Autonomous Construction Equipment Market Report Scope & Overview:

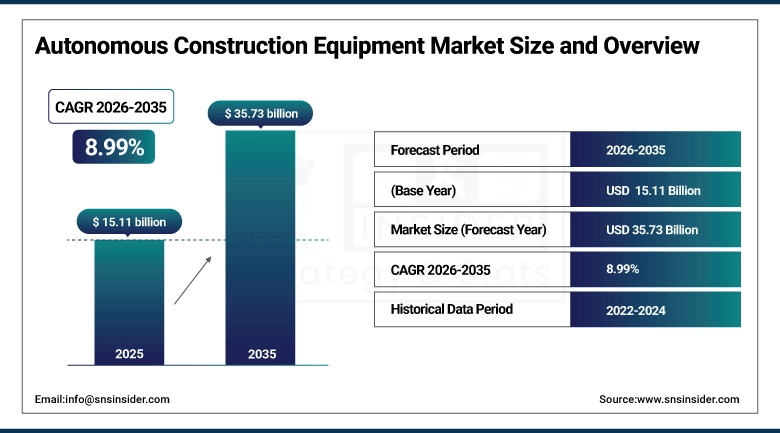

The Autonomous Construction Equipment Market size was valued at USD 15.11 Billion in 2025 and is projected to reach USD 35.73 Billion by 2035, growing at a CAGR of 8.99% during 2026–2035.

The Autonomous Construction Equipment Market is witnessing substantial growth due to technological advances in automation and AI along with the continued labor shortage around the world in the construction sector. Technology such as AI, machine learning, GPS, sensors, etc., has helped increase the accuracy, safety, and efficiency of construction equipment like never before. With the incorporation of autonomous technology into construction equipment such as excavators, graders, pavers, loaders, and material handling equipment, the number of human errors has been reduced and projects have become more efficient and timely from the years 2021 to 2035.

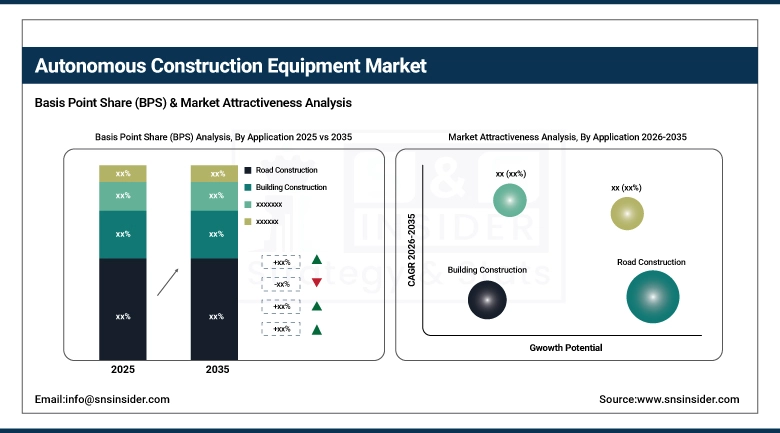

The semi-autonomous equipment segment dominated with over 62% market share in 2024, while road construction applications led adoption with more than 42% share reflecting the mature commercial deployment of GPS-guided precision grading, paving, and material handling in highway and infrastructure construction projects globally.

Market Size and Forecast:

-

Market Size in 2025: USD 15.11 Billion

-

Market Size by 2035: USD 35.73 Billion

-

CAGR: 8.99% (from 2026 to 2035)

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To get more information on Autonomous Construction Equipment Market - Request Free Sample Report

Autonomous Construction Equipment Market Trends Highlights:

-

Technological advances in AI, machine learning, GPS, and sensor technology enhancing autonomous equipment precision and reliability

-

Persistent global construction labor shortages accelerating adoption of autonomous and semi-autonomous machinery to maintain productivity

-

Road construction segment leading adoption with 42%+ share driven by grading, paving, and material handling automation maturity

