Audio Conferencing Services Market Report Scope & Overview:

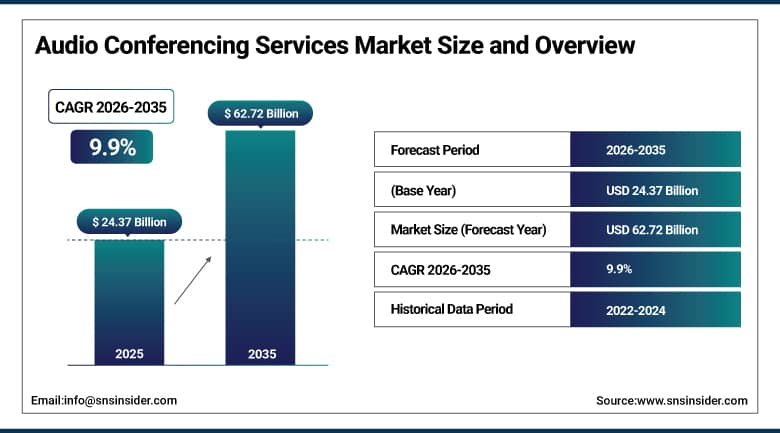

The Audio-Conferencing Services Market was valued at USD 24.37 Billion in 2025 and is expected to reach USD 62.72 Billion by 2035, growing at a CAGR of 9.9% from 2026–2035.

The global audio-conferencing services market is undergoing a commercially significant transformation driven by the permanence of hybrid work. Enterprises across every sector now maintain distributed teams as a standard operating model. Audio conferencing has consequently moved from an optional productivity tool to a core communication infrastructure investment. Vendors are competing not on voice quality alone but on AI-driven features, platform integration, and security compliance. The shift toward cloud-based deployment is accelerating adoption, as organisations eliminate physical conferencing hardware and consolidate communication budgets. Integrated platforms combining audio, video, and messaging now command the highest enterprise procurement priority.

Research confirms that 68% of enterprises rely on audio conferencing daily, with remote employees averaging 18 audio meetings per week. This frequency of use transforms audio services into business-critical infrastructure where reliability, feature depth, and vendor integration capability define competitive differentiation.

Market Size and Forecast

-

Market Size in 2026E: USD 26.78 Billion

-

Market Size by 2035: USD 62.72 Billion

-

CAGR: 9.9% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Audio Conferencing Services Market - Request Free Sample Report

Audio Conferencing Services Market Trends

-

Growing enterprise adoption of AI-powered noise cancellation and real-time transcription is improving meeting productivity and reducing the manual effort required for post-call documentation and follow-up workflows.

-

Rising integration of audio conferencing with collaboration platforms including Microsoft Teams and Cisco Webex is driving demand for unified communication services that eliminate tool switching across enterprise workflows.

-

Increasing telehealth adoption is creating specialised demand for HIPAA-compliant audio-conferencing solutions that support secure patient consultations and clinician coordination across distributed healthcare networks.

-

Growing SME adoption of on-demand audio conferencing services is expanding the addressable market, as flexible pay-as-you-go pricing models eliminate upfront infrastructure investment and align cost with actual usage.

-

Rising investment in multilingual real-time translation capabilities is enabling global enterprises to conduct cross-border audio conferences more efficiently, reducing language barriers that previously increased meeting overhead.

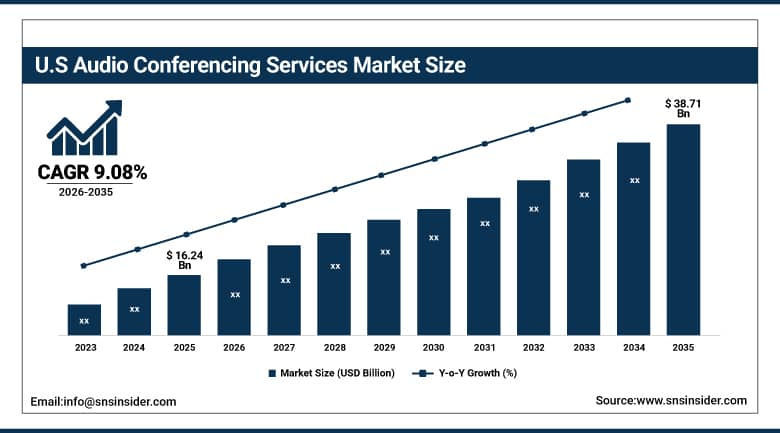

U.S. Audio Conferencing Services Market Outlook

The U.S. Audio Conferencing Services Market was valued at approximately USD 16.24 Billion in 2025 and is expected to reach approximately USD 38.71 Billion by 2035, growing at a CAGR of approximately 9.08%.

