Antimicrobial Plastics Market Report Scope & Overview:

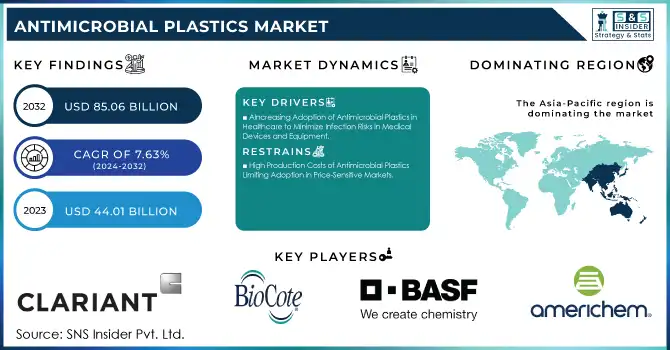

The Antimicrobial Plastics Market Size was valued at USD 44.01 billion in 2023 and is expected to reach USD 85.06 billion by 2032 and grow at a CAGR of 7.63% over the forecast period 2024-2032.

The antimicrobial plastics market is expanding with an increasing need for hygiene-based materials across the healthcare, packaging, and consumer goods industries. Increasing awareness regarding health and safety and the regulatory standards for products with stringent protection requirements drive the demand. In healthcare, for example, these plastics can be used in most medical devices and supplies at hospitals to reduce infection risks. They prevent the packaging industry from lowering product quality and shelf life. Consumer goods manufacturers have, therefore, embraced antimicrobial solutions to add a second layer of safety and strength to products such as electronic devices and personal care goods. In addition, an increasing interest in sustainability has led to the adoption of green antimicrobial agents and the creation of recycled plastic.

Get More Information on Antimicrobial Plastics Market - Request Sample Report

Some developments in the antimicrobial plastics market indicate the path that antimicrobial plastics have been taking. New technologies such as a plant-based antimicrobial solution launched in 2023 have shown the way forward for the industry by shifting towards sustainable alternatives. As observed early in 2024, the health industry has taken on materials that adhere to the highest standards of safety and improve the efficacy of medical equipment. Research developments that appeared in mid-2024 involve the utilization of natural substances to make plastics antibacterial-friendly, a movement that goes along with green thinking. By the end of 2024, a new, advanced antimicrobial material was approved to pave the way for mass production. Earlier, this year, in 2021, there was another effort to combine functionality and sustainability. The antibacterial recycled refuse sacks for households were launched. This is part of that dynamic market landscape where that convergence will meet the rapidly growing global demand in terms of technological innovations and environmental considerations.

Antimicrobial Plastics Market Dynamics:

Drivers:

-

Increasing Adoption of Antimicrobial Plastics in Healthcare to Minimize Infection Risks in Medical Devices and Equipment

The healthcare sector has emerged as a prominent driver for antimicrobial plastics, with their application in medical devices, surgical instruments, and hospital furniture steadily rising. These materials help mitigate infection risks by preventing bacterial growth on surfaces, making them indispensable in critical healthcare environments. The heightened focus on hygiene, especially in the wake of stricter hospital safety standards, has accelerated their adoption. Furthermore, advancements in antimicrobial additives have enabled the creation of plastics that remain effective over prolonged periods, ensuring long-lasting protection. The global push to combat healthcare-associated infections (HAIs) further bolsters demand, with hospitals and clinics increasingly investing in antimicrobial solutions to meet regulatory requirements and enhance patient safety.

-

Rising Use of Antimicrobial Packaging to Extend Shelf Life and Improve Food Safety

-

Growing Consumer Awareness About Hygiene and Safety Boosting Demand for Antimicrobial Products in Everyday Applications

-

Sustainability Trends Encouraging the Development of Recycled Antimicrobial Plastics for Eco-Friendly Applications

Sustainability is becoming a key driver for innovation in antimicrobial plastics, with growing efforts to incorporate recycled materials into their production. Recycled antimicrobial plastics cater to both functional and environmental requirements, enabling manufacturers to align with global sustainability goals. These materials address the dual need for hygiene and eco-consciousness, appealing to environmentally aware consumers and businesses alike. The rise in green certifications and government incentives for using recycled plastics is further propelling this trend, positioning antimicrobial plastics as a solution for sustainable growth.

