Bioplastics & Biopolymers Market Report Scope & Overview:

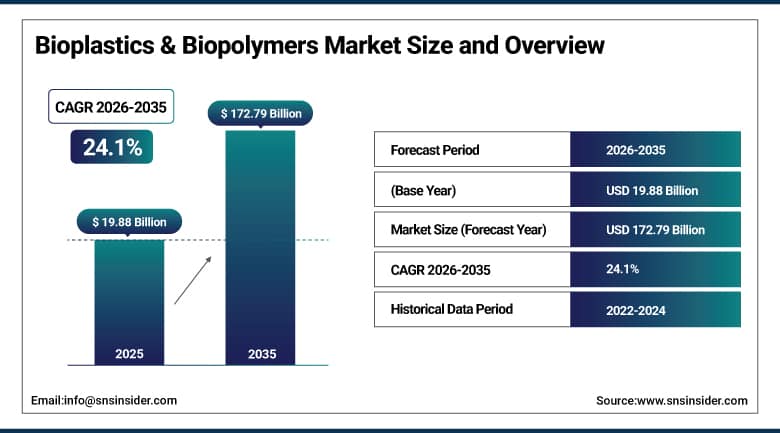

The Bioplastics & Biopolymers Market was valued at USD 19.88 billion in 2025 and is expected to reach USD 172.79 billion by 2035, growing at a CAGR of 24.1 % from 2026-2035.

Bioplastics & Biopolymers are the names for advanced green technologies based on renewable biological sources such as corn starch, sugar cane, cellulose, vegetable oils, and microbial fermentation processes. Different from the traditional plastics derived from petroleum chemicals, these materials can either be bio-derived or biodegradable or even both types. Polylactic acid (PLA), polyhydroxyalkanoates (PHA), bio-based polyethylene, and starch-based blends are some of the examples of biopolymers, which are now extensively employed as the alternative materials to plastics in various industries, such as packaging, agriculture, automotive, textile, and healthcare.

The market for bioplastics & biopolymers is experiencing tremendous growth worldwide, mainly because of the increasing consciousness about environmental pollution, accumulation of plastic wastes, and stringent government regulations regarding sustainable raw materials. Packaging still remains the major end-use sector, particularly for food and beverages packing applications. In the automotive industry, the application of bioplastics in automobile interiors helps in enhancing the efficiency and reducing the weight of cars.

Regulations regarding the use of single-use plastics and the promotion of carbon neutral technologies have increased the attractiveness of the technology. Currently, the region of Europe is at the forefront in the sector owing to strict plastic policies in the EU and high sustainability levels. In contrast, the regions of North America have been driven by Environmental Social Governance practices in corporations alongside bio-plastic developments. The region of Asia Pacific has been on the rise due to availability of agricultural resources which are useful in manufacturing along with growing manufacturing processes. However, challenges such as high costs of production, absence of industrial compost facilities and low efficiency have hindered the usage of this technology.

Market Size and Forecast

-

Market Size in 2025: USD 19.88 Billion

-

Market Size by 2035: USD 172.79 Billion

-

CAGR: 24.1% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Bioplastics & Biopolymers Market - Request Free Sample Report

Bioplastics & Biopolymers Market Trends

-

The rapid switch to compostable and biodegradable polymers as an alternative due to worldwide prohibitions against single-use plastics and increasing sustainability measures in many major economies.

-

The increased adoption of bio-based polymers such as PLA and PHA for use in packaging solutions, agriculture, and consumer use due to improved scalability and performance properties.

-

Extensive adoption of bio-based polymers in automotive applications in a bid to lower vehicle emissions for boosting the fuel efficiency, especially when used in non-structural applications.

-

Greater investment and research into fermentation and bio-refining processes for increasing efficiency and decreasing production costs.

-

Increased efforts towards the creation of a circular economic system. This would then encourages the growth of industrial composting facilities and closed-loop recycling systems for bio-based materials.

-

The growing demand for health-care applications of bio-based polymers, such as biodegradable sutures, implants, and drug-delivery devices. This is due to biocompatibility.

-

The rising demand for bio-based polymers due to the increasing pressure from companies' for ESG goals and sustainability reporting requirements.

