Life Science Tools Market Report Scope & Overview:

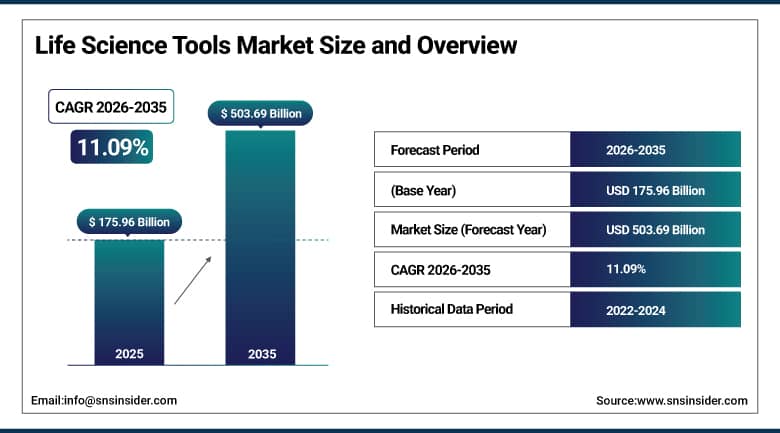

The Life Science Tools Market was valued at USD 175.96 Billion in 2025 and is expected to reach USD 503.69 Billion by 2035, growing at a CAGR of 11.09% from 2026–2035.

Life science tools cover the instruments, reagents, and consumables that researchers rely on every day to run genomic sequencing, protein analysis, cell biology work, and drug discovery programs. Demand keeps climbing as diagnostics and therapeutics companies push toward more precise, data-heavy research methods, and artificial intelligence is increasingly woven into that shift. Machine learning software is now working on the prediction of the structure of proteins and pattern recognition within very large genomic data sets, tasks that previously took research groups many months to complete manually. Cloud computing is allowing labs to exchange data and collaborate in real time beyond borders, and accelerating tasks from early research to clinical development.

The development of the artificial intelligence-based tool AlphaFold by DeepMind has changed the way protein structure prediction is viewed by researchers, being one of the major unresolved problems in biology for decades. This tool is making possible to predict the three-dimensional structure of the protein with impressive accuracy and to reduce the time necessary for drug design and the understanding of such diseases as cancer and Alzheimer's.

Market Size and Forecast

- Market Size in 2026E: USD 195.47 Billion

- Market Size by 2035: USD 503.69 Billion

- CAGR: 11.09% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get More Information On Life Science Tools Market - Request Free Sample Report

Life Science Tools Market Trends

- Rising demand for precision medicine is accelerating adoption of advanced tools like next-generation sequencing and CRISPR-based platforms.

- Growing interest in personalized therapies is boosting demand for efficient genetic research and diagnostic platforms.

- Laboratory automation is expanding, cutting error rates and speeding up high-throughput screening work.

- AI and machine learning are being built directly into data analysis, protein design, and drug development workflows.

- Decentralized clinical trials and digital health tools are increasing demand for remote data collection and analysis capabilities.

The U.S. Life Science Tools Market Outlook

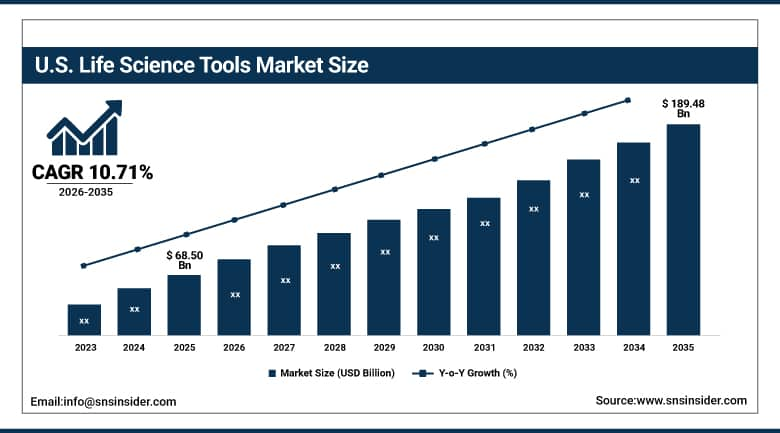

The U.S. Life Science Tools market was valued at USD 68.50 Billion in 2025 and is projected to reach USD 189.48 Billion by 2035, growing at a CAGR of 10.71% from 2026–2035.

