Automotive Brake Shims Market Report Scope & Overview:

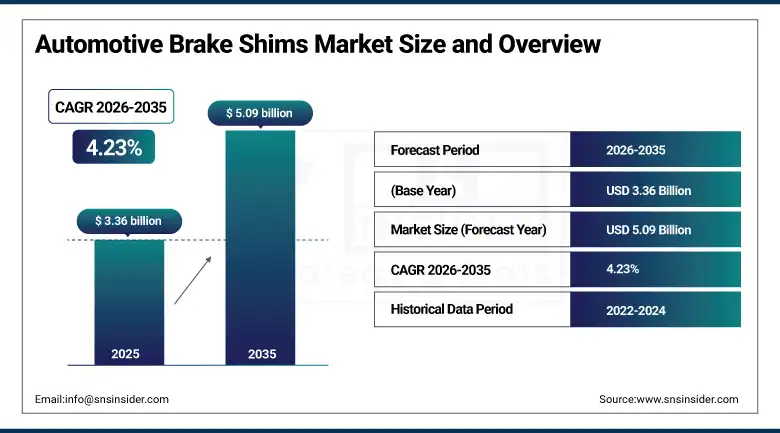

The Automotive Brake Shims Market was valued at USD 3.36 Billion in 2025 and is expected to reach USD 5.09 Billion by 2035, growing at a CAGR of 4.23% from 2026–2035.

The global market for automotive brake shims is witnessing sustained growth owing to an increase in car manufacturing, tightening NVH regulations, and the trend towards electric vehicles. Brake shims refer to a dampener used between brake pads and callipers to reduce the noise and vibrations produced during braking. The economic significance of brake shims has been heightened by increased consumer demands in terms of quiet cabin for automobiles, a feature initially available only in luxury cars but now sought after in both consumer and commercial vehicles. An electric vehicle makes this demand even more crucial because, without the sound of the engine, any problem with the NVH of the brake will be instantly noticed by the occupants of the car. This has been recognized by OEMs, who work directly with the manufacturers of the shims on designing multilayered parts made of various materials.

Electric vehicle production is reshaping brake shim specification requirements at the OEM level. Without engine noise to mask braking sounds, even minor NVH deficiencies are immediately perceptible to vehicle occupants. Automakers have responded by elevating brake shim acoustic performance from a comfort attribute to a compliance-driven engineering requirement. Global disc brake adoption in emerging markets is simultaneously expanding the addressable brake shims market geographically, as disc braking configurations require shim components that drum brake systems do not.

Market Size and Forecast

-

Market Size in 2026E: USD 3.50 Billion

-

Market Size by 2035: USD 5.09 Billion

-

CAGR: 4.23% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Automotive Brake Shims Market - Request Free Sample Report

Automotive Brake Shims Market Trends

-

Rising EV production is accelerating demand for advanced rubber and composite brake shims that provide effective NVH suppression in powertrains lacking engine noise to mask braking vibration during low-speed deceleration events.

-

Growing adoption of multilayer shim designs is enabling OEMs to meet tighter acoustic standards by combining metallic structural rigidity, rubber damping, and ceramic thermal protection within a single precision-engineered braking component.

-

Increasing regulatory pressure on vehicle noise emissions in Europe and North America is compelling automakers to elevate braking system acoustic specification from a comfort feature to a compliance-driven engineering requirement.

-

Expanding use of lightweight composite and polymer materials in brake shim construction is supporting vehicle weight reduction targets while maintaining thermal stability and vibration control performance across high-temperature braking cycles.

-

Growing aftermarket activity driven by ageing global vehicle fleets is creating demand for premium replacement brake shims that match OEM acoustic and performance specifications rather than commodity cost-only alternatives.

