Artificial Intelligence in Healthcare Market Report Scope & Overview:

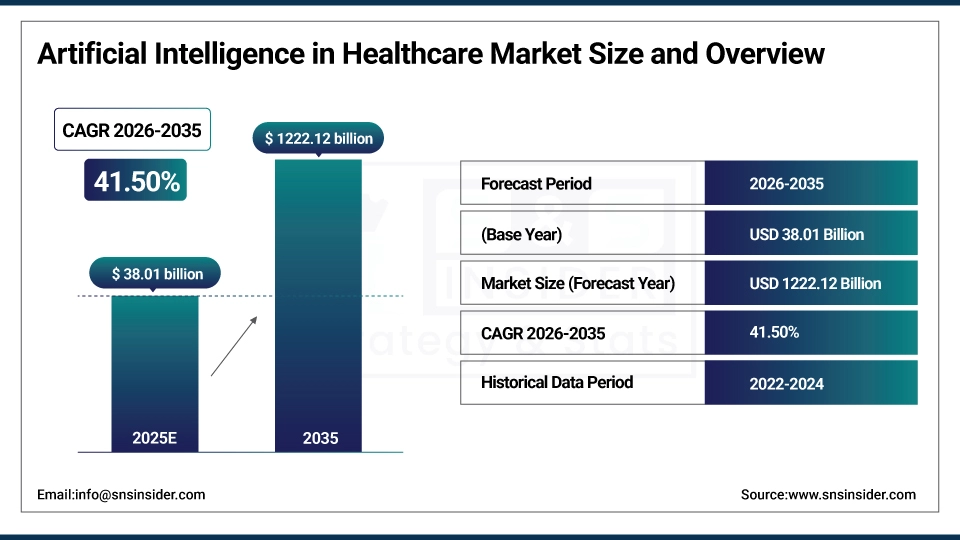

The Artificial Intelligence in Healthcare Market size is estimated at USD 38.01 Billion in 2025E and is expected to reach USD 1222.12 Billion by 2035, growing at a CAGR of 41.50% over the forecast period of 2026-2035.

Global artificial intelligence in healthcare market growth is fueled by the growing adoption of AI solutions for medical imaging and diagnostics, drug discovery, and personalized medicine. Rapid increase in the amount of healthcare data, lack of enough healthcare professionals, and increasing demand for improved patient outcomes are driving the implementation of AI in clinical and operational workflows. The significant investment by several technology giants and healthcare organizations, availability of supportive regulatory frameworks for AI-based medical devices, are providing a strong global market growth opportunities. The COVID-19 pandemic also fueled the digital transformation in healthcare industry and showcased that the role of artificial intelligence is vital in responding to pandemics, vaccine development efforts, and remote patient management.

In January 2025, 45 new AI/ML-enabled medical devices received FDA clearance, a 32% year to year increase that shows rapid acceleration of regulatory approval and clinical uptake of AI technologies in the health care environment.

Artificial Intelligence in Healthcare Market Size and Forecast:

-

Market Size in 2025E: USD 38.01 Billion

-

Market Size by 2033: USD 1222.12 Billion

-

CAGR: 41.50% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Artificial Intelligence in Healthcare Market - Request Free Sample Report

Artificial Intelligence in Healthcare Market Trends:

-

Wider use of AI algorithms for early disease detection and improving diagnostic accuracy by providing solutions for radiology, pathology, genomics, and many other use cases.

-

Generative AI to discover drugs, optimize clinical trials, and to synthetically generate patient data for research.

-

Growth of AI-based remote patient monitoring systems and wearable devices for chronic diseases and preventive health.

-

Increasing utilization of natural language processing for clinical documentation automation, medical coding and patient communication

-

Federated learning, will allow hospitals to train their AI models collaboratively without sharing data.

-

Rise in the robotic process automation for administrative tasks, claims processing, and revenue cycle management.

-

Introduction of multimodal AI systems that incorporate imaging, genomic and clinical data to go from patient profiling to a personalized treatment plan.