The United States is the world’s largest audio-conferencing services market by revenue. Enterprise demand is driven by the structural permanence of hybrid work across knowledge-intensive sectors. Large organisations have consolidated communication tools onto unified platforms, making audio a core infrastructure layer rather than a standalone service. Vendors including Cisco, Microsoft, and Zoom have responded by embedding AI transcription, noise cancellation, and compliance tools directly into their audio services. Financial services and healthcare account for the highest per-user spending due to compliance and security requirements. Cloud deployment now dominates procurement across both enterprise and mid-market segments, displacing legacy on-premises conferencing infrastructure at a measurable pace.

The Cisco Webex Calling service underwent a significant upgrade in 2024 to include artificial intelligence-based audio optimization and noise removal capabilities, catering to the needs of enterprise-level customers dealing with vast numbers of remote employees. This upgrade helped rectify an observed productivity problem that had been pinpointed by the enterprise IT departments as being caused by background noise during conferences.

Audio Conferencing Services Market Segment Analysis

-

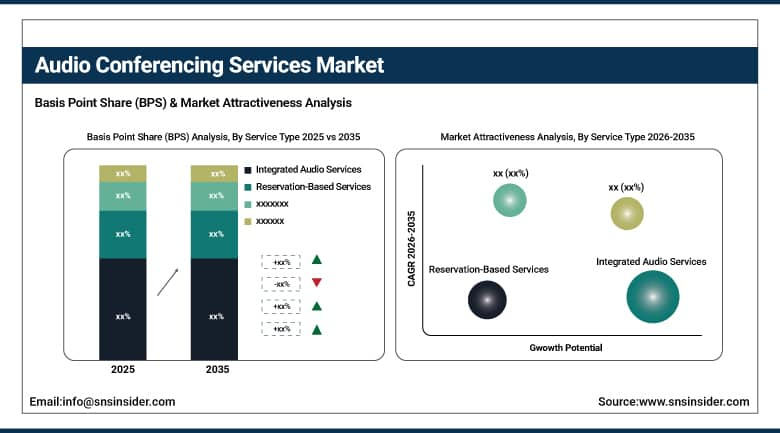

By Service Type, Integrated Audio Services dominated with approximately 33.41% share in 2024, driven by enterprise demand for unified communication platforms combining audio, video, and messaging in a single vendor relationship. On-Demand Audio Conferencing is the fastest-growing segment.

-

By Enterprise Size, Large Enterprises dominated the audio conferencing services market in 2025, accounting for the majority of subscription revenue through their higher user counts, compliance requirements, and need for enterprise-grade security and administrative controls. SMEs are the fastest-growing enterprise size segment.

-

By End User, IT & Telecom held the largest share in 2024, leveraging audio conferencing for global operations and distributed workforce management across time zones. Healthcare is the fastest-growing vertical at a CAGR of 13.23%.

-

By Deployment, cloud-based audio conferencing dominated the market in 2025 through its operational scalability, elimination of hardware maintenance overhead, and ability to receive continuous AI feature updates without customer IT intervention. On-premises deployment retains relevance among financial institutions and government agencies with strict data sovereignty and security compliance requirements.

By Service Type, integrated audio services dominate, on-demand grows fastest

Integrated Audio Services retained the dominant service type position with approximately 33.41% of the audio conferencing services market in 2024. The commercial logic is straightforward. Enterprises operating across multiple collaboration tools face significant coordination overhead, IT complexity, and per-user cost duplication. Consolidated platforms that deliver audio alongside video, messaging, and file sharing within a single administrative environment reduce this burden materially. Microsoft Teams, Cisco Webex, and Zoom’s enterprise suite have demonstrated that integrated deployment improves adoption rates, reduces call dropout frequency, and simplifies compliance documentation. Large enterprise IT procurement teams now specify integration capability as a primary vendor evaluation criterion. This requirement structurally advantages platforms with native audio services over point solutions that depend on third-party audio bridges or dial-in network aggregators for conference functionality.

