Blood Pressure Monitors Market Report Scope & Overview:

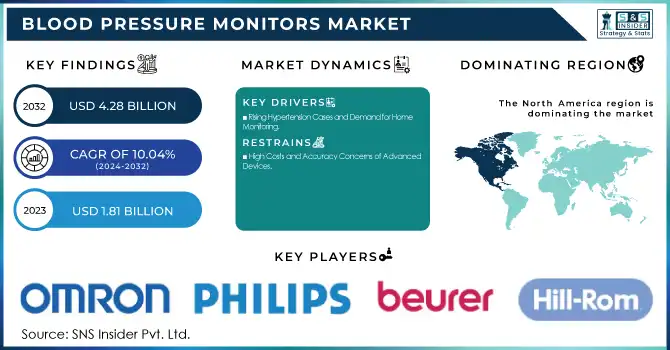

The Blood Pressure Monitors Market size is estimated at USD 1.81 Billion in 2023 and is expected to reach USD 4.28 Billion by 2032 and grow at a CAGR of 10.04% over the forecast period of 2024-2032.

This report points out the increasing prevalence and incidence of hypertension, driving demand for convenient and accurate monitoring devices. The research analyzes prescription and usage patterns of blood pressure monitors by region, indicating differences in healthcare infrastructure and consumer attitudes. It also delves into sales volume trends, examining regional demand and supply patterns and the effects of digital health and AI-based innovations that improve device precision, connectivity, and remote monitoring. The report also evaluates the increasing use of smart BP monitors, the effect of e-commerce on product availability, and the trend toward preventive healthcare solutions.

Blood Pressure Monitors Market Size and Forecast:

-

Market Size in 2023: USD 1.81 Billion

-

Market Size by 2032: USD 4.28 Billion

-

CAGR: 10.04% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

Get More Information on Blood Pressure Monitors Market - Request Sample Report

Blood Pressure Monitors Market Trends

-

Rising global prevalence of hypertension, cardiovascular diseases, and lifestyle-related disorders is significantly increasing demand for regular blood pressure monitoring solutions across homecare and clinical settings.

-

Growing awareness regarding preventive healthcare and early diagnosis is driving adoption of digital and automated blood pressure monitors for routine self-monitoring.

-

Technological advancements such as wearable blood pressure monitors, Bluetooth-enabled devices, and smartphone-integrated monitoring systems are enhancing real-time tracking and remote patient management.

-

Increasing demand for home healthcare devices, particularly among the geriatric population, is accelerating market growth due to convenience, affordability, and reduced hospital visits.

-

Expansion of telehealth services and remote patient monitoring programs is supporting integration of connected blood pressure devices into digital health ecosystems.

-

Government initiatives and public health campaigns focused on hypertension screening and cardiovascular risk reduction are strengthening market penetration in both developed and emerging economies.

-

Continuous product innovations, including cuff-less monitoring technologies and AI-enabled analytics for predictive risk assessment, are shaping the future of the blood pressure monitors market.

Blood Pressure Monitors Market Drivers

-

Rising Hypertension Cases and Demand for Home Monitoring

Hypertension has emerged as a global health problem, with more than 1.28 billion adults affected, as indicated by the World Health Organization. Yet, only 42% of them are diagnosed and under treatment, as reported by WHO, showing that there is a large gap in hypertension care. The increasing burden drove the need for self-monitoring blood pressure instruments, especially digital and wearable BP monitors, which allow the population to monitor blood pressure with ease at home. Patients increasingly prefer home healthcare options, which provide affordable, user-friendly, and dependable options for repeated visits to clinics.

The growth of artificial intelligence and the Internet of Things in the healthcare sector has also spurred the use of advanced BP monitors. Intelligent BP devices now provide instant monitoring, cloud storage, and compatibility with mobile health apps, enabling easy sharing of readings with medical professionals. This not only enhances the management of disease but also aids in the early detection of anomalies, minimizing the likelihood of complications like stroke and heart failure. Industry leaders like Omron Healthcare and Withings are driving innovation here, with cuffless and wearable BP monitors and AI-powered analytics. As people become more aware of preventive healthcare, the need for intelligent, connected, and AI-based BP monitors will rise, transforming the landscape of managing hypertension.

