Automotive Casting Market Report Scope & Overview:

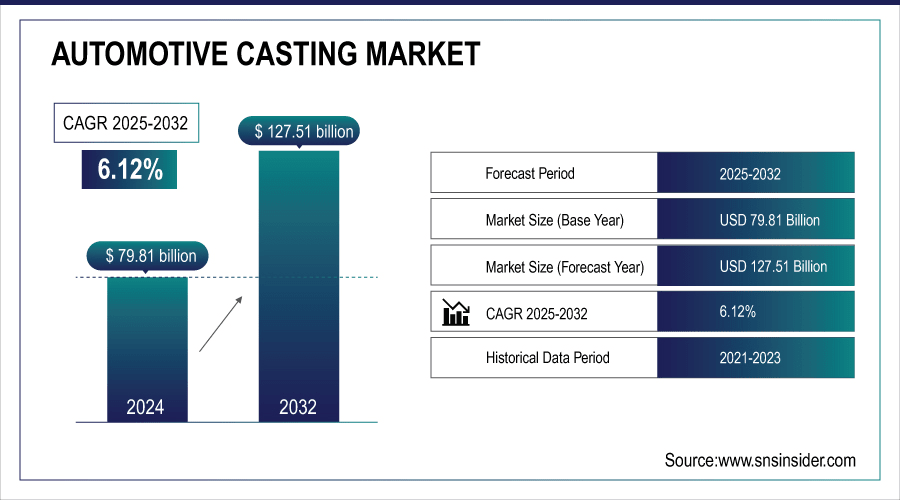

Automotive Casting Market was valued at USD 84.69 billion in 2025 and is expected to reach USD 153.40 billion by 2035, growing at a CAGR of 6.12% from 2026-2035

The Automotive Casting Market is fueled by the rising demand for lighter and fuel-efficient vehicles, the rising production of commercial and passenger vehicles, and the adoption of advanced casting technologies. The rising automotive industry in developing nations, along with the stringent emission norms that promote the adoption of efficient and reliable components, also propels the market. Additionally, the rising investment in electric vehicles and the demand for high-performance engine, transmission, and suspension components also drive the market.

A 2022 summary by the U.S. Department of Energy’s Advanced Manufacturing Office (via the American Foundry Society) highlights insights into global metal casting industries—including those serving the automotive sector. Although historical in nature, this provides context on production patterns in regions like the U.S., China, Europe, Japan, and Brazil.

Tesla’s Giga Press is a revolutionary high-pressure die casting technology that allows single-piece chassis casting, which replaces over 70 components with just one. This technology helps with the production of around 1,000 castings per day at a time of 80-90 seconds, which is a major boost to the production process and meets the trends of light, fuel-efficient, and high-performance components.

To Get More Information On Automotive Casting Market - Request Free Sample Report

Automotive Casting Market Trends

-

Growing automotive production and demand for lightweight, fuel-efficient vehicles are driving casting adoption.

-

Advances in aluminum, magnesium, and hybrid metal castings are improving performance and reducing vehicle weight.

-

Increasing use of precision and high-pressure die casting is enhancing component quality and durability.

-

Rising focus on electric vehicles is boosting demand for specialized cast components.

-

Expansion of automotive aftermarket and replacement parts is supporting market growth.

-

Adoption of automation, robotics, and 3D printing in casting processes is improving efficiency.

-

Collaborations between OEMs, foundries, and material suppliers are accelerating innovation and technology development.

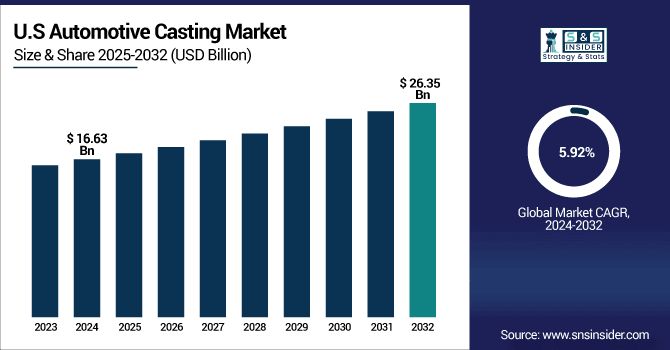

U.S. Automotive Casting Market was valued at USD 17.61 billion in 2025 and is expected to reach USD 31.31 billion by 2035, growing at a CAGR of 5.92% from 2026-2035.