On-Demand Audio Conferencing is the fastest-growing segment because it directly addresses the commercial constraints that previously limited audio conferencing adoption among smaller organisations. Traditional reservation-based and integrated services carry subscription commitments that require predictable usage forecasting. On-demand services eliminate this requirement. They provide access to high-quality conferencing infrastructure on a per-minute or per-session basis, enabling cost alignment with actual meeting activity. This pricing model is particularly attractive to SMEs with variable meeting schedules and project-based client communication patterns. As on-demand quality has reached parity with dedicated subscription services through cloud infrastructure investment, the remaining barriers to adoption have narrowed to awareness and implementation support rather than technical or commercial capability gaps.

By End User, IT & telecom dominates, healthcare grows fastest

IT and Telecom retained the dominant end user position in the audio conferencing services market in 2024. The sector’s demand profile reflects its operational structure. Technology and telecommunications companies operate globally distributed engineering, sales, and support teams that require reliable, low-latency audio communication across time zones and geographies as a daily operational necessity rather than an occasional convenience. These organisations also typically carry the most sophisticated procurement requirements, specifying platform API integration capability, call analytics dashboards, and carrier-grade uptime guarantees that justify enterprise-tier service agreements. IT sector audio conferencing adoption is also reinforced by the sector’s above-average willingness to adopt emerging AI communication features early, generating usage patterns that drive vendor platform investment in capabilities that subsequently propagate across other verticals.

Healthcare is currently the fastest-growing end-user vertical in this market, with a CAGR of 13.23% until 2035. These numbers reflect not only increased demand but also a major shift in how care delivery models are constructed in terms of structure and regulation. Telehealth solutions went from an emergency measure implemented in response to a global pandemic to a staple method of delivering care within primary care, psychiatry, chronic disease management, and post-acute follow-ups. The least expensive, yet most effective way of ensuring access to telehealth services to patients who don't necessarily have broadband Internet connection or access to a smartphone is through audio conferencing. There are certain HIPAA compliance regulations imposed on healthcare providers, which include BAAs, end-to-end encryption, and audit capabilities – two vendors with such options on offer are Cisco and Zoom.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

55.2% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Audio Conferencing Services Market Insights

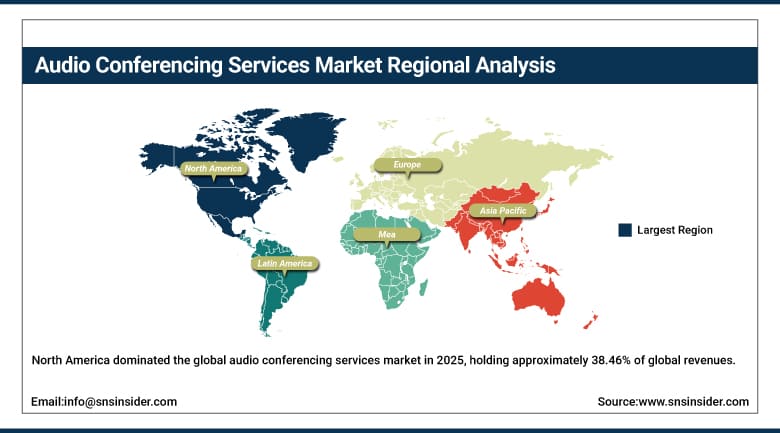

North America dominated the global audio conferencing services market in 2025, holding approximately 38.46% of global revenues, with the United States accounting for approximately 87.4% of North American revenues. The region’s leadership reflects its combination of the highest hybrid work adoption rate globally, the most mature enterprise cloud communication infrastructure, and the headquarters concentration of the market’s leading platform vendors. Cisco, Microsoft, Zoom, and RingCentral are all North American companies whose product development priorities are shaped by the demands of U.S. enterprise customers. This creates a self-reinforcing commercial dynamic where the most sophisticated audio conferencing features are deployed domestically first and subsequently distributed to global markets through platform update cycles.

Canada contributes approximately 12.6% of North American revenues through its large professional services and financial sector enterprise base, federal government digital transformation investment in secure communication infrastructure, and a creator economy and technology sector whose remote-first hiring practices sustain above-average audio conferencing usage intensity relative to population scale.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Audio Conferencing Services Market Insights

Europe is the world’s second-largest audio conferencing services market, characterised by a combination of GDPR data residency requirements that drive demand for regionally hosted conferencing infrastructure and a strong enterprise willingness to consolidate communication tools onto unified platforms that reduce vendor complexity. Germany accounts for approximately 22.3% of European revenues through its concentration of global manufacturing and industrial enterprise headquarters whose international supply chain coordination and global sales operations generate consistent audio conferencing demand at the scale of major platform deployments.

