Artificial Intelligence (AI) in Pharmaceutical Market Report Scope & Overview:

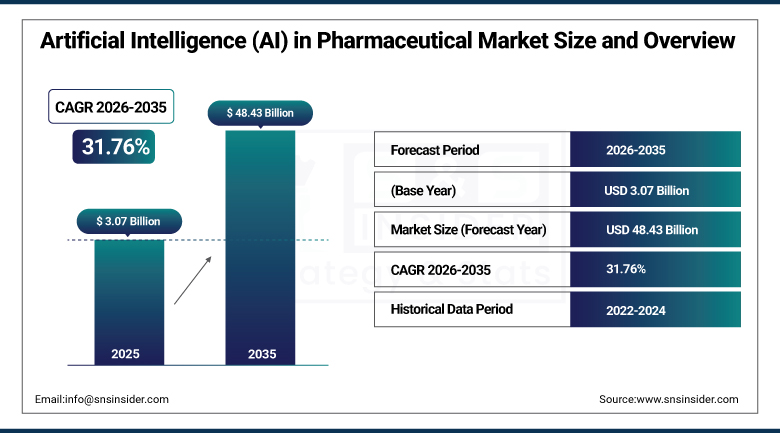

The Artificial Intelligence (AI) in Pharmaceutical Market was valued at USD 3.07 Billion in 2025 and is expected to reach USD 48.43 Billion by 2035, growing at a CAGR of 31.76% from 2026 to 2035.

Artificial Intelligence in the Pharmaceutical Industry is progressing at an ever increasing pace, thanks to the funding for venture capital, regulations, and advances in protein folding model development. Instead of investing in chemically altering drugs, investment dollars are now pouring into data science. The adaptive trial technology is already helping to cut down the recruitment process time by about forty percent, while pharmacovigilance technologies make use of data mining from electronic health records to meet their post-marketing obligations. Several drug development firms have already made use of wearable devices that employ AI algorithms to keep remote track of patients with life-threatening diseases.

The United States Food and Drug Administration qualified AIM-NASH in December 2025 as its first machine-learning biomarker, confirming an agency shift from cautious observation to active endorsement of algorithmic drug-development tools and setting a regulatory precedent that continues encouraging broader pharmaceutical industry investment in AI-driven development platforms.

Market Size and Forecast

- Market Size in 2026E: USD 4.05 Billion

- Market Size by 2035: USD 48.43 Billion

- CAGR: 31.76% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

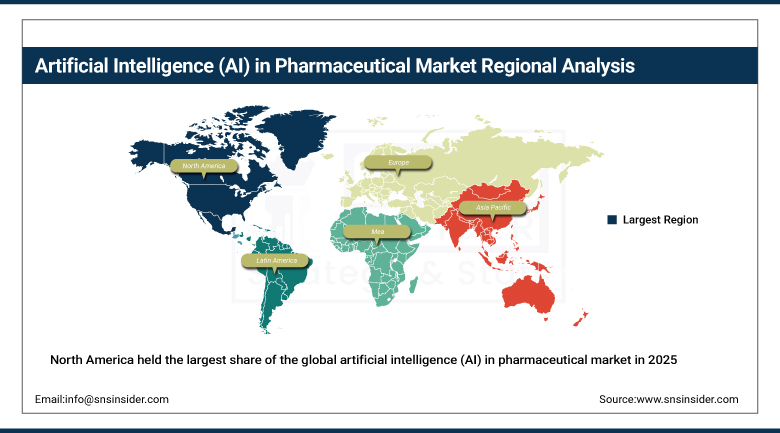

- Largest Region: North America

To Get more information On Artificial Intelligence (AI) in Pharmaceutical Marke - Request Free Sample Report

Artificial Intelligence (AI) in Pharmaceutical Market Trends

- Venture funding is redirecting research and development capital toward data-centric AI platforms rather than incremental chemistry approaches.

- Adaptive-trial algorithms are cutting clinical enrollment timelines by roughly forty percent across pharmaceutical development programs.

- Pharmacovigilance engines are mining electronic health records in near real time to meet post-market surveillance mandates.

- Generative protein-folding models continue advancing drug discovery capability well beyond traditional chemistry-based approaches.

- Regulatory bodies are shifting from cautious observation toward active endorsement of algorithmic drug-development tools.

