Autonomous Driving Software Market Report Scope & Overview:

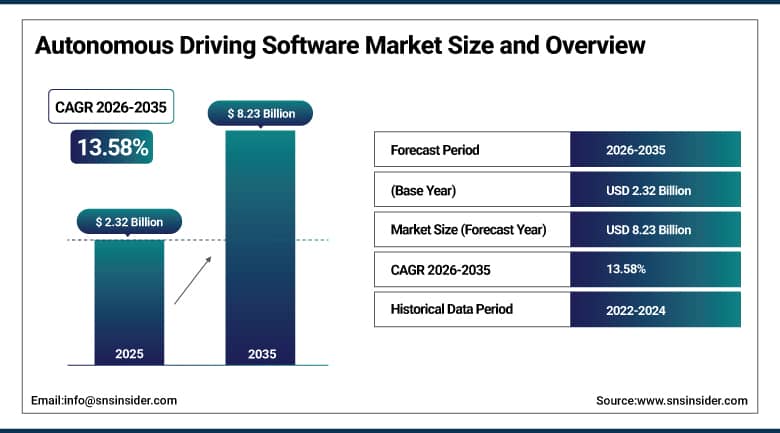

The Autonomous Driving Software Market was valued at USD 2.32 Billion in 2025 and is expected to reach USD 8.23 Billion by 2035, growing at a CAGR of 13.58% from 2026 to 2035.

The market of autonomous driving software is currently witnessing very fast and steady growth fueled by constantly progressing technologies in the fields of artificial intelligence, machine learning, and sensor fusion, allowing vehicles to perceive and navigate their surroundings with ever increasing degree of autonomy and accuracy. Autonomous driving software represents a wide range of algorithms, AI models, and control systems, which use sensor data from cameras, LiDAR, radar, and ultrasonic sensors to perform such functions as perception, localisation, path planning, decision making, and control for different levels of driving automation according to SAE standards ranging from Level 1 to Level 5. Factors such as regulatory requirements for ADAS, investments into software-defined vehicle architectures made by OEMs, and increasing robotaxi and autonomous logistics deployments drive the market.

In January 2025, Uber Technologies and NVIDIA have partnered in order to facilitate development of autonomous driving technologies powered by AI. Through this collaboration, the companies seek to improve autonomous vehicle performance by using the trip data collected by Uber along with NVIDIA's advanced solutions, such as Cosmos platform and DGX Cloud, in order to develop more effective AI models of vehicle perception, prediction, and planning.

Market Size and Forecast

-

Market Size in 2026E: USD 2.64 Billion

-

Market Size by 2035: USD 8.23 Billion

-

CAGR: 13.58% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Autonomous Driving Software Market - Request Free Sample Report

Autonomous Driving Software Market Trends

-

Software-defined vehicle architectures are accelerating autonomous driving software innovation through over-the-air updates, scalable platforms, and continuous feature enhancements.

-

Foundation AI models are improving perception accuracy and decision-making across diverse driving environments and complex traffic scenarios.

-

V2X communication integration is enhancing cooperative perception by enabling real-time data exchange between vehicles and surrounding infrastructure.

-

Simulation-based validation platforms are becoming the preferred approach for autonomous driving software testing, verification, and regulatory compliance.

-

Global regulatory harmonization is supporting faster commercialization of autonomous driving software through standardized approval frameworks and safety requirements.

U.S. Autonomous Driving Software Market Outlook

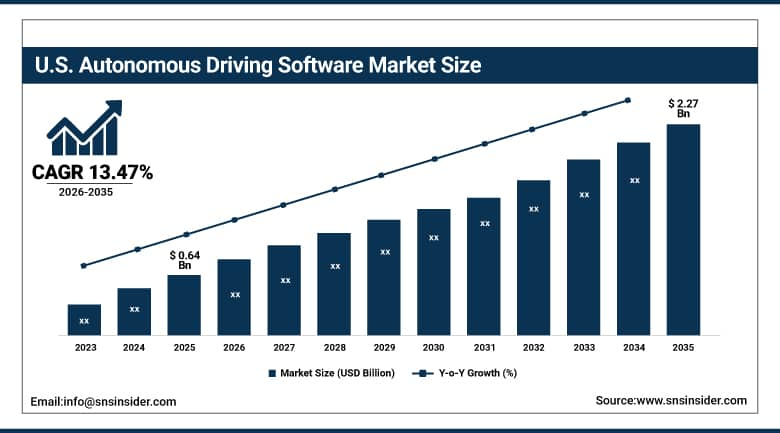

The U.S. Autonomous Driving Software Market was valued at approximately USD 0.64 Billion in 2025 and is expected to reach approximately USD 2.27 Billion by 2035, growing at a CAGR of approximately 13.47%.

