Bio-based Platform Chemicals Market Report Scope & Overview:

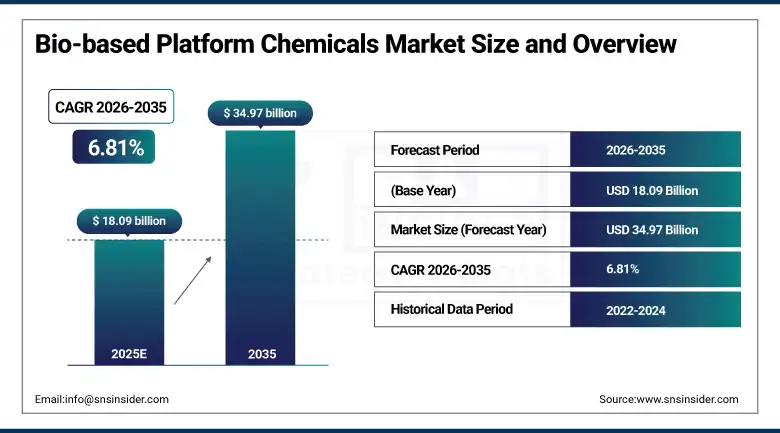

Bio-based Platform Chemicals Market was valued at USD 18.09 billion in 2025 and is expected to reach USD 34.97 billion by 2035, growing at a CAGR of 6.81% from 2026–2035.

The global bio-based platform chemicals market represents one of the most strategically important sectors in the transition from a petroleum-dependent linear chemical economy toward a circular, renewable bio-economy that produces chemicals, materials, and fuels from biological feedstocks including sugars, lignocellulosic biomass, vegetable oils, and agricultural residues.

Market Size and Forecast

-

Market Size in 2025: USD 18.09 Billion

-

Market Size by 2035: USD 34.97 Billion

-

CAGR: 6.81% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Bio-based Platform Chemicals Market - Request Free Sample Report

Bio-based Platform Chemicals Market Trends

-

Rapid commercial scale-up of bio-succinic acid production by BASF and Corbion through large-scale fermentation facilities, enabling bio-succinic acid to compete on cost with petroleum-derived succinic acid in polyurethane, resin, and pharmaceutical applications at commercially significant production volumes.

-

Growing investment in lignocellulosic biomass biorefinery technology that extracts multiple platform chemical streams including sugars, lignin, and organic acids from agricultural residues and forestry waste, improving biorefinery economics through multi-product output models that maximise feedstock value utilisation.

-

Accelerating demand for lactic acid and polylactic acid bioplastics driven by single-use plastic regulations across Europe, the U.S., and Asia Pacific that are compelling packaging manufacturers to adopt compostable bioplastic alternatives that lactic acid fermentation enables at competitive cost.

-

Rising government R&D funding for bio-based platform chemical development through programmes including the U.S. DOE's Bioenergy Technologies Office, EU Horizon Europe bio-economy research investments, and national biorefinery development programmes across Brazil, India, and China.

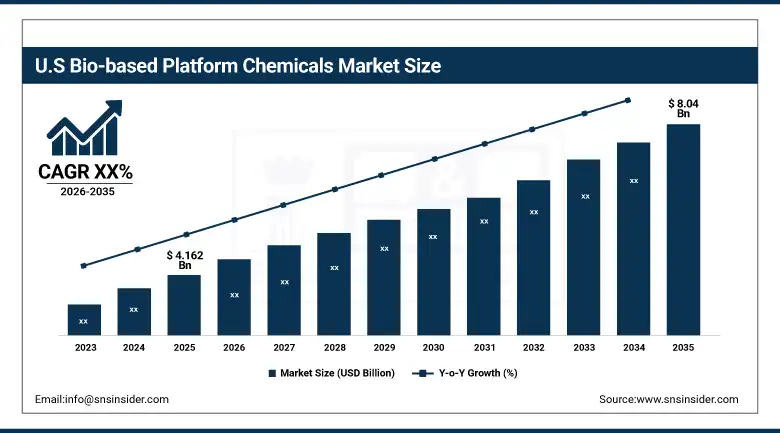

U.S. Bio-based Platform Chemicals Market was valued at approximately USD 4.162 billion in 2025 and is expected to reach approximately USD 8.04 billion by 2035, supported by DOE bioenergy investment, growing bioplastics demand, and strong domestic biotechnology innovation.

