Beer Market Report Scope & Overview:

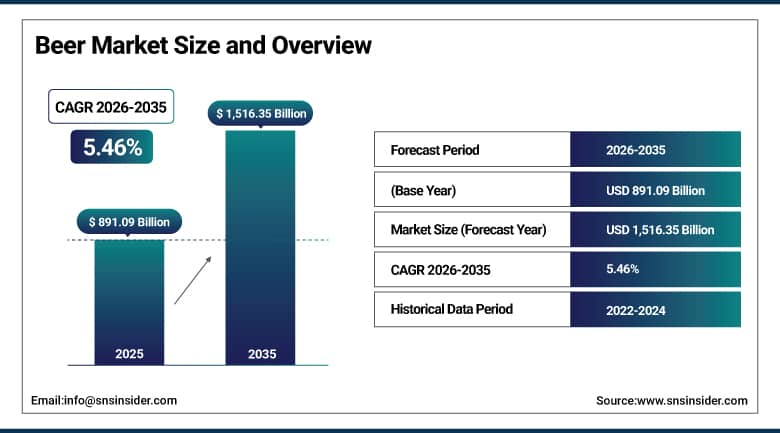

The Beer Market was valued at USD 891.09 billion in 2025 and is expected to reach USD 1,516.35 billion by 2035, growing at a CAGR of 5.46% from 2026–2035.

The most consumed alcoholic drink in the world is beer and it ranks third on the list of beverages behind water and tea. This beverage is manufactured through fermentation of malted barley, water, hops, and yeast with a process that has been perfected over thousands of years of brewing experience. In 2025, 195 million hectoliters of beer had been produced around the world thanks to increasing consumption of craft and premium types. Bar consumption, restaurant consumption, retail sales, and online sales are all increasing simultaneously. There is ongoing premiumization in this market with consumers upgrading from regular lagers to craft, specialty, and premium types. There is increased demand for non-alcoholic and low alcohol types of beer as health-conscious consumers who previously abstained are now consuming this beverage category. Beer drinks with added flavors are expanding the demographic range of people who consume beer in such forms like fruit beer, sour ales, and botanically flavored types. Urbanization and increase in disposable income in emerging markets are increasing the number of consumers for this product.

In 2025, 195 million hectoliters of beer were produced as a result of increased demand for craft and premium types.

Market Size and Forecast

- Market Size in 2026E: USD 939.77 Billion

- Market Size by 2035: USD 1516.35 Billion

- CAGR: 5.46% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: Europe

To Get More Information On Beer Market - Request Free Sample Report

Beer Market Trends

- Non-alcoholic and low-alcohol beer is the fastest-growing format globally. Over 68% of consumers cite health as the primary reason for choosing alcohol-free beer alternatives.

- Craft beer premiumization continues to reshape consumer preferences in developed markets. Independent breweries are expanding distribution through regional supermarket listings and direct e-commerce channels.

- Can packaging is taking share from bottles across multiple geographies. Cans offer superior light protection, lower weight, and stronger alignment with outdoor and active lifestyle consumption occasions.

- E-commerce and direct-to-consumer beer subscriptions are growing rapidly. Specialist online retailers and brewery subscription clubs are capturing share from traditional off-trade distribution channels.

- Sustainability packaging and carbon-neutral brewing commitments are becoming brand differentiators. Major brewers are publishing verified emissions reduction roadmaps and introducing lightweight and recycled packaging.

