Application Delivery Controller Market Report Scope & Overview:

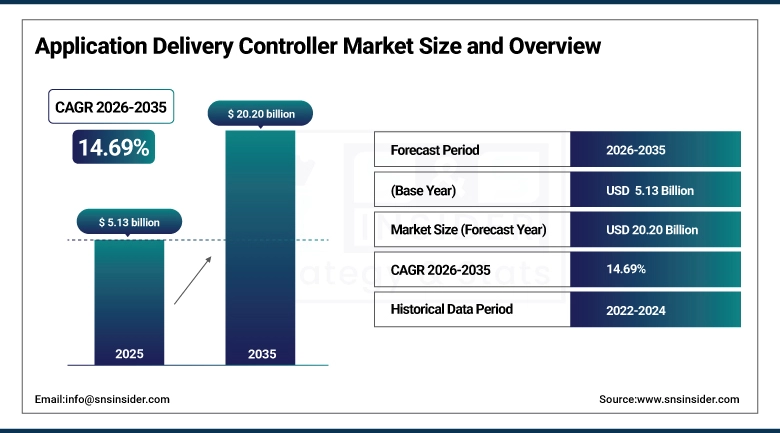

The Application Delivery Controller (ADC) Market was valued at USD 5.13 billion in 2025 and is expected to reach USD 20.20 billion by 2035, growing at a CAGR of 14.69% from 2026-2035.

ADC Market Growth Is Because Of Increased Cloud Adoption, Higher Traffic in Data Center, Growth in Hybrid and Multi-Cloud Environments, And Demand for Application Delivery That Ensures High Performance and Security. Companies Are Adopting ADC Solutions to Improve Load Balancing, Availability, Security, SSL Offloading, And Experience of Their Applications.

F5 Networks' State of Application Strategy 2024 report documents that enterprise organizations now deploy an average of 289 applications, with 60% running in public or private cloud environments creating the multi-cloud application delivery complexity that ADC solutions must manage across distributed and diverse infrastructure.

ADC Market Size and Forecast

-

Market Size in 2025: USD 5.13 Billion

-

Market Size by 2035: USD 20.20 Billion

-

CAGR: 14.69% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Application Delivery Controller (ADC) Market - Request Free Sample Report

ADC Market Trends

-

Cloud-native ADC deployment where application delivery controller functions are implemented as containerized microservices on Kubernetes orchestration platforms is enabling dynamic scaling, declarative configuration, and DevOps integration that traditional hardware and virtual ADC deployments cannot match.

-

AI-powered traffic analysis is enabling ADC systems to identify anomalous traffic patterns indicating DDoS attacks, application abuse, and bot traffic in real time using machine learning models trained on baseline traffic patterns whose deviation detection improves security response speed versus signature-based threat detection.

-

Service mesh integration with ADC functionality is creating architecture models where internal microservice communication is managed by service mesh sidecar proxies (Istio, Linkerd) while external traffic management remains ADC-delivered establishing complementary roles that sustain ADC relevance in cloud-native architectures.

-

Zero Trust network access integration with ADC is enabling application-layer identity verification that authenticates users to specific applications rather than network segments aligning with enterprise zero trust security frameworks that are replacing perimeter-based security architectures.

-

5G edge ADC deployment is emerging as SA 5G's edge computing integration creates application delivery requirements at network edge locations where ADC traffic management serves the low-latency applications that edge compute hosts and whose performance depends on edge-co-located traffic optimization.

