Aseptic Connectors and Welders Market Report Scope & Overview:

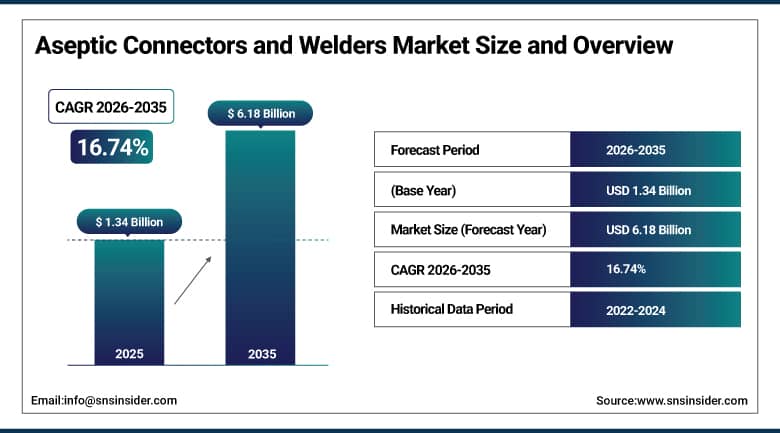

The Aseptic Connectors and Welders Market was valued at USD 1.34 billion in 2025 and is expected to reach USD 6.18 billion by 2035, growing at a CAGR of 16.74% from 2026 to 2035.

The biopharmaceutical industry has undergone a fundamental shift in how it approaches manufacturing. The transition from traditional stainless steel fixed systems to flexible, closed, and single-use bioprocessing platforms has been the defining infrastructure change of the past decade. Aseptic connectors and welders sit at the operational heart of this transformation. They enable sterile fluid transfer between process vessels, bioreactors, filtration units, and fill-finish lines without exposing product to the open environment. This closed-system capability is not a regulatory luxury. It is a commercial necessity for manufacturers producing high-value biologics, vaccines, and cell and gene therapies where a single contamination event can destroy an entire batch worth millions of dollars.

The business rationale for the expansion of markets is simple and enduring. More biological drugs are under development than ever before in the history of drug development. The worldwide pipelines of monoclonal antibodies, biosimilars, messenger RNA-based drugs, and cellular and genetic therapies have grown considerably since 2020. Each of these drug categories requires rigorous sterility during manufacturing processes. Agencies like the FDA and EMA have tightened their stance on the use of closed manufacturing processes and contamination prevention measures. Pharmaceutical manufacturers who choose to install aseptic connectors and aseptic welders are able to minimize risks associated with contamination, save money on cleaning validations, and increase batch yield predictability.

Market Size and Forecast

-

Market Size 2026E: USD 1.54 Billion

-

Market Size 2035: USD 6.18 Billion

-

CAGR: 16.74% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Aseptic Connectors and Welders Market - Request Free Sample Report

Aseptic Connectors and Welders Market Trends

-

Biopharmaceutical manufacturers are accelerating the adoption of fully closed single-use bioprocessing systems, driving structural and recurring demand for pre-sterilized aseptic connectors and welders across upstream and downstream production stages.

-

The rapid commercial expansion of cell and gene therapy manufacturing is creating specialized demand for ultra-low volume, high-sterility aseptic connection solutions suited to small-batch processing environments where every unit of product carries exceptional clinical and commercial value.

-

Genderless connector designs are gaining widespread adoption across large biomanufacturers because they eliminate gender-related connection errors, reduce operator training requirements, and simplify inventory management across multi-product facilities.

-

Automated tube welding technology is being integrated into continuous bioprocessing platforms, enabling process manufacturers to maintain sterile closed systems throughout extended production runs without manual intervention.

-

Contract manufacturing organizations are expanding their single-use bioprocessing capacity globally, which is creating a sustained and growing secondary demand for standardized aseptic connection components compatible across multiple client programs and product types.