The United Kingdom and France are significant secondary markets where financial services sector compliance requirements and public sector digital transformation investment sustain above-average enterprise audio conferencing spending. European regulatory evolution under the EU AI Act is also creating commercial pressure on vendors to provide transparency and auditability in AI-powered transcription and analytics features, which is shaping the product development roadmaps of Microsoft, Cisco, and regional competitors serving enterprise procurement teams with explicit regulatory compliance evaluation criteria.

Asia Pacific Audio Conferencing Services Market Insights

Asia Pacific is the fastest-growing regional audio conferencing services market, driven by rapid enterprise digitalisation across China, India, Japan, South Korea, and Southeast Asia whose combined corporate sector expansion is creating first-time adoption of cloud-based unified communication platforms at a pace that materially exceeds North American and European market growth rates. China accounts for approximately 55.2% of Asia Pacific revenues through its combination of a large enterprise technology sector, a domestic unified communication platform ecosystem anchored by Alibaba’s DingTalk and Tencent Meeting, and the government’s digital economy investment programme that is modernising public sector communication infrastructure.

India and Southeast Asia represent the most commercially dynamic emerging market growth opportunities within Asia Pacific, where the rapid expansion of the technology outsourcing sector, the growth of digital-first enterprise businesses, and the progressive adoption of cloud infrastructure across financial services, education, and government are collectively creating structured demand for audio conferencing services at the enterprise scale that platform vendors are actively investing to serve.

MEA & Latin America Audio Conferencing Services Market Insights

The Middle East and Africa and Latin America are growing audio conferencing services markets where digital transformation investment, expanding cloud infrastructure adoption, and the growing normalisation of remote work across corporate sectors are creating structured demand for enterprise communication services. UAE leads MEA revenues at approximately 38.4% of the regional total through its concentration of multinational corporate operations, the high proportion of expatriate professional workforce requiring international communication tools, and the government’s Smart Dubai and UAE Vision 2031 digital economy programmes that are accelerating cloud communication adoption across public and private sector organisations.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large corporate sector, the rapid adoption of cloud services across financial services and technology companies, and the structural normalisation of remote and hybrid work arrangements following COVID-19 that has created permanent demand for reliable audio conferencing infrastructure across mid-market and enterprise organisations whose workforce distribution makes physical conferencing logistically impractical as a daily communication model.

Market Dynamics

Growth Drivers: Hybrid work permanence driving enterprise communication platform investment, AI feature integration improving productivity value, and healthcare telehealth adoption creating regulated market expansion

The structural permanence of hybrid work is the market’s most durable commercial growth driver. Enterprises that restructured their workforce around distributed operating models during the pandemic have not reversed these decisions. They have instead invested in upgrading the communication infrastructure that distributed work depends on. Audio conferencing services sit at the core of this investment as the most universally accessible collaboration channel. AI integration is simultaneously expanding the commercial value delivered per subscription. Real-time transcription eliminates post-meeting documentation effort. Intelligent noise cancellation improves meeting quality in home office environments. Automated action item detection creates accountability without manual note-taking.

Healthcare’s telehealth expansion is creating a structurally distinct demand pool whose compliance requirements generate premium pricing power for vendors with HIPAA-certified infrastructure. This vertical’s audio conferencing adoption does not correlate with general enterprise technology cycles. It is driven by reimbursement policy, patient access mandates, and clinical workflow integration that create regulatory-enforced adoption incentives independent of economic conditions.

Restraints: Pricing pressure from free-tier competitors, data security and privacy compliance complexity in regulated industries, and network infrastructure limitations in developing markets

The market faces meaningful pricing pressure from the availability of high-quality free-tier audio conferencing services including Google Meet and Microsoft Teams Free that capture SME usage volume and create reference price anchors that compress willingness to pay for premium subscription tiers. This dynamic is most acute in price-sensitive markets where the feature differentiation of paid services is insufficiently communicated to justify the cost premium in procurement evaluations.

Data security and regulatory compliance requirements in BFSI, government, and healthcare create procurement complexity that extends sales cycles and increases implementation costs. Smaller enterprises in these verticals often lack the internal IT expertise to evaluate vendor compliance claims independently, creating a decision paralysis dynamic that delays adoption and benefits established vendors with recognised compliance certifications over newer entrants whose equivalent security capabilities are less transparently validated.

