Aluminum Forging Market Report Scope & Overview:

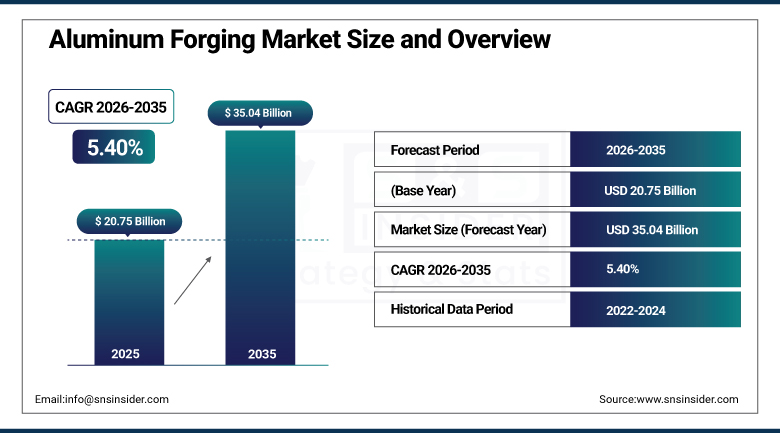

The Aluminum Forging Market was valued at USD 20.75 billion in 2025 and is expected to reach USD 35.04 billion by 2035, growing at a CAGR of 5.40% from 2026–2035.

The aluminum forging market is witnessing steady growth in the global market owing to increasing demand for lightweight and high-strength components. The growing need for fuel-efficient vehicles and advanced aerospace structures is promoting the usage of aluminum forgings across various industries. Investments made by automotive and aerospace manufacturers in advanced forging technologies are contributing to market growth. Increasing developments in industrial machinery and defense applications are playing a major role in driving demand for aluminum forgings. Growth in transportation infrastructure and stringent emission regulations are fueling the demand for aluminum forged components.

As per the U.S. Geological Survey Mineral Commodity 2025 and UN Environment, China produces 60% of primary aluminum globally, whereas secondary aluminum accounts for almost 33% of the total, due to the increasing circularity of materials used in industries. The global rate of aluminum recycling is above 90% for the automotive and construction end-use industry segments due to efficient recovery of scraps, thereby promoting more use of forged aluminum parts.

Market Size and Forecast:

-

Market Size 2026E: USD 21.83 billion

-

Market Size 2035: USD 35.04 billion

-

CAGR (2026 - 2035): 5.40%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Aluminum Forging Market- Request Free Sample Report

Aluminum Forging Market Trends:

-

Rapid adoption of lightweight aluminum forgings in electric vehicles increases structural weight reduction efficiency by nearly 18% globally

-

Automation and precision closed die forging lines expand production efficiency, reducing material waste rates by approximately 12%

-

Rising regulatory carbon reduction mandates drive shift toward recycled aluminum feedstock usage exceeding 40% in forging inputs

-

Advanced hot forging process optimization enabled 15 to 20% higher tensile strength components for aerospace applications globally

-

Digital twin simulation integration in forging plants improves defect detection accuracy rates by nearly 25% during production cycles

-

Government-backed investment programs increasing forging capacity expansion projects by over 30% across industrial manufacturing sectors

U.S. Aluminum Forging Market Size Outlook:

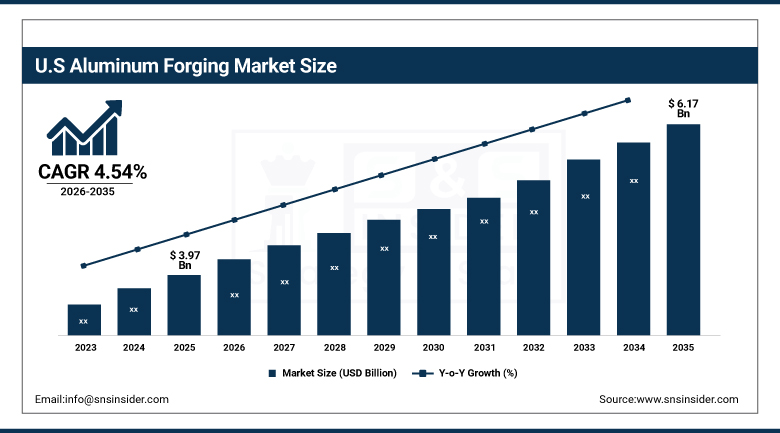

The U.S. Aluminum Forging Market was valued at USD 3.97 billion in 2025 and is expected to reach around USD 6.17 billion by 2035, growing at a CAGR of 4.54% from 2026–2035.