-

Electric-powered autonomous equipment gaining momentum as emissions regulations intensify in urban construction environments

-

Semi-autonomous segment dominant at 62% reflecting broad commercial acceptance; fully autonomous growing fastest as technology matures

-

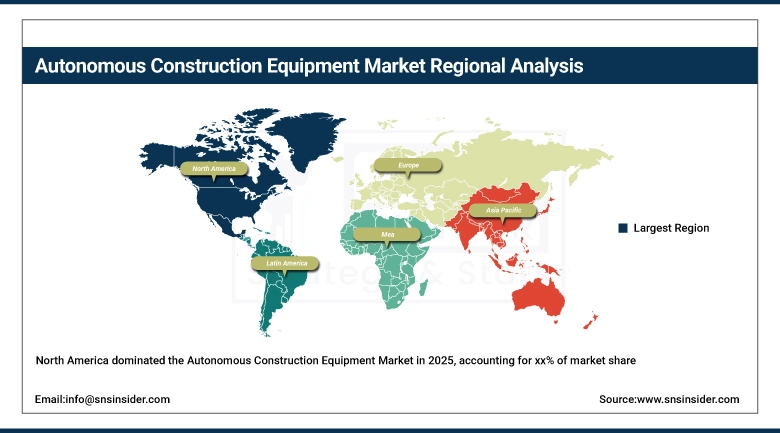

North America leads the market while Asia-Pacific is expected to register the fastest CAGR through 2026–2035

U.S. Autonomous Construction Equipment Market Size Outlook:

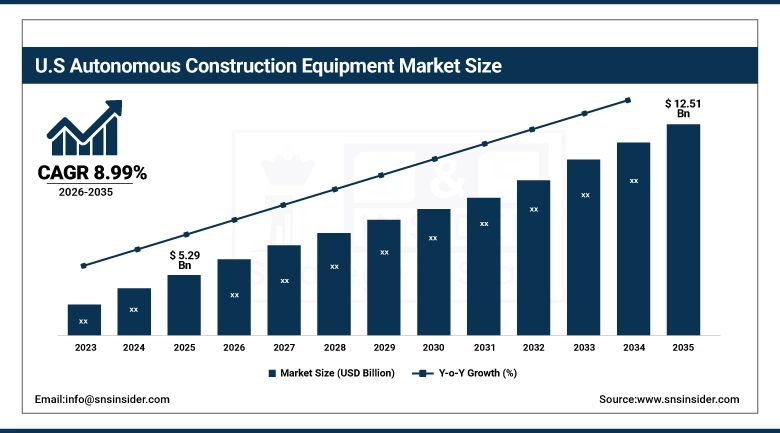

The U.S. Autonomous Construction Equipment Market was valued at USD 5.29 Billion in 2025 and is expected to reach USD 12.51 Billion by 2035, growing at a CAGR of 8.99% from 2026–2035. The growth factors include the U.S. government’s infrastructure investment initiatives, the continual shortage of skilled laborers, and the widespread use of GPS and AI-powered machines for highway constructions, mining, and massive commercial buildings. Major original equipment manufacturers (OEMs) such as Caterpillar, Deere & Company, and Komatsu in North America ensure that there is an ongoing flow of autonomous machines’ innovation and implementation.

Autonomous Construction Equipment Market Segment Highlights:

-

By Autonomy Level: Semi-Autonomous (Dominant – 62%+ share in 2025); Fully Autonomous (Fastest Growing through 2026–2035)

-

By Application: Road Construction (Dominant – 42%+ share in 2025); Building Construction (Fastest Growing through 2026–2035)

-

By Equipment Type: Earthmoving Equipment (Dominant); Material Handling (Fastest Growing through 2026–2035)

-

By Power Source: Diesel (Dominant currently); Electric (Fastest Growing through 2026–2035)

By Application, Road construction segment dominated, Building Construction is fastest growing segment

Road construction dominated the Autonomous Construction Equipment Market with over 42% application share in 2025, owing to the appropriateness of high-quality tasks involved in road construction for autonomous equipment with an environment characterized by predictability of operations and task management which matches present autonomous technology. Autonomous graders, pavers, and material handlers have demonstrated significant gains in these environments.