The U.S. Automotive Casting Market is driven by the growing demand for light and fuel-efficient vehicles, the rising production of electric and passenger vehicles, the adoption of advanced casting technology, and the tightening of emission norms, which require the use of high-performance automotive parts.

Automotive Casting Market Growth Drivers:

-

Lightweight vehicle production is increasing globally due to stricter emission regulations and fuel efficiency targets driving automotive casting demand

The automotive sector is experiencing an increasing demand for lightweighting technology in order to meet the stringent requirements of regulations related to emissions and fuel efficiency, thus driving the demand for innovative casting solutions. Aluminum and magnesium casting solutions are increasingly being used as an alternative to heavy steel components, thus resulting in a significant reduction in the overall weight of the vehicle without compromising its strength. This trend not only assists in increasing the fuel efficiency of the vehicle but also improves its performance. Governments worldwide are making it compulsory to meet the requirements, thus forcing OEMs to develop innovative casting solutions.

-

European CO₂ Targets: The European Union mandates a reduction in average CO₂ emissions for new passenger cars to 95 g/km by 2021, with further reductions of 15% by 2025 and 37.5% by 2030, under regulations such as Regulation No 443/2009 and Euro 6 standards. These regulations drive demand for lighter, more efficient automotive components.

-

Forging & Casting Innovations:

-

Ford and Honda have explored forged aluminum connecting rods, achieving up to 30% weight savings over traditional steel or cast designs.

-

Grede, a casting firm within the American Lightweight Materials Manufacturing Innovation Institute, achieved 40% weight reduction and 50% thickness reduction in differential-case components using thin-wall lost-foam casting on existing production lines.

-

Automotive Casting Market Restraints:

-

Fluctuating raw material prices and rising input costs significantly reduce profit margins across global automotive casting industry supply chain

The price of raw materials, especially aluminum, steel, and magnesium, is a major component of the production cost of automotive castings. The volatility of metal prices is one of the factors that add to the instability of the supply chain and make it difficult for manufacturers to estimate costs. The volatility of costs directly affects the profit margins of companies engaged in casting. Additionally, the problem is worsened by geopolitical issues and trade wars, resulting in a shortage of raw materials. The rising costs also affect the R&D expenditure of the manufacturers, thus obstructing the growth of the market.

Automotive Casting Market Opportunities:

-

Expanding use of additive manufacturing and 3D printing in prototyping creates new opportunities for innovation in automotive casting industry

The automotive industry is increasingly adopting additive manufacturing and 3D printing to produce prototypes and molds for casting. The use of 3D printing is opening new avenues for innovation in the automotive industry. The foundries are adopting hybrid models of casting and 3D printing to produce light and high-performance components. The increasing demand for customization and precision engineering is being met by 3D printing, which is opening new avenues for innovation in the automotive industry. The synergy between traditional casting and advanced manufacturing technologies is increasing competitiveness and allowing suppliers to tap new market opportunities.

| Company / Institution | Technology / Innovation | Key Achievements / Stats | Impact on Automotive Casting |

|---|---|---|---|

|

GM – Warren Tech Center |

3D Printing (Various Materials) |

~30,000 prototype parts 3D-printed annually; 3D-printed stainless steel seat bracket 40% lighter and 20% stronger than traditional |

Supports rapid prototyping and integration of additive manufacturing (AM) into casting workflows |

|

Foundry Lab & Eaton |

Digital Metal Casting System (Microwave + Additive Manufacturing) |

Cast aluminum parts with stainless steel pins using hybrid method |

Enables complex internal features, faster turnaround, and merges traditional casting with AM flexibility |

|

Stratasys & Materialise |

Neo Build Processor for SLA 3D Printers |

Up to 50% faster file processing/print speeds; cuts casting pattern lead times by up to 75% |