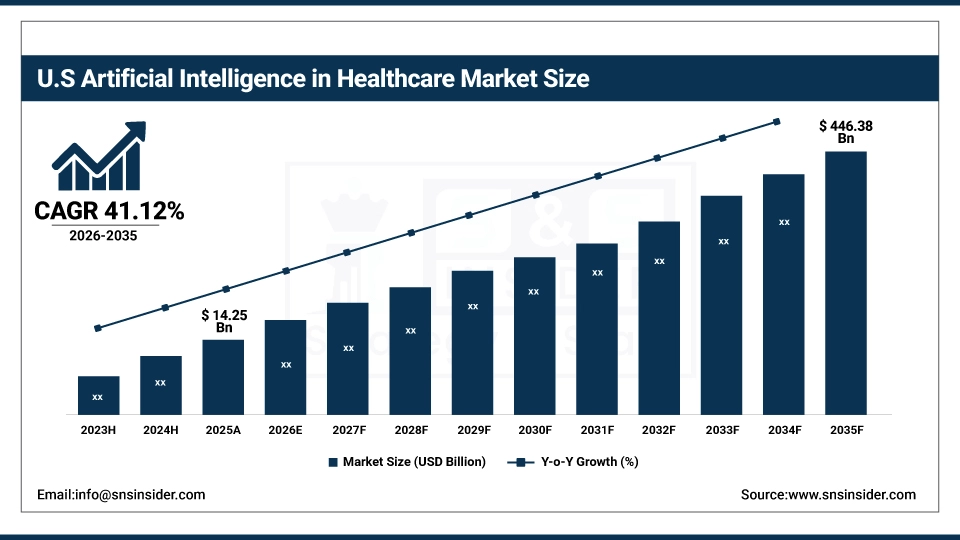

The U.S. Artificial Intelligence in Healthcare Market is estimated at USD 14.25 billion in 2025E and is expected to reach USD 446.38 billion by 2035, growing at a CAGR of 41.12% from 2026-2035. The U.S. holds the maximum market share as the U.S. artificial intelligence in the healthcare market is highly impacted by the advanced technological infrastructure, high R&D expenditure, and the presence of world-leading AI technology companies and health care organizations. Rising government support for digital health innovation, higher per capita healthcare expenditure, and quick adoption of electronic health records and cloud-based healthcare system are boosting the market growth.

Artificial Intelligence in Healthcare Market Growth Drivers:

-

Advancements in Medical Imaging & Diagnostics AI Solutions Driving Market Growth

Technological advancements in AI-powered medical imaging and diagnostic solutions is a key factor driving the growth of the global artificial intelligence in healthcare market. Image analysis by deep learning algorithms improves accuracy and speed in radiology, pathology, and in ophthalmology, leading to less diagnostic errors and earlier detection of diseases. AI implementation within PACS systems and specifically FDA-cleared diagnostic algorithms have hastened clinical adoption. By alleviating the increasing shortage of radiologists and utilizing workflow efficiencies, these solutions will aid healthcare providers in delivering higher imaging throughputs without compromising on diagnostic quality.

For example, in March 2025, top hospital networks reported an average time reduction of 40% in the interpretation of chest X-rays and CT scans using AI-assisted diagnostic systems, helping radiologists boost productivity and increase patient throughput.

Artificial Intelligence in Healthcare Market Restraints:

-

Data Privacy Concerns and Regulatory Compliance Challenges Restricting Market Expansion

Concerns related to data privacy and regulatory compliance for artificial intelligence in the healthcare industry are major factors that hinder the growth of the artificial intelligence in the healthcare industry market. Sensitivity of healthcare data, differences in data protection regulations across various international boundaries (GDPR, HIPAA), and confidentiality of patient information are some factors that hinder the growth of the market by creating obstacles in the sharing of data required for training AI models.

Artificial Intelligence in Healthcare Market Opportunities:

-

AI-Driven Drug Discovery and Precision Medicine Creating Transformative Market Opportunities

The growth of AI in drug discovery and precision medicine offers large market opportunities. AI algorithms speed up target identification, compound screening, and clinical trial design, shortening the pharmaceutical R&D timeline from years to months. Genomic, proteomic and clinical data-driven machine learning models allow truly personalization therapy based on a patient’s unique profile. The intersection of AI and CRISPR gene editing, multi-omics data merging, and real-world evidence generation creates possibilities never before existed for the development of precision therapeutics for complex diseases such as cancer, neurodegenerative diseases, or rare genetic disorders.

