Recanalization Devices Market Size & Trends:

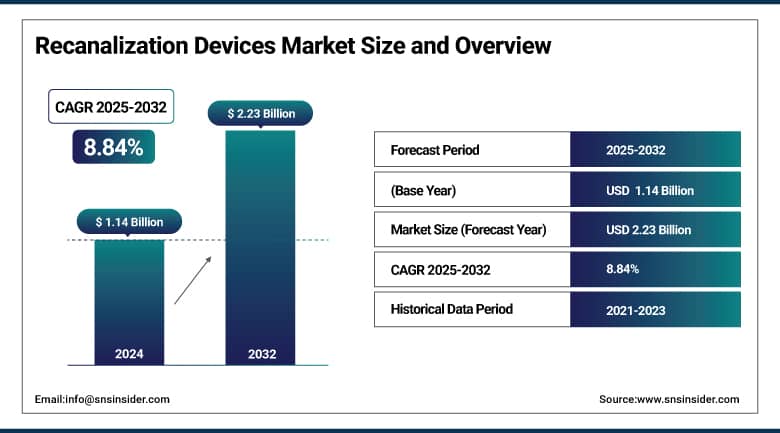

The Recanalization Devices Market size was valued at USD 1.14 billion in 2024 and is expected to reach USD 2.23 billion by 2032, growing at a CAGR of 8.84% over the forecast period of 2025-2032.

The global recanalization devices market is expected to grow steadily due to the increasing global prevalence of cardiovascular diseases, peripheral diseases, and neurovascular occlusive diseases. The increased demand for hybrid recanalization techniques, coupled with the rising accessibility to stroke and cardiac care, along with technological advancements in minimally invasive procedures, are the major factors contributing to the growth of the market. Furthermore, rising investment in the healthcare infrastructure, primarily in Asia-Pacific and Latin America, is promoting the adoption of devices.

To Get More Information On Recanalization Devices Market - Request Free Sample Report

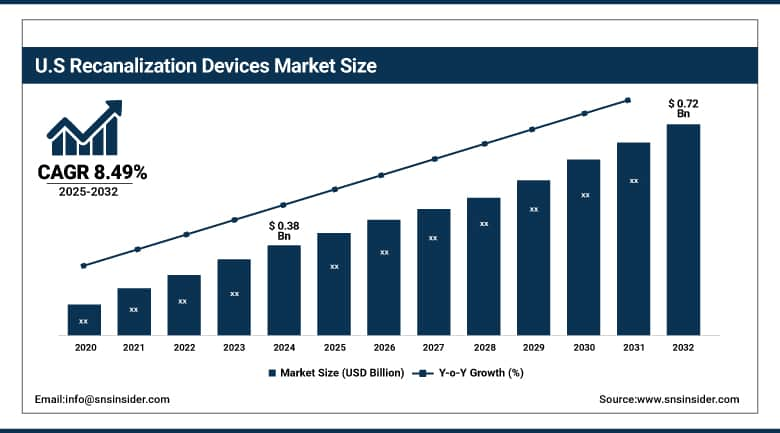

The U.S. Recanalization Devices Market size was valued at USD 0.38 billion in 2024 and is expected to reach USD 0.72 billion by 2032, growing at a CAGR of 8.49% over the forecast period of 2025-2032.

North America dominates the recanalization devices market due to the presence of advanced healthcare infrastructure and high healthcare expenditure in the U.S., as well as road density and concentration of key manufacturers and centers offering clinical services. The clear dominance in the global market is substantiated further due to a rapidly aging population, which increasingly requires vascular interventions, and ultimately, leading to strong demand for recanalisation devices both in the coronary and neurovascular segments.

Recanalization Devices Market Dynamics:

Drivers

- Increasing Prevalence of Cardiovascular and Neurovascular Disorders is Driving the Market Growth

Abstract Cardiovascular diseases (CVD), such as coronary artery disease and stroke, are some of the leading causes of death globally. Cardiovascular diseases (CVDs) are responsible for nearly 17.9 million deaths each year throughout the globe, the World Health Organisation (WHO) reported. Aging populations and a growing burden of lifestyle-associated risk factors, including high blood pressure, diabetes, and smoking, are leading to increases in ischemic stroke, the condition caused by impeded blood flow to the brain. Such conditions often urgently necessitate recanalization, or opening blocked arteries. Since the incidence of these diseases is increasing, the need for devices such as stents, catheters, and guidewires is also increasing, which is leading to significant recanalization device market growth.