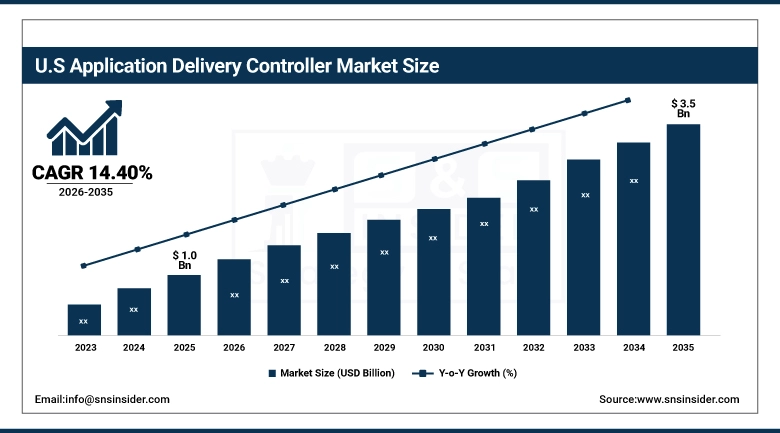

U.S. Application Delivery Controller Market was valued at USD 1.0 billion in 2025 and is expected to reach USD 3.5 billion by 2035, growing at a CAGR of 14.40% from 2026-2035.

The U.S. Application Delivery Controller (ADC) Market is expanding owing to rapid cloud computing adoption, rapid growth in hybrid and multi-cloud infrastructure adoption, cybersecurity threats, and increasing demands for secure and low latency digital applications. The rapid growth in e-commerce, artificial intelligence workload, 5G network adoption, and increased data center traffic will also accelerate ADC adoption.

Cloudflare's global network which delivers ADC functionality including DDoS protection, load balancing, and SSL termination for over 20% of the internet's web traffic demonstrates the commercial scale that cloud-delivered ADC services achieve relative to traditional hardware-based deployments.

ADC Market Segment Analysis

-

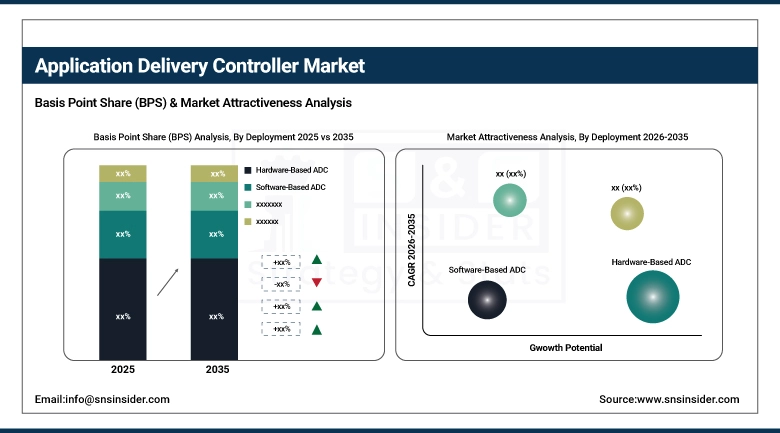

By Deployment, Hardware-Based ADC dominated with significant revenue share in 2025; Virtual ADC growing at fastest CAGR.

-

By Organization Size, Large Enterprises dominated in 2025; SMEs growing at fastest CAGR driven by cloud ADC accessibility.

-

By End-Use Industry, BFSI dominated with significant share in 2025; Retail growing at fastest CAGR.

By Deployment: Hardware dominant, Virtual ADC fastest CAGR

Hardware-Based ADCs maintained their dominant position in the Application Delivery Controller Market in 2025, reflecting the performance characteristics and total cost of ownership advantages that dedicated application delivery hardware provides for high-traffic, mission-critical application deployments. Dedicated ASIC-based ADC hardware including F5's BIG-IP appliances, Citrix ADC MPX, and A10 Networks' Thunder series delivers application traffic processing at line rates that general-purpose servers running software ADCs cannot match without substantially higher hardware cost per unit of throughput capacity. Organizations operating large-scale, on-premises data centers with predictable high traffic loads financial institutions, telecommunications providers, large healthcare systems sustain hardware ADC demand through upgrade cycles of existing hardware deployments whose performance advantages remain compelling relative to software alternatives.

Virtual ADCs software applications that run on standard x86 servers, virtual machine platforms (VMware, KVM), or cloud infrastructure (AWS, Azure, Google Cloud) are growing at the fastest deployment CAGR, driven by the cloud migration that makes hardware ADC's on-premises deployment model obsolete for cloud-hosted application workloads. A cloud-native application deployed on AWS cannot use an on-premises hardware ADC for load balancing it requires an ADC solution that deploys within the AWS environment, using either AWS's native Elastic Load Balancing services, AWS Marketplace virtual ADC offerings, or cloud-native ADC platforms from F5, Citrix, or A10 Networks whose software versions deploy on cloud instances.

