Arm Based Servers Market Report Scope & Overview:

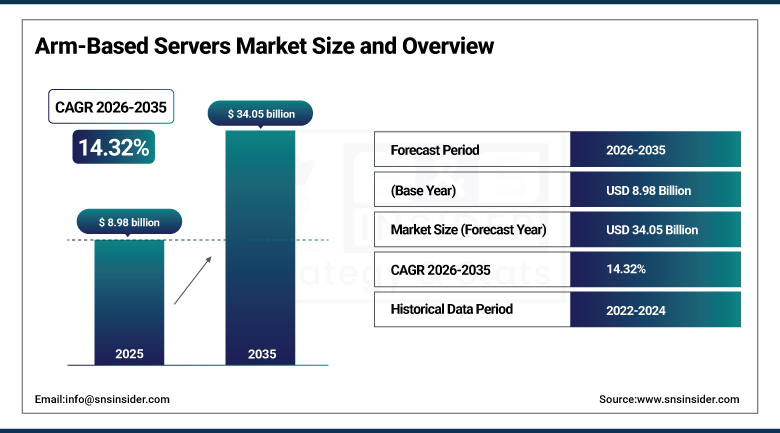

The Arm-Based Servers Market was valued at USD 8.98 billion in 2025 and is expected to reach USD 34.05 billion by 2035, growing at a CAGR of 14.32% from 2026-2035.

Arm-based Servers Market Growth is driven by increased demand for efficient and high-performance computing resources in data centers. Factors such as growing cloud adoption, artificial intelligence, edge computing, and lower total cost of ownership compared to x86 servers have led to fast enterprise and hyperscaler deployments across the globe.

Ampere Computing's Altra processor the leading third-party Arm server processor is deployed in Oracle Cloud Infrastructure, Microsoft Azure, Google Cloud, and major OEM server platforms including HPE ProLiant and Dell PowerEdge, demonstrating the ecosystem breadth that sustains Arm server adoption beyond single-cloud programs.

Arm-Based Servers Market Size and Forecast

-

Market Size in 2025: USD 8.98 Billion

-

Market Size by 2035: USD 34.05 Billion

-

CAGR: 14.32% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Arm-Based Servers Market - Request Free Sample Report

Arm-Based Servers Market Trends

-

AI inference workload optimization on Arm where Arm's Neoverse compute cores and NVIDIA's Grace CPU (Arm architecture) provide AI inference performance per watt advantages over x86 for the transformer model inference that AI application serving requires is creating a new premium demand category beyond the cost-optimization use case that drove early Arm server adoption.

-

Apple Silicon's M-series success in consumer computing is demonstrating Arm's performance credibility at compute-intensive tasks removing the performance perception barrier that historically deterred enterprise architects from specifying Arm in server infrastructure where x86 performance was assumed superior.

-

RISC-V alternative architecture development where open-source processor designs are advancing toward server-class performance creates competitive pressure on Arm's architecture licensing business model but simultaneously validates the RISC trend that Arm represents.

-

Software ecosystem maturation where major enterprise software vendors including SAP, Oracle, and Red Hat certify their applications for Arm server deployment is accelerating enterprise Arm adoption by removing the application compatibility barrier that early Arm server adopters faced.

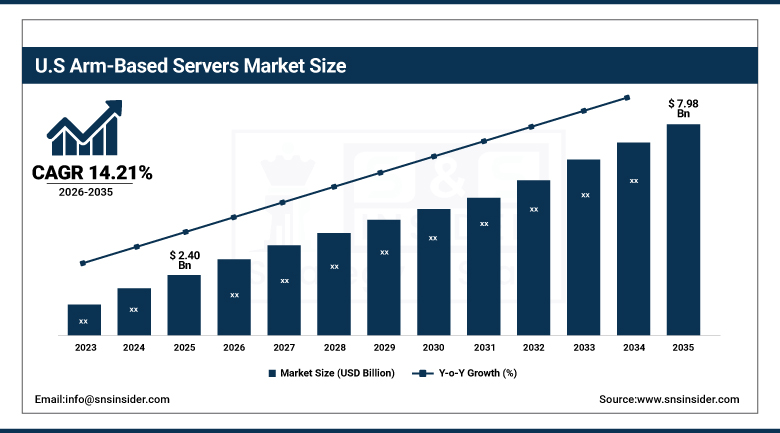

U.S. Arm-Based Servers Market was valued at USD 2.40 billion in 2025 and is expected to reach USD 7.98 billion by 2035, growing at a CAGR of 14.21%.