The U.S. is the world's most commercially significant autonomous driving software market within North America's dominant regional position. Waymo, Aurora Innovation, Mobileye, NVIDIA, Qualcomm Technologies, Aptiv, and Motional collectively define the domestic autonomous driving software commercial landscape. The NHTSA's standing general order for autonomous vehicle incident reporting, FMCSA's autonomous commercial vehicle framework, and the state-level autonomous testing permit systems create a structured regulatory environment that sustains U.S. AV software development investment. Waymo's commercial robotaxi operations in San Francisco, Phoenix, Los Angeles, and Austin, and Aurora's commercial autonomous trucking launch on the Dallas to Houston corridor, create the most commercially advanced AV software deployment demonstrators globally.

In 2025, Alphabet-backed Waymo raised a USD 16 billion funding round to accelerate robotaxi deployment into over 20 cities worldwide. The investment boosts autonomous driving software development and commercialisation, underscoring continued investor confidence in AV software platforms and services and sustaining Waymo's position as the most commercially deployed Level 4 autonomous driving operation globally.

Autonomous Driving Software Market Segment Analysis

-

By Software Type, the perception & planning software segment dominated the autonomous driving software market with approximately 43% share in 2025, while the interior sensing software segment is the fastest growing.

-

By Propulsion Type, the ICE vehicles segment dominated the autonomous driving software market with approximately 64% share in 2025, while the electric vehicles segment is the fastest growing at approximately 14.65% CAGR.

-

By Level of Autonomy, the L2 segment dominated the autonomous driving software market with approximately 42% share in 2025, while the L4 & L5 segment is the fastest growing at approximately 15.55% CAGR.

-

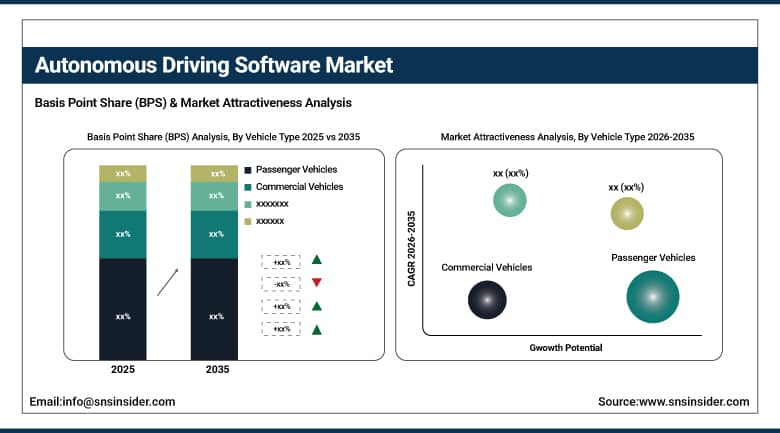

By Vehicle Type, the passenger vehicles segment dominated the autonomous driving software market with approximately 72% share in 2025, while the commercial vehicles segment is the fastest growing at approximately 14.78% CAGR.

By Vehicle Type, passenger vehicles dominate, commercial vehicles grow fastest

Passenger vehicles retained the dominant position with approximately 72% of the autonomous driving software market in 2025. The commercial primacy of passenger vehicle autonomous software reflects the extraordinary scale of global passenger car production, whose annual output of approximately 70 to 80 million units creates the largest aggregate ADAS and autonomous driving software procurement opportunity of any vehicle category. Consumer demand for advanced safety features, the competitive pressure among OEMs to offer the most technologically sophisticated driver assistance packages, and the progressive mandating of automatic emergency braking, lane departure warning, and adaptive cruise control across new vehicle type approvals sustain passenger vehicle autonomous software as the dominant revenue category.