The U.S. Aseptic Connectors and Welders Market Size Outlook

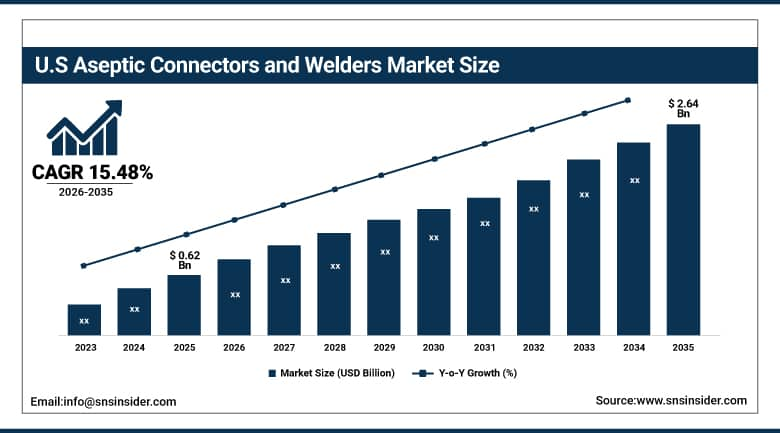

The U.S. Aseptic Connectors and Welders Market was valued at USD 0.62 billion in 2025 and is expected to reach around USD 2.64 billion by 2035, growing at a CAGR of 15.48% from 2026 to 2035.

The United States is the world's largest individual market for aseptic connectors and welders. This position reflects the country's unmatched concentration of biopharmaceutical manufacturing capacity, its deep pipeline of FDA-regulated biologics across clinical and commercial stages, and its early institutional adoption of single-use bioprocessing infrastructure. The mRNA vaccine manufacturing surge during 2020 and 2021 demonstrated in clear commercial terms how rapidly single-use closed systems could be deployed to scale production. That experience accelerated internal capital allocation decisions at major biopharmaceutical companies toward single-use platforms. The downstream effect for aseptic connector and welder suppliers has been a significant expansion in both new facility buildouts and the retrofitting of existing lines to closed-system configurations.

CPC (Colder Products Company) launched the MicroCNX Nano Series aseptic connectors in January 2025 at Advanced Therapies Week in Dallas. The product line was specifically engineered for ultra-low volume sterile fluid transfer in cell and gene therapy workflows. The launch addressed a documented gap in the market for connectors capable of handling the extremely small fluid volumes and high sterility standards required by advanced therapy medicinal product manufacturers operating under GMP conditions.

Aseptic Connectors and Welders Market Segment Analysis

-

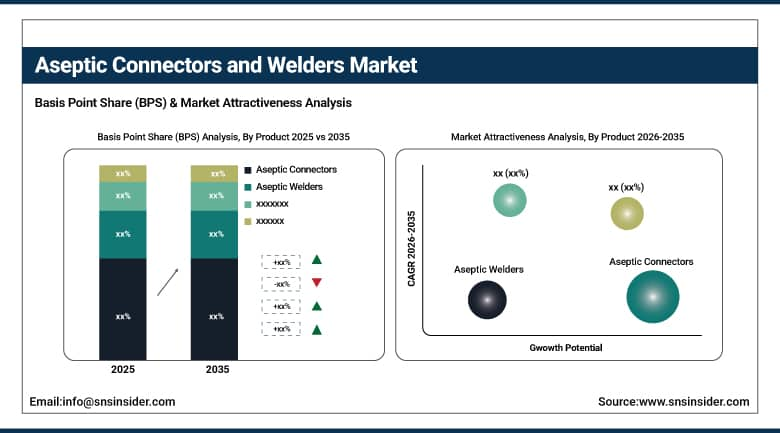

By Product, the aseptic connectors segment dominated the aseptic connectors and welders market with 68.74% share in 2025, while the aseptic welders segment is the fastest growing.

-

By Application, the upstream bioprocessing segment dominated the aseptic connectors and welders market with 46.78% share in 2025, while downstream bioprocessing is the fastest growing application.

-

By End User, the OEM segment dominated the aseptic connectors and welders market with 46.20% share in 2025, while CROs and CMOs are the fastest growing end user segment.

-

By Technology, the single-use systems segment dominated the aseptic connectors and welders market with 62.84% share in 2025, while automated single-use integration is the fastest growing technology segment.