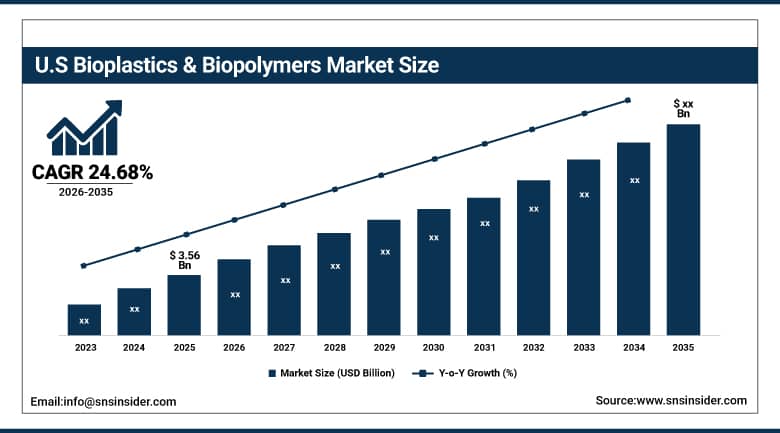

The U.S. Bioplastics & Biopolymers Market was valued at USD 3.56 billion in 2025 and is expected to grow at a CAGR of 24.68 % from 2026-2035.

One of the prominent markets for the Bioplastics & Biopolymer industry is the US, owing to the advanced industrial base in the country and the high demand for plastics in the packaging, automobile, pharmaceutical, and consumer goods sectors. The increasing consciousness among consumers about environmental issues and the focus on sustainability efforts has been encouraging the production of plastic manufacturers to shift their production from traditional plastics to bio-based and biodegradable polymers such as PLA, PHA, and bio-based polyethylene.

One of the key strengths of the US market is the existence of leading chemical companies, such as Dow Inc., DuPont, NatureWorks LLC, Corbion, and Cargill, with active investment into large-scale bio-based polymer manufacturing and improving the properties of the products. The activities of regulatory agencies, such as the EPA and FDA, as well as the prohibition of single-use plastics in certain US states, also stimulate the transition to sustainable solutions.

Focus on circular economy principles and development of the composting capacity can be named as other factors driving the market. High cost of bioplastic production and limited access to composting plants are considered weak points of the market. Nevertheless, a robust R&D sphere and growing demand will help to drive market growth.

Bioplastics & Biopolymers Market Segment Analysis

-

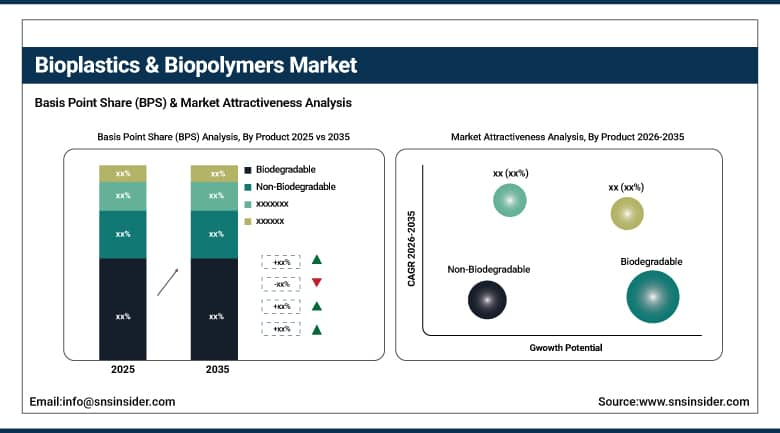

By Product, Bio-Based Plasticizers held the largest market share in 2025

-

By Application, Agriculture & Horticulture held the largest market share, around 34%, in 2025.

By Product: Bio-Based Plasticizers dominates the market

The segment of Bio-Based Plasticizers accounted for a large market share of about 68% in 2025. This was because of the growing importance being placed on sustainable waste management and reducing pollution globally. The use of biodegradable plastics that are created using renewable resources, such as corn starch, sugarcane, and cellulose, has been advantageous because they decompose naturally in a composting environment. Therefore, there is little chance of pollution from landfills or oceans, considering that these plastics do not harm the environment. Moreover, high demands from several industries, such as the packaging, agricultural, and consumer goods industry, along with the increased focus on developing affordable biodegradable plastics, have made a significant contribution to its dominance.

