Automotive Active Health Monitoring System Market Report Scope & Overview:

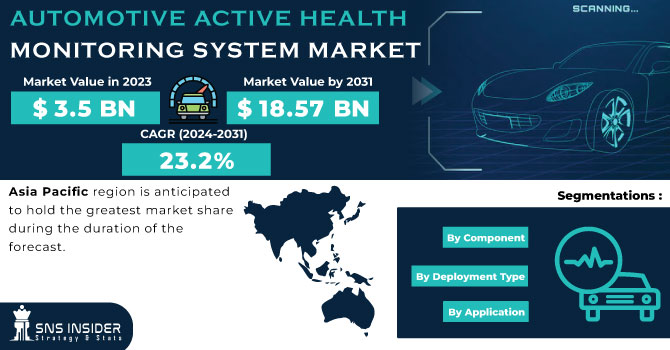

The Automotive Active Health Monitoring System Market size was valued at USD 3.5 billion in 2023 and is expected to reach USD 18.57 billion by 2031 and grow at a CAGR of 23.2% over the forecast period 2024-2031.

Get More Information on Automotive Active Health Monitoring System Market - Request Sample Report

Demand Landscape:

As automotive manufacturers strive to redefine the model of vehicular safety and comfort, the demand for sophisticated active health monitoring systems has surged exponentially. This surge is fueled by an increasing awareness among consumers regarding the paramount importance of health and wellness during transit. Moreover, stringent regulatory mandates mandating the integration of advanced safety features in vehicles have catalyzed market growth. In this competitive environment, key market players are engaged in a relentless pursuit of innovation, striving to unveil cutting-edge solutions that not only monitor vital health metrics in real-time but also offer predictive insights to preempt potential health hazards. The landscape is characterized by a excess of offerings ranging from AI-driven predictive analytics to intuitive user interfaces, each vying for dominance in this burgeoning market segment.

Against this backdrop, strategic collaborations, and partnerships are poised to emerge as pivotal catalysts, facilitating market incumbents to fortify their foothold and expand their market share. As the automotive active health monitoring system market continues to evolve, adaptability, and agility will remain quintessential for stakeholders to capitalize on the myriad opportunities and navigate the complexities inherent in this dynamic ecosystem.

Market Understanding:

An automotive active health monitoring system is a piece of vehicle technology that monitors the driver's health. This technology is found in automobiles. The automotive active health monitor system is an in-vehicle health monitoring system that measures and detects the vital health parameters and biophysical attributes of the driver. These parameters and attributes include the driver's respiration rate, blood pressure, pulse, oxygen saturation, and other important health information. In addition to that, it monitors the driver's level of consciousness as well as their level of tiredness when they are behind the wheel. The vehicle’s active health monitoring system makes use of sensors and infrared cameras in order to recognize and track human facial expressions as well as health data.

Tracking crucial driving indicators such as weariness, sleep deprivation, and distraction is the goal of vehicle health monitoring. The term active health monitoring refers to the use of health technology in a vehicle to increase its safety. Medical technology in a car can have a positive impact on both safety and health and well-being by monitoring vital signs. A bad mood, weariness, irritation, or other medical issues might lead to injuries.

MARKET DYNAMICS:

KEY DRIVERS:

-

Improved cloud-based storage capacity aids long-distance driving.

-

Technological advances and improvements will drive the market.

-

Advances in electronics and microelectronics have led to more cost-effective monitoring devices.

Recent advancements in electronics and microelectronics have catalyzed a important shift in the landscape of automotive active health monitoring systems, rendering them more economically viable and technologically sophisticated. These breakthroughs have empowered manufacturers to develop monitoring devices that not only ensure the safety and well-being of vehicle occupants but also optimize operational efficiency. Leveraging cutting-edge sensor technologies and real-time data analytics, the automotive active health monitoring system market has witnessed a surge in innovation, enabling proactive identification of potential health risks and preemptive intervention strategies. This transformative evolution heralds a new era of automotive safety solutions, where precision engineering converges with cost-effectiveness to redefine the standards of health monitoring within vehicular environments.

RESTRAINTS:

-

Costs make it difficult for developing economies to deploy them in passenger vehicles.

-

The dashboard system includes more components, making it more expensive and hindering the market.

OPPORTUNITIES:

-

The emergence of 5G technology and advances in machine learning.

-

The adoption of the Internet of Things (IoT) is expected to create several new possibilities.

The adoption of the Internet of Things (IoT) is poised to revolutionize the landscape of the Automotive Active Health Monitoring System Market. With IoT integration, automotive health monitoring systems can transcend traditional boundaries, offering real-time insights into vehicle performance and driver well-being. This convergence of technology not only enhances safety but also opens doors to personalized driving experiences and proactive maintenance solutions. By harnessing IoT capabilities, automotive manufacturers can optimize fleet management, predict potential issues, and streamline maintenance schedules, leading to significant cost savings and operational efficiencies.