By Product, the aseptic connectors segment dominates the market, while aseptic welders are the fastest-growing product segment.

Aseptic connectors constituted 68.74% share of revenue generated in the year 2025. The commercial success of these connectors stems from their flexibility of application. An aseptic connector can be used at any point in the fluid transfer process within a bioproduction facility. Aseptic connectors provide sterilization of connections between bags, bioreactors, filter units, and sampling lines without need of any thermal or electrical input. Being disposables ensures that every connection is made using a sterilized unit, avoiding the risk of cross-contamination between different product batches. In case of a manufacturing operation producing multiple products, this aspect acts as an important quality management feature.

Aseptic welders represent the fastest-growing product segment in the market. Welding systems create a hermetic, sterile tube-to-tube connection by thermally fusing two segments of thermoplastic tubing without opening the fluid path to the atmosphere. This capability is particularly valued in processes where a permanent, tamper-evident sterile connection must be established and maintained over extended periods. As continuous bioprocessing adoption increases and manufacturers design production lines with fewer manual break points, automated tube welding becomes a standard infrastructure element rather than a specialty application. Suppliers with compact, portable welding systems compatible with single-use tubing assemblies from multiple vendors are capturing disproportionate growth in this segment.

By Application, the upstream bioprocessing segment dominates the market, while downstream bioprocessing is the fastest-growing application.

Upstream bioprocessing held 46.78% of market revenue in 2025. Cell culture and fermentation operations require continuous sterile fluid transfer for media addition, seed train transfer, and sampling throughout the production cycle. Every connection made during upstream processing represents a contamination risk event. Manufacturers using single-use bioreactors and associated bag assemblies require aseptic connectors at each integration point, and the volume of connections per production run scales with process complexity. As biological drug pipelines have expanded and batch sizes have grown, upstream processing has become the highest-volume application for aseptic fluid transfer components.

Downstream bioprocessing is growing faster than any other application segment. Purification, chromatography, viral inactivation, filtration, and ultrafiltration steps each involve multiple sterile fluid transfers between process hold bags, column assemblies, and intermediate storage vessels. The transition of downstream operations from fixed stainless steel systems to single-use flow paths has lagged behind upstream adoption historically. That gap is now closing rapidly. Biopharmaceutical companies are recognizing that extending single-use closed systems through downstream processing reduces cleaning validation burden and shortens facility changeover time between products. This strategic shift is generating accelerating demand for aseptic connectors and welders in downstream configurations.

By End User, the OEM segment dominates the market, while CROs and CMOs are the fastest-growing end user segment.

OEMs accounted for 46.20% of market revenue in 2025. Original equipment manufacturers integrate aseptic connectors and welders into pre-configured single-use system assemblies that are sold to biopharmaceutical manufacturers as validated, ready-to-use process components. This embedded supply model gives OEMs a strong market position because their customers receive pre-qualified systems where the aseptic connector is already integrated, validated, and traceable within the broader equipment documentation package. The long-term supply agreements between major single-use system OEMs and aseptic component suppliers create predictable revenue streams and strong barriers to competitive displacement once a qualified supply relationship is established.

CROs and CMOs represent the fastest-growing end user segment. The pharmaceutical industry has been outsourcing increasingly complex manufacturing programs to contract service providers throughout the forecast period. Contract manufacturers operate multi-client facilities that process several different biological drugs simultaneously or in rapid succession. This operational model demands standardized, flexible, and rapidly deployable sterile processing infrastructure. Single-use systems with aseptic connectors satisfy all three requirements. They eliminate cross-product contamination risks between client programs, reduce facility changeover time dramatically, and allow rapid capacity scaling without large capital commitments. As more innovator biopharmaceutical companies rely on CMO networks for both clinical and commercial manufacturing, the CMO segment's aggregate aseptic component procurement volume is growing at rates that exceed the broader market.

By Technology, the single-use systems segment dominates the market, while automated integration is the fastest-growing technology approach.