The United States remains the anchor of global life science tools demand, supported by heavy investment in biomedical research and a deep bench of biopharmaceutical companies, academic institutions, and government-funded labs. The growing need for highly analytical instruments, reagents, and consumables has been strongly correlated to growing activity in drug discovery, genomics, proteomics, and personalized medicine. Growing adoption of automation and high throughput screening techniques, along with continuous funding from organizations such as NIH, has been propelling innovations in the industry.

Parallel Fluidics raised USD 7 million in a seed funding in November 2024 for its microfluidic and liquid handling technology platform. The investment reflects growing venture interest in the infrastructure layer that supports genomics and drug discovery workflows, rather than just the end-point diagnostic or therapeutic products themselves.

Life Science Tools Market Segment Analysis

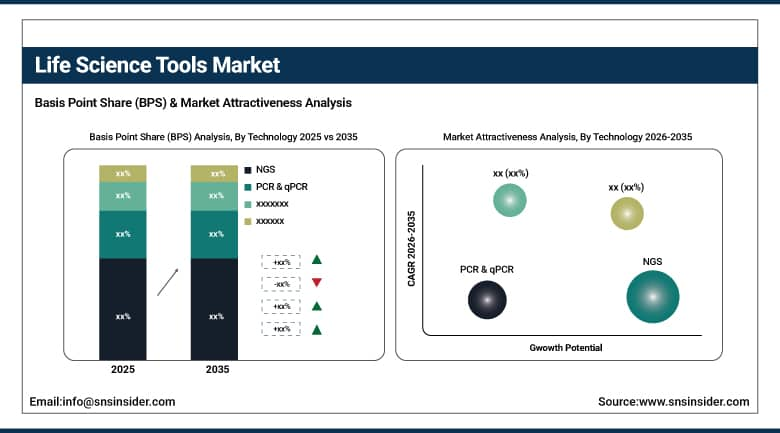

- By Technology: NGS dominated the life science tools market in 2025 with over 30% share and continues to post strong growth around 12% CAGR during the forecast period.

- By Application: genomic technology dominated the life science tools market with over 40% share in 2025, while cell biology technology is growing fastest at approximately 14% CAGR during the forecast period.

- By Type: instruments dominated the market with over 52% share in 2025, while services are projected to be the fastest-growing segment, expanding at approximately 11.8% CAGR during the forecast period.

- By End User: biopharmaceutical companies dominated the market with approximately 44% share in 2025, while the healthcare segment is expected to register the fastest growth at around 12.5% CAGR during the forecast period.

By Technology, NGS dominates and grows fastest

The market share of next-generation sequencing was the highest in 2025, at over 30%, due to its wide application in genomics, oncology, and personalized medicine. With NGS, scientists can sequence DNA and RNA at a relatively high rate and relatively lower cost, thus making it an integral part of almost all research laboratories, clinical laboratories, and drug development processes. The rising need for more genome data in precision medicine will further support the position of the segment.

The growth rate of the next-generation sequencing segment is also quite high, at about 12% CAGR, as a result of innovations such as single-cell sequencing and increased use in liquid biopsy and detection of rare diseases. The capability of delivering more genetic data in a faster and cheaper way compared to traditional methods has facilitated the use of NGS technology in research and clinical applications.

By Application, genomic technology dominates, cell biology technology grows fastest

Genomic Technology emerged as the leading technology segment in 2025, with a market share exceeding 40%, backed by further innovations in sequencing techniques as well as increased use of CRISPR gene editing in personalized healthcare and diagnostic applications. The increasing use of genomics technology for disease diagnosis and treatment planning helped maintain its leadership position.