The U.S. aluminum forging market is growing consistently owing to increased demand in automotive and aerospace applications. The usage of aluminum forgings in lightweight vehicle structures, aircraft components, and defense equipment has contributed to market growth in a consistent manner. Increased spending in the development of advanced manufacturing facilities has generated an increase in demand for high-strength forged components. Development of transportation infrastructure, industrial machinery, and energy sector applications is further driving the demand for this product.

According to U.S. Geological Survey Mineral Commodity and U.S. Department of Energy data, the United States imports approximately 80% of its primary aluminum supply, reflecting limited domestic smelting capacity. Aluminum recycling reduces energy consumption by up to 95% compared with primary production. Secondary aluminum accounts for more than 30% of total U.S. aluminum supply, while manufacturing sector remains the largest end-use consuming over 40% of fabricated aluminum products.

Aluminum Forging Market Segment Analysis:

-

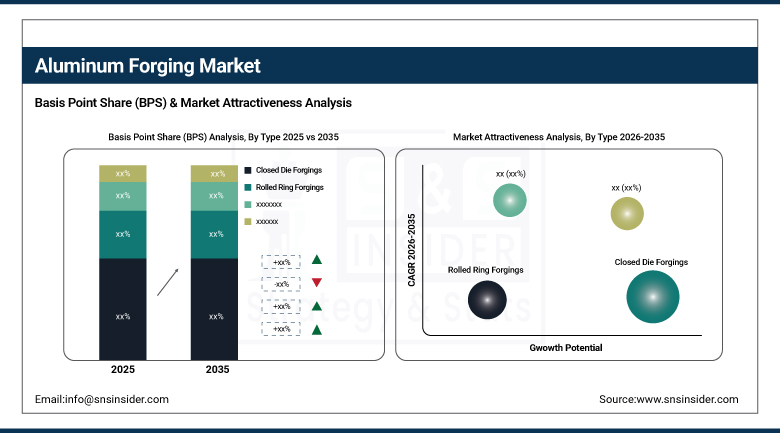

By Type, Closed Die Forgings dominated the Aluminum Forging Market with 44.78% share in 2025; while Rolled Ring Forgings is the fastest growing segment with CAGR of 7.43% during 2026 to 2035.

-

By End User, Automotive dominated the Aluminum Forging Market with 39.64% share in 2025; while Aerospace & Defense is the fastest growing segment with CAGR of 7.57% during 2026 to 2035.

-

By Alloy Type, Aluminum 6000 Series dominated the Aluminum Forging Market with 44.92% share in 2025; while Aluminum 7000 Series is the fastest growing segment with CAGR of 7.23% during 2026 to 2035.

-

By Forging Process, Hot Forging dominated the Aluminum Forging Market with 40.27% share in 2025; while Precision Forging is the fastest growing segment with CAGR of 8.60% during 2026 to 2035.

By Type, Closed Die Forgings dominated the Aluminum Forging Market, while Rolled Ring Forgings is the fastest growing segment.

Closed Die Forgings segment dominated the Aluminum Forging Market in terms of the highest revenue share in 2025. The main reason behind the dominance of this segment is the high precision and dimensional accuracy achieved while forging parts. Its popularity in automotive and aerospace industry is due to its cost-effectiveness and capability for mass-production. High demand for lightweight parts and uniform properties also help in the dominance of this segment.

Rolled Ring Forgings segment is anticipated to witness fastest CAGR during 2026 to 2035. High strength components that have great fatigue resistance and perform well even in extreme environments are required in the aviation, defense, and energy sectors. Their application in turbines, pressure vessels, and bearings increase their demand. Advanced manufacturing operations and construction activities are driving the segment's growth.

By End User, Automotive dominated the Aluminum Forging Market, while Aerospace & Defense is the fastest growing segment.

Automotive sector had the dominated share of the Aluminum Forging Market in 2025 based on revenue generation. This can be attributed to an increase in demand for lightweight and fuel-efficient vehicles. The trend is facilitated by the increase in the use of electric vehicles and emission standards. Automotive companies heavily rely on forged components to add strength and durability to their cars and ensure that they withstand any crashes.