- Advancements in Minimally Invasive Recanalization Technologies are Propelling the Market Growth

The landscape of vascular interventions has changed with recent technological advancements. These innovations, drug-eluting stents, steerable guidewires, aspiration catheters, and microcatheters, enable clinicians to access and treat complex lesions with unprecedented precision, thereby minimizing trauma to surrounding tissues. These innovations have led to better procedural outcomes, shorter length of stay, and broader applicability across a wider range of patients previously deemed high-risk. The global recanalization devices market continues to gain momentum as healthcare providers are progressively switching to advanced tools that provide a better safety profile, a rapid recovery period, and growing confidence in the clinical field towards minimally invasive techniques.

Restraint

- Risk of Procedural Complications is Restraining the Market from Growing

Recanalization procedures have associated clinical risks, in particular for more challenging anatomical sites such as coronary and cerebral arteries, which often leads clinicians and patients to avoid undertaking them. Possible complications are perforation of vessels, distal embolization, appearance of dissection of the arteries, re-occlusion, and in-stent restenosis. Improper positioning or over manipulation during neurovascular recanalization, for instance, may cause hemorrhagic stroke or aggravated ischemia. Likewise, complex or chronic total occlusions (CTOs) in coronary recanalization have a higher risk of failure or major adverse cardiovascular events. These risks breed more caution in the patient selection process by providers, and in some cases, the selection of conservative management over device-based intervention. Consequently, safety-related uncertainties can restrict the growth of recanalization devices market trends, specifically in environments with weaker surgical backup or advanced post-procedural care.

Recanalization Devices Market Segmentation Analysis:

By End User

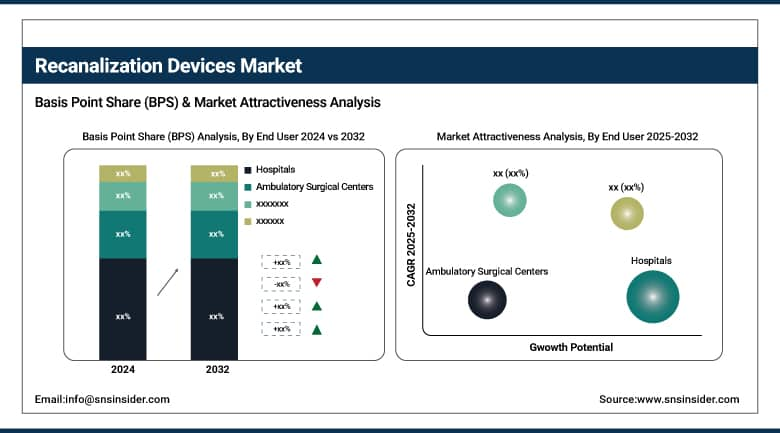

The hospitals segment held the leading share of the 2024 recanalization devices market with a 64.12% market share, owing to the availability of well-established infrastructure, advanced imaging capabilities, and the presence of multidisciplinary teams required for performing complex vascular procedures. Hospitals are usually the main STBs for acute interventions, known as recanalization, and most commonly stroke or coronary artery blockages, which are time-sensitive and high-risk. Moreover, the crucial requirement for ICUs, skilled interventionists, and post-operative monitoring systems is also avails directly to augment its maximum share in the market.

The Ambulatory Surgical Centers (ASCs) segment is expected to have a prominent growth rate in the forecast years as the healthcare industry continues to expand cost-effective, outpatient-based treatment. Because ASCs have shorter wait times, lower procedural costs, and improved recovery times, they may be appealing alternatives for selected recanalization procedures (especially peripheral interventions). In addition, ASCs are increasingly adopting and implementing recanalization devices owing to the expansion of procedural capabilities such as minimally invasive technologies, coupled with favorable regulatory trends towards outpatient vascular care.

By Product Type

The 2024 recanalization devices market was dominated by the stents segment with a 61.23% market share due to the most essential and widely used devices for restoring blood flow in a narrowed or blocked artery, either coronary or peripheral vascular. Stents are widely used because they effectively open and keep vessels open after the procedure and prevent the newly treated area from narrowing again (restenosis). As specialty clinics and hospitals increasingly use drug-eluting and bioresorbable stents, as cardiovascular diseases become more rampant across the globe, and the demand for minimally invasive interventions continues to rise, industry leaders are expected to strengthen their market holdings in 2024.