Restraint:

-

High Production Costs of Antimicrobial Plastics Limiting Adoption in Price-Sensitive Markets

The relatively high cost of antimicrobial plastics remains a significant barrier to widespread adoption, particularly in price-sensitive markets. The production of these plastics involves advanced additives and manufacturing processes, which drive up costs compared to conventional materials. Small and medium-sized enterprises (SMEs) often face challenges in adopting these solutions due to budget constraints, despite their long-term benefits. Additionally, the higher cost of antimicrobial packaging can deter its use in low-margin industries, where cost optimization is critical. Balancing functionality, affordability, and scalability remains a pressing challenge for the market.

Opportunity:

-

Rising Demand for Sustainable Antimicrobial Solutions Driving Innovation in Bio-Based Additives and Recycled Plastics

The shift towards sustainability presents a significant opportunity for innovation in bio-based additives and recycled antimicrobial plastics. These solutions cater to environmentally conscious consumers and industries, aligning with global efforts to reduce plastic waste and carbon footprints. As demand grows for sustainable materials, manufacturers have a chance to differentiate themselves by offering eco-friendly antimicrobial solutions that meet both hygiene and environmental standards.

-

Expansion of Antimicrobial Plastics in Emerging Markets with Growing Industrialization and Healthcare Infrastructure Development

|

Aspect |

Details |

|---|---|

|

Raw Material Sourcing |

Efforts to use renewable or recycled raw materials to reduce carbon footprint and minimize environmental harm. |

|

Manufacturing Process |

Adoption of energy-efficient manufacturing techniques and reduced emissions in production to lower environmental impact. |

|

Biodegradability |

Some antimicrobial plastics are being designed for improved biodegradability, reducing plastic waste accumulation. |

|

Recyclability |

Focus on making antimicrobial plastics recyclable to ensure they are reused and do not contribute to landfill waste. |

|

Eco-Friendly Additives |

Use of environmentally safe, non-toxic antimicrobial agents (e.g., silver and zinc) to reduce ecological footprint. |

|

End-of-Life Management |

Efforts to improve post-consumer recycling programs and responsible disposal methods to prevent environmental contamination. |

|

Sustainability Certifications |

Companies are pursuing eco-certifications like ISO 14001, ensuring environmentally responsible manufacturing practices. |

|

Green Packaging |

Companies adopting antimicrobial plastics in packaging that is both functional and sustainable, reduce plastic pollution. |

The antimicrobial plastics industry is increasingly focusing on sustainability, adopting practices that mitigate its environmental footprint. Companies are prioritizing the use of renewable or recycled materials and adopting energy-efficient production methods to lower emissions. Additionally, there is a strong push toward creating plastics that are biodegradable or recyclable, thus addressing long-term plastic waste concerns. Eco-friendly antimicrobial additives, such as silver and zinc, are replacing harmful chemicals, reducing the ecological impact. Furthermore, sustainable packaging solutions and improved end-of-life management strategies, including enhanced recycling programs, are becoming a key focus for the industry. These sustainability efforts contribute to the industry’s evolving role in the larger global movement toward environmental responsibility