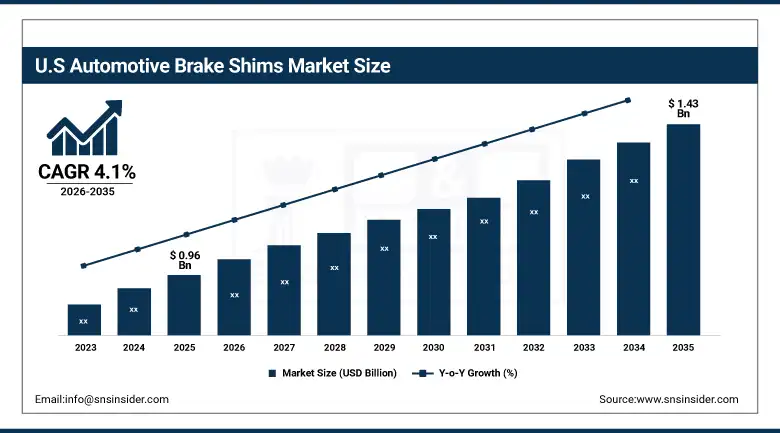

U.S. Automotive Brake Shims Market Outlook

The U.S. Automotive Brake Shims Market was valued at approximately USD 0.96 Billion in 2025 and is expected to reach approximately USD 1.43 Billion by 2035, growing at a CAGR of approximately 4.1%.

The U.S. market is driven by a combination of high vehicle production volumes, stringent federal and state noise emission standards, and an above-average rate of electric vehicle adoption that is reshaping brake shim material specification requirements across OEM procurement. American consumers place a high commercial premium on braking system quietness across all vehicle price tiers. This expectation creates direct procurement pressure on OEMs to validate brake shim performance at the system level during vehicle development programmes. The aftermarket channel is significant. The large U.S. vehicle fleet age, combined with widespread DIY brake maintenance culture and the commercial availability of OEM-equivalent shim replacement kits, sustains consistent aftermarket demand independent of new vehicle production cycles.

Brembo S.p.A. launched a new line of eco-friendly brake shims made from recycled materials in March 2024. This development directly targeted North American OEM procurement teams seeking sustainable component alternatives that comply with corporate ESG commitments without compromising the acoustic performance and thermal durability standards that braking system engineers require from NVH components installed in production vehicles.

Automotive Brake Shims Market Segment Analysis

-

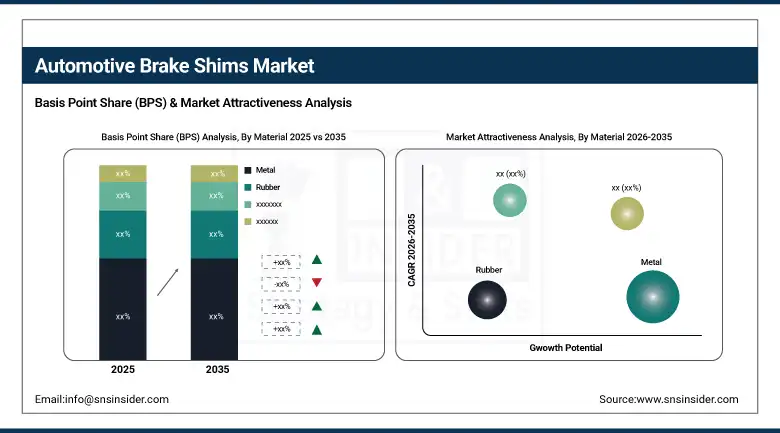

By Material, metal brake shims dominated with approximately 47.23% revenue share in 2023, providing the structural strength and thermal resistance required for high-performance and combustion engine vehicle braking applications. Rubber brake shims are the fastest-growing material segment at a CAGR of 5.62%.

-

By Sales Channel, OEM accounted for approximately 71.40% of total revenues in 2023, reflecting OEM braking system integration of engineered shim specifications from early vehicle development stages. The aftermarket segment is the fastest-growing sales channel at a CAGR of 4.74%.