Blood Pressure Monitors Market Restraints

-

High Costs and Accuracy Concerns of Advanced Devices

The affordability of high-end BP monitors, especially wearable and AI-based ones, is a primary deterrent, cutting down access to lower-income households. Secondly, the accuracy and reliability of BP monitors based on wrists and smartwatches have raised concerns among healthcare workers, prompting skepticism regarding misdiagnosis. Variation in readings with motion artifacts or incorrect cuff fitting has also triggered skepticism regarding product effectiveness. Regulatory clearance for new BP monitoring technology can be protracted, and market entry may be delayed.

Blood Pressure Monitors Market Opportunities

-

The rise of wearable blood pressure monitors and AI-driven diagnostics presents a significant growth opportunity.

Players such as Omron Healthcare and Withings have launched cuffless BP monitoring solutions, which attract technology-driven consumers. The convergence of remote patient monitoring (RPM) with telemedicine platforms is opening doors for chronic disease management. Further, government programs for preventive healthcare and digital health solutions will continue to fuel innovation and adoption in the space.

Blood Pressure Monitors Market Challenges

-

Stringent regulatory approvals and compliance requirements for medical devices pose a challenge for market players.

Organizations such as the FDA and CE have stringent regulations to guarantee device accuracy and safety, resulting in longer approval times. Furthermore, the use of cloud-based and AI-powered BP monitors poses data security and patient privacy concerns. The threat of cyber-attacks and unauthorized access to health information is a persistent challenge that necessitates strong cybersecurity practices from device manufacturers.

Blood Pressure Monitors Market Segmentation Insights

By Product

In 2023, the devices segment held 75% of the overall market share and was the leading category in the blood pressure monitors market. This is largely due to the high usage of digital and automated BP monitors in clinical and homecare applications. The rising incidence of hypertension, increasing awareness of self-monitoring, and the inclusion of AI and smart connectivity features have also driven demand. Apart from this, hospitals and clinics also heavily depend on upper arm and wrist monitors for accurate and reliable readings, further boosting the segment's high market share.

The accessories segment will see considerable growth over the years, with driving forces being enhanced demand for spares such as replacement cuffs, batteries, and calibration tools. Increasing focus on maintenance of the device, accuracy, and increasing product life has seen sales rise in accessories. Also, there is increased usage of home care healthcare and telemedicine services driving up the requirement for spare parts and consumables. Increased demand for multi-user BP monitors by home and clinic consumers has also contributed to higher demand for accessories.

By End-user

The home healthcare segment controlled 60% of the market in 2023 and is the largest end-user category. The trend is fueled by increasing cases of hypertension, combined with a growing trend toward self-monitoring and preventive care. Ease of use of digital BP monitors, advancements in telehealth services, and better affordability have further boosted adoption. Also, the growth in more people living at home with chronic conditions has further helped the segment dominate the market.

The other segment, encompassing ambulatory surgical centers, pharmacies, and corporate wellness programs, is anticipated to see the highest growth. The increase in workplace wellness programs, mobile health screenings, and retail healthcare services has fueled demand in this segment. In addition, more pharmacies providing BP monitoring services and the growth of telemedicine-based hypertension management have helped the segment grow at a high rate. The ease of having on-the-spot BP readings taken in non-traditional healthcare environments is a major driver behind the growth of this segment.

Blood Pressure Monitors Market Regional Analysis

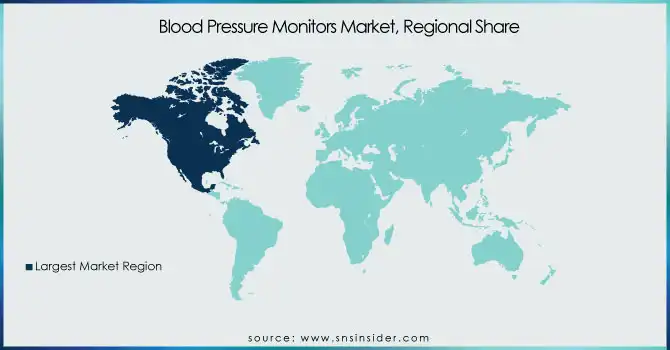

The North American region led the world in the blood pressure monitors market in 2023 due to the prevalence of high hypertension, sophisticated healthcare infrastructure, and rising use of home healthcare equipment. The United States has the highest market share, aided by government policies, reimbursement schemes, and the surge in demand for remote patient monitoring solutions. Furthermore, the concentration of major players like Omron Healthcare and GE Healthcare also bolsters market expansion in the region.

