:

Asia-Pacific Alkaline Water Electrolysis Market Insights:

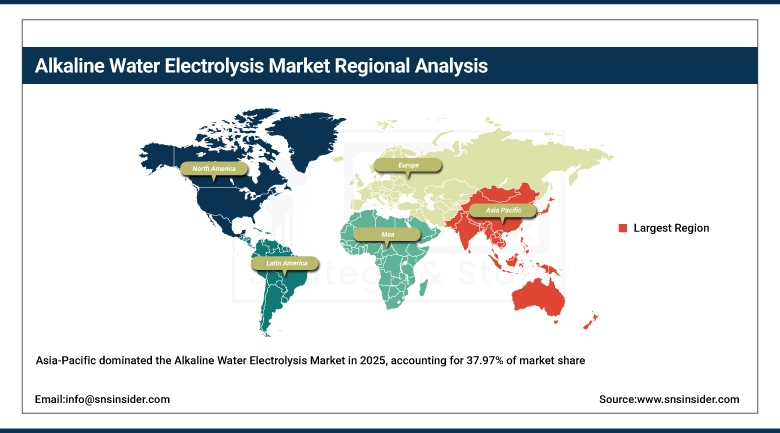

The Asia-Pacific market has dominated the global market with 37.97% market share in 2025, holding the highest market share. The region has witnessed rapid industrialization, favorable hydrogen policy from governments, and massive renewable energy integration schemes. The countries in the region, including China, Japan, South Korea, and India, have been at the forefront in the adoption of alkaline electrolysis technology, especially in heavy industries.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Alkaline Water Electrolysis Market Insights:

The largest contributor comes from Asia-Pacific, mainly because of aggressive decarbonization policies, rapid growth rates in renewable energy sources, and strong industry needs. In 2025, the majority of Asia-Pacific installations come from China, which is backed by hydrogen development initiatives and large industry deployments. The leadership position is backed by manufacturing capabilities within China, cost competitiveness, and the integration of alkaline electrolyzers with steel and chemical plants.

North America Alkaline Water Electrolysis Market Insights:

North America Alkaline Water Electrolysis Market is the fastest growing market with CAGR of 11.14%, led by strong federal backing in the form of hydrogen hub schemes in the U.S. and Canada’s renewable energy schemes. Industrial sector users in the steel, chemical, and refinery sectors are key markets, aided by existing infrastructure and cost-effective implementation models. Ongoing investment in advanced pressurized alkaline technology, alongside strategic partnerships between original equipment manufacturers and energy sector players, reinforces the region's pre-eminence.

U.S. Alkaline Water Electrolysis Market Insights:

The driving factors behind the U.S. Alkaline Water Electrolysis Market are large-scale hydrogen hub developments, strong industrial demand, and growing transportation sector applications. The key industry players in this market are Cummins, Plug Power, and Ballard Power Systems, which are utilizing federal funding and private sector investments to increase production capacities. The growing use of advanced alkaline electrolyzers in industrial hydrogen developments, hydrogen fueling infrastructure, and integration with renewable energy sources.

Europe Alkaline Water Electrolysis Market Insights:

The Europe Alkaline Water Electrolysis Market is a key region in the global market, accounting for a substantial share in 2025, owing to the robust support from policies like the EU Green Deal, in addition to massive renewable energy integration schemes. Industrial sectors like steel, chemical, and refinery industries are key markets, with support coming from European countries’ commitment to achieving a low-carbon economy. Ongoing innovations in advanced technology, in addition to robust partnerships between governments, OEMs, and energy companies, have helped this region solidify its position in the global market.

Germany Alkaline Water Electrolysis Market Insights:

Germany is the largest contributor in the European region, driven by its aggressive climate policy, high industrial demand, and its position as a leader in integrating renewables. In 2025, Germany will be a major contributor in the European region, driven by its high installed base, hydrogen strategies, and high industrial base. Germany’s position as a leader is further driven by its high industrial base, R&D, and integration of alkaline electrolyzers in its steel and chemical industries.

Latin America Alkaline Water Electrolysis Market Insights:

The Latin America alkaline water electrolysis market is growing as a lucrative market due to the increasing investment in renewable energy schemes. Brazil, Chile, and Mexico are at the forefront of the Latin American alkaline water electrolysis market. These countries have an advantage due to the availability of considerable solar and wind power, enabling the use of green hydrogen at a lower cost. Industries such as chemicals, fertilizers, and refineries are utilizing alkaline water electrolysis to reduce greenhouse gas emissions. Hydrogen refueling station projects are also gaining momentum.