The Building Construction segment will see growth at the fastest pace from 2026 to 2035, with increasing rates of urbanization around the world driving up demand for construction firms in search of automation technologies to overcome labor shortage and high costs in competitive urban construction environments.

By Autonomy, Semi-autonomous equipment segment dominated the market, Fully Autonomous is fastest growing segment

The semi-autonomous equipment segment dominated the Autonomous Construction Equipment Market with over 62% market share in 2025, due to its commercial viability, widespread adoption in the industry, and affordability compared to its autonomous counterparts. The addition of features such as GPS navigation technology, telematics, remote diagnostics, and automated control systems in semi-autonomous equipment improves efficiency and safety while still providing manual control to address uncertain and challenging site conditions.

The fully autonomous category is expected to have the highest growth rate during 2026-2035 because advancements in artificial intelligence and improved sensor fusion technology will eventually allow the operator to rely less on human interaction in construction activities.

Autonomous Construction Equipment Market Regional Analysis

|

Region |

Major Country |

Share (%) |

|---|---|---|

|

North America |

United States |

79.0% |

|

Europe |

Germany |

22.0% |

|

Asia Pacific |

China |

28.0% |

|

Middle East & Africa |

Saudi Arabia |

8.0% |

|

Latin America |

Brazil |

7.0% |

North America Autonomous Construction Equipment Market Insights:

North America is one of the largest markets for autonomous construction equipment in 2025, due to large-scale investments in infrastructure programs, highly developed ecosystems of OEMs like Caterpillar and Deere & Company, and labor shortages in the construction industry in both the U.S. and Canada that are pushing towards more autonomy in machinery use. Large federal infrastructure spending packages have created many projects in the building of roads, bridges, and utilities, where autonomous machines have shown a clear advantage over conventional machines. A highly developed infrastructure for GPS and telematics supports the implementation of autonomous technology in North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Caterpillar's autonomous haulage system has accumulated over one billion tonnes of material moved across mining operations globally demonstrating the extraordinary operational reliability and commercial maturity that autonomous heavy equipment has achieved in high-intensity applications, creating the performance track record that is accelerating adoption across adjacent construction applications globally.

Asia-Pacific Autonomous Construction Equipment Market Insights:

Asia-Pacific is expected to register the fastest CAGR in the Autonomous Construction Equipment Market through 2026–2035, due to the tremendous investments in infrastructure development, fast urbanization that has caused huge volumes of construction work, and smart construction activities undertaken by governments. The infrastructure development projects being pursued by China such as high-speed railroads, urban areas development, and industrial zones development have caused an incredible amount of demand for productivity-based autonomous equipment. The construction industry in Japan has been more active towards utilizing autonomous construction equipment because of the shortage of construction workers in the country.

Japan's construction sector faces one of the most severe skilled labor shortages in the world, with the construction workforce aging rapidly and new workforce entrants insufficient to replace retirements creating a structural, long-term demand driver for autonomous construction equipment that will sustain Japan's position as one of Asia-Pacific's most commercially advanced markets for autonomous machinery adoption through 2035.

Europe Autonomous Construction Equipment Market Insights:

Europe holds a significant share of the Autonomous Construction Equipment Market in 2025, owing to the increasing focus on safety at the construction sites, investments in upgrading the infrastructure facilities, and the presence of sustainability initiatives promoting the usage of electric autonomous machines in urban construction sites which are sensitive from the perspective of emissions. The major contributors to the market in Europe will include Germany, UK, France, and the Nordics, as all the nations are making considerable investments in smart construction technologies, including autonomous machines.