U.S. Arm-based Servers Market Growth is fueled by the increased adoption of cloud service providers, artificial intelligence, machine learning workloads, need for energy-efficient data centers, and hyperscaler investments by leading tech firms.

AWS's 2024 announcement that Graviton4-based instances deliver 40% better performance compared to Graviton3 compounding the generational improvement trajectory that demonstrates Arm's continuous innovation rate has sustained cloud customer confidence in Arm architecture's long-term competitive evolution trajectory.

Arm-Based Servers Market Segment Analysis

-

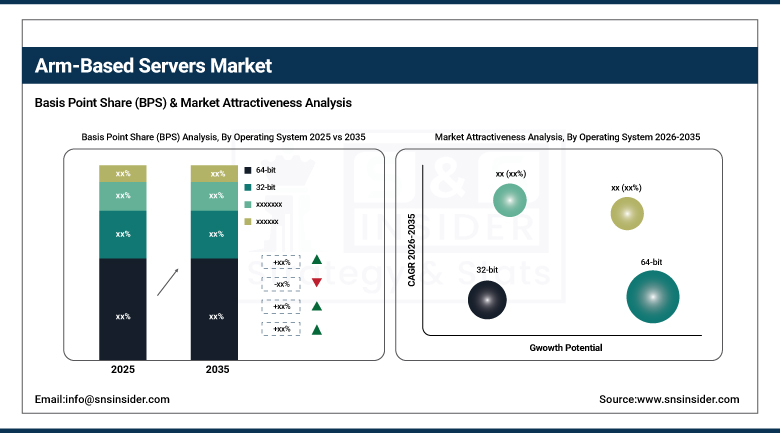

By OS, 64-bit dominated with ARM Cortex-A core holding ~81% market share in 2025; 32-bit growing at fastest CAGR of 17.48%.

-

By Core Architecture, ARM Cortex-A dominated with ~81% revenue share; ARM Cortex-M growing fastest at 17.17% CAGR.

-

By Application, Mobile Computing dominated with ~26% share in 2025; Edge Computing and HPC growing rapidly.

By OS: 64-bit/Cortex-A dominant at 81%, 32-bit/Cortex-M fastest CAGR

64-bit ARM systems held the dominant operating system position with ARM Cortex-A core based servers accounting for approximately 81% of market revenue in 2025 reflecting the overwhelming adoption of 64-bit architecture for the enterprise server, cloud computing, and high-performance computing applications that drive Arm server market revenue. 64-bit Arm's data center applicability where the memory addressability, instruction set breadth, and virtual machine compatibility of 64-bit architecture are minimum requirements for enterprise server operating systems, databases, and application servers makes the 64-bit segment the overwhelmingly dominant Arm server commercial category. The 32-bit segment growing at the fastest CAGR of approximately 17.48% is driven by embedded systems, IoT, and edge computing applications where 32-bit ARM Cortex-M's cost efficiency, power consumption, and real-time performance characteristics are specifically optimal for microcontroller-class server applications in smart manufacturing, building management, and industrial IoT.

By Core Architecture, ARM Cortex-A dominated, ARM Cortex-M growing fastest

The leader in Arm-Based Servers Market was the ARM Cortex-A with an 81% revenue share, owing to its outstanding performance in high compute applications, cloud-based infrastructure, and data center implementations. The Cortex-A processors have efficiency and scalability, making it the most preferred for enterprise as well as hyperscale use cases. On the other hand, the fastest growing category is ARM Cortex-M, posting a CAGR of 17.17%.

By Application: Mobile Computing dominant, Edge Computing growing rapidly

Mobile Computing held approximately 26% of the Arm-Based Servers Market in 2025, reflecting Arm's architectural origins in mobile processor design and the continuing deployment of Arm processors in smartphone application processors, tablets, and mobile computing devices many of which serve server-equivalent roles in cloud-connected mobile computing architectures. Enterprise Server deployments are growing as the software ecosystem maturation and hyperscaler validation remove the adoption barriers that previously limited Arm server penetration in on-premises enterprise data centers. Edge Computing represents the fastest-growing application category within the non-mobile segments where Arm's power efficiency advantage creates specific architectural preference for the battery-powered or power-constrained edge server deployments that are growing across smart city, industrial IoT, and telecommunications edge infrastructure.