The guidewires segment is anticipated to exhibit the fastest CAGR over the forecast years due to the increasing use of guidewires in different vascular interventions, particularly as they become more precise, flexible, and compatible with complex anatomies. These devices are used for advancing tortuous vessels, and they allow for safe and effective catheter, balloon, and stent delivery. Increased utilization of hybrid and image-guided methods especially in neurovascular and peripheral recanalization fuels demand for expertly designed guidewires; thus, this segment is projected to be one of the most upward trends in the recanalization devices market.

By Procedure Type

The direct recanalization segment dominated the market with a 55.08% market share in 2024, during the forecast period, due to the broader acceptance in clinical practice and its established efficacy in the management of acute vascular occlusions, such as in stroke and coronary artery disease. This technique enables immediate vascular reperfusion by means of stents, catheters, and thrombectomy devices acting on the vascular occlusion. Due to shorter procedural time, simplicity of approach, effectiveness, and higher success rates, it has become the standard of care in most hospitals, and its preference in emergency procedures continues to strengthen its market dominance.

The hybrid recanalization segment will grow at the fastest rate in the forecast years due to a rise in the adoption of multi-modal treatment strategies for these vascular lesions by healthcare providers. Such a strategy is a blend of localized mechanical techniques with adjunctive pharmacological or image-guided interventions, with the advantage of higher precision and better clinical outcomes. The hybrid technique is already on the rise in the neurovascular and peripheral spheres, where the anatomy of the vessels and characteristics of the clots can be highly variable. The rapid market growth of hybrid recanalization is due to the flexibility offered the personalized medicine and integration of technology pipeline, providing a choice of tailored and highly effective interventions.

By Application

As per the Recanalization Devices Market analysis, the coronary recanalization segment accounted for the largest share of the market in 2024 with a 46.25% market share, owing to the global burden of coronary artery disease (CAD) continues to be one of the major causes of morbidity and mortality. Standard recanalization procedures, such as stent, catheter, and balloon angioplasty, are used to restore blood flow in occluded coronary arteries. Coronary recanalization has the largest revenue share of the overall cardiac procedures market owing to factors such as the increasing geriatric population, availability of widespread screening practices for early diagnosis of cardiovascular diseases, and increasing number of patients undergoing elective and emergency procedures pertaining to cardiac disorders.

The cerebral recanalization segment is anticipated to see the fastest growth during the forecast years, as the number of acute ischemic strokes rises, and more emphasis is placed on immediate action. Material and methodsNew neurointerventional devices, including mechanical thrombectomy systems and aspiration catheters, have contributed to improved outcomes when performed within a therapeutic window. Moreover, the emergence of new stroke centers, encouraging reimbursement policy in the developed world, and the steep rise in the number of neurologists and interventionists, comfortable with working with cerebral recanalisation techniques, is pushing this segment to grow at the fastest pace ever in the coming years.

Recanalization Devices Market Regional Insights:

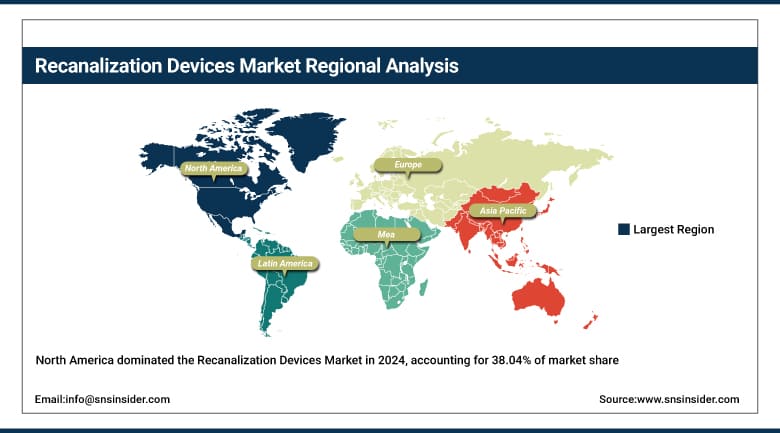

North America dominated the recanalization devices market with a 38.04% market share in 2024, owing to the well-settled healthcare infrastructure, high adoption of minimally invasive procedures, and the presence of leading medical device manufacturers. Strong reimbursement modalities, timely access to innovative technologies, and high awareness among medical practitioners and patients about endovascular interventions serve as favorable conditions for the growth of this market within the region. Furthermore, the high burden of cardiovascular and neurovascular disease in the U.S. & Canada is a major factor that is expected to drive the recanalization market. In addition, considerable clinical research activity and better regulatory pathways also help cement regional market leadership in this area.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific has risen as the most lucrative & fastest-growing region with a 9.42% CAGR over the forecast period in the recanalization devices market due to quickly developing healthcare infrastructure, an increase in healthcare investments, and a growing burden of vascular disorders such as stroke and peripheral artery disease. With better access to advanced care, the growing number of specialized stroke and cardiac centers, the use of endovascular procedures is also increasing across countries such as China, India, and Japan. With government efforts to increase universal health coverage and the rising awareness about minimally invasive treatments, device adoption throughout the region is being accelerated, and Asia Pacific is expected to be an important growth engine for the market.

The recanalization devices market is growing in Europe due to the higher adoption of minimally invasive vascular procedures and the increasing burden of cardiovascular as well as neurovascular disorders in the region. Advances in Endovascular treatment within the region (Germany, France, and the U.K., where a supportive environment for innovation and access to specialized treatment centers are present) are driving strong growth within the region. Ager population, better stroke management protocols, and the increased accessibility of recanalization procedures in metropolitan and regional hospitals also support the increase. With the improvement of clinical outcomes and increasing awareness, Europe remains a leader in the global recanalization landscape.

Latin America is experiencing substantial growth in the forecast years in the market due to Cardiovascular and neurovascular diseases are increasing burdens in Latin America, and expectations for recanalization procedures are on the rise. But it is only sparsely adopted, as health care spending and infrastructure are lacking. Although stents and guidewires will be utilized more frequently in major urban hospitals, a large portion of this growth will be held back by limited geographical distribution.

MEA also demonstrates moderate growth as the incidence of stroke and peripheral artery disease increases, and the demand increases. However, growth is limited due to the heterogeneous nature of the healthcare systems, lower per capita healthcare spending, and lower penetration of advanced interventional technologies, especially in towns and rural areas. While key markets such as Saudi Arabia, UAE, and South Africa dominate the adoption, wider regional uptake could take time.

Recanalization Devices Market Key Players

-

Medtronic plc

-

Abbott Laboratories

-

Terumo Corporation

-

Stryker Corporation

-

Becton

-

Dickinson and Company (BD)

-

Penumbra, Inc.

-

Cook Medical

-

Merit Medical Systems

Recent Developments in the Recanalization Devices Market:

-

May 2025 Terumo Corporation is at the forefront of a revolutionary shift in the neurovascular and carotid stent markets, fueled by explosive technological innovation. With a strong track record in minimally invasive therapy, Terumo is revolutionizing clinical outcomes through its strong pipeline of products and recent FDA approvals. The company's ongoing commitment to innovation and clinical excellence is making it a prime disruptor in the worldwide neurovascular care market.

- June 4, 2025, Cardinal Health launched in the U.S. its Kendall DL Multi System, a single-patient-use multi-parameter monitoring cable and lead wire system. Intended to simplify patient care from admission to discharge, the system continually monitors cardiac activity, blood oxygen, and temperature from a single connection point. The new solution improves clinician workflows, provides consistent monitoring, and offers higher value across the hospital.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.14 Billion |

| Market Size by 2032 | USD 2.23 Billion |

| CAGR | CAGR of 8.84% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Balloon Angioplasty Devices, Stents, Catheters, Aspirators, Guidewires) • By Procedure Type (Email-based Recanalization, Direct Recanalization, Hybrid Recanalization) • By Application (Coronary Recanalization, Peripheral Recanalization, Cerebral Recanalization, Others) • By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, Terumo Corporation, Stryker Corporation, Becton, Dickinson and Company (BD), Cardinal Health, Inc., Penumbra, Inc., Cook Medical, Merit Medical Systems, and other players. |

Frequently Asked Questions

North America dominated the Recanalization Devices Market in 2024.

The “Stents” segment dominated the Recanalization Devices Market.

Advancements in minimally invasive recanalization technologies are propelling the market growth.

The Recanalization Devices Market was USD 1.14 billion in 2024 and is expected to reach USD 2.23 billion by 2032.

The Recanalization Devices Market is expected to grow at a CAGR of 8.84% from 2025 to 2032.

Get in Touch