-

By Vehicle Type, passenger cars dominated the automotive brake shims market in 2025 as the highest-volume vehicle segment globally, generating the greatest aggregate shim procurement volume across both OEM and aftermarket channels. Electric vehicles are the fastest-growing vehicle type.

-

By Application, disc brakes dominated the automotive brake shims market in 2025, driven by the global shift from drum to disc braking systems across passenger cars and commercial vehicles that has progressively displaced drum brake applications across mainstream vehicle categories.

By Material, metal dominates, rubber grows fastest

Metal brake shims retained the dominant material position with approximately 47.23% of the metal shims emerged as the leading type in the automotive brake shims market with an approximated share of 47.23% in 2023, as they provide real benefits from an engineering perspective. The metals used, such as steel and aluminium, have proven their ability to withstand the high temperatures created during repeated braking without compromising dimensional stability and noise dampening capacity. Metallic shims are chosen by OE brake systems designers because the temperatures involved exceed the thermal resistance limits of rubber and other polymer substitutes. Metal shims' precise stamping facilitates tight dimensional tolerances necessary for integration into a brake system. Steel is the most preferred metal since it combines high strength, competitiveness in price, and qualification data by OE manufacturers.

Rubber brake shims are the fastest-growing material segment at a CAGR of 5.62% through 2035. The commercial driver is the electric vehicle market’s NVH requirement, which is structurally more demanding than conventional vehicle braking acoustic standards. Electric vehicles operate without engine noise across low-speed driving scenarios where brake application occurs most frequently. Any NVH deficiency in the braking system is directly audible to vehicle occupants in a way that conventional powertrains mask through ambient drivetrain sound. Rubber shims’ superior vibration damping characteristics address this requirement more effectively than metal alternatives at equivalent cost. Their thermal resilience and compatibility with both ceramic and metallic brake pads make them versatile across the broad range of EV braking configurations that different platform architectures deploy. Tier-1 suppliers including Trelleborg and Nisshinbo are expanding their rubber shim portfolios specifically to serve growing EV OEM specifications globally.

By Sales Channel, OEM dominates, aftermarket grows fastest

OEM retained the dominant sales channel position with approximately 71.40% of the automotive brake shims market in 2023. This dominance is structurally supported by the integration of brake shim specifications into braking system design programmes from the earliest vehicle engineering stages. OEM braking system engineers do not select shims as an afterthought. They specify shim material, geometry, and acoustic performance requirements as part of the braking system noise and vibration validation programme that every new vehicle platform must pass before regulatory certification and production launch approval. This early integration creates long-term supply agreements between shim manufacturers and tier-1 braking system suppliers whose production volumes are locked for the duration of a vehicle model’s production life. The OEM channel consequently generates highly predictable revenue with substantially lower selling cost per unit than the aftermarket channel.

The aftermarket segment is the fastest-growing sales channel at a CAGR of 4.74% through 2035. This growth reflects the commercial opportunity created by the global vehicle fleet’s age profile. Vehicles produced 5 to 15 years ago are now entering the primary brake maintenance replacement window. Brake shim replacement is a standard component of brake pad service events. Consumers replacing brake pads at independent garages and through DIY maintenance are increasingly selecting premium replacement shim kits that replicate OEM acoustic performance rather than substituting lower-cost generic alternatives that do not match the original braking system’s noise specification. Aftermarket shim packaging and online retail distribution have improved significantly, making premium replacement shims accessible through the e-commerce channels that an increasing proportion of DIY and professional aftermarket parts procurement now flows through.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.4% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Automotive Brake Shims Market Insights

North America is a significant automotive brake shims market, with the United States accounting for approximately 82.5% of North American revenues. The market is characterised by a combination of high new vehicle production standards requiring advanced NVH compliance, a large and ageing vehicle fleet generating consistent aftermarket replacement demand, and above-average EV adoption rates that are progressively shifting OEM brake shim specifications toward rubber and composite material alternatives. Major OEM programmes at Ford, General Motors, and Stellantis specify engineered brake shim solutions that meet the acoustic standards North American consumers expect across all vehicle price tiers, creating sustained procurement demand from the braking system tier-1 suppliers serving these platforms.