For example, in February 2025, an AI-based drug discovery solution was able to identify three new targets in oncology in less than six months, with one of them progressing to Phase I clinical trials, thus proving the revolutionary use of AI in speeding up drug development.

AI in Healthcare Market Segment Analysis:

-

By component, Software solutions accounted for the largest share of 48.67% in 2025, and the service segment is anticipated to exhibit the fastest growth, at a CAGR of 43.28%.

-

By application, the medical imaging & diagnostics segment has registered the highest market share of about 26.35% in 2025, followed by the drug discovery & development segment, which is anticipated to register the highest CAGR of 44.76%.

-

By technology, machine learning had the highest market share of about 52.41% in 2025E, and is projected to grow at the highest rate, with a CAGR of 42.15%.

-

By end use, healthcare providers led the market with a share of nearly 58.29% in 2025E, while the healthcare companies segment is expected to be the fastest-growing segment with A CAGR of 43.52%.

By Application, Medical Imaging & Diagnostics Dominates, While Drug Discovery & Development Shows Rapid Growth

The medical imaging & diagnostics market held the largest revenue share of around 26.35% in 2025 as Artificial Intelligence has seen a very high acceptance in radiology departments and pathology labs & diagnostic centers. The growth of this market is mainly attributed to the increasing number of medical imaging procedures, shortage of radiologists, and proven ability of AI to improve the accuracy and efficiency of diagnostics. From 2026 to 2035, the drug discovery & development market is anticipated to witness the highest CAGR of 44.76%, specifically attributed to the critical need for pharmaceutical industry to reduce R&D costs, as well as shorten the time-to-market for new pharmaceuticals. This market is primarily driven by AI-enabled analysis of complex biological data, prediction of compound efficacy and toxicity, and multi-omics data integration to discover new drug targets.

By Component, Software Solutions Leads the Market, While Services Registers Fastest Growth

In 2025, the software solutions segment contributed more than 48.67% revenue share owing to the adoption of AI platforms and tailored solutions for clinical decision support, imaging analysis, administrative automation, and other areas respectively. The rise of cloud-based AI solutions, enhances integration with existing healthcare IT infrastructure, and pre-trained models for specific medical applications are major enablers. On the other hand, the services segment, which is led by implementation, consulting, maintenance, and training services, is expected to record the highest CAGR of almost 43.28% between 2026 and 2035. The expansion is driven by the requirement of healthcare organizations to hire high-quality specialists for AI deployment, the customization of the solution to a specific clinical workflow, and the continuous optimization of AI systems.

By Technology, Machine Learning Leads and Registers Fastest Growth

The machine learning portion of the market represented the largest share of the artificial intelligence in the healthcare market with around 52.41%, due to its adaptability to a wide range of applications in the healthcare industry, such as predictive analytics, medical image pattern recognition, and risk stratification models. The critical drivers of this market include improvements in algorithms, the availability of large labeled datasets in the healthcare industry, and successful clinical validation in a wide range of specialties. This market is expected to grow at the highest rate with a CAGR of around 42.15% over the forecast period of 2026-2035, as the complexity and specialization of deep learning models continue to advance in the healthcare industry.

By End Use, Healthcare Providers Lead, While Healthcare Companies Segment Grows the Fastest

The healthcare providers category held the largest revenue share of 58.29% in the artificial intelligence in healthcare market in 2025, on account of huge investments made by hospitals and healthcare systems on AI solutions for clinical decision support, operational efficiency, and patient experience enhancement. This will be driven by the need to improve care quality metrics, reduce clinical errors and optimize resource utilization in value-based care models. However, is anticipated to observe the highest CAGR of 43.52% during the forecasted period of 2026-2035 in the under category of healthcare companies owing to the rising use of AI from pharmaceutical and biotechnology companies over the full drug development value chain. These forces include the exponential expansion of genomic and drug discovery data, the urgency for R&D efficiency gains, and the push to trump the competition to market with first-in-class AI therapeutics.