Aerospace & defense sector is set to witness the fastest growth rate between 2026 and 2035 due to several factors. These include the increase in aircraft production and modernization of the existing defense aircrafts. An increase in the demand for lightweight materials has contributed to the rise in the use of aluminum forgings in these applications. Commercial airlines and military organizations have made investments to stimulate this market.

By Alloy Type, Aluminum 6000 Series dominated the Aluminum Forging Market, while Aluminum 7000 Series is the fastest growing segment.

Aluminum 6000 Series segment held the dominated revenue share in the Aluminum Forging Market in 2025. The segment is mainly driven due to its excellent strength-to-weight ratio and corrosion resistance properties. It finds its wide application scope in automotive structural parts, industrial machinery, and transportation equipment. Its wide availability, low costs, and suitability for mass production have further contributed to its popularity.

Aluminum 7000 Series segment is poised to experience the fastest CAGR during 2026-2035. The growing demand for high strength material in aerospace and defense is anticipated to be driving market growth. This segment holds high tensile strength, making it fit for high-strength applications such as aircraft and aerospace equipment. Increased defense budget expenditure and the need for lightweight aircraft will drive the demand in high performance industrial applications.

By Forging Process, Hot Forging dominated the Aluminum Forging Market, while Precision Forging is the fastest growing segment.

Hot Forging segment had the dominated market share in terms of revenue generation in the Aluminium Forging Market in 2025. This technology is most popular owing to the fact that hot forging helps in producing highly complex and strong components even under extremely high temperatures. This technology improves the ductility of metal and eliminates internal flaws in the metals, thus making it suitable for applications in industries such as automotive, aerospace, and machinery.

Precision Forging segment has the fastest CAGR in the period between 2026 and 2035. This high rate of growth can be attributed to the increased demand for highly accurate and lightweight materials. This technology has been witnessing high popularity in the aerospace, defence, and automotive industries for efficient performance. Improved material yield along with dimensional accuracy and high mechanical properties contribute significantly to fast-paced adoption.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.45% |

|

Europe |

Germany |

27.80% |

|

Asia Pacific |

China |

41.20% |

|

Middle East & Africa |

UAE |

17.30% |

|

Latin America |

Brazil |

46.10% |

North America Aluminum Forging Market Insights.

North America in the aluminum forging market holds a significant position with a market share in 2025, supported by a well-established aerospace and automotive manufacturing base. The region benefits from advanced industrial infrastructure and consistent defense spending in the United States and Canada. Growing demand for lightweight vehicle components, aircraft structures, and industrial machinery parts is contributing to steady market development. Increasing adoption of high-performance forged components and ongoing investments in advanced manufacturing technologies continue to support regional market growth and competitiveness.

According to U.S. Environmental Protection Agency and U.S. Department of Energy, aluminum beverage container recycling rates in the United States are 43% indicating secondary aluminum utilization. Federal Corporate Average Fuel Economy standards target an average of nearly 49 miles per gallon for light-duty vehicles by model year 2026 driving lightweight adoption. Aerospace manufacturing in North America relies on forged aluminum components for weight reduction and structural.

Europe Aluminum Forging Market Insights.

The Europe Aluminum Forging Market shows strong presence in 2025 due to strict emission reduction policies and advanced engineering industries. Countries like Germany, France, United Kingdom, and Italy are key contributors to demand. High focus on electric vehicles, aerospace engineering, and industrial machinery production is supporting steady market growth. Increasing adoption of lightweight structural components is further strengthening consumption. Expanding regulatory frameworks for carbon neutrality and energy efficiency is driving aluminum forging adoption.

According to Eurostat and EEA, Europe maintains aluminum recycling rates exceeding 90% for beverage cans, with secondary aluminum contributing more than half of production output; European Automobile Manufacturers Association reports Europe accounts for around 15% of global motor vehicle production, supporting demand for forged aluminum components in lightweight applications. Under European Green Deal and Fit for 55 framework, EU targets 55% greenhouse gas reduction by 2030, driving lightweight material adoption.

Asia Pacific Aluminum Forging Market Insights.