Accelerates master pattern development for investment casting tooling and prototyping |

|

Waupaca Foundry |

3D-printed cores and molds |

Launch parts faster at reduced cost; improve dimensional control; replace traditional core box tooling; shorten design-to-casting by 2–3 weeks; support reshoring |

Enhances hybrid casting efficiency, precision, and industrial viability for low-volume production |

|

Industry-wide Survey |

Hybrid 3D sand printed cores (binder-jet) |

>90% of foundries have adopted this approach |

Blends conventional green-sand molds with digital cores for high-precision complex assemblies |

|

ZF Friedrichshafen |

Metal filament + Desktop 3D Printers (Prusa, Ultimaker) |

Fabricated large-scale press-dies at North American HQ; implementation expanded globally in Germany |

Accelerates sheet metal forming tooling and supports global manufacturing operations |

Automotive Casting Market Segment Highlights

-

By Material, Aluminium dominated with ~48% share in 2025; Aluminium fastest growing (CAGR).

-

By Vehicle Type, Passenger Vehicles dominated with ~62% share in 2025; Passenger Vehicles fastest growing (CAGR).

-

By Casting Type, Die Casting dominated with ~47% share in 2025; Investment Casting fastest growing (CAGR).

-

By Component, Engine dominated with ~41% share in 2025; Brakes and Wheels fastest growing (CAGR).

-

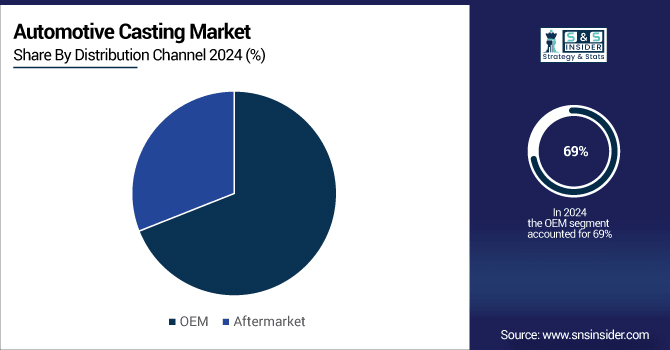

By Distribution channel, OEM dominated with ~69% share in 2025; Aftermarket fastest growing (CAGR).

Automotive Casting Market Segment Analysis

By Distribution channel, OEM dominated while Aftermarket is projected to lead growth

OEM dominated the Automotive Casting Market in 2025 because original equipment manufacturers prefer high-quality, reliable, and durable components. Their emphasis on strict quality requirements, mass production, and long-term business relationships with casting suppliers ensures OEMs have the highest revenue share, leading the automotive casting market.

Aftermarket is projected to register the highest growth rate from 2026-2035, driven by the increasing demand for vehicle maintenance, renovation, and replacement. The increasing vehicle life span, rising consumer interest in upgraded parts, and the rise of independent service facilities are driving the growth of the aftermarket automotive casting market at a rapid pace.

By Process, Die Casting dominated while Investment Casting is projected to lead growth

Die Casting accounted for the major market share in the Automotive Casting Market in 2025 because of its capability to manufacture complex parts with high precision and excellent strength and surface finish. Its efficiency, low production cost, and suitability for mass production in engines, transmissions, and structural automotive components made it the preferred choice for manufacturers, resulting in substantial revenue in the market.

Investment Casting process is anticipated to register the fastest growth between 2026 and 2035, as it enables complex designs, high accuracy, and smooth surface finishes. The use of Investment Casting is on the rise in the production of specialized engine components, aerospace components, and electric vehicles, where high accuracy, strength, and performance are required, thereby driving the growth of the automotive casting market.

By Application, Engine dominated while Brakes and Wheels are projected to lead growth

Engine was the dominant segment in the Automotive Casting Market in 2025 as engines require strong, high-performance, and heat-resistant parts, which are effectively met by casting. The rising demand for fuel-efficient and electric engines, as well as the rising demand for low emissions, is further propelling the demand for cast engine parts.

Brakes & Wheels is expected to witness the highest growth rate during the forecast period 2026-2035, due to the increasing demand for light-weight and high-strength materials to improve the safety and efficiency of vehicles. Rising vehicle production, the use of advanced materials, and the need for performance improvement in commercial and passenger vehicles are expected to drive the high growth rate of this market.