Artificial Intelligence in Healthcare Market Regional Highlights:

Asia Pacific Artificial Intelligence in Healthcare Market Insights:

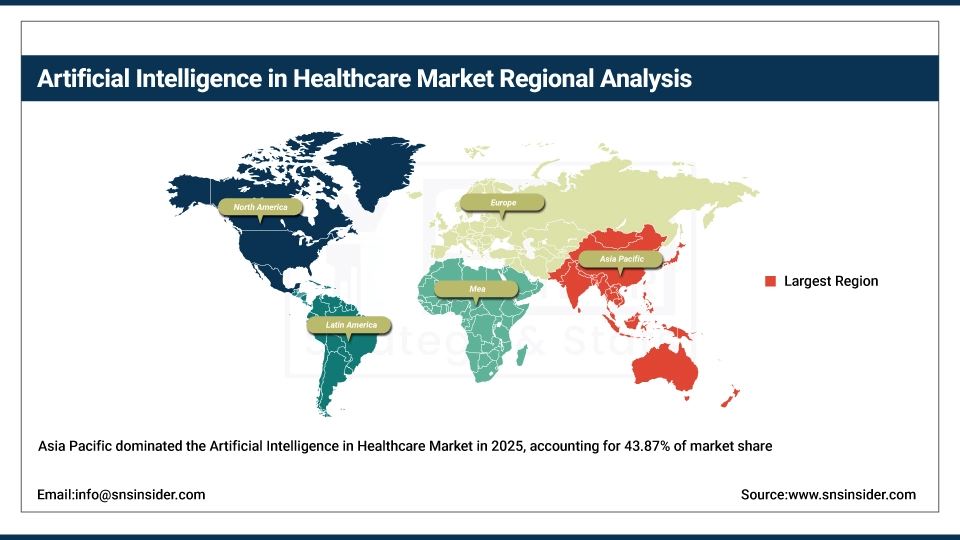

The Asia Pacific market is the fastest-growing regional market, with a CAGR of 43.87%, due to the massive healthcare digitization projects, increasing numbers of medical imaging procedures, and significant government investments in AI infrastructure. The key factors include the massive patient bases in China and India, which create a huge amount of healthcare data, the rising incidence of chronic diseases that demand sophisticated diagnostic capabilities, and the proactive regulatory frameworks that foster innovation in AI. The region has a robust technology infrastructure, substantial venture capital investments in health-tech startups, and joint efforts between academic and healthcare organizations to develop region-specific AI solutions for the varied healthcare needs of the population.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Artificial Intelligence in Healthcare Market Insights:

The artificial intelligence in healthcare market in North America has showed highest revenue share of 44.52% in 2025 owing to presence of developed healthcare IT infrastructure, high healthcare spending and early adoption of novel technologies. The key enablers are existence of world leading AI tech companies, world-leading AMIs conducting AI research and favorable AI diagnostic reimbursement policies. It is also halfway accessible to vast amounts of venture capital pouring into healthcare AI startups, collaborations between technology leaders and healthcare institutions and forward-thinking FDA guidelines on accelerated medical device approvals for AI/ML-enabled products.

Europe Artificial Intelligence in Healthcare Market Insights:

European region accounts for second most dominant market for artificial intelligence in healthcare after North America. Solid government backing for digital health, the availability of rich patient data through a universal healthcare system and global-leading research institutes in the development of state-of-the-art AI for health care are all driving forces behind our discovery. Reasons for the growth of artificial intelligence in healthcare market in Europe are coordinated approach to health data spaces in EU, transnational collaboration on AI research projects, and AI solutions for challenges of the healthcare workforce and the aging population.

Latin America (LATAM) and Middle East & Africa (MEA) Artificial Intelligence in Healthcare Market Insights:

Artificial Intelligence in Healthcare Market in Latin America & Middle East & Africa would be driven by increasing investments in healthcare infrastructure, increasing penetration of smartphones enabling digital healthcare, and government initiatives to increase access to healthcare. The major factors for growing include applications for telemedicine which produce data for evaluation by AI, working with international tech firms to deploy AI models, and emphasis on affordable healthcare delivery through AI. There is an increasing number of start-ups across the regions developing health-tech applications of AI that is relevant to the regions' disease epidemiology and healthcare infrastructure.