The United States represents one of the world's most strategically significant bio-based platform chemicals markets, supported by the DOE's Bioenergy Technologies Office providing substantial R&D funding for advanced fermentation and biorefinery technology, a world-class industrial biotechnology research base encompassing MIT, Berkeley, and dozens of national laboratory and private research centres, and a large domestic agricultural sector that provides abundant renewable biomass feedstocks at globally competitive prices.

Bio-based Platform Chemicals Market Segment Insights

-

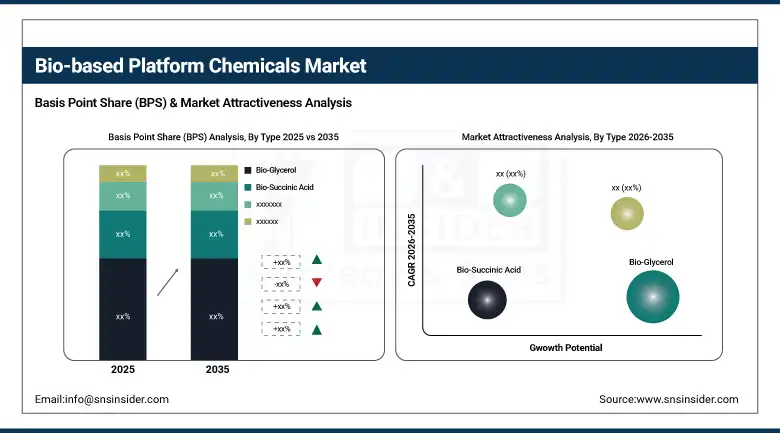

According to Type, Glycerol dominated the market in 2025 as the most commercially mature and widely deployed bio-based platform chemical across pharmaceuticals, personal care, and food applications; Bio-Succinic Acid and Lactic Acid are among the fastest-growing chemical types driven by bioplastics demand and commercial scale-up investment.

-

In terms of Feedstock, Sugars and Starch dominated in 2025 as the most established and commercially optimised fermentation feedstock for bio-based platform chemical production; Lignocellulosic Biomass is the fastest-growing feedstock as second-generation biorefinery technology matures toward commercial viability.

-

By Application, Polymers and Bioplastics dominated the market in 2025 as the largest single application category for bio-based platform chemicals; Pharmaceuticals and Nutraceuticals and Personal Care and Cosmetics are among the fastest-growing applications driven by premium sustainability positioning.

Bio-based Platform Chemicals Market Segment Analysis

By Type: Glycerol dominates, Bio-Succinic Acid and Lactic Acid grow fastest

The Bio-Glycerol product category retained its position as the leading Bio-based Platform Chemicals type during the forecast period (2025), due to its high commercial readiness, being a coproduct of biodiesel manufacturing process, and wide range of uses in the pharmaceutical industry as a solvent and excipient, in personal care as a humectant and skin conditioner, in food & beverage as a sweetener and preservative, and in industrial sector as a plasticizer and chemical intermediate.

Bio-Succinic Acid and Lactic Acid were identified as the fastest-growing bio-based platform chemicals types from 2018 to 2035, owing to their important position within the value chain of bioplastics production, and large investments for scale-up production by BASF, Corbion, Nature Works, and Evonik, which is helping reduce the price per kg of these chemicals to become comparable to those produced from petrochemicals. Lactic acid's dominance as the raw material for polylactic acid bioplastics makes it one of the most important bio-based platform chemicals, due to rapid growth in demand for PLA as restrictions imposed by regulations in Europe and Asia Pacific on petroleum-based single-use plastics increase demand for compostable bioplastics.

By Feedstock: Sugars and Starch dominate, Lignocellulosic Biomass grows fastest

Sugars and Starch retained the dominant feedstock position in 2025, reflecting the commercial maturity and well-optimised fermentation processes that convert glucose, sucrose, and starch-derived sugars into bio-based platform chemicals through established industrial microbiology at commercially viable yields and production costs. Sugar-based fermentation is the most commercially proven bio-based platform chemical production pathway, with extensive installed global capacity for glucose and sucrose fermentation producing lactic acid, succinic acid, glutamic acid, and other platform chemicals at industrial scale.