By Organization Size: Large Enterprise dominant, SME fastest CAGR

Large Enterprises dominated the ADC Market in 2025, reflecting the scale and complexity of enterprise application portfolios hundreds of applications serving thousands of users across geographically distributed offices, data centers, and cloud environments whose traffic management requirements create the ADC investment justification that SME application deployments typically do not reach. Large financial institutions, healthcare systems, retailers, and technology companies whose business continuity, security compliance, and user experience requirements create uncompromising application availability demands are the primary ADC hardware customers organizations for whom ADC hardware investment of USD 100,000-500,000 is justified by the business consequence of application unavailability that ADC-less infrastructure would impose.

SMEs are growing at the fastest organization size CAGR, driven by the cloud ADC's democratization of advanced application delivery capability through subscription pricing that eliminates the upfront hardware investment barrier. SaaS-delivered ADC services including Cloudflare's load balancing and DDoS protection, AWS Shield and Elastic Load Balancing, and Azure Application Gateway provide ADC functionality at per-request or monthly subscription pricing that SMEs can adopt without capital budgeting, procurement processes, or hardware lifecycle management. The growing SME e-commerce sector where small and medium online retailers whose transaction volume does not justify hardware ADC investment nonetheless require DDoS protection, SSL offloading, and geographic load balancing is the primary driver of SME ADC adoption through cloud and managed service delivery models.

By End-Use: BFSI dominant, Retail fastest CAGR

The BFSI sector dominated the ADC Market in 2025, reflecting the financial services industry's uncompromising requirements for application availability, security, and transaction throughput. Digital banking applications mobile banking apps, online trading platforms, payment processing systems serve millions of concurrent users whose transaction failures represent both revenue loss and regulatory liability that financial institutions cannot tolerate. Banks whose mobile banking apps experience outages during peak trading hours face customer complaints, regulatory scrutiny, and competitor advantage that justify premium ADC investment at hardware appliance performance levels that software alternatives match only at substantial cost premium. Financial services' regulatory compliance requirements including PCI DSS for payment card processing, SWIFT security requirements, and banking privacy regulations specify application security controls including web application firewall functionality that ADC integration provides most efficiently.

The Retail segment is growing at the fastest end-use CAGR, driven by the explosive growth of e-commerce that creates application traffic patterns whose peak intensity Black Friday, Cyber Monday, single-day sales events can exceed average traffic by 10-100x in hours. A retail application architecture that cannot scale to handle peak traffic events fails at the moments of highest commercial opportunity losing sales, destroying brand reputation, and enabling competitors whose applications remain available to capture the purchasing intent that traffic spikes represent. Cloud ADC and cloud-native load balancing solutions whose auto-scaling capabilities provision additional capacity within minutes of traffic surge detection enable retail application architectures whose peak performance is guaranteed without the over-provisioned infrastructure that hardware ADC requires for equivalent peak capacity.

