Audio Visual Hardware Market Key Insights:

To Get More Information on Audio Visual Hardware Market - Request Sample Report

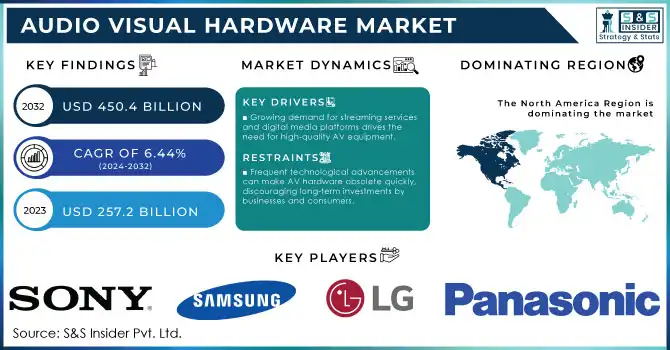

The Audio Visual Hardware Market size was valued at USD 257.2 billion in 2023 and is expected to reach USD 450.4 Billion by 2032, growing at a CAGR of 6.44% from 2024-2032.

The audio-visual (AV) hardware market is driven by growing demand for AV devices in different end-user sectors including entertainment, education, corporate, and retail. This growth is being driven by the world's ongoing consumption of digital content and the growing demand for experiential, participatory opportunities. This is evident in the massive adoption of 4K and later 8K televisions, such as those from Samsung and LG, and the use of advanced projectors and sound systems. The availability of smart classrooms and learning has substantially fueled the demand for AV equipment such as interactive displays and projectors in the education sector. Moreover, the growing integration of virtual and augmented reality (VR/AR) technologies is providing exciting new growth opportunities for automation vehicles with hardware manufacturers. As an example, the increase in the adoption of VR headsets with AV systems used in gaming and simulation in 2023 provided a boost to the growth of the market. With hybrid work models on the rise, the pandemic-driven boom has also heightened the demand for video conferencing hardware solutions such as camera, microphone and AV processor equipment to create better remote communication--both for companies and their employees.

AV hardware is more commonly used in retail for digital signage, advertising, and in-store customer experience. In 2023, the reliance on AV technology for many retailers was further displayed as new retailers rolled out AV solutions to garner attention and sales.

With yet another year passing by, technology continues to advance, particularly in the sound processing department when it comes to AI-enhanced understanding of audio people want to hear and how to best deliver it to them, as well as improvements in image quality that keep this portion of the AV hardware market in development. The growing adoption of connected smart devices over the globe such as smart TVs, soundbars, & voice-activated assistants, among others, is contributing to the growth of the market through offering consumers audio-visual experiences that are enjoyable & seamless.

Market Dynamics

Drivers

-

Growing demand for streaming services and digital media platforms drives the need for high-quality AV equipment.

-

Educational institutions are increasingly using AV hardware like interactive displays and projectors for digital learning environments.

-

Increased interest in 4K and 8K TVs, VR, and AR technology reflects a trend toward more immersive and interactive media experiences.

The audio-visual (AV) hardware market is rapidly progressing, owing to the increasing proliferation of ultra-high-definition 4K and 8K displays as well as augmented reality and virtual reality (AR/VR) technologies. This indicates a promising direction for greater experiential, interactive output within consumer, corporate, educational, and retail sectors. With rising expectations for better sound and image quality, AV hardware makers are rethinking their designs to offer higher-resolution, crisper audio and visual out of the box. The latest trend involves 4K and 8K high-definition screens that boast improved detail, color depth, and contrast to create more realistic visuals that improve viewing experiences. Such sophisticated displays are also being sought for professional uses, where premium AV systems elevate presentations, training and digital signage beyond entertainment. The adoption of VR and AR only propels the AV market forward, offering experiences beyond the average screen. VR headsets, which combine visual and audio effects for immersive 360-degree experiences, became popular for gaming, simulations, and virtual meetings. As an example, when it comes to gaming, VR makes it possible by simulating a realistic environment where the user can interact as though it was real. VR/AR are reinventing training in industries such as healthcare and manufacturing through simulation of real-world scenarios that facilitate improved learning while minimizing risk to the organization.

As businesses continue to integrate advanced AV solutions to enhance customer engagement and streamline operations, this desire for immersive technologies is changing consumer behaviors and business practices. With the growing demand for high-quality, interactive AV technology, innovation in the AV industry is accelerating as manufacturers focus on creating visuals with sharper clarity, more immersive sound quality, and enhanced interactivity. With the expanding spectrum of interest around these solutions included across different domains, the AV hardware market is likely to forge on into the future, evolving to provide immersive experiences across various domains.

Restraints

-

Frequent technological advancements can make AV hardware obsolete quickly, discouraging long-term investments by businesses and consumers.