Single-use systems generated 62.84% of aseptic connectors and welders market revenue in 2025. The commercial case for single-use technology in biopharmaceutical manufacturing has been thoroughly validated. Eliminating cleaning and sterilization cycles between batches reduces facility turnaround time from days to hours. The elimination of cleaning validation requirements removes a substantial regulatory documentation burden. Pre-gamma-sterilized single-use components arrive ready for immediate deployment, which compresses process setup timelines. For manufacturers producing multiple products in shared facilities, single-use systems make co-location of different programs operationally practical in ways that fixed stainless steel infrastructure cannot match.

Automated integration of single-use aseptic systems is the fastest-growing technology approach within the market. Historically, aseptic connections were made manually by trained operators following strict aseptic technique protocols. This introduced human variability as a source of process risk. Automated welding and connection systems reduce operator intervention to a minimum. They execute connections through precise, validated mechanical sequences that deliver consistent outcomes regardless of operator skill level. Continuous bioprocessing platforms, which are gaining adoption among manufacturers seeking to improve productivity and reduce batch-to-batch variability, require automated closed-system fluid handling as a foundational enabling technology. Aseptic connection automation is therefore a prerequisite for rather than an accessory to modern continuous manufacturing.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.34% |

|

Europe |

Germany |

29.74% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

18.63% |

|

Latin America |

Brazil |

44.72% |

North America Aseptic Connectors and Welders Market Insights

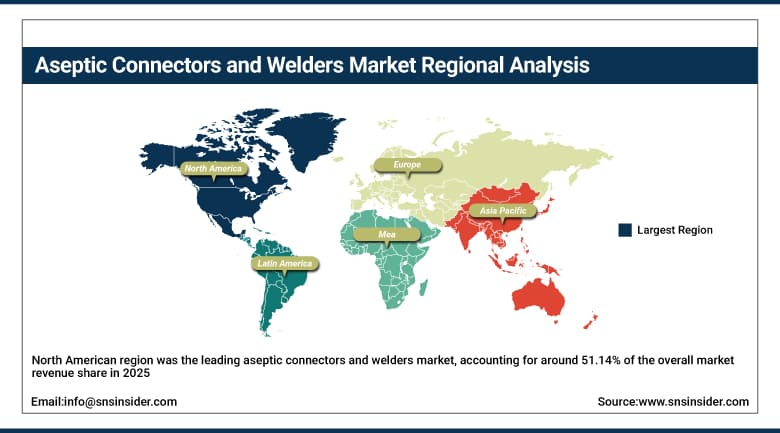

The North American region was the leading aseptic connectors and welders market, accounting for around 51.14% of the overall market revenue share in 2025. Demand within the region was primarily attributed to the United States. The US had the biggest biopharmaceutical manufacturing sector, with several large-scale biologic manufacturing plants controlled by both legacy pharma firms and emerging biotech companies. Regulatory requirements related to sterility assurance and contamination control in terms of FDA regulations have consistently increased, making investments in closed systems increasingly important for institutional applications. The US had commercial infrastructure supporting drug reimbursement policies, thus creating incentives for drug producers to invest in equipment.

There were substantial increases in investments in manufacturing capacity domestically within the US biopharmaceutical manufacturers following the pandemic, driven by commercial demands as well as biosecurity strategies. These investments created multiyear procurement opportunities for bioprocessing equipment used for aseptic fluid transfer. There was additional investment in domestic biopharmaceutical manufacturing capabilities funded through BARDA during 2023 and 2024.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Aseptic Connectors and Welders Market Insights

Europe accounted for approximately 23.47% of global aseptic connectors and welders market revenue in 2025. Germany, Switzerland, France, Ireland, and the United Kingdom are the leading country-level markets within the region. Each hosts major biopharmaceutical production facilities operated by global pharmaceutical companies and contract manufacturers. The European Medicines Agency's strict GMP framework and its emphasis on process robustness and contamination control has been a consistent driver of aseptic technology adoption. EMA regulatory guidance on advanced therapy medicinal products has specifically reinforced requirements for closed manufacturing systems, which directly expands the addressable market for aseptic connectors and welders in cell and gene therapy applications across European facilities.

Ireland has emerged as one of Europe's most commercially significant biopharmaceutical manufacturing hubs, hosting production facilities for several of the world's highest-revenue biologics. The concentration of manufacturing capacity at sites near Dublin and Cork has made Ireland a priority market for aseptic processing equipment suppliers, who have established regional application support and distribution infrastructure to serve the dense cluster of GMP biomanufacturing clients operating within a relatively compact geography.