Opportunities: EHR-integrated clinical audio platforms, regional language AI transcription for emerging markets, and government digital transformation procurement creating large-scale adoption programmes

The integration of audio conferencing directly within EHR platforms represents the most commercially valuable product development direction for healthcare-focused vendors. Clinicians who can initiate HIPAA-compliant audio consultations from within the same interface where they document patient encounters experience a qualitatively different workflow efficiency improvement that standalone conferencing platforms cannot deliver. Vendors that achieve native EHR integration through partnership with Epic, Cerner, and Oracle Health access a sticky adoption model where switching costs are substantially higher than in general enterprise audio conferencing.

Government digital transformation procurement represents a large-scale adoption opportunity whose multi-year contract values and standardised deployment requirements make it commercially attractive for platform vendors with proven public sector security certification. Nations across Southeast Asia, the Middle East, and Latin America are executing national digital government infrastructure programmes that include secure audio communication as a core component, creating procurement tender opportunities whose scale justifies dedicated investment in public sector compliance certification and local data residency infrastructure.

Recent Developments:

-

2024: Cisco expanded its Webex Calling platform with AI-powered audio optimisation, background noise removal, and real-time meeting transcription capabilities, targeting large enterprise customers managing distributed workforces and seeking to reduce the manual documentation burden that high meeting frequency imposes on knowledge workers across global operations.

-

2024: Microsoft integrated advanced audio AI features into Microsoft Teams Premium, including intelligent recap with automatic action item extraction and speaker identification, reducing the post-meeting administrative effort that had been identified by enterprise IT departments as the primary friction point reducing meeting productivity outcomes across distributed organisations.

-

2025: Zoom expanded its contact centre and audio conferencing integration capabilities in 2025, enabling enterprise customers to unify customer-facing and internal communication workflows within a single administrative platform, reducing the vendor management complexity that multi-platform communication architectures impose on IT operations teams across large enterprise deployments.

Audio Conferencing Services Market Key Players

-

Cisco Systems Inc. (Webex)

-

Microsoft Corporation (Teams)

-

Zoom Video Communications Inc.

-

Avaya Holdings Corp.

-

RingCentral Inc.

-

Google LLC (Google Meet)

-

8x8 Inc.

-

Dialpad Inc.

-

GoTo (LogMeIn Inc.)

-

BlueJeans by Verizon

-

Tata Communications Ltd.

-

Lifesize Inc.

-

Fuze Inc.

-

Arkadin (NTT)

-

West Technology Group (Intercall)

-

PGi (Premiere Global Services)

-

BT Conferencing

-

AT&T Business

-

Vonage Holdings Corp.

-

Bandwidth Inc.

Audio Conferencing Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 24.37 Billion |

| Market Size by 2035 | USD 62.72 Billion |

| CAGR | CAGR of 9.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Integrated Audio Services, On-Demand Audio Conferencing Services, Reservation-Based Services) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises) • By End User (IT & Telecom, BFSI, Healthcare, Education, Government, Retail, Others) • By Deployment (Cloud, On-Premises) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cisco Systems Inc. (Webex), Microsoft Corporation (Teams), Zoom Video Communications Inc., Avaya Holdings Corp., RingCentral Inc., Google LLC (Google Meet), 8x8 Inc., Dialpad Inc., GoTo (LogMeIn Inc.), BlueJeans by Verizon, Tata Communications Ltd., Lifesize Inc., Fuze Inc., Arkadin (NTT), West Technology Group (Itercall), PGi (Premiere Global Services), BT Conferencing, AT&T Business, Vonage Holdings Corp., Bandwidth Inc. |

Frequently Asked Questions

Ans: North America dominated the Audio Conferencing Services Market in 2024, holding a 38.46% market share.

Ans: The Integrated Audio Services segment dominated the Audio Conferencing Services Market in 2024, accounting for 33.41% of the market share.

Ans: The major growth factor driving the Audio Conferencing Services Market is the increasing demand for seamless communication solutions, especially fueled by remote and hybrid work models and the shift towards integrated, cloud-based communication platforms.

Ans: The market size of the Audio Conferencing Services Market in 2024 was USD 22.16 billion.

Ans: The Audio Conferencing Services Market is expected to grow at a CAGR of 9.9% during the forecast period from 2025 to 2032.

Get in Touch