Lignocellulosic Biomass is the fastest-growing feedstock for bio-based platform chemicals through 2035, driven by the progressive commercial maturation of second-generation biorefinery technology that can cost-effectively convert agricultural residues, forestry waste, and energy crops into fermentable sugars without competing with food crop cultivation. Lignocellulosic feedstocks including wheat straw, corn stover, sugarcane bagasse, and wood residues are abundant, geographically widespread, and available at very low cost relative to food-grade sugar feedstocks, providing the economic foundation for dramatically lower-cost bio-based platform chemical production when efficient conversion technology reaches commercial scale.

By Application: Polymers and Bioplastics dominate, Pharmaceuticals and Personal Care grow fastest

Polymers and Bioplastics led the Bio-based Platform Chemicals Application segment in 2025 to emerge as the biggest end-use application segment, thanks to the huge market potential being created by the regulatory pressure on oil-based plastics to drive up production capacity investments in bio-based polymers such as lactic acid, succinic acid, and itaconic acid that can be used to produce environmentally friendly bioplastics. Regulatory measures such as the Single-Use Plastics Directive in the European Union, the California SB 54 plastic ban, and other similar laws in Asia Pacific are creating huge demand for bioplastics out of compliance considerations.

Pharmaceuticals and Nutraceuticals and Personal Care and Cosmetics are some of the rapidly growing application segments over the period up to 2035, fueled by the premium sustainability positioning offered by bio-based material usage in these high-growth and high-margin business sectors.

Bio-based Platform Chemicals Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

72% |

|

Europe |

Germany |

32% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

South Africa |

28% |

|

Latin America |

Brazil |

55% |

Europe Bio-based Platform Chemicals Market Insights

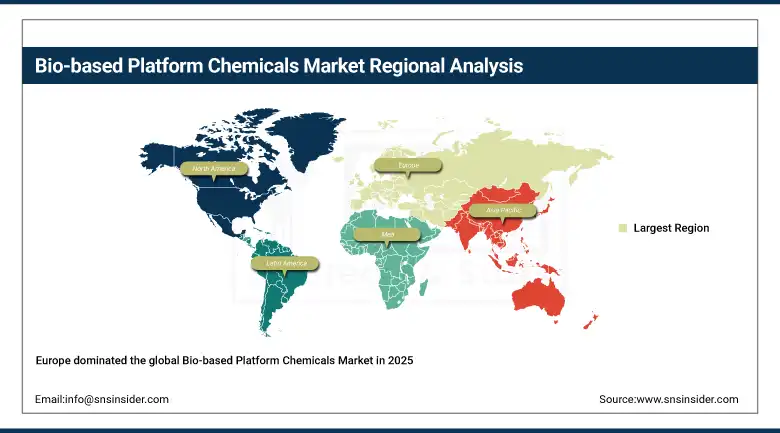

Europe dominated the global Bio-based Platform Chemicals Market in 2025, driven by the world's most comprehensive sustainability regulatory framework including the EU Chemical Strategy for Sustainability, the European Green Deal, and the EU Bioeconomy Strategy that collectively create the strongest regulatory pull for bio-based chemical adoption. The EU's prohibition of specific high-concern petroleum-derived chemicals and progressive restriction of others under REACH is creating systematic demand for bio-based replacement chemistries across multiple chemical market segments. Germany, France, the Netherlands, and the UK are the leading European bio-based platform chemical consumers, each supported by strong domestic biotechnology and chemical industries investing in bio-based transition.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Bio-based Platform Chemicals Market Insights

Asia Pacific is the fastest-growing regional bio-based platform chemicals market, driven by abundant and diverse biomass feedstock resources including agricultural residues from rice, wheat, and sugarcane across China, India, Thailand, and Indonesia, rapidly expanding bioplastics manufacturing capacity driven by domestic single-use plastics regulations, and growing government investment in biorefinery development as part of national bioeconomy and circular economy strategy programmes. China leads Asian bio-based platform chemical production through its world-class fermentation industry producing lactic acid, amino acids, and organic acids at global scale, while India's rapidly growing bioplastics market is creating expanding domestic demand for lactic acid and succinic acid bio-based feedstocks.