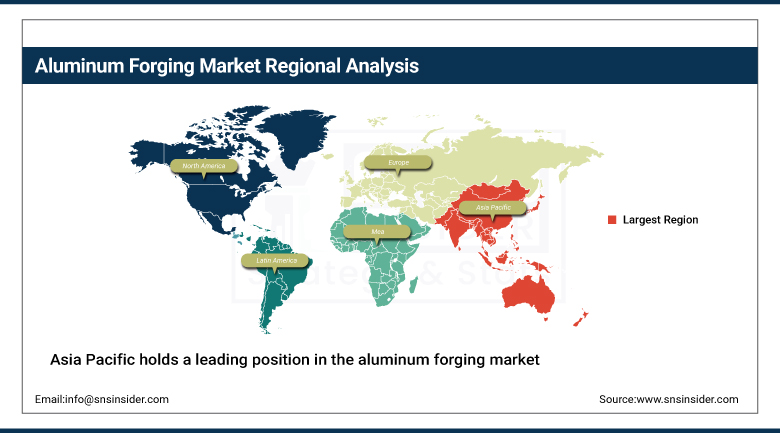

Asia Pacific holds a leading position in the aluminum forging market with a market share of about 41.85% in 2025 and is also expected to record the fastest CAGR growth of 6.31% during the forecast period. The region’s strength is driven by rapid industrialization and strong expansion of automotive production across China, India, Japan, South Korea, and Southeast Asia. Growing electric vehicle manufacturing, aerospace development, and industrial machinery demand are significantly increasing adoption. Rising infrastructure investments and export-oriented manufacturing activities further support sustained market expansion. Strong government initiatives continue to reinforce regional growth momentum and long-term competitiveness.

According to the United States Geological Survey Mineral Commodity 2025 and the International Energy Agency, China produced approximately 40 million metric tons of primary aluminum in 2024, representing the majority share of global output, while India produced about 4 million metric tons. Asia accounts for more than half of global aluminum smelting capacity, supporting downstream forging activity. The IEA also reports that China accounted for around 60% of global electric vehicle sales in 2024, strengthening demand for lightweight forged aluminum components.

Get Customized Report as per Your Business Requirement - Enquiry Now

Middle East & Africa and Latin America Aluminum Forging Market Insights.

The Middle East & Africa region along with Latin America is witnessing steady growth in the Aluminum Forging Market due to rising infrastructure and industrial development. Countries like UAE, Saudi Arabia, South Africa, Brazil, and Mexico are emerging as key demand centers. Increasing investments in oil and gas equipment, construction machinery, and transportation infrastructure are supporting market expansion. Growing need for durable and lightweight components is further boosting product adoption. Rising industrial diversification strengthens long term demand outlook.

According to USGS Mineral Commodity 2025 and UNEP, aluminum production is concentrated in energy-rich regions, with Middle East smelters using hydro and gas-based capacity and Latin America led by Brazil’s bauxite chain. Recycling supplies over one-third of aluminum, reflecting policy-driven energy efficiency targets, while secondary production uses up to 95% less energy than primary smelting, supporting forging in industrial manufacturing applications across transport and machinery sectors worldwide industrial trends.

Market Dynamics:

Growth Drivers: Rising demand for lightweight materials in automotive and aerospace manufacturing boosting forged aluminum adoption globally

Strong demand for lightweight and high strength materials in automotive and aerospace industries is driving aluminum forging usage. Manufacturers are increasingly replacing steel components with aluminum forgings to improve fuel efficiency and reduce emissions. Growing production of electric vehicles and advanced aircraft is further strengthening adoption. Aluminum forging provides superior strength to weight ratio and durability. Government regulations focused on emission reduction are encouraging industries to shift toward lightweight engineered materials globally.

According to the U.S. Department of Energy, a 10% reduction in vehicle weight can improve fuel economy by 6–8%, driving substitution toward lightweight aluminum alloys in automotive manufacturing. The European Commission mandates a 55% reduction in CO2 emissions from new cars by 2030 versus 2021 levels. The IEA electric vehicles accounted for over 18% of global car sales in 2023, while ICAO targets carbon-neutral aviation growth, supporting increased adoption of high-strength forged aluminum components.

Restraints: Complex manufacturing processes and tooling requirements creating operational barriers for aluminum forging industry expansion

Complex manufacturing processes and high tooling requirements are creating operational barriers in aluminum forging industry expansion. Precision control of temperature, pressure, and material flow is necessary for producing defect free components. Initial setup costs for forging dies and equipment are significantly high. Additionally, frequent maintenance and replacement of tools increase operational challenges. These factors reduce flexibility for new entrants and limit rapid scalability of production facilities in competitive industrial environments.