Antimicrobial Plastics Market Segments

By Type

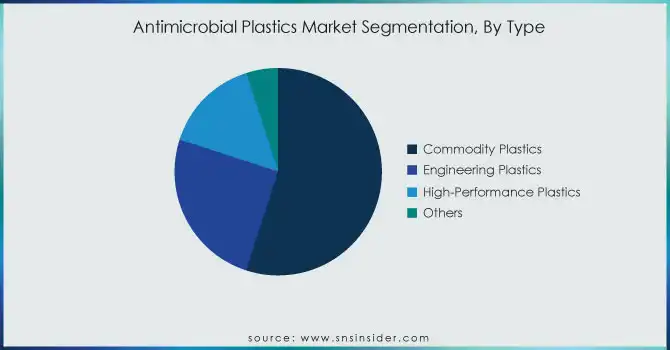

Commodity plastics dominated the antimicrobial plastics market in 2023, accounting for an estimated 55% market share. Within this category, polypropylene (PP) emerged as the leading subsegment, holding approximately 20% of the commodity plastics market share. The dominance of commodity plastics is attributed to their extensive use across various industries due to their cost-effectiveness, durability, and versatility. Polypropylene, in particular, is widely utilized in packaging, medical devices, and consumer goods, thanks to its lightweight nature and strong resistance to microbial growth. For instance, antimicrobial PP is extensively used in food packaging to enhance product safety and shelf life, while its application in healthcare includes syringes and protective equipment.

By Additive

Inorganic antimicrobial additives dominated the antimicrobial plastics market in 2023, capturing a 65% market share. Among these, silver-based additives dominated, contributing approximately 40% to the inorganic additives segment's share. Silver's high efficacy against a broad spectrum of microorganisms and its long-lasting antimicrobial properties make it the preferred choice across industries. For example, silver-based antimicrobial plastics are commonly used in medical instruments, food storage containers, and water filtration systems, providing enhanced safety and hygiene. Silver additives are particularly favored in healthcare, where infection control is critical.

By End-use

The healthcare segment dominated the end-use sector for antimicrobial plastics in 2023, holding a 40% market share. Within this category, medical devices and equipment accounted for approximately 25% of the healthcare segment's share. The widespread adoption in healthcare is driven by the critical need to minimize healthcare-associated infections (HAIs) through antimicrobial solutions. Applications such as surgical instruments, hospital furniture, and diagnostic devices rely heavily on antimicrobial plastics for improved hygiene and patient safety. For instance, antimicrobial coatings on catheters and ventilators have become standard practice to reduce infection risks in hospitals.

Antimicrobial Plastics Market Regional Analysis

The Asia-Pacific region dominated the antimicrobial plastics market in 2023, accounting for a 45% market share. This dominance is primarily driven by the region's robust industrial base, rapid urbanization, and increasing awareness of hygiene across sectors such as healthcare, packaging, and consumer goods. Countries like China, Japan, and India played a significant role in this leadership. China, being the largest contributor, demonstrated extensive use of antimicrobial plastics in healthcare applications, such as medical devices and hospital infrastructure, backed by government initiatives to modernize the healthcare system. For instance, China's substantial investments in improving healthcare facilities have led to an increased demand for antimicrobial materials to ensure safety and infection control. Similarly, Japan's advanced manufacturing capabilities and strong emphasis on innovation have propelled the use of antimicrobial plastics in electronics and packaging. In India, the growing demand for hygienic packaging in the booming e-commerce and food delivery sectors has further fueled the market. Reports highlight that over 30% of the region's demand for antimicrobial plastics in 2023 came from healthcare and packaging applications, reflecting their significant role in driving Asia-Pacific’s dominance.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Key Players

-

Americhem Inc (AMERGY Antimicrobial Additives, Polymer Masterbatches)

-

BASF SE (Ultramid C37LC, Ultradur B1520)

-

BioCote Limited (Antimicrobial Coatings, Polymer Additives)

-

Clariant AG (AddWorks AGC 970, AddWorks PKG 902)

-

Dupont (Delrin Antimicrobial Resins, Zytel Antimicrobial Resins)

-

Ensinger (TECAFORM AH, TECANYL MT)

-

King Plastic Corporation (King StarBoard, King MicroShield)

-

Lifespan Technologies (Guardian Antimicrobial Polymers, Lifespan Resins)

-

Lonza (Lonzabac Antimicrobial Additives, Densil Antimicrobial Solutions)

-

Microban International Ltd. (Microban Antimicrobial Additives, Microban Embedded Polymers)