Asia Pacific Aseptic Connectors and Welders Market Insights

The Asia Pacific Region is the world’s fastest growing regional market for aseptic connector and welding products, with a forecasted CAGR of around 16.94% between 2026 and 2035. The Chinese market occupies the position of the largest market in the region. There have been major developments within the biopharmaceutical segment in China, with several biopharma companies making large scale investments in their biologics production capacity amid NMPA regulatory harmonization with international GMP practices. The Indian market is fast developing, underpinned by the growth in its contract manufacturing industry along with biosimilar development for domestic and export markets.

China's biopharmaceutical sector has invested aggressively in next-generation manufacturing infrastructure since 2021, with several domestic biologics companies constructing GMP facilities specifically designed around single-use bioprocessing platforms from the ground up. This greenfield investment approach has created a particularly receptive market for integrated single-use systems including aseptic connectors, because facilities built entirely around single-use infrastructure require far more per-square-meter aseptic component content than older facilities that are partially retrofitting fixed stainless steel systems.

Middle East & Africa and Latin America Aseptic Connectors and Welders Market Insights

The Middle East, Africa, and Latin America regions collectively represent smaller but growing markets for aseptic connectors and welders. National pharmaceutical self-sufficiency initiatives are driving investment in domestic biopharmaceutical manufacturing in Saudi Arabia, the UAE, South Africa, and Brazil. The COVID-19 pandemic reinforced government policy commitments to building local biologics and vaccine manufacturing capability across all four regions. Investments by international pharmaceutical companies in technology transfer programs and manufacturing partnerships with local organizations are creating new facilities that require contemporary GMP-compliant bioprocessing infrastructure. These government-backed manufacturing expansion programs represent a structurally new and expanding source of demand that did not exist at scale a decade ago.

Brazil's national biopharmaceutical development initiative, supported by the Ministry of Health's Productive Development Partnerships program, has channeled public funding into partnerships between international pharmaceutical companies and domestic manufacturers at organizations including Instituto Butantan and Fiocruz. These partnerships involve technology transfer of biological manufacturing processes that require full GMP bioprocessing infrastructure, including aseptic fluid transfer systems, creating direct procurement demand for aseptic connectors and welders within the Brazilian domestic manufacturing sector.

Market Dynamics

Growth Drivers: Expanding global biologics pipelines and accelerating single-use technology adoption across biopharmaceutical manufacturing are the primary structural forces powering sustained market growth.

The global biologics pipeline has never been larger. Regulatory agencies approved more than 50 new biological drugs in 2024 across major markets. Each approved biologic represents a commercial manufacturing program that requires continuous supply of aseptic fluid transfer components. The clinical pipeline feeding future commercial approvals is proportionally even larger, with hundreds of biologics in Phase II and Phase III trials requiring clinical manufacturing scale aseptic processing infrastructure. This pipeline-to-approval trajectory creates a multi-year forward demand commitment for the aseptic connectors and welders market that is structurally independent of short-term economic cycles. Manufacturers cannot withdraw from single-use platforms without compromising product quality and regulatory standing. This creates a deeply loyal and recurring customer base for established aseptic component suppliers.

Restraints: Supply chain concentration risk and extractable and leachable regulatory scrutiny create compliance complexity and procurement vulnerability for biopharmaceutical manufacturers.

A significant proportion of single-use bioprocessing components are manufactured from specialized polymer formulations produced by a limited number of material suppliers globally. This supply chain concentration became a documented vulnerability during the COVID-19 pandemic when surge demand exposed procurement capacity limits. Biopharmaceutical manufacturers have responded by developing multi-supplier qualification strategies and maintaining safety stock buffers. These responses add procurement cost and administrative complexity. Separately, regulatory requirements for extractables and leachables testing of single-use components in direct product contact add a layer of analytical validation that suppliers must support and that buyers must complete before deploying any new connector or welder type in a GMP manufacturing process.