By Application: Agriculture & Horticulture dominates the market

Agriculture & Horticulture was the largest segment with almost 34% market share in 2025. This can be attributed to the rising requirement for sustainable farming practices and environmentally friendly farming inputs. Mulch films, plant pots, seed coatings, and greenhouse films are some common applications of bioplastics and biopolymers that offer numerous advantages including biodegradation and improved soil quality. The use of biodegradable mulch films by farmers has gained momentum to reduce the process of removing plastic film waste in order to save on labor expenses. In addition to this, government policies in regions such as Europe and North America favoring biodegradable agricultural products have contributed to the growth of this segment. Innovations in materials have also played an important role in improving the resilience of bioplastics for outdoor applications. Thus, a rising interest in sustainable agriculture and environmental conservation worldwide make Agriculture & Horticulture one of the biggest end-use markets.

Bioplastics & Biopolymers Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

35% |

|

North America |

United States |

69% |

|

Europe |

Germany |

33% |

|

Middle East & Africa |

Saudi Arabia |

34% |

|

Latin America |

Brazil |

52% |

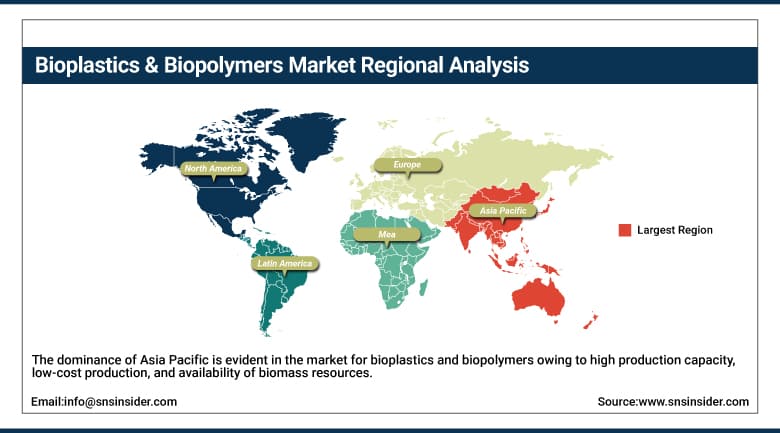

Asia Pacific Bioplastics & Biopolymers Market Insights

The dominance of Asia Pacific is evident in the market for bioplastics and biopolymers owing to high production capacity, low-cost production, and availability of biomass resources. China accounts for most of the regional demand, backed by high production of packaging materials, growing consumer goods industry, and use of biodegradable plastics. Growing government initiatives towards plastic waste management and increasing environmental awareness are other factors boosting the market.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Bioplastics & Biopolymers Market Insights

North America represents a region which embraces innovation, and the United States is one of the leading nations in terms of demands made within the region. Market growth in the industry can be attributed to the strong R&D activities carried out in bio-materials, companies' sustainability strategies, and application in packaging, automotive, and health care sectors.

Europe Bioplastics & Biopolymers Market Insights

Europe has robust adoption driven by regulation, and Germany is one of the major markets. Regulations related to single-use plastics and environment have fueled the demand for bio-polymers. With sophisticated chemical manufacturing processes and circular economy policies, Europe continues to grow at a stable rate.

MEA and Latin America Bioplastics & Biopolymers Market Insights

MEA is a developing market, which leads the market in terms of diversification to sustainable products, with Saudi Arabia at the forefront of the growth. The growth is spurred on by development within industry and environmental sustainability projects.

Latin America is headed by Brazil, due to abundant agricultural feedstock and growing biodegradable packaging market demand. Growth is encouraged by growing environmental awareness and regulation.

Bioplastics & Biopolymers Market Growth Drivers:

-

Rising environmental regulations and single-use plastic bans accelerating Bioplastics & Biopolymers market adoption globally.

The market of Bioplastics & Biopolymers is propelled by growing environmental consciousness, stringent laws against single use plastic products, and rising inclination towards sustainable and renewable materials. Regulatory bodies in various countries have enforced a ban on usage of plastics, which is promoting the use of biodegradable and bio-based plastic products in packaging, agricultural, automotive, and healthcare industries. Growing consumer preferences for eco-friendly products are compelling companies to utilize bioplastics instead of conventional oil-based plastic products. Additionally, innovation and technology developments are improving the quality and performance of biopolymer materials. Applications of bioplastic materials in packaging of foods, development of medical devices, and manufacturing of lighter automobiles are contributing towards robust growth of the market around the globe.