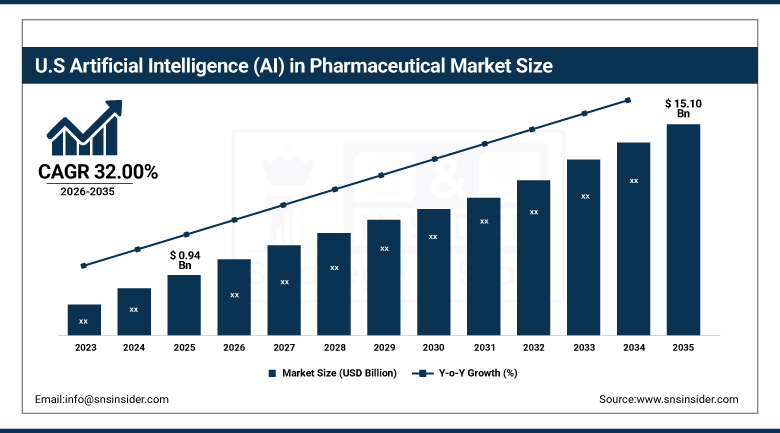

The United States Artificial Intelligence (AI) in Pharmaceutical Market Outlook

The United States Artificial Intelligence (AI) in Pharmaceutical Market was valued at USD 0.94 Billion in 2025 and is expected to reach USD 15.10 Billion by 2035, growing at a CAGR of 32.00% from 2026 to 2035.

The USA had a leading market share in North American AI pharmaceuticals due to the availability of major pharmaceutical firms in the country along with the well-developed infrastructure for health care. The country remained one of the top commercially valuable national markets for this kind of technology all throughout the year due to the continual support of regulation regarding algorithmic drug development.

The drug discovery startup company Isomorphic Labs founded by Alphabet through Google DeepMind received funding to the tune of $1 billion in 2025, which clearly shows investors' confidence that AI-first pharma pipelines will outdo traditional chemistry-based drug discovery methods.

Artificial Intelligence (AI) in Pharmaceutical Market Segmentation Analysis

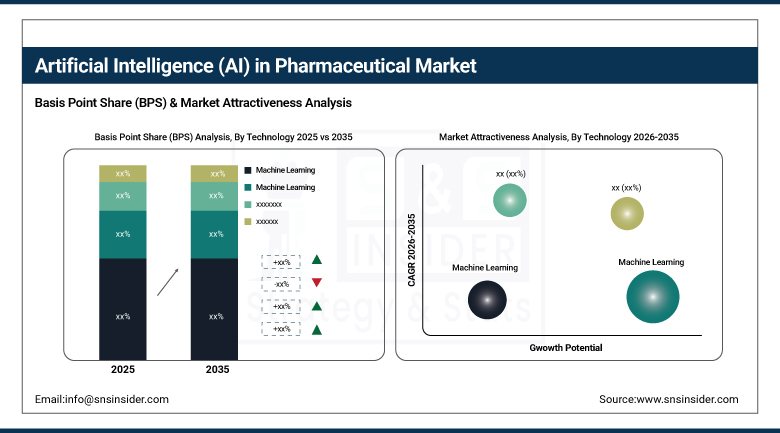

- By Technology, the machine learning segment held approximately 38.21% share in 2025, while the generative AI segment is the fastest growing, with a CAGR of approximately 42.31%.

- By Offering, the software platforms segment held approximately 45.32% share in 2025, while the AI-as-a-service segment is the fastest growing, with a CAGR of approximately 43.78%.

- By Application, the drug discovery pre-clinical development segment held approximately 34.42% share in 2025, while the pharmacovigilance safety monitoring segment is the fastest growing, with a CAGR of approximately 43.65%.

- By Deployment Mode, the cloud segment held approximately 67.72% share in 2025, while the on-premises hybrid segment is the fastest growing, with a CAGR of approximately 42.76%.

By Technology, machine learning led the market, generative AI grew fastest

The machine learning segment dominated the technology category in 2025, holding approximately 38.21% of total revenue, anchored by established algorithms that continue powering the majority of current drug discovery, clinical trial optimization, and safety monitoring applications. That established analytical foundation keeps machine learning firmly at the top of the broader technology segmentation across nearly every current AI in pharmaceutical deployment.

The generative AI segment is projected to grow at the fastest CAGR of approximately 42.31% during the forecast period, propelled by rapid advances in generative protein-folding models that continue redirecting research and development capital toward data-centric platforms instead of incremental chemistry tweaks. That fundamental shift in drug discovery methodology continues pushing generative AI adoption well ahead of the broader technology segmentation.

By Offering, software platforms led the market, AI-as-a-service grew fastest

The software platforms segment held the largest offering share in 2025, at approximately 45.32%, anchored by licensable AI platforms that pharmaceutical companies integrate directly into their existing research and development workflows. That direct integration capability keeps software platforms firmly at the top of the broader offering segmentation across nearly every major pharmaceutical AI deployment.

The AI-as-a-service segment is projected to grow at the fastest CAGR of approximately 43.78% during the forecast period, as smaller biotech firms and startups increasingly favor consumption-based access to sophisticated AI capability over building or licensing dedicated software platforms outright. Rising demand for flexible, scalable AI access continues pushing this offering category's growth rate ahead of the broader offering segmentation.