Arm-Based Servers Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

89% |

|

Asia Pacific |

China |

42% |

|

Europe |

United Kingdom |

27% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

48% |

North America Arm-Based Servers Market Insights

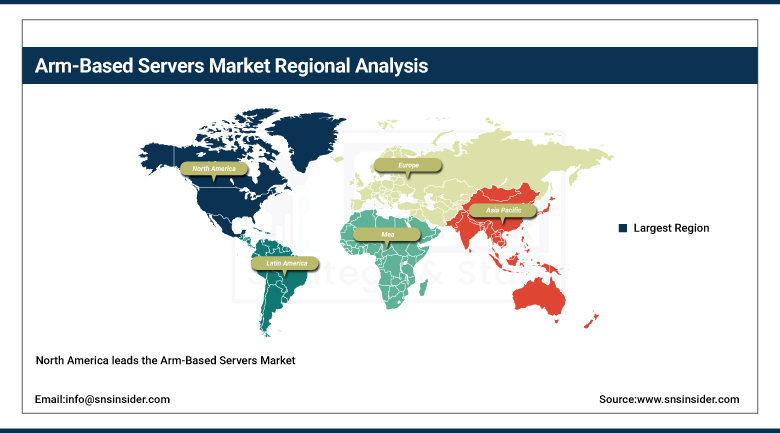

North America leads the Arm-Based Servers Market, anchored by the United States' hyperscale cloud provider Arm server deployments and the growing enterprise adoption that cloud provider validation enables. The U.S. Arm server ecosystem where Arm Holdings (Softbank subsidiary), NVIDIA, Ampere Computing, Amazon (Annapurna Labs), Apple, and Qualcomm each develop Arm server processors in different market segments sustains the most technically diverse Arm server product landscape globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Arm-Based Servers Market Insights

Asia Pacific is the fastest-growing regional Arm-Based Servers Market, driven by China's domestic Arm server development where Huawei's Kunpeng 920 processor (Arm Cortex-A architecture) is deployed in Chinese data center infrastructure as a technology sovereignty alternative to U.S. x86 processors whose export control vulnerability motivates domestic processor development and the region's large cloud computing market whose cost sensitivity creates strong incentive for Arm server adoption where price-performance advantages are quantifiable. Taiwan's server ODM manufacturing base where Quanta, Wistron, and Inventec produce the majority of Arm server hardware for global hyperscale customers — creates Asia Pacific's commercial position at the manufacturing center of the Arm server supply chain.

Europe Arm-Based Servers Market Insights

Europe's Arm-Based Servers Market is growing with the European Processor Initiative (EPI) whose Rhea processor development program targets Arm-based high-performance computing for European scientific and commercial data centers and the progressive adoption of cloud Arm instances by European enterprises attracted by cost efficiency and the data sovereignty advantages of EU-hosted cloud Arm infrastructure. UK-based Arm Holdings' corporate headquarters sustains British engagement with Arm server ecosystem development, with Arm's architectural licensing model enabling UK-originated technology to underpin global server computing infrastructure.

MEA and Latin America Arm-Based Servers Market Insights

The Middle East's Arm-Based Servers Market is growing with the Gulf states' data center investment — where hyperscale cloud provider regional deployments in UAE, Saudi Arabia, and Qatar include Arm server infrastructure alongside x86 and the region's strategic interest in Arm's architecture as a non-U.S.-indigenous processor alternative. Latin America's market is developing as cloud adoption grows and as regional cloud providers evaluate Arm server economics for their cost-sensitive enterprise customer markets.

Arm-Based Servers Market Growth Drivers:

-

Hyperscale cloud provider validation and energy efficiency advantages driving sustained Arm-based servers market growth globally

The Arm-Based Servers Market is witnessing a period of significant growth due to the approval received from hyperscale cloud service providers as well as the inherent energy-efficient nature of Arm-based technology. Leading cloud service providers are increasingly deploying Arm servers as they lower energy usage while enhancing their efficiency and overall cost-effectiveness. This becomes especially important for high-volume data centers that require AI, analytics, and cloud capabilities. With increasing sustainability goals and compute requirements, Arm-based servers are being increasingly accepted around the world.

Arm-Based Servers Market Restraints:

-

Software ecosystem fragmentation and application recompilation barriers creating Arm-based servers market adoption challenges globally

The Arm server market's growth is constrained by the software ecosystem's incomplete coverage where enterprise applications written in languages whose compiled binaries require x86 instruction set compatibility create migration barriers for organizations whose application portfolios contain legacy x86-only executables. While interpreted language applications (Python, Java, JavaScript) run natively on Arm servers without recompilation, compiled language applications (C, C++, Fortran) require recompilation and re-testing whose IT cost and schedule impact creates adoption friction for organizations with large legacy application estates.