AI in Healthcare Market Competitive Landscape:

IBM Watson Health (founded in 2015) utilizes the strong AI capabilities of IBM to provide cognitive computing solutions for healthcare institutions, especially in the areas of oncology, genomics, and population health management using its Watson platform and cloud-based AI services.

-

In February 2025, developed an improved clinical trial matching platform using natural language processing to interpret electronic health records, improving patient enrollment efficiency by 35% for cancer research institutions.

Google Health (founded in 2018) utilizes Google's expertise in AI, data analytics, and machine learning to address healthcare issues, focusing on medical image analysis, disease prediction models, and healthcare data management through partnerships with large healthcare institutions.

-

In November 2024, developed a multimodal AI platform for diabetic retinopathy detection by integrating retinal scans with electronic health record data, demonstrating 98.5% accuracy in clinical validation studies for varied populations.

Microsoft Healthcare (founded in 2017) combines its AI capabilities on its cloud platform to enable healthcare institutions with solutions for clinical decision support, medical image analysis, and operational optimization using Azure-based AI services and industry solutions.

-

In January 2025, expanded its AI model catalog with 15 new healthcare-specific models for rare disease diagnosis and treatment recommendation, accessible through Azure AI for regulated healthcare workloads.

Artificial Intelligence in Healthcare Market Key Players:

-

IBM Watson Health

-

Google Health

-

Microsoft Healthcare

-

NVIDIA Corporation

-

Intel Corporation

-

Amazon Web Services (AWS)

-

Oracle Corporation

-

Siemens Healthineers

-

GE Healthcare

-

Philips Healthcare

-

Johnson & Johnson

-

Medtronic

-

Roche Diagnostics

-

Qiagen

-

Tempus Labs

-

Butterfly Network

-

PathAI

-

Caption Health

-

Zebra Medical Vision

-

HeartFlow

-

Insilico Medicine

-

BenevolentAI

-

Owkin

-

DeepMind

-

Verily Life Sciences

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 38.01 Billion |

| Market Size by 2035 | USD 1222.12 Billion |

| CAGR | CAGR of 41.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software Solutions, Services) • By Application (Robot-assisted Surgery, Virtual Assistants, Administrative Workflow Assistants, Connected Medical Devices, Medical Imaging & Diagnostics, Clinical Trials, Fraud Detection, Cybersecurity, Dosage Error Reduction, Precision Medicine, Drug Discovery & Development, Lifestyle Management & Remote Patient Monitoring, Wearables, Others (Patient Engagement, etc.)) • By Technology (Machine Learning, Natural Language Processing) • By End-users (Healthcare Providers (Hospitals, Outpatient Facilities, and Others), Healthcare Payers, Healthcare Companies (Pharmaceutical, Biotechnology, Medical Devices), Patients, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IBM Watson Health, Google Health, Microsoft Healthcare, NVIDIA Corporation, Intel Corporation, Amazon Web Services (AWS), Oracle Corporation, Siemens Healthineers, GE Healthcare, Philips Healthcare, Johnson & Johnson, Medtronic, Roche Diagnostics, Qiagen, Tempus Labs, Butterfly Network, PathAI, Caption Health, Zebra Medical Vision, HeartFlow, Insilico Medicine, BenevolentAI, Owkin, DeepMind, Verily Life Sciences |

Frequently Asked Questions

North America dominated the market, holding the highest revenue share of 44.52% in 2025.

The Machine Learning segment dominated the market with a share of about 52.41% in 2025.

Advancements in AI-powered Medical Imaging & Diagnostics Solutions are a key factor driving the market growth.

Ans: The Artificial Intelligence in Healthcare Market size is estimated at USD 38.01 billion in 2025 and is expected to reach USD 1222.12 billion by 2035.

The Artificial Intelligence in Healthcare Market is expected to grow at a CAGR of 41.50% over the forecast period.

Get in Touch