By Material Type, Aluminium dominated while Aluminium is projected to lead growth

Aluminum led the Automotive Casting Market in 2025 because of its light weight, corrosion resistance, and high strength-to-weight ratio, making it the preferred material for engines, transmission parts, and body components. It is projected to register the highest growth rate from 2026 to 2035 as carmakers are expected to increasingly turn to aluminum to meet the growing need for fuel-efficient and environmentally friendly vehicles, including electric vehicles.

By Vehicle Type, Passenger Vehicles dominated while Passenger Vehicles are projected to lead growth

Passenger Vehicles accounted for the largest share in the Automotive Casting Market in 2025, owing to the large production and sales volume across the globe. The market is projected to register the highest growth rate from 2026 to 2035, driven by the rising number of vehicle sales, urbanization, and the growing demand for lighter and fuel-efficient vehicles, as well as the adoption of electric and hybrid passenger vehicles.

Automotive Casting Market Regional Analysis

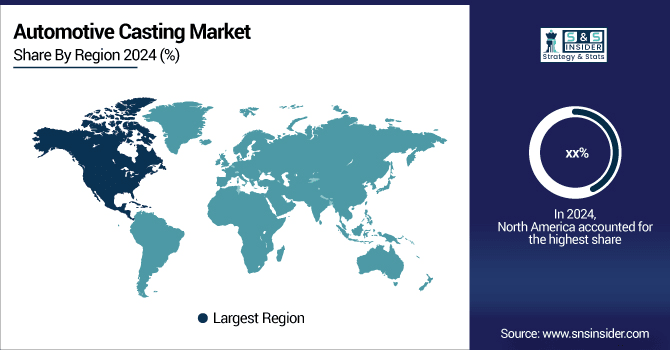

North America Automotive Casting Market Insights

North America represented a prominent market share in the Automotive Casting Market in 2025 because of the well-developed manufacturing facilities, high adoption of innovative casting technology, and strong presence of key automotive OEMs. Increasing demand for lightweight, fuel-efficient, and electric vehicles, along with strict emission and safety standards, is fueling the demand for high-quality cast parts. Technological development and investments in electric mobility also aid the market in the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Automotive Casting Market Insights

Asia Pacific dominated the Automotive Casting Market with about 41% revenue share in 2025 due to rapid industrialization, growing automotive manufacturing facilities, and high demand for passenger and commercial vehicles. The region benefits from cost-effective labor, advanced production technologies, and strong supply chains. Additionally, increasing vehicle exports, rising investments in electric vehicles, and supportive government initiatives for automotive growth contributed significantly to securing the highest market revenue.

Europe Automotive Casting Market Insights

Europe has been a major contributor to the Automotive Casting Market in 2025, thanks to the presence of major automotive players, advanced casting technology, and strict emission and safety standards. The rising demand for light-weight, fuel-efficient, and electric vehicles has led to the increased use of high-quality cast components. Electric mobility, government support, and sustainable manufacturing practices have further fueled the growth of the Automotive Casting Market in the European region.

Middle East & Africa and Latin America Automotive Casting Market Insights

Middle East & Africa had a moderate share in the Automotive Casting Market in 2025 because of the increasing automotive production, rising demand for commercial vehicles, and investments in industrial infrastructure. The rising urbanization, economic development, and adoption of advanced casting technologies are driving the market.

Latin America contributed significantly to the Automotive Casting Market in 2025, supported by expanding vehicle production, rising demand for passenger and commercial vehicles, and growing industrialization. Favorable government policies, infrastructure development, and increasing adoption of lightweight, fuel-efficient components further enhance market growth in the region.

Automotive Casting Market Competitive Landscape:

Aisin Corporation

Aisin Corporation is a key player in the Automotive Casting Market, recognized for producing high-precision, durable components for engines, transmissions, and electric drivetrains. Its focus on lightweight, fuel-efficient, and electrified vehicle parts, combined with a global manufacturing footprint and advanced casting technologies, enables it to meet growing demand for performance, sustainability, and innovation, reinforcing its leadership in the automotive casting sector.

