Silica Market Report Scope & Overview:

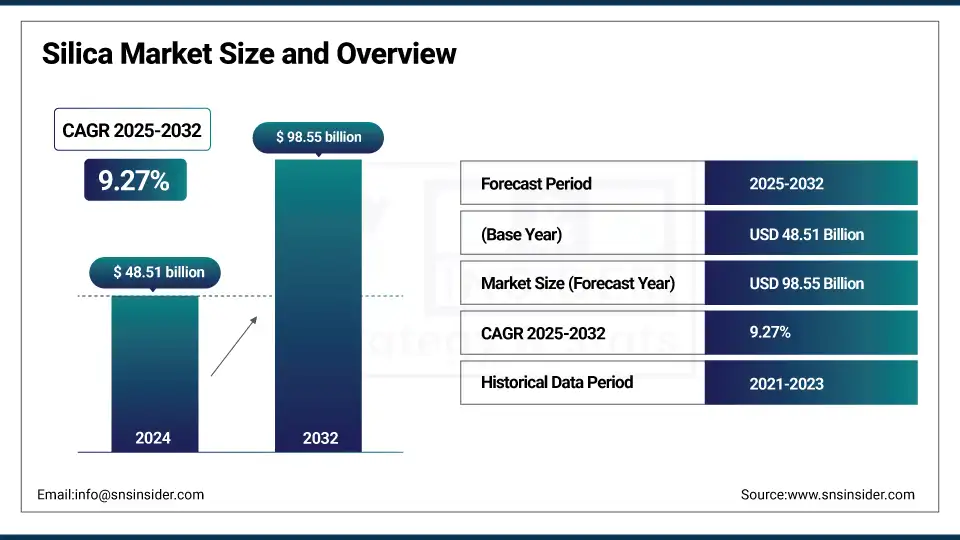

The Silica Market size was valued at USD 48.51 billion in 2024 and is expected to reach USD 98.55 billion by 2032, growing at a CAGR of 9.27% over the forecast period of 2025-2032.

Strong growth of the silica market is owing to the increased demand for industrial silica in hydraulic fracturing and a surge in the use of silica applications across the glass and ceramics industry. Green tire and lightweight composite sustainability initiatives are further molding silica market outlook, while innovations in electronics and 3D printing are reinforcing the silica market size. Silica companies are concentrating on innovation and expansion of production capacity to increase their silica market share and silica market size overall.

Market Size and Forecast:

-

Market Size in 2024: USD 48.51 Billion

-

Market Size by 2032: USD 98.55 Billion

-

CAGR: 9.27% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Silica Market - Request Free Sample Report

U.S. industrial silica consumption reached 120 million tons in 2023, an 11% increase over 2022, the U.S. Geological Survey reported. MSHA implemented tougher silica exposure standards in April 2024. It will also be increasing capacity for precipitated silica, in the amount of 50%, in Charleston, from 2026 on, which further confirming the on-going silica market assessment and strategy change made in the global silica market scene.

Silica Market Trends:

-

Rising demand from the construction industry for high-performance concrete and cement additives is significantly driving silica consumption.

-

Growing use of silica in glass manufacturing, especially for solar panels and automotive glass, is accelerating market growth.

-

Expanding rubber and tire manufacturing sectors are increasing the demand for precipitated silica to enhance fuel efficiency and durability.

-

Rapid industrialization and infrastructure development in emerging economies are strengthening bulk silica adoption.

-

Increasing applications in electronics, semiconductors, and specialty coatings are expanding high-purity silica demand.

-

Sustainability trends and innovations in eco-friendly and energy-efficient silica production technologies are shaping future market opportunities.

Silica Market Drivers:

-

Increasing hydraulic fracturing activities significantly boost industrial silica demand

Hydraulic fracturing continues to be one of the principal drivers of the silica market, as industrial silica is critical to the production of proppant used in hydraulic fracturing. Base on the U.S. Geological Survey, the apparent consumption of industrial sand and gravel (silica) in the U.S. reached 120 million tons in 2023, a rise of 11% on the year prior. This is because growth in the silica market largely operates on the energy activities of fracking, which in turn dictates silica market size and has even caused silica providers to increase silica production capabilities to meet energy market demands. This fashion indicates close positive relationship between energy exploitation and the usage of silica.

-

Rising demand for sustainable materials drives silica applications in green manufacturing

The silica market is in the midst of favoring sustainable materials including in the glass/ceramics industry and with green composites e.g. green tires. Industrial sand is primarily used in the production of glass which accounts for 26% of industrial sand use, while foundry sand has a much higher use of silica, specifically in cast iron and aluminum production. Silica suppliers are increasing production of their precipitated and colloidal silica to provide materials optimized for sustainability driven markets. This transition mirrors silica market dynamics that continue to evolve based on environmental drivers with resulting impact on product innovation and size of the silica market all around including automotive and construction.