Canada contributes approximately 17.5% of North American revenues through its significant vehicle assembly operations serving both domestic and export markets, the aftermarket demand generated by its large in-service vehicle fleet, and the progressive adoption of EV braking system specifications by Canadian OEM assembly plants that are producing electric vehicle variants of established North American platform families in response to federal zero-emission vehicle targets.

Europe Automotive Brake Shims Market Insights

Europe is a technologically sophisticated automotive brake shims market where EU vehicle noise regulation under the UN ECE R51.03 standard and the Euro 7 emissions framework are creating measurable regulatory pressure on automotive OEMs to improve braking system acoustic performance. Germany accounts for approximately 28.4% of European revenues as the region’s largest automotive manufacturing market, driven by the premium vehicle OEM programmes of Volkswagen Group, BMW, Mercedes-Benz, and their tier-1 braking system supplier ecosystem that demands the highest acoustic and thermal performance specifications from brake shim components across both ICE and electrified vehicle platforms.

ZF Friedrichshafen AG launched eco-friendly brake shims made from recyclable materials in 2024, directly targeting European OEM procurement teams operating under corporate sustainability mandates that require demonstrable environmental credentials from braking system component suppliers. This development reflects the broader European automotive supply chain’s progressive integration of lifecycle sustainability criteria into component qualification processes alongside the traditional performance and cost specifications that have historically defined brake shim supplier selection.

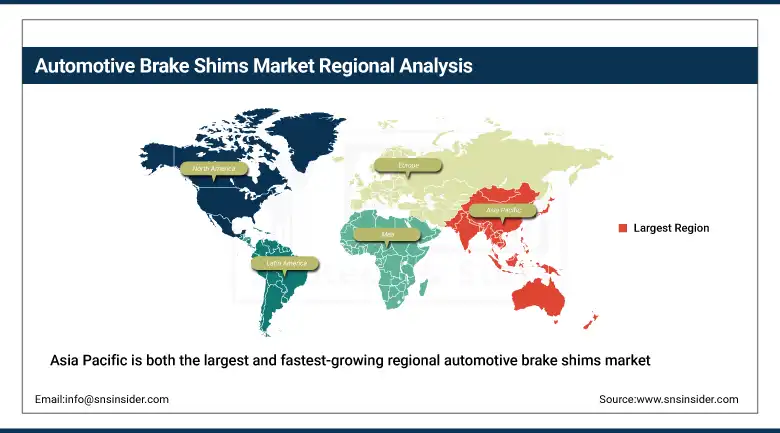

Asia Pacific Automotive Brake Shims Market Insights

Asia Pacific is both the largest and fastest-growing regional automotive brake shims market, accounting for the majority of global market revenues through China’s extraordinary vehicle production scale, Japan’s technically demanding OEM quality standards, India’s rapidly expanding vehicle production base, and South Korea’s globally significant automotive export programmes. China accounts for approximately 54.6% of Asia Pacific revenues through its combination of the world’s highest annual vehicle production volume, a rapidly growing EV fleet that creates structurally elevated brake shim acoustic requirements, and a domestic braking component supply chain whose scale and engineering capability have progressively improved to serve both domestic and international OEM specifications.