The U.S. Beer Market Outlook

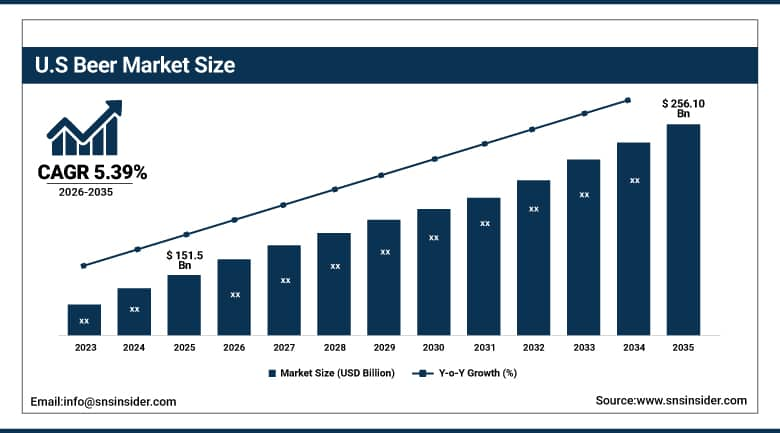

The U.S. Beer Market was valued at approximately USD 151.5 billion in 2025 and is expected to reach approximately USD 256.10 billion by 2035, growing at a CAGR of 5.39%.

The U.S. is a highly developed market commercially. The country led the trend of the modern craft beer revolution which changed the global consumer preference for brewing products starting from the 1980s. More than 9,500 craft beer breweries work in the U.S. in 2025. There is the largest number of breweries of this type in one country in the world at the moment. Domestic premium craft beer brands like Sierra Nevada, Stone Brewing, and New Belgium have good distribution and high popularity among consumers. Zero-alcohol beer becomes the fastest-growing segment in the U.S., which includes such brands as Heineken 0.0, Athletic Brewing, and Guinness 0.0. Leading multinationals like Anheuser-Busch InBev and Molson Coors create innovations in terms of premiums and beyond-beer products due to lower standard lager volumes. Such beverages as hard seltzers, craft ready-to-drink cocktails, and flavored malt beverages pose a direct competition for beer products by occupying the same consumption moment. Different three-tier systems work in various states in the U.S. Direct-to-consumer selling of craft beer became crucial for small and medium-sized brewers.

More than 9,500 craft beer breweries operate in the U.S. in 2025. The craft segment experiences above-average revenue per litre growth.

Beer Market Segment Analysis

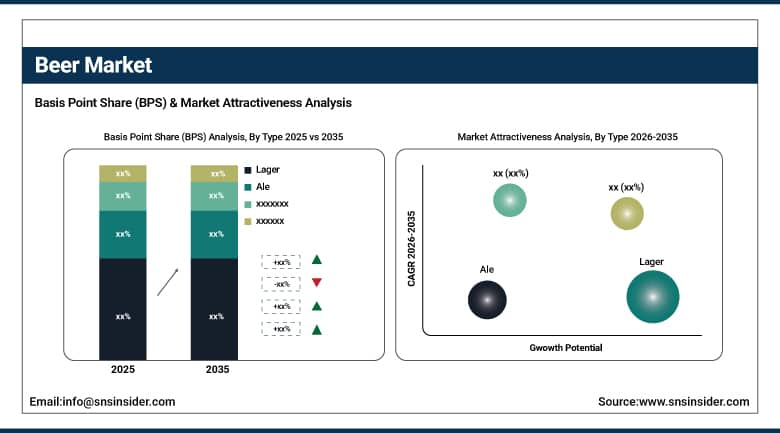

- By Type, lager dominated with a 41.82% share in 2025 through its global consumer recognition, broad demographic appeal, and universal availability across retail and on-trade channels. Ale is the fastest-growing type at a CAGR of 6.28% driven by craft beer expansion, IPA popularity, and growing consumer interest in flavor-forward beer styles.

- By Packaging, bottle dominated with a 46.37% share in 2025 through its established premium brand association and traditional on-trade presence. Can is the fastest-growing packaging at a CAGR of 5.83% through superior portability, outdoor occasion suitability, and growing craft producer adoption.

- By Production, industrial accounted for 55.46% share in 2025 through mass-scale brewing efficiency, global distribution reach, and mainstream lager brand volumes. Craft is the fastest-growing through premiumization, local provenance appeal, and flavor innovation that commands above-average price points.