The Cell Biology Technology segment recorded the highest growth rate in 2025 at a CAGR of approximately 14%. It is being driven by the advancements in single-cell biology and stem cell research. Tools such as single-cell RNA sequencing are enabling scientists to get better insights into the biological nature of diseases, resulting in faster drug discovery and development, especially in oncology and regenerative medicine.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

79.20% |

|

Europe |

Germany |

24.80% |

|

Asia Pacific |

China |

43.60% |

|

Middle East & Africa |

Saudi Arabia |

23.40% |

|

Latin America |

Brazil |

47.10% |

North America Life Science Tools Market Insights

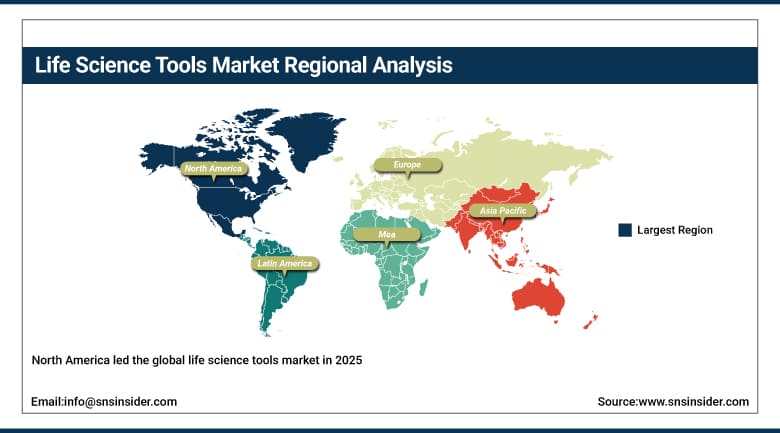

North America led the global life science tools market in 2025, driven by substantial investment in biotechnology and healthcare infrastructure, particularly across the United States. Having companies like Thermo Fisher Scientific, Illumina, and Agilent Technologies in the region makes its competitiveness higher, while at the same time there is intensive R&D in genomics, diagnostics, and drug discovery.

The increasing popularity of such technologies as CRISPR gene editing and genomic sequencing technology is fostering the development of the region. The region's interest in personalized medicine and precision healthcare is another factor behind the continuous demand for life sciences instruments.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Life Science Tools Market Insights

The region had an important share of the world market in 2025 due to substantial government investment in biomedical research and developed healthcare system. The further investments made by the European Union in genomics and biotechnology, along with an increasing number of clinical trials, contribute to the consistent growth in the demand for life science tools in Europe.

The already-developed research infrastructure in countries like Germany, France, and the UK serves as the foundation for the regional demand, while the cooperation between the countries boosts the introduction of new analytical tools in European laboratories.

Asia Pacific Life Science Tools Market Insights

Asia Pacific is the fastest-growing regional market, expanding at over 12% CAGR, spurred by rising demand for diagnostics, expanding research capabilities, and improving healthcare systems in China, India, and Japan. The growth of the biopharmaceuticals industry in the region, along with the growing genomics and biotech industry, is another factor that is driving the rapid growth in the region.

Increased investment in healthcare infrastructure is contributing to increased usage of cutting-edge life sciences equipment in the region, owing to increased adoption of laboratory automation, artificial intelligence, and precision medicine. Increased investment in R&D and life sciences infrastructure is further contributing to increased demands for these tools.

Middle East & Africa and Latin America Life Science Tools Market Insights

The Middle East & Africa and Latin America markets are expanding as healthcare and research investment grows across both regions. Growing use of genomic technologies and a growing trend towards personalization in medicine are among the factors fueling demand, along with government efforts to build capacity for research in the area.

Growing involvement in clinical research and the continuing need for efficient laboratory technology are key growth drivers in the developing markets. Though still early-stage compared to North America, Europe, and the Asia Pacific, investments in research facilities are slowly carving out a slice of the global pie.

Market Dynamics

Growth Drivers: Growing Demand for Precision Medicine and AI-Driven Laboratory Automation

Increasing demand for precision medicine is among the key drivers driving market growth, thanks to the developments in genomics, diagnostics, and drugs. The application of novel technologies like next generation sequencing and CRISPR technology is enhancing genetic research and facilitating targeted treatments. The shift towards precision medicine is further fueling the demand for advanced life science equipment.