Middle East & Africa and Latin America Autonomous Construction Equipment Market Insights:

The Middle East, Africa, and Latin America showed increasing involvement in their autonomous construction equipment markets in 2025, owing to massive construction infrastructure projects in Gulf countries, increased mining in Africa and Latin America, and increased investments in construction by private companies in Brazil, Mexico, Saudi Arabia, and the United Arab Emirates. Massive projects in Gulf countries such as NEOM in Saudi Arabia and several other projects in the UAE rank among some of the most impressive construction projects globally, and the need for autonomous construction equipment with high efficiency to work under extreme weather conditions is expected to be enormous.

Autonomous Construction Equipment Market Drivers:

-

Global construction labor shortages and safety imperatives accelerate autonomous equipment adoption across all construction segments

The increasing scarcity of qualified construction labor, resulting from the aging population in advanced countries, challenging working conditions, and rivalry from other industries, is serving as an influential structural pull factor for self-governed and partially self-governed construction machines that can operate productively without needing the complete number of human operators. Autonomous machines help address the critical issues concerning the safety of the construction industry because they eliminate the risk of human involvement while handling the construction machines and working in hazardous situations such as extreme climatic conditions and uneven terrain. The rise in government safety regulations specifying safe distances between workers and heavy construction machinery adds another dimension to the demand for autonomous functionality.

According to industry data, autonomous construction equipment can reduce operational costs by 15–25% while improving productivity by up to 30% compared to conventional human-operated machinery in standardized construction tasks quantifiable performance advantages that are driving rapid commercial adoption across highway construction, mining, and large-scale infrastructure development globally.

-

AI, GPS, and IoT technology convergence enables increasingly capable and commercially viable autonomous construction systems

The integration of computer vision technology using artificial intelligence, highly accurate GPS technology, IoT sensor systems, and telematics technology is increasingly becoming a reality in developing construction equipment with self-driving technology that is reliable and affordable. With machine learning technology trained on large amounts of data on operations, the technology is able to identify construction site conditions, adjust to changing terrain conditions, and undertake complicated sequences of actions without much human interaction. The connectivity of this technology through the cloud ensures monitoring of equipment performance and maintenance of the equipment and even helps in optimizing the efficiency of fleets.

Autonomous Construction Equipment Market Restraints:

-

High upfront costs, complex site conditions, and regulatory frameworks constrain autonomous equipment adoption pace

One of the significant limitations that Autonomous Construction Equipment Market experiences is associated with the large initial capital expenditure needed to invest in autonomous equipment. The cost of autonomous equipment is often significantly higher than that of traditional machines. This factor makes autonomous construction equipment expensive and difficult to justify in the case of smaller companies operating in developing countries due to the lack of quick returns on investment opportunities for such equipment especially if the equipment will operate in diverse locations. The fact that autonomous machines are subject to numerous variables and uncertainties of construction site locations is another issue that complicates their usage. In addition, there are no regulatory guidelines for liability and safety of autonomous machines used in the construction sector.

Autonomous Construction Equipment Market Opportunities:

-

Electric Autonomous Equipment Innovation and Infrastructure Mega-Projects Create Exceptional Commercial Growth Opportunities

One of the most significant innovation opportunities that the Autonomous Construction Equipment Market will see until 2035 is the combination of equipment electrification and automation. Electric autonomous equipment is emission-free, noise-free, and economically efficient compared to the combustion type as per the emissions standards that are being imposed by authorities for the construction industry. Top construction equipment OEMs are currently designing electric autonomous platforms for excavators, loaders, and material handlers. At the same time, large-scale infrastructure projects, which include the Belt and Road Project of China, National Infrastructure Pipeline of India, and NEOM of Saudi Arabia, present a large market opportunity for the manufacturers of autonomous equipment.

Recent Developments:

-

In 2024, Caterpillar expanded its autonomous haulage system to new mine sites, with the system surpassing one billion tonnes of material moved globally demonstrating exceptional operational reliability and commercial scale of autonomous heavy equipment deployment.