- By Distribution Channel, on-trade channels serve pubs, bars, and restaurants providing the social and experiential consumption contexts that sustain premium beer value. Off-trade supermarkets and convenience stores are growing through packaged beer at-home consumption; Online is the fastest-growing channel through subscription boxes, direct brewery sales, and e-commerce platform availability.

By Type, lager dominates, ale is expected to grow fastest

Lager held its market share leadership with around 41.82% of the beer market in 2025. Its taste profile of being crisp and clean is a universal one that appeals to consumers regardless of their demographic and geographical profiles. Standard and premium lager categories of beers such as Heineken, Budweiser, Corona, Stella Artois, and Carlsberg are among the largest global distributors. Due to its cold fermentation technique and consistent flavor consistency, it remains the most scalable type of beer to produce industrially in large volumes. Premium lagers are witnessing strong demand growth as consumers switch from standard domestic lagers to imports and premium craft lager types. The innovation in lager type by adding flavors such as citrus and fruit elements into the brew has helped expand its consumer base.

Ale remains the fastest growing style segment at a CAGR of 6.28% up until 2035. The growth of craft beer around the world has increased consumer awareness about the different styles of ale ranging from the American IPA to the Belgian saison, British bitter, and German wheat beer. India Pale Ales have gained consumer recognition outside craft beer enthusiasts by investing in supermarket shelving along with multipacks aimed at consumers to drink at home. Sour ales or mixed fermentation beers continue to gain consumer interest among affluent consumers due to their complexity, scarcity, and high prices which place them in the same category as craft spirits for premium occasions. The New England IPA style has seen remarkable success in America and is gaining traction globally.

By Packaging, bottle dominates, can is expected to grow fastest

Bottles retained the dominant packaging position with approximately 46.37% of the beer market in 2025. Glass bottle packaging maintains a premium aesthetic association in both on-trade and off-trade contexts that supports higher price point positioning for premium and specialty beer brands. European beer culture retains a particularly strong preference for bottled beer in both returnable deposit systems used in Germany, Denmark, and the Netherlands, and single-trip glass formats across Southern European markets. Craft breweries historically preferred bottle packaging for its design canvas flexibility and premium brand communication before the craft can movement fundamentally shifted packaging preferences in the North American and Australian craft sectors.

Can packaging is the fastest-growing format at a CAGR of 5.83% through 2035. Cans provide superior light protection that prevents the UV-induced skunking that is a persistent quality defect vulnerability for beer in clear and green glass bottles. The portability advantage of cans in outdoor, sports, and festival consumption occasions aligns perfectly with the active lifestyle and outdoor recreation contexts that beer brands are targeting through sponsorship and marketing investment. Craft brewery adoption of canning has accelerated since smaller-scale canning line technology became commercially accessible, enabling independent breweries to package their most commercially successful beers in the consumer-preferred format for grocery retail placement where can multipack shelf presence drives mainstream consumer trial.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.4% |