Bioplastics & Biopolymers Market Restraints:

-

High production costs compared to conventional plastics limiting large-scale commercial adoption.

Although it shows promising future growth, the Bioplastics & Biopolymers industry has some restrictions. Firstly, the expensive manufacturing process is a drawback that hinders its adoption over more affordable plastic materials. Secondly, scarcity of industrial composting and recycling infrastructure renders biodegradable polymers ineffective. Inadequate performance characteristics like poor thermal resistance and mechanical properties impede their application in high-strength and durable items. Moreover, the dependency on crops makes biopolymer prices highly volatile. Incompatibility with the current waste management system makes sorting, collecting, and recycling harder. Absence of adequate consumer knowledge on disposal processes further hampers its environmental advantages. Lastly, the lack of regulations on an international scale poses difficulties for the implementation of a unified biopolymer solution.

Bioplastics & Biopolymers Market Opportunities:

-

Expansion of circular economy initiatives creating strong demand for bio-based and compostable plastics globally.

A number of drivers make the market opportunities for Bioplastics & Biopolymers appear promising. These include initiatives by organizations on circular economy, awareness by consumers about green materials. Furthermore, the improvements in technology in terms of fermentation and synthetic biology processes have increased the productivity levels, leading to reduced costs. There are growing usages in the form of food packaging that is compostable due to the rise of food delivery services and e-commerce. There has been growing usage in the agricultural industry through mulch films and coatings to improve soil conditions while reducing plastic contamination. There is rapid innovation within the health care industry due to the biocompatibility of the materials. In addition, there are promising opportunities in the automotive industry especially for electric cars and other emerging economies.

Recent Developments:

-

2025: NatureWorks LLC expanded its PLA (polylactic acid) capacity to meet rising global demand from packaging and food service industries, strengthening supply of low-carbon bioplastics used in compostable applications.

-

2026: Corbion enhanced PLA-based material performance for high-heat packaging and industrial compostable applications, improving durability and commercial usability in food packaging systems.

-

2025: BASF advanced its biomass balance approach, replacing fossil feedstocks with renewable raw materials to reduce carbon footprint in engineering plastics and expand sustainable polymer offerings for automotive and packaging sectors.

Bioplastics & Biopolymers Market Key Players

-

NatureWorks LLC

-

Braskem S.A.

-

BASF SE

-

Novamont S.p.A.

-

DuPont de Nemours Inc.

-

Arkema S.A.

-

Mitsubishi Chemical Group Corporation

-

Eastman Chemical Company

-

Toray Industries Inc.

-

Evonik Industries AG

-

Solvay S.A.

-

Avantium N.V.

-

Biome Bioplastics Limited

-

FKuR Kunststoff GmbH

-

Plantic Technologies Limited

-

Futerro S.A.

-

CJ CheilJedang Corporation

-

Saudi Basic Industries Corporation (SABIC)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.88 Billion |

| Market Size by 2035 | USD 172.79 Billion |

| CAGR | CAGR of 24.1% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Biodegradable, Non-Biodegradable) • By Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive & Transportation, Coatings & Adhesives) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NatureWorks LLC, Braskem S.A., BASF SE, TotalEnergies Corbion, Novamont S.p.A., DuPont de Nemours Inc., Arkema S.A., Mitsubishi Chemical Group Corporation, Eastman Chemical Company, Toray Industries Inc., Evonik Industries AG, Solvay S.A., Danimer Scientific Inc., Avantium N.V., Biome Bioplastics Limited, FKuR Kunststoff GmbH, Plantic Technologies Limited, Futerro S.A., CJ CheilJedang Corporation, Saudi Basic Industries Corporation (SABIC) |

Frequently Asked Questions

Ans: The Bioplastics & Biopolymers Market is expected to grow at a CAGR of 24.68 % from 2026 to 2035.

Ans: Bio-Based Plasticizers dominated the bioplastics & Biopolymers market due to the increasing global emphasis on sustainable waste management and reducing environmental pollution.

Ans: Agriculture & Horticulture held the largest market share. It is due to the increasing demand for sustainable farming practices.

Ans: Asia Pacific dominated; North America and Europe hold significant positions.

Ans: The Bioplastics & Biopolymers Market was valued at USD 19.88 billion in 2025.

Get in Touch