Commercial vehicles are the fastest growing segment because autonomous trucking's commercial launch, logistics automation's last-mile delivery vehicle deployment, and mining and port autonomous vehicle operations create above-average autonomous software procurement from commercial fleet operators whose economic case for automation rests on labour cost reduction, fuel efficiency improvement, and operational productivity gains. Aurora's commercial autonomous trucking launch on the Dallas to Houston corridor in April 2024, whose revenue-generating truck deployments create the first commercial-scale autonomous trucking software procurement, demonstrates the structural commercial momentum that sustains commercial vehicle AV software's fastest-growing segment designation.

By Software Type, perception and planning dominates, interior sensing grows fastest

Perception and planning software retained the dominant position with approximately 43% of the autonomous driving software market in 2025. Its commercial primacy reflects the technical reality that environmental awareness and trajectory planning constitute the most computationally intensive, algorithmically complex, and safety-critical software functions in any autonomous driving system. Each autonomous vehicle above Level 1 requires perception software to process multi-sensor fusion data from cameras, LiDAR, and radar and planning software to generate safe, comfortable, and legally compliant trajectories from the perceived environment. The commercial scale of L2 ADAS deployment across tens of millions of annual global vehicle production creates massive perception and planning software procurement from suppliers including Mobileye, NVIDIA, Qualcomm, and Continental whose system-on-chip solutions embed the processing capability for perception and planning workloads.

Interior sensing software is the fastest growing segment because regulatory mandates for driver monitoring systems are creating compliance-driven procurement across new vehicle type approvals globally. Euro NCAP's 2026 safety rating requirements for driver monitoring system presence, the EU's General Safety Regulation mandating driver drowsiness and attention warning systems, and NHTSA's investigation of Level 2 ADAS attention monitoring collectively create structured first-time interior sensing software specification in vehicles that previously lacked any occupant monitoring capability. Each new vehicle model that adds a camera-based driver monitoring system to achieve regulatory compliance or Euro NCAP safety rating creates interior sensing software procurement whose commercial aggregate across global annual vehicle production sustains the segment's fastest growing designation.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Autonomous Driving Software Market Insights

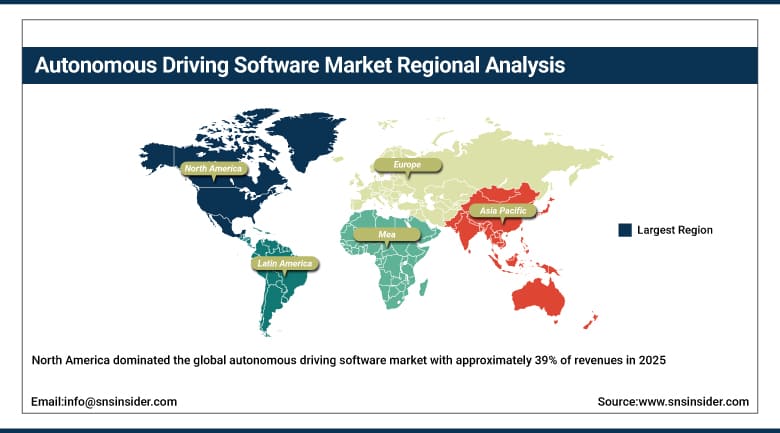

North America dominated the global autonomous driving software market with approximately 39% of revenues in 2025, underpinned by strong R&D investment, regulatory support for AV testing, and the commercial presence of Waymo, Aurora Innovation, Mobileye, NVIDIA, Qualcomm Technologies, and Aptiv whose combined autonomous driving software development and deployment activities define the global AV technology frontier. The United States accounts for approximately 87.4% of North American revenues through these commercial operations combined with GM Cruise, Ford Latitude AI, and the major automotive OEM ADAS procurement from Mobileye and Continental.

Canada contributes approximately 12.6% of North American revenues through Mobileye's Toronto research operations, the automotive manufacturing sector's ADAS content procurement, and the government's support for AV testing infrastructure across provincial demonstration corridors.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Autonomous Driving Software Market Insights

Europe is a technically sophisticated autonomous driving software market where the EU General Safety Regulation's mandatory ADAS requirements, Euro NCAP's 2026 advanced safety system rating criteria, and the automotive industry's deep engineering investment in autonomous technology create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through Continental's autonomous system portfolio, CARIAD's (Volkswagen) software development, BMW's personal pilot system, and Mercedes-Benz's DRIVE PILOT conditional automation deployment.