|

Europe |

Germany |

22.7% |

|

Asia Pacific |

China |

49.6% |

|

Middle East & Africa |

South Africa |

28.4% |

|

Latin America |

Brazil |

44.8% |

Europe Beer Market Insights

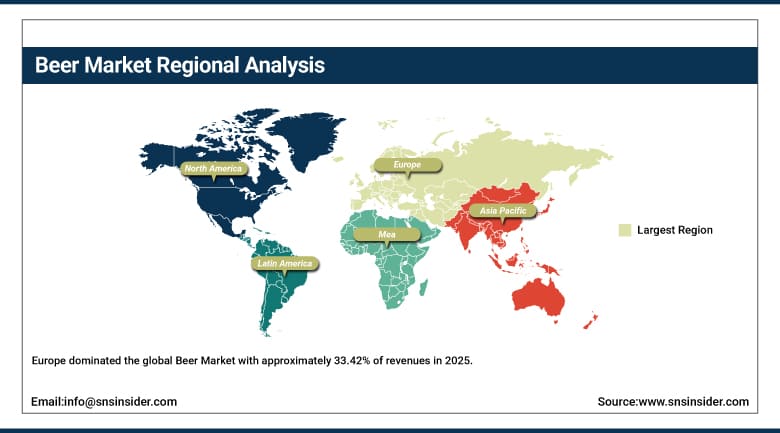

Europe dominated the global Beer Market with approximately 33.42% of revenues in 2025. Germany accounts for approximately 22.7% of European revenues through its extraordinarily rich brewing tradition, Reinheitsgebot quality heritage, and beer consumption embedded across all social contexts. The UK maintains one of the world's most distinctive beer cultures through its cask ale tradition, thriving craft scene, and pub consumption that provides the highest premium pricing context of any distribution channel. Belgium's artisanal ale heritage produces globally prestigious exports including Trappist and Belgian strong ale categories commanding the highest price per litre of any mainstream beer type. European premium lager exports from Germany, the Netherlands, Czech Republic, and Denmark sustain strong global brand recognition for the region's beer sector.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Beer Market Insights

North America is a large and commercially dynamic beer market. The U.S. accounts for approximately 83.4% of North American revenues. The American craft beer revolution has been the most commercially influential beer market development of the past four decades globally. Non-alcoholic beer is the fastest-growing U.S. segment, reflecting the health-conscious consumer shift that is reshaping category dynamics. Mexico is the world's largest beer exporter and a major regional market through its powerful Corona, Modelo, and Tecate brands. Premium imported Mexican beer consumption in the U.S. is sustaining high per-litre value growth within the overall volume-flat American beer market. E-commerce and direct brewery sales are creating new distribution channels that bypass traditional three-tier regulatory frameworks where permissible.

Asia Pacific Beer Market Insights

Asia Pacific has the highest CAGR of beer consumption at 7.29% to 2035. China makes up about 49.6% of Asia Pacific revenues being the largest single country beer market in terms of volumes in the world. Chinese local beer brands like Snow, Tsingtao, and Yanjing lead in terms of volume sales while global premium beer brands like Heineken and Budweiser are increasing thanks to premiumization within urban areas. The Indian beer market is among the fastest growing in the world as a result of rapid urbanization, rising disposable income in the middle class, and liberalization of regulations within important states. Japan maintains advanced premium and craft beer consumption despite demographic challenges due to its declining population.

MEA & Latin America Beer Market Insights

Middle East and Africa and Latin America are emerging markets for beer that have their own dynamics within each region. South Africa is the market leader in MEA at about 28.4% due to its mature beer market along with the domestic dominance of SABMiller previously now being taken over by AB InBev brands. The sub-Saharan African countries are witnessing growth due to urbanization, youth population trends, and increased mainstream lager penetration. Nigeria and Ethiopia are two of the commercially active African countries for beer market development. Brazil is the market leader in Latin America at about 44.8% due to it being one of the biggest national beer markets in the world. The beers Cerveja Brahma, Antarctica, and Skol lead through the AB InBev AmBev operation in Brazil.

Market Dynamics

Growth Drivers: Premiumization, craft beer expansion, non-alcoholic segment growth, and rising disposable incomes in developing markets are driving global beer market growth.

The trend towards consumer premiumization ensures continued rapid gains in beer revenues due to spending shifting from normal and to premium and craft beers. Craft beers have changed forever consumer expectation of beer taste and their willingness to pay premium prices for superior beers. The development of non-alcoholic beers will now allow healthy and previously abstaining consumers to try beer for the first time. In addition, increased disposable income in Africa, Asia, and Latin America makes beer category entry possible for many consumers in developing countries. Increased access to premium and craft beers via online sales in markets lacking specialty beer off-trade infrastructure is also an ongoing development. Beer's strong socio-cultural integration into the lives of global consumers makes beer demand highly sustainable.

Restraints: Health consciousness reducing alcohol consumption, regulatory restrictions, and intense competition from hard seltzers and RTD cocktails are restraining beer market volume growth.