Opportunities: The global expansion of cell and gene therapy manufacturing is creating a high-value and underserved application segment for specialized aseptic connection technology.

Cell and gene therapies present unique manufacturing requirements that differ substantially from conventional biologics production. Batch sizes are extremely small. Each unit of product often represents a single patient treatment. The value per unit is extraordinary, frequently exceeding USD 500,000 per dose at commercial pricing. In this environment, contamination is not a quality event. It is a therapeutic and commercial catastrophe. Aseptic connector and welder suppliers that develop validated solutions specifically engineered for the tubing dimensions, volume ranges, and sterility standards of cell and gene therapy workflows are positioned to capture premium pricing and long-term supply relationships with a therapy category that regulators and payers are prioritizing for access. This specialized segment rewards technical differentiation and validated performance over commodity pricing.

Recent Developments

-

2025: CPC introduced MicroCNX Nano Series aseptic connectors during Advanced Therapies Week in Dallas to meet the critical sterile fluid handling needs associated with low volume and high sterility level of cell and gene therapies manufacturing operations.

-

2025: Sartorius extended the Flexsafe portfolio with new aseptic connector combinations tailored for use in continuous bioprocess technology platforms that would reduce the number of connections made manually during upstream processing.

-

2024: Getinge announced AseptiQuik automated tube welder with improved software control and a new validated weld integrity monitoring system allowing biopharmaceutical companies to get instant verification and documentation regarding the quality of tube welds made.

-

2024: Cytiva (Danaher) introduced a novel Flexchoice closed-system connector series characterized by genderless coupling design and sterile bags integration that could help biopharmaceutical companies reduce the time and variability of manual operations during process setup and operation.

-

2023: Parker Hannifin finished the extension of its bioprocessing fluid transfer product line with a series of aseptic connectors designed to handle large bore flow applications in biologics manufacturing operations which had been a significant gap within the single-use connector offering.

Aseptic Connectors and Welders Market Key Players are:

-

Sartorius AG

-

Danaher Corporation (Cytiva and Pall)

-

Thermo Fisher Scientific

-

Merck KGaA (MilliporeSigma)

-

Parker Hannifin Corporation

-

Saint-Gobain Performance Plastics

-

CPC (Colder Products Company)

-

Getinge AB

-

GE Healthcare Life Sciences (Cytiva)

-

Meissner Filtration Products

-

BioPure Technology

-

Cole-Parmer (Antylia Scientific)

-

Entegris Inc.

-

Lynx SU Connections

-

Fluid Line Technology

-

Terumo BCT

-

Qosina Corp.

-

Bioris GmbH

-

NewAge Industries

-

Foxx Life Sciences

Aseptic Connectors and Welders Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.34 Billion |

| Market Size by 2035 | USD 6.18 Billion |

| CAGR | CAGR of 16.74% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Aseptic Connectors, Aseptic Welders) • By Application (Upstream Bioprocessing, Downstream Bioprocessing, Fill and Finish Operations, Sampling, Others) • By End User (Original Equipment Manufacturers, Biopharmaceutical Manufacturers, Contract Research Organizations and Contract Manufacturing Organizations, Academic and Research Institutes) • By Technology (Single-Use Systems, Reusable Systems) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

Frequently Asked Questions

Ans: Key trends include rising adoption of single-use systems, demand for genderless and high-flow connectors, and integration of aseptic components in continuous and modular bioprocessing systems.

Ans: North America and Europe lead the supply, supported by advanced biopharmaceutical infrastructure, OEM presence, and strict regulatory standards promoting aseptic technology adoption.

Ans: Major players include Sartorius AG, Merck KGaA, Danaher (Cytiva), Saint-Gobain, Dover Corporation (CPC), Watson-Marlow, and Qosina, all known for strong product innovation and global distribution networks.

Ans: The increasing complexity of biopharmaceutical products and the rise of high-purity manufacturing by the industry are the factors propelling the aseptic connectors & welders market growth.

Ans: The Aseptic Connectors & Welders market size was valued at USD 1.62 billion in 2024 and is expected to reach USD 4.94 billion by 2032, growing at a CAGR of 14.98% over 2025-2032.

Get in Touch