India represents the most commercially significant emerging market within Asia Pacific for automotive brake shims, as the country’s vehicle production volume growth, the progressive tightening of CMVR braking system standards, and the introduction of EV manufacturing programmes by Tata Motors, Mahindra, and international OEMs establishing domestic production are collectively creating a growing market for engineered brake shim solutions that exceed the acoustic and thermal performance of the commodity alternatives that previously dominated Indian vehicle braking system supply chains. Uno Minda’s January 2025 introduction of Heavy Duty Organic Brake Pads with RMR (Rubber Metal Rubber) Shims demonstrates the indigenous capability development occurring within the Indian braking system supply chain.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Automotive Brake Shims Market Insights

The Middle East and Africa and Latin America are growing automotive brake shims markets where expanding vehicle production, rising consumer safety and comfort expectations, and the progressive adoption of disc braking systems across previously drum-brake-dominated vehicle segments are creating growing demand for engineered shim components. Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through its significant vehicle imports, the commercial investment of major international automotive brands in the Kingdom’s growing consumer vehicle market, and the Saudi government’s Vision 2030 automotive sector development initiatives that are expanding local vehicle assembly operations.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its significant domestic vehicle production base that includes manufacturing operations for Volkswagen, Fiat Chrysler, General Motors, Toyota, and Renault whose combined production volumes create sustained OEM brake shim procurement demand. The Brazilian aftermarket is also commercially significant, driven by the large in-service vehicle fleet whose age profile and high annual mileage create brake maintenance replacement cycles that support consistent brake shim aftermarket demand through independent garage and retail distribution channels.

Market Dynamics

Growth Drivers: Electric vehicle production growth elevating brake shim NVH specification requirements, global disc brake adoption expanding addressable market

Electric vehicle adoption is the most commercially transformative demand driver for the brake shims market. EVs eliminate engine noise that previously masked braking NVH in conventional vehicles. This creates an engineering requirement for higher-performance acoustic damping throughout the braking system. Brake shim material specifications are being elevated as a direct consequence. Higher-specification shims generate higher per-unit revenue for manufacturers. This per-unit value growth is compounding with EV production volume growth to create a commercially significant demand expansion that is concentrated within the rubber and composite material segments whose NVH performance is best suited to EV braking system requirements.

The trend towards the replacement of drum by disc brake setups in developing countries on a worldwide basis is also having the effect of extending the addressable market for brake shims globally at the same time. Disc brake setups need shims. Drum brake setups do not. As the manufacture of cars and trucks in India, Southeast Asia, and Latin America increasingly adopts disc brake setups, the worldwide brake shim addressable market expands in step with it. The expansion is irrespective of growth in automobile manufacture, which produces its own increase in demand.

Restraints: Raw material cost volatility for steel, rubber, and composite inputs, and supply chain complexity in multi-material shim manufacturing creating quality consistency challenges

Steel, rubber compound, and composite material input costs are subject to commodity price volatility that directly impacts brake shim manufacturing margins. Brake shim manufacturers operating on relatively thin margins in the OEM channel face procurement cost pressure when steel or synthetic rubber prices move adversely, as OEM supply agreements typically constrain the price adjustment flexibility that is needed to pass input cost increases through to customers in short timeframes.

Multi-material brake shims combining metallic, rubber, and adhesive layers require precision manufacturing processes whose quality consistency across high-volume production runs is operationally demanding. Delamination, adhesive bond failure, or dimensional inconsistency at any layer interface creates acoustic performance degradation that is difficult to detect through visual inspection and may only manifest during vehicle NVH validation testing, creating rework cost and production delay risks that quality management investment must mitigate.

Opportunities: EV-specific multilayer shim product development, aftermarket premium segment growth, and regenerative braking system integration creating new shim design requirements

EV-specific multilayer brake shim product development represents the most commercially valuable near-term innovation opportunity. Automakers are requesting brake shim solutions engineered specifically for regenerative braking system architectures, where the transition between regenerative and friction braking creates specific vibration signatures that conventional shim designs were not optimised to suppress. Suppliers that develop validated EV braking system shim solutions gain first-mover specification advantages in OEM programmes whose multi-year production volumes make supply agreement values commercially significant.