Consumers' health awareness is encouraging consumers to reduce the consumption of alcohol both in terms of frequency and volume in important demographics in mature economies. Novel alcoholic drinks like hard seltzers, canned cocktails, and ready-to-drink alcoholic beverages based on spirits are increasingly becoming alternatives to beer and competing with it for the same consumption during social occasions. Government regulations in different economies, limiting marketing practices of alcoholic beverages and adopting minimum unit pricing, limit consumer contact and purchases. Beer prices are increasing due to higher excise duties, thus impacting price-sensitive consumer segments regarding volume consumed. There is cost instability in the input costs for barley, hops, aluminum, and glass materials.

Opportunities: Non-alcoholic beer innovation, functional beer formats, and e-commerce direct-to-consumer growth create substantial beer market expansion opportunities globally.

The technology for non-alcoholic beer has made significant advancements and offers the taste of the drink without having any taste issues associated with the process of dealcoholizing. This development has resulted in converting the earlier skeptic mainstream consumers into habitual drinkers of non-alcoholic beers. Health functional beers are being produced using vitamins, probiotics, adaptogens, and electrolytes to produce beverages aimed at health-conscious consumers. Direct sales of craft beer through the channel of subscriptions and online marketing help craft breweries to have an effective relationship with consumers on a nationwide basis which is not economical through conventional means of distribution. The emerging markets of Africa and south and southeast Asia offer new areas for premium beer consumption.

Recent Developments:

- 2025: Anheuser-Busch InBev expanded its global non-alcoholic portfolio with new Budweiser Zero and Corona Cero variants in additional markets. The company reported non-alcoholic segment volume growth exceeding 15% globally in 2025.

- 2025: Heineken N.V. accelerated investment in its EverGreen sustainability strategy, committing to 100% renewable electricity across brewing operations by 2030. The company launched its first carbon-neutral certified beer in select European markets.

- 2025: Carlsberg Group launched its Snap Pack plastic-free multipack technology across additional markets, eliminating plastic rings from its six-pack and multipack formats. The technology has removed over 1,200 tonnes of single-use plastic from European markets annually.

Beer Market Key Players are:

- Anheuser-Busch InBev SA

- Heineken N.V.

- Carlsberg A/S

- Molson Coors Beverage Company

- Asahi Group Holdings Ltd.

- Kirin Holdings Company Ltd.

- Constellation Brands Inc.

- Grupo Modelo

- FEMSA Cerveza

- Beijing Yanjing Brewery Co. Ltd.

- China Resources Beer Holdings Co. Ltd.

- Tsingtao Brewery Co. Ltd.

- SABMiller plc

- Diageo plc

- Boston Beer Company

- Sierra Nevada Brewing Co.

- Athletic Brewing Company

- New Belgium Brewing Company

- Stone Brewing Co.

- Duvel Moortgat NV

Beer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 891.09 Billion |

| Market Size by 2035 | USD 1,516.35 Billion |

| CAGR | CAGR of 5.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Lager, Ale, Stout & Porter, Specialty Beer, Others) •By Packaging (Bottle, Can, Draft/Keg, Others) •By Production (Industrial, Craft) •By Distribution Channel (On-Trade, Off-Trade, Online) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Anheuser-Busch InBev SA, Heineken N.V., Carlsberg A/S, Molson Coors Beverage Company, Asahi Group Holdings Ltd., Kirin Holdings Company Ltd., Constellation Brands Inc., Grupo Modelo, FEMSA Cerveza, Beijing Yanjing Brewery Co. Ltd., China Resources Beer Holdings Co. Ltd., Tsingtao Brewery Co. Ltd., SABMiller plc, Diageo plc, Boston Beer Company, Sierra Nevada Brewing Co., Athletic Brewing Company, New Belgium Brewing Company, Stone Brewing Co., and Duvel Moortgat NV. |

Frequently Asked Questions

Get in Touch