The United Kingdom, France, and the Netherlands are significant secondary markets where Arm Holdings’ processor architecture for automotive SoCs, Renault's autonomous technology partnership with Qualcomm, and the Netherlands’ automotive software ecosystem create consistent procurement. Aptiv's Dublin headquarters and Continental AG’s European operations sustain regional supply capability.

Asia Pacific Autonomous Driving Software Market Insights

Asia Pacific is the fastest growing regional autonomous driving software market, driven by China's extraordinary smart vehicle adoption, Japan's automotive OEM ADAS investment, South Korea's Samsung and Hyundai autonomous programmes, and India's rapidly expanding automotive market. China accounts for approximately 44.8% of Asia Pacific revenues through Baidu's Apollo autonomous driving platform, Huawei's HiCar and autonomous driving system, Pony.ai's robotaxi operations, and the Chinese government's Made in China 2025 initiative that prioritises smart transportation technology.

India represents the most commercially dynamic emerging market within Asia Pacific where the growing automotive production sector's ADAS content adoption, government road safety mandates creating automatic emergency braking specification, and the technology industry's autonomous system development investment create above-average autonomous driving software market growth from initial ADAS adoption levels.

MEA & Latin America Autonomous Driving Software Market Insights

The UAE leads MEA revenues at approximately 31.2% through Abu Dhabi's Department of Municipalities and Transport autonomous vehicle initiative, Dubai's smart mobility programme, and NEOM's autonomous transport infrastructure investment creating structured government-led AV software procurement. Saudi Arabia's Vision 2030 smart city development adds complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its automotive manufacturing sector's ADAS content adoption, the growing premium vehicle segment's advanced safety feature specification, and the technology sector's autonomous system development. Mexico's automotive industry and Colombia's smart mobility investment collectively sustain regional market growth through 2035.

Growth Drivers: Regulatory ADAS mandates and robotaxi commercial deployment creating structured software procurement

Government regulatory mandates for advanced driver assistance system integration in new vehicles represent the most commercially certain structural growth driver for the autonomous driving software market. The EU General Safety Regulation's requirement for autonomous emergency braking, lane departure warning, intelligent speed assistance, driver drowsiness and attention warning, and reversing detection systems in all new vehicle type approvals from 2022 creates non-discretionary ADAS software procurement across European automotive OEM production. NHTSA's investigation of existing L2 ADAS attention monitoring, Japan's SIP programme mandating intelligent transport system integration, and South Korea's Road Traffic Act revision requiring ADAS in new commercial vehicles collectively create a global regulatory framework that sustains structured autonomous driving software demand independent of consumer pull.

Robotaxi commercial deployment by Waymo, Baidu Apollo Go, and Aurora Innovation creates the most commercially visible L4 autonomous driving software revenue stream whose commercial scale is expected to grow substantially as deployment expands from initial demonstration cities to commercial-scale multi-city operations. Each Waymo vehicle operating commercially in a new city creates autonomous driving software procurement and licensing revenue whose aggregate across an expanding commercial fleet sustains above-average L4 segment growth through the forecast period.

Restraints: High development cost and regulatory liability uncertainty moderating deployment pace

The extraordinary software development investment required to achieve commercially deployable L3 and above autonomous driving capability creates financial barriers that limit the number of organisations capable of sustained autonomous driving software development. Each novel autonomous driving software version that requires simulation validation across billions of test scenarios, physical road testing across diverse real-world conditions, and regulatory approval submission creates development cost investment whose scale restricts autonomous driving software innovation to a relatively small number of well-capitalised automotive OEMs and technology companies.

Regulatory liability uncertainty for autonomous vehicle incidents creates commercial caution that moderates the pace of L3 and above autonomous driving software deployment. Each legal and regulatory question about liability allocation between software developer, OEM, and vehicle operator in an autonomous vehicle incident creates deployment risk that sustains conservative geographic rollout strategies from AV software developers whose commercial launch decisions are conditioned on favourable liability frameworks.