-

In 2024, Komatsu launched its next-generation autonomous dump truck with enhanced AI-based obstacle detection and route optimization capabilities, advancing fully autonomous haulage system performance for mining and large-scale construction applications.

-

In 2023, Doosan Bobcat launched RogueX at CONEXPO-CON/AGG, featuring an electric drivetrain and autonomous capabilities specifically designed for compact construction and mining site operations in challenging environments.

-

In 2023, Volvo CE introduced the ROCSYS autonomous charging solution for its electric construction equipment fleet, enabling 24/7 autonomous charging operations that enhance uptime and eliminate manual charging requirements for electric autonomous equipment.

Autonomous Construction Equipment Companies are:

-

Caterpillar Inc. (Autonomous Excavators, Loaders, Dozers)

-

Bobcat Company (Compact Track Loaders, Skid-Steer Loaders with Autonomous Features)

-

CNH Industrial America LLC (Autonomous Tractors, Excavators)

-

Komatsu Ltd. (Intelligent Machine Control Dozers, Autonomous Haulage Systems)

-

AB Volvo (Autonomous Haulers, Excavators)

-

Hitachi Construction Machinery Co., Ltd. (Excavators, Loaders with Aerial Imaging Technology)

-

Sany Group (Autonomous Cranes, Excavators)

-

Royal Truck & Equipment (Autonomous Truck-Mounted Attenuators)

-

TOPCON CORPORATION (Construction Automation Solutions, GNSS Systems)

-

Built Robotics (Autonomous Excavator Upgrades, Bulldozer Automation Kits)

-

Deere & Company (John Deere) (Autonomous Tractors, Graders)

-

Doosan Infracore (Smart Excavators, Loaders)

-

Trimble Inc. (Automation Control Systems, Software)

-

Leica Geosystems AG (Machine Control Systems, Autonomous Grading)

-

Hyundai Construction Equipment Co., Ltd. (Smart Excavators, Loaders)

-

Komatsu Mining Corp. (Autonomous Mining Trucks, Drills)

-

JCB (Compact Excavators, Loaders with Telematics)

-

Liebherr Group (Autonomous Mining Trucks, Excavators)

-

XCMG Group (Intelligent Excavators, Loaders)

-

Cognex Corporation (Vision Systems, Automation Tools for Construction)

| Report Attributes | Details |

|---|---|

|

Market Size in 2025 |

USD 15.11 billion |

|

Market Size by 2035 |

USD 35.73 billion |

|

CAGR |

CAGR of 8.99% From 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Autonomy (Semi-Autonomous, Fully Autonomous) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Caterpillar Inc., Bobcat Company, CNH Industrial America LLC, Komatsu Ltd., AB Volvo, Hitachi Construction Machinery Co., Ltd., Sany Group, Royal Truck & Equipment, TOPCON CORPORATION, Built Robotics, Deere & Company (John Deere), Doosan Infracore, Trimble Inc., Leica Geosystems AG, Hyundai Construction Equipment Co., Ltd., Komatsu Mining Corp., JCB, Liebherr Group, XCMG Group, Cognex Corporation. |

Frequently Asked Questions

North America is one of the largest markets in 2025, while Asia-Pacific is expected to register the fastest CAGR through 2035.

Ans: Semi-Autonomous equipment dominated with over 62% market share in 2025, while Fully Autonomous is the fastest-growing autonomy level through 2035.

Ans: Rising demand for efficiency, labor cost reduction, and productivity improvements drives adoption, as autonomous equipment automates tasks, reduces errors, and optimizes construction project resources.

Ans: The Market was valued at USD 15.11 Billion in 2025 and is projected to reach USD 35.73 Billion by 2035.

Ans: The Autonomous Construction Equipment Market is expected to grow at a CAGR of 8.99% during 2026–2035.

Get in Touch