-

Milliken Chemical (AlphaSan Silver Antimicrobial, Millad NX)

-

Parx Materials N.V (Saniconcentrate, PlasticShield)

-

Polyone Corporation (OnColor Antimicrobial Solutions, OnCap Antimicrobial Masterbatch)

-

RTP Company (Antimicrobial Masterbatches, Thermoplastic Compounds)

-

Sanitized AG (Sanitized PL 14-32, Sanitized BC 02-16)

-

Teknor Apex Company (Apex Flexible Vinyl, Monprene Thermoplastic Elastomers)

-

The Dow Chemical Company (INFUSE Olefin Block Copolymers, SURLYN Ionomers)

-

Toray Industries, Inc. (Torayca Resin, Amilan Nylon Resins)

-

Toyobo Co., Ltd. (Nerbrid Antimicrobial Resin, VYLON Polymer Additives)

-

Tosaf Compounds Ltd. (Antibacterial Masterbatches, Flame Retardant Compounds)

Recent Developments

-

January 2024: BASF partnered with Kingfa Sci & Tech to produce and distribute Ultramid B10TW3 polyamide 6 resin with silver ion antibacterial technology across China, boosting BASF's presence in the Asian market.

-

January 2024: Milliken launched ALPHA GUARD PLUS, an antimicrobial coating for textiles offering long-lasting protection against bacteria, fungi, and mold, targeting healthcare, hospitality, and athletic wear applications.

-

December 2023: Avient Corporation expanded its Cesa Withstand portfolio with new grades designed to prevent microbe development in critical applications.

-

September 2023: Microban International unveiled Ascera, a new technological advancement in antimicrobial solutions.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 44.01 Billion |

| Market Size by 2032 | USD 85.06 Billion |

| CAGR | CAGR of 7.63% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Commodity Plastics [Polyethylene (PE), Polyvinyl Chloride (PVC), Polypropylene (PP), Polystyrene (PS), Polyethylene Terephthalate (PET), Poly (methyl methacrylate) (PMMA), Polyurethane (PUR), Acrylonitrile Butadiene Systems (ABS)), Engineering Plastics [Polycarbonate (PC), Polyoxymethylene (POM), Polyamide (PA), Thermoplastic polyurethane (TPU), Others], High-Performance Plastics, Others) • By Additive (Inorganic Antimicrobial Additives [Copper, Silver, Zinc], Organic Antimicrobial Additives [Triclosan, Oxybisphenoxarsine (OBPA), Others]) • By End-use (Building & Construction, Healthcare, Packaging, Automotive, Electronics, Commercial, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | PARX Materials N.V, King Plastic Corporation, BioCote Limited, BASF SE, Microban International Ltd., Americhem Inc, Lonza, Sanitized AG, Polyone Corporation, Clariant AG and other key players |

| Key Drivers | • Growing Consumer Awareness About Hygiene and Safety Boosting Demand for Antimicrobial Products in Everyday Applications • Sustainability Trends Encouraging the Development of Recycled Antimicrobial Plastics for Eco-Friendly Applications |

| Restraints | • High Production Costs of Antimicrobial Plastics Limiting Adoption in Price-Sensitive Markets |

Frequently Asked Questions

Ans: The Antimicrobial Plastics Market is expected to grow at a CAGR of 7.63%

Ans: The Antimicrobial Plastics Market Size was valued at USD 44.01 billion in 2023 and is expected to reach USD 85.06 billion by 2032.

Ans: Rising demand for sustainability, industrial growth in emerging markets, and integration into smart devices are driving the expansion of antimicrobial plastics.

Ans: Stringent regulatory compliance and varying approval processes across regions delay the development and commercialization of antimicrobial plastic products.

Ans: The Asia-Pacific region led the antimicrobial plastics market in 2023 with a 45% market share, driven by industrial growth, urbanization, and heightened hygiene awareness, particularly in healthcare, packaging, and consumer goods, with China, Japan, and India as key contributors.

Get in Touch