Opportunities: Autonomous logistics and SDV architecture creating software monetisation platforms

Autonomous logistics represents the most commercially certain near-term L4 autonomous driving software revenue opportunity whose economic case for automation rests on measurable trucking labour cost reduction and fuel efficiency improvement that creates commercially viable business models independent of consumer preference. Aurora's commercial autonomous trucking, Waymo Via's logistics programme, and Kodiak Robotics’ autonomous trucking operations demonstrate the commercial validation of L4 logistics autonomous software whose revenue models include per-mile licensing, fleet management fees, and operational service contracts.

Software defined vehicle architecture adoption by major OEMs creates a platform monetisation opportunity for autonomous driving software beyond the initial vehicle sale through over-the-air feature activation, subscription-based capability upgrade, and usage-based software licensing. Each vehicle sold with latent autonomous driving hardware capable of software-enabled capability upgrade creates a recurring revenue opportunity for autonomous driving software developers whose OTA monetisation model compounds with fleet scale growth.

Recent Developments:

-

2025: Uber Technologies and NVIDIA announced a strategic partnership in January 2025 to advance AI-powered autonomous driving technologies, integrating Uber's trip data with NVIDIA's Cosmos platform and DGX Cloud to create more efficient AI models for AV perception and planning.

-

2025: Alphabet-backed Waymo raised a USD 16 billion funding round in 2025 to accelerate robotaxi deployment into over 20 cities worldwide, representing the largest single autonomous driving software commercialisation investment in market history.

-

2025: Toyota deployed its Arene software development platform in the latest RAV4 model in 2025, marking a concrete step toward software defined vehicle adoption by a major OEM and demonstrating how autonomous driving software platforms are being embedded deeply into vehicle electronics and user interfaces.

Autonomous Driving Software Market Key Players:

-

Waymo LLC (Alphabet Inc.)

-

Mobileye Global Inc. (Intel)

-

Qualcomm Technologies Inc.

-

Aurora Innovation Inc.

-

Aptiv PLC

-

Continental AG

-

Robert Bosch GmbH

-

Baidu Inc. (Apollo)

-

Pony.ai Inc.

-

Huawei Technologies Co. Ltd.

-

Valeo SA

-

Motional (Hyundai and Aptiv JV)

-

CARIAD SE (Volkswagen Group)

-

Kodiak Robotics Inc.

-

Argo AI (Ford and VW)

-

PlusAI Inc.

-

Zoox Inc. (Amazon)

-

OXA Autonomy Ltd.

Autonomous Driving Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.32 Billion |

| Market Size by 2035 | USD 8.23 Billion |

| CAGR | CAGR of 13.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Software Type (Perception & Planning Software, Mapping & Localization Software, Data Analytics Software, Interior Sensing Software, Others) • By Propulsion Type (ICE Vehicles, Electric Vehicles) • By Vehicle Type (Passenger Vehicles, Commercial Vehicles) • By Level of Autonomy (L1, L2, L3, L4 & L5) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Waymo LLC (Alphabet Inc.), NVIDIA Corporation, Mobileye Global Inc. (Intel), Qualcomm Technologies Inc., Aurora Innovation Inc., Aptiv PLC, Continental AG, Robert Bosch GmbH, Baidu Inc. (Apollo), Pony.ai Inc., Huawei Technologies Co. Ltd., Valeo SA, Denso Corporation, Motional (Hyundai and Aptiv JV), CARIAD SE (Volkswagen Group), Kodiak Robotics Inc., Argo AI (Ford and VW), PlusAI Inc., Zoox Inc. (Amazon), and OXA Autonomy Ltd. |

Frequently Asked Questions

North America dominated the Autonomous Driving Software Market with approximately 39% of revenues in 2025.

Perception and Planning Software dominated with approximately 43% share in 2025.

The Autonomous Driving Software Market is expected to grow at a CAGR of 13.58% from 2026 to 2035.

The Autonomous Driving Software Market was valued at USD 2.32 Billion in 2025.

Government regulatory mandates for ADAS integration in new vehicles creating non-discretionary autonomous driving software procurement, and robotaxi commercial deployment by Waymo, Baidu Apollo Go, and Aurora Innovation creating structured L4 autonomous software revenue streams that demonstrate commercial viability.

Get in Touch