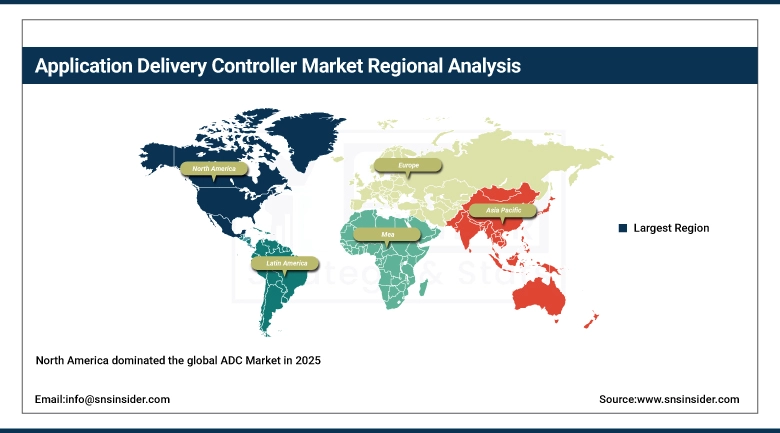

ADC Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

87% |

|

Europe |

United Kingdom |

27% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

North America ADC Market Insights

North America dominated the global ADC Market in 2025, sustained by the United States' position as the primary market for cloud infrastructure services, enterprise software, and digital commerce whose application delivery requirements create the ADC demand that sustains North American market leadership. The U.S. market's cloud ADC adoption is more commercially mature than any other regional market where AWS, Azure, and Google Cloud native load balancing services supplement rather than replace commercial ADC solutions, creating a multi-tier ADC market where cloud-native services serve baseline traffic management and specialized commercial ADC provides advanced security, SSL offloading, and multi-cloud orchestration above cloud-native capabilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific ADC Market Insights

Asia Pacific is the fastest-growing regional ADC Market, driven by the rapid digital transformation across emerging economies in India and China whose growing internet user populations, expanding cloud adoption, and increasing e-commerce activity create proportional ADC demand alongside the sophisticated ADC markets of Japan and South Korea. China's domestic ADC market is served by both international ADC vendors and domestic alternatives including Sangfor Technologies and HuaWei's enterprise networking division whose compliance with Chinese data localization requirements sustains domestic ADC adoption for the large proportion of Chinese enterprise application traffic that data sovereignty regulations require to process within China's national network boundaries. India's growing IT services sector whose cloud-delivered software development, managed services, and enterprise IT operations create expanding ADC requirements is sustaining Indian ADC market growth above the regional average.

Europe ADC Market Insights

Europe's ADC Market is growing with strong enterprise digital transformation across Germany, France, the UK, and Scandinavia, where hybrid cloud adoption combining on-premises infrastructure with public cloud services creates the multi-environment application delivery complexity that ADC solutions address most effectively. The EU's GDPR compliance requirements for application data handling create security-motivated ADC investment where application-layer security features including WAF, DDoS protection, and TLS inspection are deployed as GDPR compliance measures that ADC integration provides more systematically than application-level security approaches. European financial services digitalization where incumbent banks are accelerating digital transformation to compete with fintech challengers sustains BFSI ADC demand across major European markets.

MEA and Latin America ADC Market Insights

The Middle East's ADC Market is growing with the Gulf states' digital economy investment where government e-services platforms, growing fintech sectors, and digital commerce infrastructure create application delivery requirements that ADC solutions address. Saudi Arabia's Vision 2030 digital transformation ambitions including government service digitalization, smart city applications, and growing tech startup ecosystem create growing ADC demand from both public sector digital infrastructure and the commercial technology sector. Latin America's market concentrates in Brazil and Mexico, where expanding e-commerce, growing digital banking adoption, and increasing cloud migration by major corporations create proportional ADC demand growth.

ADC Market Growth Drivers:

-

Cloud application migration and cybersecurity requirements driving sustained application delivery controller market growth globally

The Drivers for the Application Delivery Controller (ADC) Market include the increased dependence of enterprises on cloud computing and hybrid IT architectures. The increase in internet traffic, the growth of AI-driven workload processing, and the development of data center technologies have increased the demand for intelligent traffic and load balancing. The increasing concern about cybersecurity issues, like DDoS and application layer attacks, has also resulted in the increased uptake of ADCs with built-in features of security such as SSL inspection, web application firewall, and secure access control. Other drivers for the ADC market include remote working, e-commerce, 5G networks, and SaaS applications.

ADC Market Restraints:

-

Cloud-native load balancing competition and complexity of multi-cloud environments creating ADC market challenges globally

Cloud-native load balancing services AWS Elastic Load Balancing, Azure Application Gateway, and Google Cloud Load Balancing provide baseline traffic management functionality that reduces the commercial case for third-party ADC deployments in single-cloud application environments. As organizations move applications to cloud infrastructure, some portion of the traffic management requirement that hardware ADCs previously served is absorbed by cloud-native services whose economics no upfront cost, per-request pricing that scales proportionally with usage make them natural default choices for simple load balancing use cases. ADC vendors whose differentiation depends on advanced capabilities multi-cloud management, AI-powered security, performance optimization beyond basic load balancing must articulate and demonstrate value above cloud-native baselines in environments where procurement defaults to the cloud provider's native service.