Automation and AI adoption in laboratories is yet another key driver in this market. Automation and use of AI technology minimize errors associated with humans, speed up repetitive processes, and help enhance productivity in high throughput screening and genomic analysis. Automated liquid handling and sample processing equipment have now become integral to drug discovery process.

Restraints: Stringent Regulatory Compliance and Rising Data Privacy & Security Challenges

Strict regulations in the field of medicine and research can considerably postpone the development of new products, posing challenges for companies producing the tools of life sciences. Compliance with the latest regulatory requirements is a significant factor that makes the process of bringing new tools to the market longer and more expensive.

Nowadays, the problem of secure and private storage of the massive amounts of information generated by new devices is a serious hindrance to their implementation. Companies have to spend more money on data security systems and measures in order to guarantee protection of personal data.

Opportunities; Expansion of Precision Medicine, Laboratory Automation, and Emerging Healthcare Markets

The expansion of precision medicine, laboratory automation, and AI integration is opening substantial opportunities across the life science tools market. Increasing use of genomics and diagnostic solutions from both research and clinical perspectives has created an opportunity for vendors to broaden their range of products as well as forays into related applications.

The emerging market in Asia-Pacific, Latin America, and Middle East & Africa regions provides a significant growth opportunity as investments in healthcare infrastructure increase. The vendors that have instruments that are more affordable and scalable could benefit from this trend in the next decade.

Recent Developments:

- 2024: In November 2024, Parallel Fluidics secured a USD 7 million seed funding round to advance microfluidic and liquid-handling technologies supporting next-generation life science tools.

- 2024: In 2024, Illumina expanded its sequencing platform portfolio with enhanced throughput options aimed at clinical and translational research applications.

- 2024: In 2024, Thermo Fisher Scientific broadened its mass spectrometry lineup to improve sensitivity for proteomics and biopharma quality control applications.

- 2025: In 2025, Agilent Technologies expanded its genomics solutions portfolio with new microarray and liquid chromatography offerings aimed at precision medicine research.

Life Science Tools Market key players are:

- Agilent Technologies, Inc.

- Becton, Dickinson and Company (BD)

- F. Hoffmann-La Roche Ltd.

- Bio-Rad Laboratories, Inc.

- Danaher Corporation

- Illumina, Inc.

- Thermo Fisher Scientific Inc.

- QIAGEN N.V.

- Merck KGaA

- Shimadzu Corporation

- Hitachi High-Tech Corporation

- Bruker Corporation

- Carl Zeiss AG

- Oxford Instruments plc

- Waters Corporation

- Beckman Coulter, Inc.

- Sartorius AG

- Eppendorf SE

- Revvity, Inc.

- Mettler-Toledo International Inc.

Life Science Tools Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 175.96 Billion |

| Market Size by 2035 | USD 503.69 Billion |

| CAGR | CAGR of 11.09% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (NGS, Nucleic Acid Preparation, Nucleic Acid Microarray, PCR & qPCR, Flow Cytometry, Mass Spectrometry, Separation Technologies, Others) • By Application (Genomic Technology, Cell Biology Technology, Proteomics Technology, Others) • By Type (Instruments, Consumables, Services) • By End-User (Biopharmaceutical Companies, Government & Academic Industry, Healthcare, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Agilent Technologies, Inc., Becton, Dickinson and Company (BD), F. Hoffmann-La Roche Ltd., Bio-Rad Laboratories, Inc., Danaher Corporation, Illumina, Inc., Thermo Fisher Scientific Inc., QIAGEN N.V., Merck KGaA, Shimadzu Corporation, Hitachi High-Tech Corporation, Bruker Corporation, Carl Zeiss AG, Oxford Instruments plc, Waters Corporation, Beckman Coulter, Inc., Sartorius AG, Eppendorf SE, Revvity, Inc., Mettler-Toledo International Inc. |

Frequently Asked Questions

Next-generation sequencing (NGS) held the largest product share in 2025, at over 30% of total market revenue.

Growth is driven by rising demand for precision medicine, expanding laboratory automation, and the integration of AI into genomic and proteomic research workflows.

The Life Science Tools Market was valued at USD 175.96 Billion in 2025.

The market is expected to grow at a CAGR of 11.09% between 2026 and 2035.

Get in Touch