The aftermarket premium segment is growing as brake repair professionals and consumer vehicle owners increasingly recognise that OEM-specification brake shim replacement delivers measurably superior braking quietness compared to commodity alternatives. Online retail platforms have improved premium replacement shim product discovery and price comparison for professional buyers and DIY consumers alike, creating a distribution channel efficiency improvement that is translating into aftermarket revenue growth for shim manufacturers willing to invest in aftermarket packaging, part number coverage, and online merchandising capability.

Recent Developments:

-

2025: Uno Minda introduced Heavy Duty Organic Brake Pads with RMR (Rubber Metal Rubber) Shims in India in January 2025, improving friction stability, thermal resistance, and NVH performance for commercial vehicle applications, reflecting the growing sophistication of the Indian braking system supply chain and the domestic OEM market’s rising acoustic performance requirements for mass-market vehicle programmes.

-

2025: Akebono Brake Industry Co., Ltd. entered into a partnership with a leading electric vehicle manufacturer in June 2025 to develop specialised brake shims engineered for electric vehicle braking system architectures, directly addressing the elevated NVH performance requirements that EV drivetrains create for braking system acoustic management.

-

2024: Brembo S.p.A. launched a new line of eco-friendly brake shims made from recycled materials in March 2024, targeting automotive OEM procurement teams seeking sustainable component alternatives that satisfy corporate ESG commitments without compromising the acoustic performance and thermal durability standards that braking system engineers require for production vehicle qualification.

Automotive Brake Shims Market Key Players

-

Robert Bosch GmbH

-

ZF Friedrichshafen AG

-

Brembo S.p.A.

-

Akebono Brake Industry Co., Ltd.

-

Nisshinbo Holdings Inc.

-

Trelleborg AB

-

Valeo S.A.

-

Continental AG

-

Federal-Mogul LLC

-

Meneta

-

NUCAP Industries Inc.

-

EBC Brakes

-

TMD Friction Holdings GmbH

-

Sangsin Brake

-

Uno Minda Limited

-

Hella Pagid GmbH

-

ITT Inc. (Wolverine Brakes)

-

DRiV Inc.

-

Shandong Gold Phoenix Co., Ltd.

-

Rizhao DSS International Trading Co., Ltd

Automotive Brake Shims Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.36 Billion |

| Market Size by 2035 | USD 5.09 Billion |

| CAGR | CAGR of 4.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Metal, Rubber, Composite, Ceramic, Others) • By Sales Channel (OEM, Aftermarket) • By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles) • By Application (Disc Brakes, Drum Brakes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Robert Bosch GmbH, ZF Friedrichshafen AG, Brembo S.p.A., Akebono Brake Industry Co., Ltd., Nisshinbo Holdings Inc., Trelleborg AB, Valeo S.A., Continental AG, Federal-Mogul LLC , Meneta, NUCAP Industries Inc., EBC Brakes, TMD Friction Holdings GmbH, Sangsin Brake, Uno Minda Limited, Hella Pagid GmbH, ITT Inc. (Wolverine Brakes), DRiV Inc., Shandong Gold Phoenix Co., Ltd., Rizhao DSS International Trading Co., Ltd. |

Frequently Asked Questions

Asia Pacific dominated the Automotive Brake Shims Market in 2025, driven by China’s extraordinary vehicle production scale and the region’s rapidly expanding electric vehicle manufacturing base.

Metal brake shims dominated with approximately 47.23% revenue share in 2023, driven by their structural strength and thermal resistance in high-performance vehicle braking applications.

Rising electric vehicle production creating structurally elevated brake NVH specification requirements, global disc brake adoption expanding the addressable market in emerging regions, and the extension of premium acoustic standards from luxury to mainstream vehicle segments that is elevating per-unit brake shim specification and value across OEM procurement programmes.

The Automotive Brake Shims Market was valued at USD 3.36 Billion in 2025.

The Automotive Brake Shims Market is expected to grow at a CAGR of 4.23% from 2026 to 2035.

Get in Touch