CHALLENGES:

-

Lack of infrastructure may hinder the active health monitoring system market.

-

Data protection & privacy concerns may hinder the active health monitoring system industry.

IMPACT OF RUSSIA-UKRAINE WAR:

The escalating tensions have disrupted the global supply chain, leading to material shortages and increased production costs for automotive manufacturers. As a result, companies operating in the automotive sector are facing unprecedented challenges in maintaining consistent production levels and meeting consumer demands. The uncertainty surrounding the geopolitical situation has also dampened investor confidence, leading to a slowdown in market growth and innovation within the Automotive Active Health Monitoring System segment. Additionally, heightened geopolitical risks have prompted automotive companies to reassess their sourcing strategies and diversify their supply chains to mitigate potential disruptions in the future. In this volatile landscape, adaptability and resilience have become imperative for businesses to navigate through the challenges posed by the Russia-Ukraine conflict and sustain their presence in the Automotive Active Health Monitoring System Market.

IMPACT OF ECONOMIC SLOWDOWN:

The demand for innovative safety features like Active Health Monitoring Systems, which thrive in prosperous economic climates, experiences a slight decline as consumers prioritize essential expenses over luxury upgrades. Furthermore, reduced purchasing power and tightened budgets among businesses and consumers alike constrain investments in advanced automotive technologies, dampening the growth prospects of the market segment. This downturn forces stakeholders within the automotive industry to recalibrate their strategies, emphasizing cost-efficiency and value propositions to weather the economic storm. Amidst these challenges, opportunities for market players lie in agile adaptation, focusing on streamlining operations, enhancing product affordability, and leveraging technological advancements to maintain competitiveness in a constrained economic landscape. Thus, the impact of economic slowdown on the Automotive Active Health Monitoring System market underscores the imperative for resilience and strategic agility in navigating turbulent economic waters.

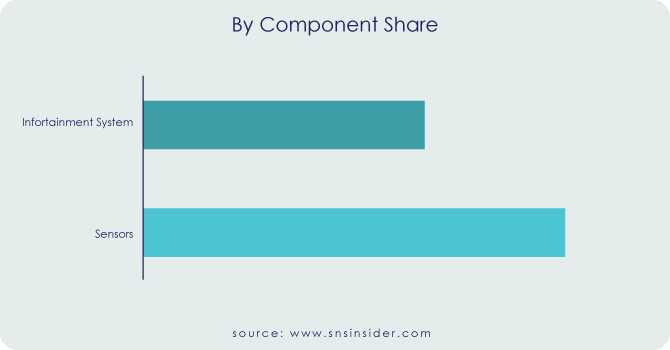

Market, By Component:

The global market has been divided into sensors, and infotainment systems based on the component segment. During the projected period, the others segment, which comprises the infotainment system, camera, processor, and network, is expected to increase at a significant rate. It is expected to grow due to the ongoing development of camera and infotainment systems, as well as the introduction of digital health applications and monitoring systems.

Market, By Application:

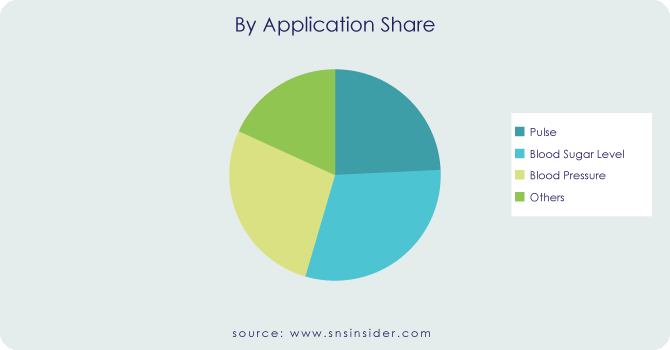

The global market has been divided into Pulse, Blood Sugar Level, Blood Pressure, and Others Based on the application segment. The pulse sector is projected to dominate the market for automobile active health monitoring systems. An increase in the driver's pulse rate is likely to result in an accident. This can be avoided by incorporating an automotive active health monitoring system. As a result, the pulse segment is expected to grow during the projection period.

Market, By Deployment Type:

The global market has been divided into On-premises and Cloud-based based on the deployment type segment. The cloud-based category is expected to dominate the automotive active health monitoring system market. When compared to an on-premises active health monitoring system, the cloud-based active health monitoring system delivers better data security.