Middle East & Africa Alkaline Water Electrolysis Market Insights:

The Middle East & Africa Alkaline Water Electrolysis Market is witnessing growth as a strategic market due to the availability of renewable energy resources and ambitious national hydrogen strategies. Saudi Arabia, the UAE, and South Africa are at the forefront of adoption, backed by large-scale solar and wind power projects that make green hydrogen production extremely cost-competitive. Chemicals, fertilizers, and refining industries are incorporating alkaline electrolyzers to achieve decarbonization objectives, with export-focused hydrogen projects aiming to make the region a global supplier of clean energy.

Alkaline Water Electrolysis Market Competitive Landscape:

Nel Hydrogen is a major Norwegian company that has specialized in the field of electrolyzer technology, with a strong position in the alkaline water electrolysis business. The company has a range of products, including large-scale alkaline electrolyzers, which are used for industrial hydrogen production, power-to-gas, and renewable energy integration. The company has a strong focus on cost-efficient solutions, with decades of operating history and global presence.

-

In 2025, Nel announced expansion of its Herøya facility to increase electrolyzer production capacity, reinforcing its role as a dominant supplier in Europe and Asia.

Siemens Energy, based out of Germany, is a significant global energy technology company that plays an important role in the alkaline water electrolysis industry. Siemens Energy combines electrolyzers with large-scale hydrogen-based projects to facilitate decarbonization within industries, mobility, and power. Siemens Energy’s competitive advantage comes from their engineering capabilities, global presence, and turnkey hydrogen solutions.

-

In 2025, Siemens Energy advanced its green hydrogen initiatives by deploying electrolyzers in European hydrogen hubs, aligning with EU climate targets and strengthening its leadership in integrated hydrogen systems.

Cummins Inc. is a US-based company that is a global leader in power solutions. It has been growing at a rapid pace in hydrogen technology solutions as well, including alkaline water electrolysis technology. With the acquisition of Hydrogenics Corporation, it is offering both PEM and alkaline technologies to customers in the growing hydrogen market in North America. It is using its scale advantages to provide reliable solutions to customers through its strong investments in research and development.

-

In 2025, Cummins scaled up electrolyzer production in North America to meet demand from DOE-funded hydrogen hub projects, reinforcing its role as the fastest-growing supplier in the U.S. and Canada.

Alkaline Water Electrolysis Market Key Players:

-

Nel Hydrogen

-

Cummins Inc.

-

ITM Power

-

McPhy Energy

-

Thyssenkrupp AG

-

Hydrogenics

-

Toshiba Energy Systems & Solutions

-

Plug Power Inc.

-

Ballard Power Systems

-

Asahi Kasei Corporation

-

Teledyne Energy Systems

-

Electrochaea GmbH

-

Green Hydrogen Systems

-

Enapter AG

-

Haldor Topsoe (Topsoe A/S)

-

Linde plc

-

Sunfire GmbH

-

HydrogenPro ASA

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.85 Billion |

| Market Size by 2035 | USD 43.11 Billion |

| CAGR | CAGR of 13.07% From 2026 to 2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Power Generation & Industrial Use (steel, chemicals, refineries), Energy Storage & Grid Balancing, Transportation (fuel cells, mobility), Others) • By Capacity (Large-scale (>2 MW), Medium-scale (500 kW–2 MW), Small-scale (<500 kW), Others) • By Technology Type (Traditional Alkaline Electrolyzers (liquid electrolyte), Advanced Alkaline Electrolyzers (pressurized, improved efficiency), Hybrid/Next-gen Alkaline Systems, Others) • By Installation Type (On-site Industrial Installations, Utility-scale Renewable Integration (solar, wind, hydro), Distributed/Small-scale Installations (commercial, pilot projects), Others) • By End User (Industrial (steel, chemicals, fertilizers), Utilities & Energy Companies, Transportation & Mobility Providers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nel Hydrogen, Siemens Energy, Cummins Inc., ITM Power, McPhy Energy, Thyssenkrupp AG, Hydrogenics, Toshiba Energy Systems & Solutions, Plug Power Inc., Ballard Power Systems, Asahi Kasei Corporation, Teledyne Energy Systems, Electrochaea GmbH, Green Hydrogen Systems, Enapter AG, Haldor Topsoe (Topsoe A/S), Air Liquide, Linde plc, Sunfire GmbH HydrogenPro ASA. |

Frequently Asked Questions

Asia-Pacific, led by China, dominates global adoption, while North America is the fastest-growing region due to federal hydrogen hub initiatives and private sector investments.

Traditional alkaline electrolyzers (liquid electrolyte) currently dominate due to maturity and cost-effectiveness.

High capital costs, lower efficiency compared to PEM electrolysis, water purity requirements, and supply chain constraints for catalyst materials are key challenges.

Power generation and industrial use (steel, chemicals, refineries) dominate the market 47.46% due to large-scale hydrogen demand, while transportation and mobility providers are the fastest-growing segment.

Rising demand for green hydrogen, strong government support through subsidies and hydrogen missions, and industrial decarbonization initiatives are the primary growth drivers.

Get in Touch