Arm-Based Servers Market Opportunities:

-

AI inference infrastructure and HPC scientific computing creating transformative Arm-based servers market growth opportunities globally

AI inference infrastructure represents the Arm server market's fastest-growing emerging application where NVIDIA's Grace Hopper and Grace Blackwell superchips combine Arm Cortex-A CPU clusters with Hopper and Blackwell GPU accelerators for the AI model serving infrastructure that cloud AI services require at hyperscale. Each AI inference rack whose CPU component is Arm-based rather than x86-based represents an Arm server adoption event whose unit value substantially exceeds conventional server procurement due to the premium compute integration that AI serving infrastructure requires. High-performance computing scientific applications where NVIDIA's Grace CPU and Arm's Neoverse V2 architecture achieve competitive performance at substantially lower power consumption than x86 HPC processors are attracting HPC center architects whose energy budget constraints make power efficiency a primary procurement criterion.

Recent Developments:

-

2026: AWS launched Graviton4 High Memory instances delivering 3 TB RAM configurations with Graviton4's 192 Arm Cortex-X4 cores for in-memory database and large-scale data analytics applications achieving 45% cost reduction versus equivalent Intel Xeon High Memory instances for SAP HANA and Redis cluster workloads, enabling enterprise database administrators to migrate in-memory workloads from on-premises x86 infrastructure to Arm cloud instances with documented TCO improvement that the Graviton4 architecture's memory bandwidth and core count achieves at AWS's manufacturing scale advantages over x86 processor suppliers.

-

2025: NVIDIA launched Grace Blackwell Superchip combining 72 Arm Neoverse V2 CPU cores with dual Blackwell GPU dies in a single NVLink-connected package achieving 30x performance improvement over equivalent CPU-GPU configurations for AI model fine-tuning workloads, positioning the superchip as the primary computing platform for the AI training and fine-tuning market segment whose compute requirements per dollar investment determines which organizations can economically develop proprietary AI models.

Arm-Based Servers Market Key Players

Some of the Arm-Based Servers Market Companies

-

Arm Holdings plc (Softbank Group)

-

Amazon Web Services Inc. (Graviton)

-

Ampere Computing LLC

-

NVIDIA Corporation (Grace CPU)

-

Apple Inc. (M-series)

-

Qualcomm Technologies Inc. (Centriq)

-

Huawei Technologies Co. Ltd. (Kunpeng)

-

Microsoft Corporation (Azure Cobalt)

-

Marvell Technology Inc. (ThunderX)

-

Fujitsu Limited (A64FX)

-

HPE (Hewlett Packard Enterprise)

-

Dell Technologies Inc.

-

Lenovo Group Ltd.

-

Supermicro Computer Inc.

-

Wiwynn Corporation

-

Quanta Computer Inc.

-

Inventec Corporation

-

Phytium Technology Co. Ltd.

-

Nuviatech Inc. (Qualcomm)

-

SiPearl SAS

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.98 Billion |

| Market Size by 2035 | USD 34.05 Billion |

| CAGR | CAGR of 14.32% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Operating System (32-bit, 64-bit) • By Core Architecture (ARM Cortex-A, ARM Cortex-M, Others) • By Application (Mobile Computing, Enterprise Servers, Edge Computing, High-Performance Computing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Arm Holdings (SoftBank Group), Amazon Web Services (Graviton), Ampere Computing, NVIDIA (Grace CPU), Apple (M-series), Qualcomm (Centriq), Huawei (Kunpeng), Microsoft (Azure Cobalt), Marvell (ThunderX), Fujitsu (A64FX), HPE, Dell Technologies, Lenovo Group, Supermicro, Wiwynn, Quanta, Inventec, Phytium, Nuviatech, and SiPearl SAS. |

| Company Profiles | Advanced Micro Devices, Inc., Ampere Computing LLC, ARM Limited, Cloud Software Group, Inc., Huawei Technologies Co., Ltd., Linaro Limited, Marvell, Red Hat, Inc., SUSE, Texas Instruments Incorporated, Qualcomm, Fujitsu, Supermicro, Hewlett Packard Enterprise (HPE), NVIDIA, Cavium (Now part of Marvell), Broadcom, Oracle, IBM, Samsung Electronics, Google, Microsoft |

Frequently Asked Questions

Ans: The Arm-Based Servers Market was valued at USD 8.98 billion in 2025.

Ans: North America leads; Asia Pacific is the fastest growing regional market.

Ans: 32-bit OS servers are growing fastest at approximately 17.48% CAGR; 64-bit dominated in 2025.

Ans: ARM Cortex-A dominated with approximately 81% share; ARM Cortex-M is growing fastest at 17.17% CAGR.

Ans: The Arm-Based Servers Market is expected to grow at a CAGR of 14.32% from 2026 to 2035.

Get in Touch