MARKET SEGMENTATION:

By Component:

-

Sensors

-

Infotainment System

By Application:

-

Pulse

-

Blood Sugar Level

-

Blood Pressure

-

Others

By Deployment Type:

-

On-premises

-

Cloud-based

REGIONAL ANALYSIS:

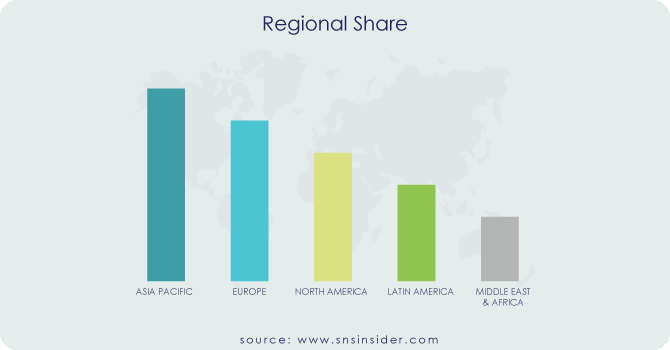

The global market for automotive simulation may be broken down into the following regions: North America, Europe, Asia Pacific, and the rest of the world. In the Automotive Active Health Monitoring System Market, the Asia Pacific region is anticipated to hold the greatest market share during the duration of the forecast. The Asia-Pacific region is home to the world's largest market for automobiles and includes both developing and developing economies, such as China and India. Japan is one of the developed nations in this region. In recent years, this region has developed into a significant center for the production of automobiles. Developments in infrastructure and increasing levels of industrialization in emerging nations have led to the opening of new paths and the creation of many opportunities for automobile original equipment manufacturers (OEMs).

APAC stands as a diverse landscape, boasting rapid urbanization, burgeoning technological advancements, and varying regulatory frameworks across its constituent countries. The market analysis necessitates a granular examination encompassing factors such as economic growth trajectories, shifting consumer preferences, and infrastructure development. With automotive safety gaining paramount importance, the demand for Active Health Monitoring Systems experiences an upward surge.

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of the Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

KEY PLAYERS:

Bosch, Continental, Faurecia (France), TATA Elxsi (India), Acellent Technologies (U.S.), Qualcomm Technologies, Inc, (U.S.), Questex LLC (U.S.), Hoana Medical (U.S.), Kritikal Solutions Pvt. Ltd (India), LORD MicroStrain Sensing Systems (U.S.), and Plessey Semiconductors (UK) are some of the affluent competitors with significant market share in the Automotive Active Health Monitoring System Market.

Recent Developments:

-

Bosch, renowned for its innovative prowess, introduced a cutting-edge health monitoring solution integrated into vehicle seats, ensuring real-time monitoring of driver and passenger well-being.

-

Continental, leveraging its expertise in automotive technology, revealed a sophisticated AI-driven system capable of analyzing vital signs and stress levels, providing proactive alerts to drivers for optimized safety.

-

Denso showcased its advanced sensor technology designed to detect fatigue and distraction, promising enhanced driver awareness and accident prevention. These strategic advancements underscore the commitment of key players to revolutionize automotive safety standards, fostering a safer and more secure driving experience for consumers worldwide.

TATA Elxsi (India)-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 3.5 Billion |

| Market Size by 2031 | US$ 18.57 Billion |

| CAGR | CAGR of 23.2% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Sensors, Infotainment System) • by Application (Pulse, Blood Sugar Level, Blood Pressure, Others) • by Deployment Type (On-premises, Cloud-based) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Faurecia (France), TATA Elxsi (India), Acellent Technologies (U.S.), Qualcomm Technologies, Inc, (U.S.), Questex LLC (U.S.), Hoana Medical (U.S.), Kritikal Solutions Pvt. Ltd (India), LORD MicroStrain Sensing Systems (U.S.), and Plessey Semiconductors (UK) |

| Key Drivers | •Improved cloud-based storage capacity aids long-distance driving. •Technological advances and improvements will drive the market. |

| RESTRAINTS | •Costs make it difficult for developing economies to deploy them in passenger vehicles. •The dashboard system includes more components, making it more expensive and hindering the market. |

Frequently Asked Questions

Ans:- The study includes a comprehensive analysis of market trends, as well as present and future market forecasts. DROC analysis, as well as impact analysis for the projected period. Porter’s five forces analysis aids in the study of buyer and supplier potential as well as the competitive landscape etc.

Ans:- Yes.

Ans:- High cost & dashboard system includes more components making it more expensive are the primary market restraints for Active Health Monitoring System market.

Ans:- An automotive active health monitoring system is a piece of vehicle technology that monitors the driver's health.

Ans:- The market forecast period is 2024-2031 according to the study report.

Get in Touch