North America Bio-based Platform Chemicals Market Insights

North America represents a significant bio-based platform chemicals market anchored by the United States, with approximately 72% of North American revenues driven by DOE bioenergy investment, world-class industrial biotechnology innovation, and growing domestic bioplastics demand. Brazil, as the world's leading sugarcane ethanol producer, plays a dual role as both a major South American bio-based platform chemical consumer and a globally significant biochemical feedstock supplier. Canada contributes through its extensive forestry biomass resources and growing biorefinery investment in lignocellulosic feedstock conversion technologies.

Latin America and MEA Bio-based Platform Chemicals Market Insights

Latin America is a unique and strategically important bio-based platform chemicals market where Brazil dominates at approximately 55% of regional revenues through its world-leading sugarcane biorefinery industry, major lactic acid and succinic acid fermentation operations, and Braskem's green polyethylene production from sugarcane ethanol that has established Brazil as a global leader in commercially proven large-scale bio-based chemical manufacturing. MEA participation is growing through South African biorefinery development and Middle Eastern investment in non-oil revenue diversification through biotechnology.

Market Growth Drivers:

Sustainability regulations restricting petroleum-derived chemicals and corporate net-zero supply chain commitments creating structural commercial demand shift toward bio-based alternatives: The primary structural growth drivers for the Bio-based Platform Chemicals Market are the escalating global sustainability regulatory framework that is progressively restricting petroleum-derived chemicals across consumer products, packaging, and industrial applications while creating regulatory pull for bio-based alternatives, combined with the extraordinary breadth and depth of corporate sustainability commitments among the world's largest consumer goods companies, retailers, and manufacturers that are mandating bio-based ingredient sourcing through their supply chains. The EU Chemical Strategy for Sustainability's essential use restrictions, the REACH regulatory process identifying high-concern synthetic chemicals, and single-use plastics legislation collectively create a regulatory architecture that systematically expands the commercial opportunity for bio-based platform chemicals across multiple chemical market segments simultaneously.

Market Restraints

Higher production costs relative to petroleum-derived equivalents, feedstock price volatility, and scale-up challenges for emerging bio-based platform chemical types constraining market growth velocity: A significant restraint on the Bio-based Platform Chemicals Market is the persistent cost premium of most bio-based platform chemicals relative to their petroleum-derived equivalents at current production scale, driven by lower fermentation yields in some chemical categories, complex downstream purification requirements, and the capital intensity of biorefinery infrastructure relative to established petrochemical production assets. Agricultural feedstock price volatility, particularly for food-grade sugars and starches that compete with food production uses, creates raw material cost uncertainty that challenges bio-based platform chemical producer profitability during periods of high agricultural commodity prices. The scale-up of emerging bio-based platform chemical types from laboratory and pilot scale to commercial production volumes requires multi-year capital investment programmes that create financing risk particularly for novel chemical types without established commercial markets that provide revenue certainty during the investment period.

Market Opportunities

Lignocellulosic biorefinery commercialisation, synthetic biology-enabled yield improvement, and premium brand bio-based ingredient sourcing: The commercial maturation of lignocellulosic biorefinery technology, enabling cost-effective conversion of abundant agricultural and forestry residues into fermentable sugars without food crop competition, represents the single most transformative cost reduction opportunity in the bio-based platform chemicals market, with the potential to reduce feedstock costs below those of current sugar-based routes through use of low-cost, non-food residue feedstocks available at negative or minimal raw material cost. Synthetic biology tools including CRISPR-engineered fermentation organisms that produce target platform chemicals with dramatically higher yield, selectivity, and productivity than conventional fermentation strains are progressively improving bio-based platform chemical production economics across all chemical types. Premium brand sustainability positioning, where bio-based ingredient sourcing in cosmetics, pharmaceuticals, and food products commands consumer price premiums of 10 to 30% that more than offset production cost differences versus petroleum alternatives, represents a commercial value capture mechanism that makes bio-based platform chemicals commercially viable in premium market segments before cost parity with petroleum-based routes is achieved.