Europe is the second-largest market, with the UK, Germany, and France taking the lead owing to increased awareness regarding preventive healthcare and the well-established medical device market. Increasingly aging populations and high diagnosis rates for cardiovascular diseases are major growth drivers. Government-sponsored healthcare programs and positive regulatory policies also drive the adoption of BP monitors in clinics and homes.

The Asia-Pacific area is projected to experience the fastest growth due to the growing rate of hypertension, rising healthcare expenditures, and broadening availability of medical devices. China, Japan, and India are the contributing countries owing to their size and rising self-monitoring awareness. Wearable and smart blood pressure monitors are becoming increasingly in demand in this area, driven by digital health advancements.

Need any customization research on Blood Pressure Monitors Market - Enquiry Now

Blood Pressure Monitor Market Key Players

-

Omron Healthcare – Evolv, Platinum, Gold, Silver, 7 Series, 10 Series, 3 Series

-

Hill-Rom Holdings, Inc. (Welch Allyn, Inc.) – Connex ProBP 3400, Spot Vital Signs 4400, Home BP Monitor

-

Nihon Kohden Corporation – Life Scope G5, Life Scope SVM Series

-

Koninklijke Philips N.V. (Philips Healthcare) – IntelliVue MP Series, SureSigns VS Series

-

Masimo – Rad-97, MightySat Rx with BP Monitoring

-

Beurer GmbH – BM 26, BM 28, BM 55, BM 85

-

GE Healthcare – Dinamap ProCare Series, Carescape V100

-

American Diagnostic Corporation – Diagnostix 700 Series, Prosphyg 775

-

SunTech Medical, Inc. – Tango M2, CT40, Oscar 2

-

A&D Medical Inc. – UA-651, UA-767, UA-1030T

-

Withings – BPM Connect, BPM Core

-

Briggs Healthcare – HealthSmart Standard, HealthSmart Premium

-

Kaz Inc. – SmartTemp BP Monitors

-

Microlife AG – BP A6 BT, BP B3 AFIB, BP W3 Comfort

-

Rossmax International Ltd. – X5, X9, S150

-

GF Health Products Inc. – Lumiscope 1143, 1145, 1147

-

Spacelabs Healthcare Inc. – OnTrak Ambulatory BP Monitor

-

B. Braun SE – Vista 120, Vista BP Monitoring Systems

Recent Developments

In Jan 2025, Novosound showcased the world's first ultrasound-based continuous blood pressure monitoring wearable at CES 2025, marking a breakthrough in the BP monitoring market. CEO Dave Hughes emphasized that ultrasound technology is the key to achieving real-time, non-invasive BP tracking, addressing a critical need in healthcare.

In Nov 2024, OMRON Healthcare received FDA De Novo authorization for its new AI-powered blood pressure monitors with IntelliSense AFib detection, marking a breakthrough in home monitoring by integrating machine learning for atrial fibrillation detection, a major stroke risk factor.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.81 Billion |

| Market Size by 2032 | USD 4.28 Billion |

| CAGR | CAGR of 10.04% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product [Devices (Sphygmomanometer, Digital BP Monitors, Ambulatory BP Monitors), Accessories (Blood Pressure Cuffs, Transducers, Others)] • By End-user [Hospitals & Clinics, Home Healthcare, Others] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Omron Healthcare, Hill-Rom Holdings (Welch Allyn), Nihon Kohden Corporation, Koninklijke Philips N.V. (Philips Healthcare), Masimo, Beurer GmbH, GE Healthcare, American Diagnostic Corporation, SunTech Medical, A&D Medical, Withings, Briggs Healthcare, Kaz Inc., Microlife AG, Rossmax International, GF Health Products, Spacelabs Healthcare, B. Braun SE. |

Frequently Asked Questions

Ans. The key drivers are rise in the people suffering from hypertension.

Ans. Asia Pacific is the fastest growing region of the Blood Pressure Monitors Market.

Ans. The major key players are Omron Healthcare, Hill-Rom Holdings, Koninklijke Philips, Beurer GmbH, GE Healthcare, American Diagnostic Corporation, SunTech Medical

Ans. The Blood Pressure Monitors Market was valued at USD 1.81 Billion in 2023 and is estimated to reach USD 4.28 Billion by 2032 with a growing CAGR of 10.04% over the forecast period of 2024-2032.

Ans. The Compound Annual Growth rate for Blood Pressure Monitors Market over the forecast period is 10.04%.

Get in Touch