-

Integrating AV hardware with existing IT and communication systems can be complex and costly, especially in corporate settings, which may slow down adoption.

-

The AV hardware industry faces scrutiny over e-waste and energy consumption, with increased pressure to adopt sustainable practices, which can add to costs.

The audio-visual (AV) hardware industry is increasingly under scrutiny from various stakeholders for its environmental impact, such as e-waste and energy usage. New technologies such as 4K/8K displays, VR/AR systems, and high-end audio equipment drive new demand in Consumer AV, and outside of our industry the competition between existing devices creates more e-waste every year as upgrades remove dated appliances. The accelerating speed of technology evolution and shortened lifecycle has compounded the problem, leading manufacturers to seek environmentally friendly practices such as recyclable materials and take-back programs for obsolete equipment.

A similar scenario is also present in the AV sector with regards to energy consumption. A powerful visual screen or massive public-facing video screen with dynamic reminders requires high (and continuous) energy consumption (and carbon emissions), for full-time commercial deployments such as digital signage and video-conferencing, typical with multiple projectors and/or mega-sound systems. In response, regulators and environmentally-conscious consumers are calling for reductions in the carbon footprint of AV products. To that end, manufacturers are incorporating energy-efficient features such as LED displays and AV systems with “eco-mode” functions that minimize off-peak power use.

However such environment-friendly initiatives mean extra cost for manufacturers. Some companies are spending in this direction on research and development of energy-saving components, eco-friendly designs, and modular designs that can be easily repaired or upgraded. Though they reduce the environmental footprint of production, these improvements raise production costs, and one can assume that some manufacturers will pass those costs on to consumers, thereby raising prices and putting the brakes on high-end AV high-tech adoption.

Segment Analysis

By Application

Professional segment dominated the market and represented significant revenue share in 2023. This industry is characterized by fierce competition with both national and international, large and small players. Brand reputation also plays a huge role in the buying decisions of potential customers since established brands are often synonymous with quality and features. Companies such as AVI-SPL Inc., AVI Systems Inc., Ford Audio-Video LLC, Solotech Inc. are the leaders in the market. Expect healthy competition among these respective top vendors, with an opportunity for a market expansion in the future.

We anticipate that the market will see considerable growth on the consumer side. There has also been an upsurge in demand amongst consumers for AV products that can be easily integrated into smart home networks and offer features such as voice control and automation. In parallel with the expansion of streaming services and online gaming, there has been a push for evermore high-performing AV gear to provide high-quality picture, sound, and low-latency performance. Other commonly used devices, like tablet devices and wireless speakers, are also rising in popularity because they are portable and user-friendly. Value-add capabilities such as integrated streaming and fitness tracking are increasing the attractiveness of consumer audio visual systems, thus creating a dynamic and rapidly evolving marketplace.

By Type

In 2023, the equipment segment dominated the market and accounting for 77.2% of revenue. The key factors boosting this growth are the growing use of high-resolution display usage, advanced audio system requirements, and use of VR/AR technologies. Manufacturers have come up with multi-purpose devices like smart TVs and in terms of installation, new wireless solutions have simplified their installation. As technology evolves, better user experience with intuitive interfaces, voice control, and personalization would further propel this growth.

The digital signal management (DSM) segment is expected to register highest CAGR during the forecast period. This growth is the result of increasing complexity of AV systems requiring routing, processing and control of signals, hence DSM solutions are positioned to provide effective solutions in these areas. Also, the merging AV devices and transition to an IP-centric ecosystem, thus exhibiting the requirement for centralized management, an aspect well performed under a DSM platform. As the demand for seamless, integrated experiences continues to grow, DSM presents the perfect balance of automating processes while also visualizing the omega human interface for its intuitive GUI. As AV technology continues to evolve, DSM's role in providing efficient, reliable, and user-centric audio-visual experiences is likely to become even more essential.

Regional Analysis

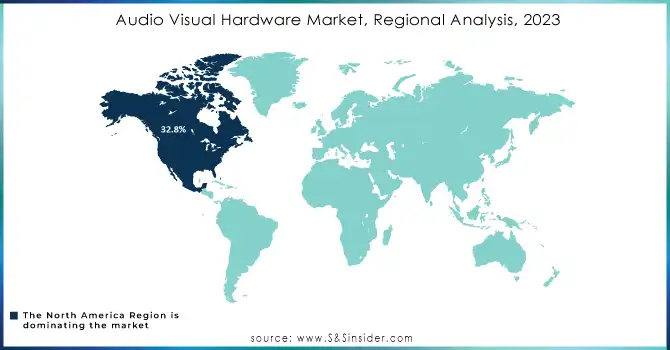

North America dominated the market and accounted for a total market share of 32.8% in 2023. Fewer consumers in the region are still in search of AV solutions that can offer both flexibility and convenience. Premium products still dominate, however there is increasing demand for entry-level models which provide core functionality with more flexibility. For instance In 2023, a notable budget-friendly option was the launch of the Roku Streambar. Combining a soundbar and streaming capabilities, this affordable product provides decent sound projection and clarity, making it an excellent choice for users looking to upgrade their TV's audio without breaking the bank. Although it lacks some of the high-end cinematic features of more expensive models, like advanced surround sound, the Streambar offers great value with 4K HDR support and Bluetooth connectivity. This product is a solid alternative for those with limited space and budget