By Application, drug discovery pre-clinical development led the market, pharmacovigilance safety monitoring grew fastest

The drug discovery pre-clinical development segment held the largest application share in 2025, at approximately 34.42%, as pharmaceutical companies increasingly rely on AI-discovered molecules that demonstrate substantially higher phase one success rates than traditional discovery approaches. That improved success rate continues keeping drug discovery firmly at the center of overall AI in pharmaceutical demand across nearly every major biopharmaceutical program.

The pharmacovigilance safety monitoring segment is projected to grow at the fastest CAGR of approximately 43.65% during the forecast period, as pharmacovigilance engines increasingly mine electronic health records in near real time to meet post-market surveillance mandates. Rising regulatory emphasis on continuous safety monitoring continues pushing this application category's growth rate well ahead of the broader application segmentation.

By Deployment Mode, cloud led the market, on-premises hybrid grew fastest

The cloud segment dominated the deployment mode category in 2025, holding approximately 67.72% of total revenue, favored for the scalable computing resources that AI model training and inference workloads demand without requiring substantial in-house infrastructure investment. That scalability advantage keeps cloud deployment firmly at the top of the broader deployment mode segmentation across the majority of pharmaceutical AI applications worldwide.

The on-premises hybrid segment is projected to grow at the fastest CAGR of approximately 42.76% during the forecast period, as pharmaceutical companies handling particularly sensitive proprietary research data increasingly favor hybrid architectures that balance cloud scalability with on-premises data control. Rising data security concerns continue pushing this deployment mode category's growth rate ahead of the broader deployment mode segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.90% |

|

Europe |

Germany |

27.60% |

|

Asia Pacific |

China |

37.40% |

|

Middle East & Africa |

UAE |

27.80% |

|

Latin America |

Brazil |

37.20% |

North America Artificial Intelligence (AI) in Pharmaceutical Market Insights

North America held the largest share of the global artificial intelligence (AI) in pharmaceutical market in 2025, supported by the presence of leading pharmaceutical companies and advanced healthcare infrastructure across the region. Continued venture capital investment in AI-first pharmaceutical pipelines kept the region firmly ahead of every other region in this market throughout the year.

The U.S. held an 86.90% market share for the regional revenue, owing to the presence of leading pharmaceutical and AI technology companies. Canada added a lower market share for regional revenue, but this market share was rising due to the existence of biotech research companies in Canada, making North America the top leader in this market over all others.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Artificial Intelligence (AI) in Pharmaceutical Market Insights

Europe held a substantial share of the global artificial intelligence (AI) in pharmaceutical market in 2025, supported by strong pharmaceutical manufacturing and growing biotechnology research investment across the continent. Germany accounted for roughly 27.60% of regional revenue, supported by its concentration of pharmaceutical companies and life sciences research institutions integrating AI into drug development workflows.

France, the United Kingdom, and Switzerland followed a broadly similar trajectory, as continued pharmaceutical research investment extended AI adoption across the continent's largest biopharmaceutical markets. Continued regulatory support for algorithmic drug-development tools is expected to keep supporting steady European demand through the remainder of the forecast period.

Asia Pacific Artificial Intelligence (AI) in Pharmaceutical Market Insights

Asia Pacific was the fastest-growing region in the global artificial intelligence (AI) in pharmaceutical market, driven by rapid growth of biotechnology research and healthcare investments across the region's largest and most populous economies. Rising government investment in domestic AI and pharmaceutical research capability continued driving regional demand at a pace considerably faster than more mature Western markets.

China accounted for roughly 37.40% of regional revenue, supported by aggressive government investment in domestic AI and biotechnology research infrastructure. Japan and South Korea contributed significant additional regional demand through their own advanced pharmaceutical and AI research sectors, reinforcing Asia Pacific's position as the clear growth leader in this market.

MEA & Latin America Artificial Intelligence (AI) in Pharmaceutical Market Insights

In 2025, the Middle East and Africa region experienced consistent growth in the use of AI in the pharmaceutical sector owing to increasing efforts towards biotechnology research and increased government funding for innovation within the health industry in the Gulf countries in particular. The UAE represented around 27.80% of the revenues generated in the region, thanks to technology diversification policies within the country.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.20% of regional revenue, where growing pharmaceutical research investment continued to support category growth. Mexico and Argentina followed a similar trajectory as regional biotechnology research infrastructure expanded further through the remainder of the forecast period.

Growth Drivers: Regulatory endorsement and adaptive trial efficiency gains

Venture funding, regulatory endorsements, and rapid advances in generative protein-folding models continue redirecting research and development capital toward data-centric AI platforms instead of incremental chemistry tweaks. Adaptive-trial algorithms already cutting enrollment timelines by roughly forty percent continue demonstrating measurable efficiency gains that keep pharmaceutical companies investing further in AI-driven clinical development.