Silica Market Restraints:

-

Environmental and zoning restrictions limit expansion opportunities for silica production

Domestic zoning laws and environmental regulations limit the development of new silica mines in North America. The U.S. Geological Survey says some areas where silica sand is mined have imaging problems or land use restrictions because of local ecosystems and community opposition. BenToshi’s restrictions obstruct silica companies’ potential to expand industrial silica production and, as such, constrain the increase of the market size for silica and the pace of market share penetration into key geographies, such as the Midwest. This is a regulatory environment that will pose substantial barriers to any ramp up in future capacity.

Silica Market Segmentation Analysis:

By Product

Precipitated silica held a 38% silica market share in 2024, making it the dominant product type, driven by its extensive use in green tires and oral care products. Evonik and PPG Industries have both expanded their precipitated silica manufacture considerably due to increasing demand in the automotive industry. Since silica improves rolling resistance, European Automobile Manufacturers Association The use of silica in tires allows fuel savings, and that goes to the ground of global warming. Such a move will significantly drive the silica market and will augment the demand for sustainable silica products.

Precipitated silica is projected to grow at a CAGR of 9.87% between 2025 and 2032, emerging as the fastest-growing segment. The demand is driven by its wide use in environmentally friendly tires, toothpaste and food defoamers. Silica companies like Solvay and Evonik are investing significant amounts to expand capacity in the face of green material demand. This is in line with the latest trends of silica and sustainability requirements that Europe and North America have been demanding, resulting in accelerating growth of the silica market and its application and usage in multiple sectors.

By Form

Crystalline silica dominated the silica market with a 53.5% share in 2024, primarily due to its use in the glass and ceramics industry. Flat glass, solar and container glass continue to drive demand for high-purity silica sand. An increase in industrial silica for solar glass is emphasized by the U.S. Geological Survey as a product of the Inflation Reduction Act. This extensive use, especially in clean energy infrastructure, is why crystalline silica’s market position continues, and the importance of the inclusion of crystalline silica for evaluating the silica market globally.

Amorphous silica is expected to grow at a CAGR of 9.39% from 2025 to 2032, driven by its expanding use in lithium-ion batteries, coatings, and 3D printing. Solvay and Wacker Chemie launch R&D into battery-grade amorphous silica materials. Worldwide production of electric vehicles is increasing and the need for safer, better performing additives is growing. This is indicative of a momentum in silica market trends toward advanced, functional for high-purity materials, driving growth in the silica market overall through new and sustainable silica application.

By End-use Industry

Glass manufacturing led the silica market in 2024 with a 32.4% market share, supported by strong demand for architectural glass and solar panel substrates. Silica is a key component of glass, and when used in high purity grades it provides optimal clarity and strength. The National Renewable Energy Laboratory found that more silica-based glass was needed as solar panel deployment skyrocketed. This demand surge underlines silica’s place in industrial silica applications and how it is more fundamental than other materials, in the rise of energy-efficient and renewable technologies.

Building and construction is projected to grow at a CAGR of 9.67% during 2025–2032, making it the fastest-growing end-use industry. Demand for silica-enhanced concrete, insulation panels, and lightweight mortars is rising due to green building mandates. According to the U.S. Department of Energy, federal projects increasingly use silica-based materials for thermal performance. This sector’s growth highlights changing silica market trends and underlines silica market share expansion across infrastructure projects promoting sustainability and energy efficiency in modern construction.

Silica Market Regional Analysis:

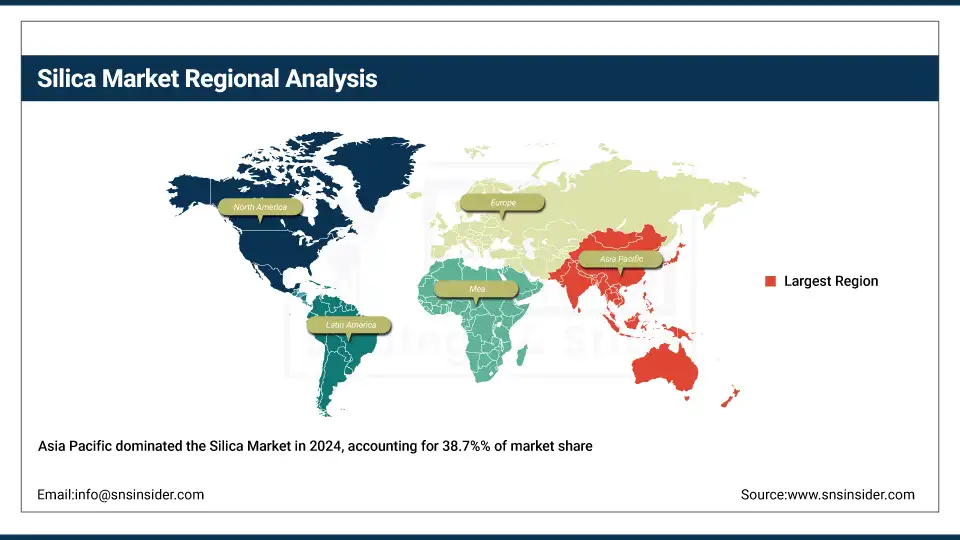

Asia Pacific dominated the silica market with a 38.7% share in 2024 and is the fastest-growing region through 2032 with the highest CAGR of 9.58%. China's dominance stems from massive glass production, solar panel exports, and electronics manufacturing, while India supports silica market growth via smart city projects and industrial infrastructure. Government-backed initiatives like China’s “New Infrastructure Plan” and India’s PMAY (Housing for All) fuel silica market trends. Asia Pacific’s expanding silica applications in solar glass and semiconductors continue to drive regional silica market size and industrial silica output.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America held a 21.5% silica market share in 2024, driven by widespread use of industrial silica in hydraulic fracturing and specialty glass manufacturing. According to the U.S. Geological Survey, the U.S. consumed 120 million tons of industrial sand and gravel in 2023, with over 80% used for oil and gas fracking. The United States, led by states like Texas and Wisconsin, dominates regional production. These silica applications sustain silica market growth, supported by ongoing infrastructure upgrades and the growing glass and ceramics industry.

Europe accounted for a 24.3% silica market share during the 2025–2032 forecast period, propelled by eco-friendly infrastructure and strong demand in the glass and ceramics industry. Countries like Germany and France are advancing silica applications in architectural glass and insulation through EU Green Deal policies. Silica companies are scaling up sustainable production to meet emission reduction goals. This regional silica market growth aligns with Europe’s transition toward low-carbon construction, reinforced by stringent building regulations and a rising preference for industrial silica in energy-efficient materials.

Latin America is witnessing steady silica market growth, supported by Brazil and Argentina’s construction, agriculture, and glass industries. Local silica companies are increasing output for water filtration and lightweight glass applications, contributing to regional silica market share. Brazil’s construction sector, projected to expand under national housing programs like “Casa Verde e Amarela,” is encouraging silica applications in cement and tiles. Additionally, regional demand for agrochemical-grade silica is rising, reinforcing silica market trends across Latin America’s industrial silica landscape.

The Middle East & Africa is projected to be the fastest-growing silica market from 2025 to 2032, with increasing demand from construction and solar industries. Saudi Arabia’s NEOM project and the UAE’s clean energy expansion are boosting silica applications in smart glass and concrete. The region’s silica market analysis highlights government infrastructure investments and economic diversification efforts as key drivers. South Africa leads in quartz silica mining, supplying the local glass and ceramics industry. These factors collectively enhance silica market size and market share regionally.

Key Players:

The major silica market competitors include Evonik Industries AG, Wacker Chemie AG, PPG Industries Inc., Cabot Corporation, Imerys S.A., Solvay SA, W.R. Grace & Co., Sibelco, US Silica, and Madhu Silica Pvt. Ltd.

Recent Developments:

-

In December 2024, Mitsubishi Chemical Group expanded its synthetic silica powder capacity in Japan to support semiconductor packaging demand, incorporating automation and sustainability measures.

-

In November 2024, NGT directed CPCB to draft nationwide silica mining guidelines to address environmental concerns and regulate operations sustainably in states like Uttar Pradesh.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 48.51 billion |

| Market Size by 2032 | USD 98.55 billion |

| CAGR | CAGR of 9.27% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Fumed, Precipitated, Colloidal, Fused Silica, Silica Gel, Others) •By Form (Amorphous, and Crystalline) •By End-use Industry (Building & Construction, Oil & Gas, Glass Manufacturing, Water Treatment, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Evonik Industries AG, Wacker Chemie AG, PPG Industries Inc., Cabot Corporation, Imerys S.A., Solvay SA, W.R. Grace & Co., Sibelco, US Silica, and Madhu Silica Pvt. Ltd. |

Frequently Asked Questions

Environmental regulations and land-use restrictions are limiting silica production and expansion opportunities.

Asia Pacific is dominating and the fastest-growing region, led by China and India.

Key silica companies include Evonik, Wacker Chemie, PPG, Cabot, Imerys, Solvay, and US Silica.

Hydraulic fracturing, glass and ceramics, green tires, and 3D printing are fueling silica market demand.

The silica market size in 2024 was valued at approximately USD 48.51 billion globally.

Get in Touch