-

2025: Aisin, alongside Toyota Group partners, launched the Toyota Software Academy and Global AI Accelerator (GAIA) to upskill over 100 engineers in AI and software—all toward advancing smart mobility and electrification.

-

2024: Aisin partnered with BMW to co-produce e-axles (build-to-print) in China and Europe, aligning with BMW’s electrification strategy and using Aisin’s global manufacturing footprint.

-

2025: Aisin Takaoka began field trials using Bio-M-Coke, a palm kernel shell–derived biofuel, to replace traditional coke in iron melting—achieving carbon-neutral casting operations with 100% part replacement at partner facilities.

-

2024: Exhibiting at the Automotive Engineering Exposition, Aisin showcased the Xin1 integrated eDrive, a future-ready electric drivetrain, plus advanced safety and convenience solutions like the Intelligent Pillar Unit and AI-powered boarding systems.

Nemak

Nemak is a prominent player in the Automotive Casting Market, specializing in lightweight aluminum and magnesium components for engines, transmissions, and structural automotive parts. Its focus on innovation, sustainability, and high-precision manufacturing enables it to meet the growing demand for fuel-efficient and electric vehicles. Strategic expansions and advanced production technologies strengthen Nemak’s position, supporting global growth and reinforcing its leadership in automotive casting solutions.

-

2025: Nemak agreed to acquire GF Casting Solutions' automotive division for USD 336 million, adding advanced aluminum/magnesium structural component capabilities and production capacity across Europe, China, and the U.S.

-

2023: Nemak completed a major USD 18 million facility expansion in Sheboygan, Wisconsin, adding 35,300 ft² of die-casting production with two 4,500-ton machines to support growth and sustainability in EV components.

Key Players

Some of the Automotive Casting Market Companies

-

Nemak

-

Ryobi Die Casting

-

Rheinmetall Automotive

-

Robert Bosch GmbH

-

Dynacast

-

Pace Industries

-

Gibbs Die Casting

-

Martinrea Honsel

-

Aisin Group

-

Bocar Group

-

Shiloh Industries

-

Endurance Technologies

-

Koch Enterprises

-

Linmar Corporation

-

Sunbeam Lightweighting

-

Cast Products, Inc.

-

Casteks Metal Science Co., Ltd.

-

Bedford Machine & Tool Inc.

-

Alcast Technologies

-

Meridian Lightweight Technologies

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 84.69 Billion |

| Market Size by 2035 | USD 153.40 Billion |

| CAGR | CAGR of 6.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Process(Die Casting, Sand Casting, Investment Casting) • By Application(Transmission and Suspension, Engine, Brakes and Wheels) • By Material Type(Steel, Iron, Aluminium) • By Vehicle Type(Commercial Vehicles, Passenger Vehicles) • By Distribution Channel(OEM, Aftermarket) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nemak, Ryobi Die Casting, Rheinmetall Automotive, GF Casting Solutions, Dynacast, Pace Industries, Gibbs Die Casting, Martinrea Honsel, Aisin Group, Bocar Group, Shiloh Industries, Endurance Technologies, Koch Enterprises, Linmar Corporation, Sunbeam Lightweighting, Cast Products, Inc., Casteks Metal Science Co., Ltd., Bedford Machine & Tool Inc., Alcast Technologies, Meridian Lightweight Technologies |

Frequently Asked Questions

The market was valued at USD 484.69 Billion in 2025 and is projected to reach USD 153.40 Billion by 2035.

Asia Pacific dominated with about 41% revenue share in 2025, driven by industrialization, automotive manufacturing growth, cost-effective labor, and strong supply chains.

Die Casting dominated by process, Engine by component, Aluminium by material, Passenger Vehicles by vehicle type, and OEM by end-user, reflecting high demand and production efficiency.

Key growth factors include rising demand for lightweight, fuel-efficient vehicles, increasing EV production, and adoption of advanced die casting, investment, and precision casting technologies.

The Automotive Casting Market is projected to grow at a CAGR of 6.12% from 2026 to 2035, driven by EV adoption and lightweight vehicle demand.

The market was valued at USD 484.69 Billion in 2025 and is projected to reach USD 153.40 Billion by 2035.

Get in Touch