Asia-Pacific region is expected to see substantial growth during 2024 2032. Factors contributing to this growth include surging demand for smart home solutions, favorable expansion of high-speed internet networks, and adoption of OTT streaming services that are driving increasing demand for high-resolution displays and immersive audio systems. Moreover, academic and corporate settings are adopting AV technology for remote work, e-learning, and virtual meetings. Furthermore, integration of Artificial Intelligence (AI) & Augmented Reality (AR) into AV hardware is creating a better user experience and showcases the demand of intelligence in vehicles that are changed in the region.

Do You Need any Customization Research on Audio Visual Hardware Market - Inquire Now

Key Players

The major key players are

-

Sony Corporation – Sony Bravia XR A80J OLED TV

-

Samsung Electronics – Samsung QLED 8K TV

-

LG Electronics – LG C1 OLED TV

-

Panasonic Corporation – Panasonic 4K Blu-ray Player

-

Bose Corporation – Bose Soundbar 700

-

Vizio Inc. – Vizio 4K Smart TV

-

Harman International – JBL Bar 9.1 Soundbar

-

Sharp Corporation – Sharp 8K TV

-

Epson America Inc. – Epson EF-100 Mini-Laser Projector

-

BenQ Corporation – BenQ TK850i 4K UHD Projector

-

Crestron Electronics – Crestron Mercury Conference System

-

Barco – Barco ClickShare Conference

-

NEC Display Solutions – NEC MultiSync UN552S

-

Mitsubishi Electric – Mitsubishi LaserVue TV

-

Epson – Epson Home Cinema 3800 Projector

-

Pioneer Electronics – Pioneer Elite SC-LX704 AV Receiver

-

Yamaha Corporation – Yamaha YSP-5600 Soundbar

-

JVC Kenwood Corporation – JVC DLA-NX9 4K Projector

-

Harman Kardon – Harman Kardon Citation 500 Speaker

Recent Developments

February 2024: Companies like Sony and LG Electronics have been pushing innovations in high-resolution digital signage, with more widespread adoption of 4K and 8K displays. These are increasingly used in retail and public spaces for dynamic, real-time updates, offering businesses more interactive ways to engage customers.

January 2024: Focus AV discusses the rise of advanced video conferencing solutions and immersive presentation technologies, such as AR and VR, transforming corporate and educational settings. These technologies are revolutionizing business meetings and training, with AI-driven enhancements for automated camera tracking and voice improvements.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 257.2 Billion |

| Market Size by 2032 | USD 450.4 Billion |

| CAGR | CAGR of 6.44% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Equipment, Digital Signal Management (DSM), Cables & Connectors) • By Application (Professional, Consumer) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Sony Corporation, Samsung Electronics, LG Electronics, Panasonic Corporation, Sonos Inc., Bose Corporation, Vizio Inc., Harman International, Sharp Corporation, Epson America Inc., BenQ Corporation, Crestron Electronics, Barco, NEC Display Solutions. |

| Key Drivers | • Growing demand for streaming services and digital media platforms drives the need for high-quality AV equipment. • Educational institutions are increasingly using AV hardware like interactive displays and projectors for digital learning environments. |

| Restraints | • Frequent technological advancements can make AV hardware obsolete quickly, discouraging long-term investments by businesses and consumers. • Integrating AV hardware with existing IT and communication systems can be complex and costly, especially in corporate settings, which may slow down adoption. |

Frequently Asked Questions

Challenges in Audio Visual Hardware Market are

- Frequent technological advancements can make AV hardware obsolete quickly, discouraging long-term investments by businesses and consumers.

- Integrating AV hardware with existing IT and communication systems can be complex and costly, especially in corporate settings, which may slow down adoption.

one main growth factor for the Audio Visual Hardware Market is

- Growing demand for streaming services and digital media platforms drives the need for high-quality AV equipment.

The North America dominated the market and represented significant revenue share in 2023

The CAGR of Audio Visual Hardware Market during the forecast period is of 6.44% from 2024-2032.

Audio Visual Hardware Market was valued at USD 257.2 billion in 2023 and is expected to reach USD 450.4 Billion by 2032, growing at a CAGR of 6.44% from 2024-2032.

Get in Touch