ADC Market Opportunities:

-

AI-powered security and multi-cloud ADC orchestration creating transformative application delivery controller market growth globally

AI-native ADC security represents the market's most commercially compelling differentiation opportunity, where machine learning models that continuously adapt to evolving application traffic patterns and threat techniques provide security effectiveness that signature-based WAF rules cannot match against zero-day attacks and sophisticated bot networks. An ADC whose WAF adapts to new attack techniques within hours of their first observation by analyzing traffic anomalies that deviate from normal application interaction patterns provides security currency that traditional rule-update cycles cannot maintain against adversaries who continuously evolve their techniques. Multi-cloud ADC management providing application delivery visibility and policy control across applications distributed across multiple cloud providers addresses the operational complexity that enterprise multi-cloud architectures create, where inconsistent native load balancing capabilities and separate management consoles across cloud providers create configuration fragmentation that ADC orchestration resolves.

Recent Developments:

-

2026: F5 Networks launched its BIG-IP Next Cloud-Native ADC a Kubernetes-native application delivery platform deploying as Helm charts on any Kubernetes distribution with declarative configuration through Kubernetes custom resources enabling DevOps teams to manage ADC policies through the same GitOps workflows used for application deployment, eliminating the separate ADC management workflows that created friction between application development velocity and network policy governance in traditional ADC architectures.

-

2025: A10 Networks released its Thunder ADC 6.0 with integrated AI-powered distributed denial of service protection using behavioral AI trained on 10 billion daily network events to distinguish legitimate traffic from attack traffic during volumetric DDoS events achieving 99.97% traffic scrubbing accuracy at 1 Tbps+ attack volumes in carrier-scale validation testing, targeting telecommunications providers and large enterprises whose volumetric DDoS exposure requires carrier-grade mitigation performance that traditional ADC security does not scale to address.

ADC Market Key Players

Some of the Application Delivery Controller Market Companies

-

F5 Networks Inc. (BIG-IP)

-

Citrix Systems Inc. (Cloud Software Group)

-

A10 Networks Inc.

-

Radware Ltd.

-

Fortinet Inc.

-

Barracuda Networks Inc.

-

Kemp Technologies Inc. (Progress Software)

-

Cloudflare Inc.

-

AWS (Elastic Load Balancing)

-

Microsoft Corporation (Azure Application Gateway)

-

Google LLC (Cloud Load Balancing)

-

Imperva Inc.

-

HAProxy Technologies LLC

-

Sangfor Technologies Inc.

-

Akamai Technologies Inc.

-

Fastly Inc.

-

Brocade Communications (Broadcom)

-

NetScout Systems Inc.

-

Alteon WebSystems (Radware)

-

NGINX Inc. (F5)

Application Delivery Controller Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.13 Billion |

| Market Size by 2035 | USD 20.20 Billion |

| CAGR | CAGR of 14.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Deployment (Hardware-Based ADC, Software-Based ADC, Virtual ADC) • By Organization Size (Large Enterprises, SMEs) • By End-Use Industry (BFSI, IT & Telecom, Healthcare, Retail, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | F5 Networks Inc., Citrix Systems Inc., A10 Networks Inc., Radware Ltd., Fortinet Inc., Barracuda Networks Inc., Kemp Technologies Inc., Cloudflare Inc., Amazon Web Services (AWS), Microsoft Corporation, Google LLC, Imperva Inc., HAProxy Technologies LLC, Sangfor Technologies Inc., Akamai Technologies Inc., Fastly Inc., Broadcom Inc., NetScout Systems Inc., Alteon WebSystems, NGINX Inc. |

Frequently Asked Questions

The Application Delivery Controller Market was valued at USD 5.13 billion in 2025.

North America dominated; Asia Pacific is the fastest growing regional market.

BFSI dominated; Retail is growing at the fastest CAGR driven by e-commerce expansion.

Hardware-Based ADC dominated; Virtual ADC is growing at the fastest CAGR.

The Application Delivery Controller Market is expected to grow at a CAGR of 14.69% from 2026 to 2035.

Get in Touch