Recent Developments:

-

2025: Corbion expanded its lactic acid and PLA precursor production capacity at its Thailand facility, targeting the rapidly growing Asia Pacific bioplastics market where single-use plastics regulations are driving demand for compostable packaging materials derived from lactic acid fermentation.

-

2025: Genomatica advanced commercial licensing of its bio-based butanediol production technology to additional partners, expanding the deployment of its engineered fermentation organism platform that converts glucose to bio-based BDO for polyurethane and spandex fibre applications.

-

2025: Avantium announced progress on its commercial-scale furandicarboxylic acid production facility, producing the bio-based PEF polymer precursor that offers superior oxygen barrier performance to conventional PET for food and beverage packaging applications.

-

2024: Evonik Industries expanded its bio-based amino acid production capacity for animal nutrition applications, leveraging its industrial fermentation expertise to increase production of bio-glutamic acid and bio-lysine from renewable feedstocks for sustainable animal feed ingredient markets.

-

2025: Gevo Inc. advanced its sustainable aviation fuel and bio-based isobutanol production programme, demonstrating the commercial viability of using bio-based platform chemical intermediates as precursors for renewable transportation fuels that command significant sustainability price premiums from aviation industry customers.

Bio-based Platform Chemicals Market Key Players

Some of the Bio-based Platform Chemicals Market Companies are:

-

BASF SE

-

Corbion N.V.

-

NatureWorks LLC

-

Evonik Industries AG

-

Cargill Incorporated

-

Braskem S.A.

-

Amyris Inc.

-

Genomatica Inc.

-

Gevo Inc.

-

Avantium N.V.

-

DuPont de Nemours Inc.

-

Archer-Daniels-Midland Company (ADM)

-

Novozymes A/S

-

DSM-Firmenich AG

-

PTT Global Chemical PCL

-

LG Chem Ltd.

-

Mitsubishi Chemical Corporation

-

Toray Industries Inc.

-

Total Energies Corbion (Joint Venture)

-

Futerro SA

Bio-based Platform Chemicals Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.09 Billion |

| Market Size by 2035 | USD 34.97 Billion |

| CAGR | CAGR of 6.81% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Bio-Glycerol, Bio-Succinic Acid, Bio-Itaconic Acid, Bio-Glutamic Acid, Bio-3-Hydroxypropionic Acid, Lactic Acid, Others) • By Feedstock (Sugars and Starch, Lignocellulosic Biomass, Vegetable Oils, Agricultural Residues, Others) • By Application (Polymers and Bioplastics, Pharmaceuticals and Nutraceuticals, Food and Beverages, Personal Care and Cosmetics, Agriculture, Industrial Chemicals, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE; Corbion N.V.; NatureWorks LLC; Evonik Industries AG; Cargill Incorporated; Braskem S.A.; Amyris Inc.; Genomatica Inc.; Gevo Inc.; Avantium N.V.; DuPont de Nemours Inc.; Archer-Daniels-Midland Company (ADM); Novozymes A/S; DSM-Firmenich AG; PTT Global Chemical PCL; LG Chem Ltd.; Mitsubishi Chemical Corporation; Toray Industries Inc.; Total Energies Corbion (Joint Venture); Futerro SA |

Frequently Asked Questions

Europe dominated the Bio-based Platform Chemicals Market in 2025, driven by the world's most comprehensive sustainability regulatory framework including the EU Chemical Strategy for Sustainability, European Green Deal, and EU Bioeconomy Strategy that collectively create the strongest regulatory pull for bio-based chemical adoption across multiple industrial market segments.

Lignocellulosic Biomass is expected to grow at the fastest feedstock CAGR through 2035.

Bio-Glycerol dominated the market in 2025 as the most commercially mature and widely deployed bio-based platform chemical, utilised across pharmaceuticals, personal care, food and beverage, and industrial applications, available at growing volumes and declining cost as a co-product of the expanding global biodiesel industry.

The Bio-based Platform Chemicals Market was valued at USD 18.09 billion in 2025.

The Bio-based Platform Chemicals Market is expected to grow at a CAGR of 6.81% from 2026 to 2035.

Get in Touch