Opportunities: Increasing electrification in automotive and growing EV production driving new opportunities for forged aluminum components

Increasing electrification in automotive sector and rapid growth in electric vehicle production are creating strong opportunities for aluminum forging market expansion. EV manufacturers require lightweight, durable, and high-performance components to enhance battery efficiency and vehicle range. Aluminum forgings are widely used in motor housings, suspension parts, and structural frames. Rising investments in EV infrastructure and global shift toward sustainable mobility solutions are further accelerating demand for advanced forged aluminum components.

According to the International Energy Agency, global electric car sales exceeded 14 million units in 2023, representing about 18% of total new car sales, reflecting rapid electrification of the automotive sector. As per the United Nations Economic Commission for Europe, regulatory frameworks for vehicle efficiency are tightening, including CO₂ reduction targets across major markets. These measurable trends are increasing adoption of lightweight materials such as aluminum forgings in EV structural, chassis, and powertrain components.

Recent Developments:

-

2026: Howmet Aerospace strengthened advanced forging capacity for aerospace engines and expanded additive manufacturing capabilities for next-generation turbine components.

-

2025: Bharat Forge Limited invested in digital manufacturing platforms and increased aerospace forging production capacity for global OEM customers.

-

2025: Nippon Steel Corporation progressed advanced materials and forging technologies supporting automotive electrification and industrial efficiency improvements initiatives.

-

2024: Alcoa Corporation focused on portfolio restructuring and operational efficiency improvements across upstream bauxite and alumina segments globally.

Aluminum Forging Market Key Players are:

-

Alcoa Corporation

-

Howmet Aerospace

-

Kaiser Aluminum

-

ATI Inc.

-

Bharat Forge Limited

-

OTTO FUCHS Beteiligungen GmbH

-

Aubert & Duval

-

Voestalpine AG

-

Kobe Steel Ltd.

-

Nippon Steel Corporation

-

Daido Steel Co., Ltd.

-

SIFCO Industries

-

Carpenter Technology Corporation

-

AVIC Heavy Machinery Co., Ltd.

-

China First Heavy Industries

-

Jiangsu Pacific Precision Forging Co., Ltd.

-

Scot Forge Company

-

Liebherr Group

-

Sumitomo Electric Industries, Ltd.

-

Farinia Group

Aluminum Forging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.75 Billion |

| Market Size by 2035 | USD 35.04 Billion |

| CAGR | CAGR of 5.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Open Die Forgings, Closed Die Forgings, Rolled Ring Forgings, Impact Forgings) • By End User (Automotive, Aerospace & Defense, Industrial Machinery, Oil & Gas, Construction) • By Alloy Type (Aluminum 6000 Series, Aluminum 7000 Series, Aluminum 5000 Series, Other Aluminum Alloys) • By Forging Process (Cold Forging, Warm Forging, Hot Forging, Precision Forging) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Alcoa Corporation, Howmet Aerospace, Kaiser Aluminum, ATI Inc., Bharat Forge Limited, OTTO FUCHS Beteiligungen GmbH, Aubert & Duval, Voestalpine AG, Kobe Steel Ltd., Nippon Steel Corporation, Daido Steel Co., Ltd., SIFCO Industries, Carpenter Technology Corporation, AVIC Heavy Machinery Co., Ltd., China First Heavy Industries, Jiangsu Pacific Precision Forging Co., Ltd., Scot Forge Company, Liebherr Group, Sumitomo Electric Industries, Ltd., Farinia Group |

Frequently Asked Questions

The Aluminum Forging Market is expected to grow at a CAGR of 5.40% from 2026 to 2035.

The Aluminum Forging Market was valued at USD 20.75 billion in 2025.

Rising demand for lightweight, high-strength components in automotive and aerospace industries, along with strict emission regulations, is driving global aluminum forging demand.

The closed die forgings segment dominated the market in 2025 due to high precision, cost-effectiveness, and suitability for mass production in automotive and aerospace applications.

Asia Pacific dominated the Aluminum Forging Market due to rapid industrialization, strong automotive production growth, and expanding aerospace and manufacturing industries.

Get in Touch