Increasing awareness of artificial intelligence among pharma manufacturers and rising adoption of AI in the pharmaceutical market for research and development activities and drug development continue driving sustained industry growth. Pharmacovigilance engines mining electronic health records in near real time to meet post-market surveillance mandates continue reinforcing structural demand growth across nearly every major pharmaceutical AI application category worldwide.

Restraints: Data quality challenges and algorithmic validation requirements

Achieving genuinely reliable AI model performance requires access to high-quality, comprehensive clinical and research datasets that remain fragmented and inconsistently structured across many pharmaceutical organizations. That data quality challenge continues limiting how quickly some pharmaceutical companies can deploy AI capability at meaningful scale.

Rigorous regulatory validation requirements for AI-driven drug development tools, while increasingly supportive following recent qualification precedents, continue requiring substantial evidence generation before algorithmic tools can be fully integrated into regulated development workflows. That validation burden continues adding time and cost to AI deployment even as the underlying regulatory environment grows more favorable.

Opportunities: AI-as-a-Service expansion and precision medicine applications

Growing demand for AI-as-a-Service offerings presents substantial opportunity for providers positioned to serve smaller biotech firms and startups seeking flexible, consumption-based access to sophisticated AI capability. Providers capable of delivering scalable, accessible AI infrastructure stand to capture a growing share of demand from resource-constrained organizations that cannot justify building dedicated in-house platforms.

The growing importance of precision medicine and increased investment in research and development for AI technology applications presents a further significant growth avenue, as drugmakers face increasing demand to reduce drug prices while reducing clinical trial failure rates. Companies capable of delivering genuinely predictive, cost-reducing AI capability stand to capture meaningful new revenue streams through 2035.

Recent Developments:

- 2025: Xaira Therapeutics secured a billion-dollar funding round, reflecting strong capital market confidence that AI-first pharmaceutical pipelines will outpace traditional chemistry-based drug development approaches.

- 2025: NVIDIA Corporation continued expanding its computing infrastructure partnerships with pharmaceutical companies, supporting the specialized processing power required for generative protein-folding models and large-scale drug discovery AI training.

- 2025: Recursion Pharmaceuticals continued advancing its AI-driven drug discovery platform following its merger integration, strengthening its position in applying machine learning to identify novel therapeutic candidates across multiple disease areas.

Artificial Intelligence (AI) in Pharmaceutical Market key players are:

- AstraZeneca plc

- Atomwise Inc.

- Bayer AG

- Cloud Pharmaceuticals Inc.

- GNS Healthcare, Inc.

- IBM Corporation

- Merck & Co., Inc.

- Microsoft Corporation

- Novartis AG

- NVIDIA Corporation

- Pfizer Inc.

- Recursion Pharmaceuticals, Inc.

- XtalPi Inc.

- Isomorphic Labs Limited

- Insitro, Inc.

- Insilico Medicine

- Schrödinger, Inc.

- Xaira Therapeutics, Inc.

- BenevolentAI Ltd.

- Tempus AI, Inc.

Artificial Intelligence (AI) in Pharmaceutical Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.07 Billion |

| Market Size by 2035 | USD 48.43 Billion |

| CAGR | CAGR of 31.76% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Machine Learning, Generative AI) • By Offering (Software Platforms, AI-as-a-Service) • By Application (Drug Discovery Pre-Clinical Development, Pharmacovigilance Safety Monitoring) • By Deployment Mode (Cloud, On-Premises Hybrid) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AstraZeneca plc, Atomwise Inc., Bayer AG, Cloud Pharmaceuticals Inc., GNS Healthcare, Inc., IBM Corporation, Merck & Co., Inc., Microsoft Corporation, Novartis AG, NVIDIA Corporation, Pfizer Inc., Recursion Pharmaceuticals, Inc., XtalPi Inc., Isomorphic Labs Limited, Insitro, Inc., Insilico Medicine, Schrödinger, Inc., Xaira Therapeutics, Inc., BenevolentAI Ltd., Tempus AI, Inc. |

Frequently Asked Questions

The Artificial Intelligence (AI) in Pharmaceutical Market is expected to grow at a CAGR of 31.76% from 2026 to 2035.

The Artificial Intelligence (AI) in Pharmaceutical Market was valued at USD 3.07 Billion in 2025.

North America held the largest share of the Artificial Intelligence (AI) in Pharmaceutical Market in 2025, while Asia Pacific was the fastest-growing region.

The Machine Learning segment held approximately 38.21% share in 2025.

Venture funding and regulatory endorsement combined with adaptive-trial algorithms cutting enrollment timelines is the major growth factor.

Get in Touch